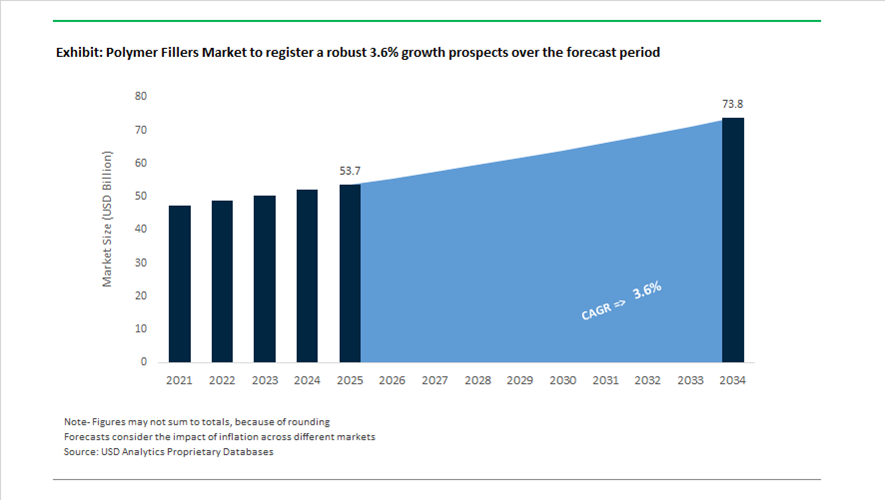

Polymer Fillers Market Size 2025–2034: $53.7 Billion to $73.8 Billion at 3.6% CAGR Driven by Lightweighting, Circular Feedstocks, and Functional Reinforcement

The global polymer fillers market is projected to expand from $53.7 billion in 2025 to $73.8 billion by 2034, reflecting a CAGR of 3.6%. Growth is anchored in construction materials, automotive lightweighting, electrical insulation, packaging durability, and specialty conductive plastics. Mineral fillers such as calcium carbonate, kaolin, talc, diatomite, perlite, hollow glass microspheres, carbon black, and carbon nanotubes (CNTs) remain central to polymer cost optimization and performance enhancement. However, the market is increasingly defined by functional differentiation—thermal stability, conductivity, flame retardancy, density reduction, and sustainability metrics—rather than volume alone.

Strategic consolidation is reshaping supply depth and mineral access. In June 2024, J.M. Huber Corporation acquired Active Minerals International, strengthening its kaolin and attapulgite filler portfolio for industrial polymers and construction compounds. Earlier, in April 2024, Huber Engineered Materials acquired Natrium Products, adding specialty sodium bicarbonate technologies used as functional fillers and foaming agents in lightweight polymer structures. These acquisitions position Huber to deliver engineered mineral systems tailored for mechanical reinforcement and density control in high-load plastic formulations.

Sustainability and circular feedstocks are now competitive differentiators. In late 2024, Cabot Corporation launched REPLASBLAK® black masterbatches, certified under ISCC PLUS, using circular raw materials such as tire pyrolysis oil. The technology reduces product carbon footprint (PCF) while preserving conductivity and tint strength. In September 2025, Cabot formalized its 2030 sustainability roadmap, targeting a 5–10% reduction in average PCF across its specialty carbons portfolio—an initiative aligned with EU carbon disclosure standards and OEM decarbonization mandates. Price realignments implemented in December 2024 underscore the rising capital requirements for environmental upgrades and advanced processing.

Distribution and integration strategies are also evolving. In September 2025, Omya introduced Omya Performance Polymer Distribution (OPPD), integrating Distrupol’s thermoplastics network with Omya’s mineral filler supply chain. This unified model enables customized filler-polymer compound packages for mobility and healthcare applications. At the same K 2025 exhibition, Omya unveiled the Omyasphere 900 hollow glass microspheres, engineered for aerospace and electric vehicle composites where density reduction directly enhances energy efficiency.

In Latin America, Imerys expanded its regional footprint in January 2025 through the acquisition of a Brazilian diatomite and perlite business. These fillers provide lightweighting and thermal insulation advantages for automotive and construction plastics, reinforcing Imerys’ specialty mineral platform.

Advanced conductive and high-performance polymer fillers are gaining traction in electronics and EV systems. In mid-2024, Polyplastics launched Duramid PA6X G 30 HF BK159D, a CNT-filled polyamide engineered for electrostatic discharge protection in sensitive electronic assemblies. Meanwhile, Evonik doubled long-chain polyamide capacity in Shanghai in November 2025, expanding access to filler-compounded VESTAMID® grades for chemically resistant automotive and new energy vehicle components.

