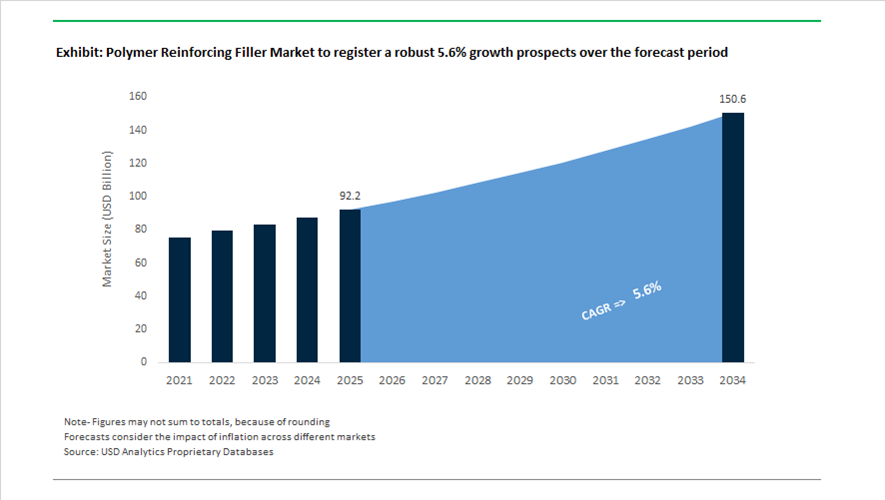

Polymer Reinforcing Filler Market Valued at $92.2 Billion in 2025, Forecast to Reach $150.6 Billion by 2034 at 5.6% CAGR

The global polymer reinforcing filler market is valued at $92.2 billion in 2025 and is projected to reach $150.6 billion by 2034, expanding at a CAGR of 5.6%. Growth is driven by escalating demand for carbon black, silica, graphene, conductive fillers, specialty mineral fillers, and sustainable reinforcing additives across automotive tires, battery energy storage systems, lightweight packaging, construction composites, and high-performance coatings. Reinforcing fillers are critical to enhancing tensile strength, modulus, abrasion resistance, thermal conductivity, and electrical performance in polymer matrices, particularly in thermoplastics, elastomers, and engineered plastics.

In October 2024, Birla Carbon inaugurated its first Asian post-treatment facility in Patalganga, India, focused on specialty carbon blacks with enhanced surface chemistry for advanced polymer reinforcement. In the same month, Birla Carbon launched Continua™ 8030 in India, a sustainable carbonaceous material derived from end-of-life tires, targeting circular economy integration in rubber and thermoplastic compounds. These developments marked an early shift toward low-carbon reinforcing fillers and circular carbon black technologies, aligning with ESG mandates in automotive and industrial polymer markets.

Innovation accelerated in 2025 with performance-driven filler technologies. In October 2025, Cabot Corporation expanded its Ville Platte, Louisiana facility to produce circular reinforcing carbons under its EVOLVE® Sustainable Solutions platform, enabling drop-in replacements for conventional carbon black derived from tire pyrolysis oil. In late 2025, Cabot announced the acquisition of Bridgestone Corporation’s reinforcing carbons plant in Mexico, strengthening supply chain resilience for the automotive tire sector in North America. In November 2025, HydroGraph Clean Power reported commercial validation of its FGA-1 Fractal Graphene, demonstrating a 23% improvement in top-load compression strength for PET packaging at ultra-low loading levels of 0.0015 wt%. This breakthrough significantly advances nano-reinforced polymer composites and lightweight packaging solutions.

Also in November 2025, Orion S.A. confirmed that its PRINTEX® kappa 100 acetylene black had been qualified by major producers for Battery Energy Storage Systems. This high-purity conductive filler is now being deployed in grid modernization projects, strengthening demand for electrically conductive polymer fillers in lithium-ion battery modules and energy infrastructure. In October 2025, Evonik partnered with Schneider Electric to automate a thermoplastic processing plant in Essen, focusing on optimized dispersion and mechanical performance of reinforcing additives in recycled polymers. The initiative addresses a key industry challenge: maintaining structural integrity in mechanically recycled plastics through advanced filler dispersion control.

Strategic consolidation intensified in 2026. In January 2026, Evonik introduced TEGO® Dispers 695, a hyperdispersant designed to improve loading efficiency and stability of reinforcing fillers in radiation-curing and solvent-borne ink systems, expanding filler performance in specialty coatings. In February 2026, Michelin acquired Flexitallic to integrate high-performance gasket fillers and extreme-environment specialty materials into its polymer composite operations. In the same month, Arclin completed the acquisition of Polymer Solutions Group, integrating specialty reinforcing technologies into construction and transportation markets. Earlier in 2026, Arclin finalized its acquisition of The Willamette Valley Company, adding eight R&D and manufacturing facilities dedicated to custom filler systems for wood, railroad, and concrete reinforcement applications. By February 2026, Birla Carbon inaugurated a dedicated production line in Trecate, Italy, to scale finishing and packaging of Continua™ 8030, reinforcing Europe’s role in circular filler adoption.