Structural Market Trends and High-Value Growth Opportunities in the Polymer Fillers Market

Strategic Shift from Commodity Fillers to Engineered Multi-Functional Additives

The polymer fillers market is undergoing a structural upgrade as processors move away from untreated Ground Calcium Carbonate and low-value mineral extenders toward engineered fillers that deliver mechanical, thermal, and processing advantages simultaneously. This shift is not cosmetic. It is driven by OEM pressure to reduce resin consumption, lower carbon intensity, and improve part performance without increasing formulation complexity or cost volatility. Engineered solutions such as Precipitated Calcium Carbonate, surface-treated talcs, and high-aspect-ratio mineral systems are increasingly positioned as functional replacements for elastomers, impact modifiers, and even higher-cost polymers.

In 2025, Imerys introduced its GeoMax™ engineered GCC platform at the K-Show, specifically designed to push mineral loading beyond traditional thresholds while preserving surface finish and melt flow. By enabling higher filler incorporation without sacrificing processing speed, GeoMax™ allows converters to reduce virgin polymer content per part, delivering direct Scope 3 emission reductions and measurable cost savings in high-volume automotive and consumer applications. This strategy reflects a broader industry movement toward “mineral efficiency” rather than simple filler substitution.

Energy infrastructure has emerged as another performance-driven demand center. Advanced insulation fillers such as Polarite™ 503E have been developed for medium- and high-voltage cable compounds, where dielectric stability must be maintained under prolonged thermal and moisture stress. These surface-treated fillers are engineered to preserve electrical insulation properties across extreme operating environments, aligning polymer filler innovation with global grid modernization and renewable energy integration.

Operational efficiency is also shaping filler design. Highly compacted talc grades such as Steamic® T1WN are gaining adoption as processors seek to eliminate dust generation, reduce air entrainment, and increase compounding throughput. By improving bulk density and feeding consistency, these fillers enable higher line speeds and lower scrap rates, particularly in automotive interiors and durable consumer goods where throughput efficiency directly impacts margins.

Accelerated Adoption of Circular and Bio-Based Fillers under Regulatory Pressure

The enforcement of the EU Packaging and Packaging Waste Regulation in February 2025 has structurally altered filler demand by embedding recycled-content compliance into material selection decisions. Mandatory targets, including 30% recycled content for contact-sensitive PET packaging by 2030, are forcing brand owners and compounders to adopt fillers that enhance recyclability rather than compromise it. This has elevated circular mineral fillers from niche sustainability options to core formulation components.

Imerys’ launch of Polwhite™ LOOP, the first ISCC PLUS certified circular kaolin, illustrates how recycled mineral streams are now being engineered to meet automotive-grade performance standards. Designed for tire inner liners, this filler demonstrates that circular minerals can deliver equivalent barrier properties to virgin materials while supporting OEM net-zero commitments and regulatory reporting requirements.

Bio-based filler systems are scaling rapidly in parallel. By mid-2025, Avient expanded its Maxxam™ BIO polypropylene compounds incorporating up to 40% natural cellulose fiber sourced from wood and agricultural residues. These bio-filled composites are being adopted in automotive interior components where stiffness, dimensional stability, and weight reduction are prioritized alongside carbon footprint reduction.

Packaging applications further highlight the operational role of fillers in circularity. In late 2024, PepsiCo launched flexible film packaging in the UK and Ireland containing 50% recycled plastic, enabled by advanced filler dispersion and stabilization systems. This deployment underscores how high-purity fillers and dispersion control are essential to maintaining film integrity and mechanical strength when post-consumer recyclate levels rise sharply.

High-Thermal-Conductivity Fillers for EV Battery Architectures

Electrification is creating one of the most attractive margin pools for polymer fillers through demand for thermally conductive yet electrically insulating materials. Battery spacers, module housings, and thermal interface components must dissipate heat efficiently while meeting stringent fire resistance and dielectric safety standards such as UL 94 V-0.

In early 2025, Evonik introduced ORTEGOL® DA 801, a specialized dispersant that enables polymer systems to accommodate filler loadings of up to 90% by weight without compromising flow behavior. This innovation supports the use of alumina and aluminum trihydroxide fillers in battery materials, delivering thermal conductivities in the 1.5 W/mK to 3 W/mK range required for fast-charging EV platforms while maintaining processability.

Advanced filler chemistries are also gaining traction. Research published in the Journal of Energy Storage in 2025 demonstrated that polyethylene-boron nitride composites produced via additive manufacturing can encapsulate phase-change materials for effective battery cooling. These filler systems establish efficient thermal pathways while preserving electrical insulation, directly mitigating the risk of thermal runaway.

Automotive validation data from 2025 further indicates that metal-filled polymer composites such as PC+ABS can now replace aluminum in selected battery housing applications. These composites achieve electrical performance within 1.3% of aluminum while delivering meaningful weight reduction and improved corrosion resistance, reinforcing the role of engineered fillers in metal-to-plastic substitution strategies.

Lightweight Mineral-Filled Composites for Infrastructure and Durable Goods

Beyond mobility, infrastructure decarbonization is opening large-volume opportunities for advanced polymer fillers. Global corrosion-related losses exceed $2.5 trillion annually, and conventional materials such as steel and concrete account for roughly 23% of global emissions, according to 2025 engineering assessments. This is accelerating adoption of mineral-filled polymer composites in non-structural and semi-structural applications.

Glass fiber reinforced polymers enhanced with optimized mineral fillers are increasingly deployed in traffic poles, bridge edge elements, and utility infrastructure. These systems offer corrosion resistance, faster installation, and lower lifecycle emissions compared to metal alternatives. Fillers play a critical role in balancing stiffness, impact resistance, and cost in these applications.

Innovation in paving and construction further expands volume potential. Aramco has patented non-metallic paving panels that rely on high mineral filler content to deliver compressive strength and UV durability comparable to asphalt. This development signals a scalable demand channel for calcium carbonate and silicate fillers in industrial infrastructure.

In parallel, next-generation engineered cementitious composites incorporating polymer fillers have achieved densities as low as 111 lb/ft³ while maintaining compressive strengths of 5.8 ksi. These materials offer enhanced ductility and seismic resistance, making them attractive for modular and earthquake-prone construction markets where traditional rigid materials underperform.

Polymer Fillers Market Share and Segmentation Insights

Inorganic Fillers Lead Polymer Filler Consumption Across PVC, Polyolefins, and Engineering Plastics

Inorganic fillers accounted for 68.40% of the Polymer Fillers Market by filler type in 2025, reflecting their dominant role in modifying mechanical, thermal, and barrier properties of polymer compounds used across multiple industries. Materials such as calcium carbonate, talc, kaolin, silica, carbon black, and glass fibers are widely used in PVC, polypropylene, polyethylene, and engineering plastics to improve stiffness, dimensional stability, and impact resistance while reducing material costs. Calcium carbonate remains the highest-volume polymer filler due to its extensive use in PVC pipes, films, and profiles. In 2025, surface-modified inorganic fillers have gained traction, with stearate, silane, and titanate surface treatments improving filler dispersion, reducing moisture absorption, and enhancing polymer-filler interfacial adhesion for higher filler loadings and improved compound performance.

Building and Construction Sector Drives Polymer Filler Demand in PVC and Polyolefin Compounds

Building and construction represented 34.80% of the Polymer Fillers Market by end-use industry in 2025, supported by extensive use of filled polymers in PVC pipes, window profiles, siding, insulation components, and structural plastic materials. Mineral fillers such as calcium carbonate and talc are widely incorporated into PVC and polypropylene compounds to improve stiffness, dimensional stability, and processability in construction applications. The scale of global infrastructure development and residential construction continues to drive polymer compound demand in this sector. In 2025, lightweight construction materials and engineered filler technologies are influencing compound formulations, enabling thinner wall profiles, improved structural performance, and optimized cost efficiency in polymer-based construction materials used in modern building systems.

Polymer Fillers Market Competitive Landscape

The global polymer fillers market is shifting toward engineered, high-performance mineral fillers that enhance recyclability, lightweighting, and thermal stability. Competitive dynamics are driven by EV battery applications, sustainable packaging demand, and specialty fillers that improve mechanical properties while reducing carbon footprint.

Imerys Advances High-Aspect-Ratio Fillers for EV, Energy Transition, and Circular Elastomers

Imerys S.A. leads the transition toward functional mineral fillers with a strong focus on energy transition and EV applications. The launch of Polwhite™ LOOP introduces circular kaolin for tire reinforcement, improving rolling resistance and sustainability without compromising mechanical strength. Polarite™ 503E targets high-voltage cable insulation with superior dielectric stability under extreme conditions. The company reported €546 million EBITDA in 2025, supported by 15% growth in its graphite and carbon segment. Expansion of talc processing in China strengthens supply to EV manufacturers, while the EMILI lithium project enhances battery material integration. Strategy centers on high-performance minerals, conductive additives, and low-carbon filler solutions.

Omya Strengthens Sustainable Fillers with Recycled Calcium Carbonate and Lightweight Microspheres

Omya AG is repositioning its portfolio toward sustainable and lightweight polymer fillers. The launch of Omyaloop FC introduces pre-consumer recycled calcium carbonate for food-contact plastics, reducing carbon emissions by up to two-thirds. The OPPD platform integrates mineral supply with polymer distribution, creating a one-stop solution for compounders. Omyasphere 900 series hollow glass microspheres enable weight reduction in automotive and electronics components while improving thermal performance. Advanced surface treatment technologies allow calcium carbonate integration into engineering biopolymers like PET. Strategy emphasizes circular materials, lightweighting, and high-performance filler integration.

Cabot Expands Circular Carbon Fillers with EV Battery Integration and Sustainable Reinforcing Solutions

Cabot Corporation is strengthening its leadership in carbon-based fillers through circular reinforcing technologies. The acquisition of Mexico Carbon Manufacturing enhances North American production capacity for specialty carbons. A supply agreement with PowerCo SE positions Cabot as a key supplier of conductive additives for EV battery cells. The EVOLVE® platform converts end-of-life tires into circular carbon fillers, supporting sustainability goals. A global price increase of up to 20% reflects rising energy and supply chain costs. Strategy focuses on circular carbon materials, EV integration, and high-performance reinforcing fillers.

Minerals Technologies Scales Satellite Plant Model for Sustainable Packaging and Cost-Efficient Filler Production

Minerals Technologies Inc. (MTI) is expanding its satellite plant model to deliver on-site filler production for high-volume industries. The company launched multiple satellite plants in Asia, with 50% dedicated to sustainable packaging applications. It reported $2.07 billion in revenue in 2025, with strong performance in specialty additives. MTI’s precipitated calcium carbonate (PCC) technology enhances opacity and reduces reliance on wood fiber in packaging and thermoplastics. With 56 global satellite facilities, MTI ensures supply chain efficiency and reduced logistics costs. Strategy centers on localized production, packaging sustainability, and crystal-engineered fillers.

Sibelco Accelerates Circular Fillers with Recycled Glass Integration and Low-Carbon Mineral Solutions

Sibelco is advancing circular economy initiatives through large-scale glass recycling and high-purity mineral fillers. The integration of Strategic Materials Inc. expands its recycling capacity to approximately 5 million tonnes annually across 60 sites. The company achieved a 21% reduction in Scope 1 and 2 emissions intensity, reinforcing its sustainability commitments. Revenue reached €2,225 million with strong EBITDA growth since 2020. Recycled glass and silica fillers are increasingly used in construction plastics and coatings as alternatives to virgin materials. Strategy emphasizes circular materials, low-carbon production, and sustainable filler solutions.

Huber Engineered Materials Leads Flame-Retardant Fillers with Surface-Modified ATH and MDH Technologies

Huber Engineered Materials (HEM) dominates halogen-free flame retardant filler markets with ATH and MDH technologies. These fillers provide both fire and smoke suppression for wire, cable, and construction polymers. The company is advancing surface-modified fillers that enable higher loading levels without compromising mechanical properties. Expansion of custom-engineered mineral solutions targets polyolefins used in automotive and electrical applications. Strategy focuses on replacing hazardous additives, enhancing safety performance, and supporting regulatory compliance in high-risk environments.

China – Regulatory Acceleration Driving Compostable and Functional Filler Scale-Up

China’s polymer fillers industry in 2025 is being reshaped by regulatory enforcement and supply-chain localization, positioning the country as a high-volume adopter of biodegradable and performance-oriented fillers. The final implementation phase of the Action Plan for Plastic Pollution (2021–2025) has forced packaging converters and compounders to rapidly replace conventional inorganic fillers with certified compostable and bio-based alternatives, particularly in express logistics and takeaway food packaging. This shift has materially increased demand for starch-based fillers, cellulose-reinforced polymers, and surface-modified mineral fillers that comply with compostability labeling and municipal waste sorting requirements. Concurrently, the rollout of GB 30981.1-2025 standards has tightened permissible heavy-metal thresholds in fillers such as calcium carbonate and talc, directly impacting toy, healthcare, and consumer electronics exports.

From a production standpoint, Chinese chemical hubs such as Cangzhou and Zhanjiang scaled the output of ultra-fine calcium carbonate and talc masterbatches in mid-2025, optimized for high-speed extrusion and thin-wall molding. These developments are reinforced by BASF’s Zhanjiang Verbund site reaching full-scale operations in 2025, integrating localized filler and additive manufacturing to support EV battery housings and structural plastics. Policy support remains explicit, with the Ministry of Industry and Information Technology offering tax credits for recycled mineral fillers derived from industrial byproducts, effectively lowering the cost base for circular-economy polymer formulations.

United States – Advanced Materials Funding and Nano-Filler Commercialization

The U.S. polymer fillers market is increasingly defined by federal funding programs and a rapid pivot toward high-performance, PFAS-free, and nano-engineered fillers. In June 2025, the Advanced Materials & Manufacturing Challenge under TechConnect 2025 mobilized more than $8 billion in combined public and private funding, accelerating R&D pipelines for sustainable and multifunctional polymer fillers. Parallel to this, the National Nanotechnology Initiative’s 2025 budget prioritized nanoscale fillers such as nanoclays, boron nitride, and carbon nanotubes to improve mechanical strength and thermal stability in aerospace-grade and 3D-printed polymers.

Regulatory pressure has also reshaped material choices. Following state-level PFAS bans, U.S. compounders have increasingly substituted fluoropolymer processing aids with ceramic-based and boron-nitride fillers. Infrastructure spending under the Bipartisan Infrastructure Law further expanded demand for glass-fiber- and mineral-reinforced polymers in bridge decks and traffic systems. On the cost side, producers such as Eastman Chemical announced price increases in May 2025 for specialty alcohols used in filler surface treatments, reflecting higher compliance and operating costs. Notably, July 2025 marked the industrial scaling of carbon-negative BioBlack fillers, introducing a bio-based alternative to petroleum-derived carbon black for automotive interiors.

India – Localization, Traceability, and Fire-Safe Filler Development

India’s polymer fillers industry is advancing along a dual trajectory of localization and regulatory digitization. Under the Make in India additives push, Lubrizol committed $200 million to a new Aurangabad manufacturing facility, its largest regional investment, to produce advanced additives and fillers for polymers and industrial fluids. Policy momentum has intensified through PLASTINDIA 2026, which targets zero-waste manufacturing and localized production of hollow glass microspheres and specialty fillers to drive 20% sectoral growth.

Regulatory oversight has increased sharply. Effective July 1, 2025, Plastic Waste Management Rules mandate QR-coded traceability for all additives and fillers, forcing suppliers to integrate digital reporting into extended producer responsibility systems. On the resource side, the government fast-tracked modernization of talc and kaolin mining in Rajasthan to secure domestic inorganic filler supply for construction plastics and paints. Simultaneously, India’s expanding EV charging infrastructure has driven laboratory-scale and pilot commercialization of halogen-free, intumescent flame-retardant fillers, aligning polymer filler development with fire safety and sustainability norms.

Germany – Smart Fillers and Circular Reinforcement Systems

Germany continues to lead the polymer fillers industry in advanced engineering, circularity, and decarbonized production. BASF’s commitment to invest €1.5–2 billion annually through 2028 at Ludwigshafen includes modernization of reinforcing filler and light stabilizer lines, reinforcing the site’s role as a European innovation anchor. Regulatory leadership under the European Green Deal and Omnibus Act VII has pushed German producers to ensure all food-contact polymer fillers meet stringent migration and safety thresholds.

Innovation visibility peaked at K 2025, where German manufacturers introduced smart fillers with polymer-coated particles capable of responding to mechanical stress through color or conductivity changes. Circularity has also moved from pilot to commercialization, with Baerlocher launching calcium-based stabilizer and filler systems designed to preserve mechanical properties after multiple recycling loops. On the production side, companies such as Quarzwerke integrated hydrogen-powered kilns in late 2025, cutting the carbon footprint of calcined clay and silica fillers by more than one-third.

Brazil – Trade Protection and Bio-Filler Commercialization

Brazil’s polymer fillers landscape in 2025 is shaped by trade policy intervention and bio-based material innovation. To address a widening trade deficit, the government tightened import controls on polymers and fillers in December 2025, introducing provisional anti-dumping duties on materials from North America. Earlier in May 2025, anti-dumping tariffs on U.S. suspension-grade PVC reached 43.7%, pushing domestic converters toward mineral-filled and bio-filled alternatives for pipes and construction plastics.

Brazil’s competitive advantage lies in biomass-derived fillers. In 2025, researchers successfully commercialized sugarcane bagasse-based cellulose fillers for bioplastic automotive components, aligning polymer filler demand with the country’s agricultural base. Sustainability has extended upstream, with the National Mining Plan introducing “Green Talc” provisions that mandate water-neutral extraction methods for plastics-grade mineral fillers.

Japan – High-Purity and Nano-Reinforced Filler Leadership

Japan’s polymer fillers industry occupies a high-value niche focused on purity, reliability, and nanotechnology integration. In January 2025, LifeSprout finalized a commercialization agreement for Lumina™, a bio-stimulatory polymer filler, reinforcing Japan’s leadership in medical-grade and regenerative filler applications. Beyond healthcare, filler innovation is tightly coupled with electronics and AI infrastructure. Shin-Etsu Chemical launched its CLG series in mid-2025, incorporating specialized fillers that prevent pump-out and material migration in high-density AI server cooling modules.

Nanotechnology remains a defining strength. Japanese firms in 2025 pioneered nanocellulose-reinforced polyolefins, achieving up to 25% weight reduction in aerospace interior panels without compromising structural integrity. This positions Japan at the intersection of lightweighting, sustainability, and next-generation polymer filler design.

Comparative Snapshot – Polymer Fillers Industry by Country

Polymer Fillers Market County Level Snapshot

|

Country

|

Primary Policy or Demand Driver

|

Key Filler Focus

|

Strategic Positioning

|

|

China

|

Plastic pollution mandates and export safety standards

|

Compostable, recycled mineral fillers

|

High-volume regulatory-driven adoption

|

|

United States

|

Federal R&D funding and PFAS bans

|

Nano-fillers, bio-based carbon black

|

Innovation-led performance materials

|

|

India

|

Localization and digital traceability

|

Mineral fillers, fire-retardant systems

|

Cost-competitive domestic scaling

|

|

Germany

|

Green Deal and circular economy

|

Smart fillers, low-carbon minerals

|

Engineering and sustainability benchmark

|

|

Brazil

|

Trade protection and biomass availability

|

Cellulose bio-fillers, mineral substitutes

|

Bio-based differentiation

|

|

Japan

|

Electronics and medical purity standards

|

Nano-reinforced, pump-out-resistant fillers

|

High-value niche leadership

|

Polymer Fillers Market Report Scope

Polymer Fillers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$53.7 Billion

|

|

Market Size (2034)

|

$73.8 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Filler Type (Inorganic Fillers, Organic Fillers, Nanofillers), By Functionality (Reinforcing Fillers, Extending Fillers, Functional Fillers), By Polymer Compatibility (Thermoplastics, Thermosets, Elastomers), By End-Use Industry (Automotive & Transportation, Building & Construction, Packaging, Electrical & Electronics, Consumer Goods & Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Imerys SA, Omya AG, Minerals Technologies Inc., BASF SE, Cabot Corporation, 20 Microns Limited, Quarzwerke Group, Huber Engineered Materials, Hoffmann Mineral GmbH, LKAB Group, Sudarshan Chemical Industries Limited, GCR Group, Unimin Corporation, Shin-Etsu Chemical Co. Ltd., Rogers Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymer Fillers Market Segmentation

By Filler Type

- Inorganic Fillers

- Organic Fillers

- Nanofillers

By Functionality

- Reinforcing Fillers

- Extending Fillers

- Functional Fillers

By Polymer Compatibility

- Thermoplastics

- Thermosets

- Elastomers

By End-Use Industry

- Automotive & Transportation

- Building & Construction

- Packaging

- Electrical & Electronics

- Consumer Goods & Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polymer Fillers Industry

- Imerys SA

- Omya AG

- Minerals Technologies Inc.

- BASF SE

- Cabot Corporation

- 20 Microns Limited

- Quarzwerke Group

- Huber Engineered Materials

- Hoffmann Mineral GmbH

- LKAB Group

- Sudarshan Chemical Industries Limited

- GCR Group

- Unimin Corporation

- Shin-Etsu Chemical Co. Ltd.

- Rogers Corporation

*- List not Exhaustive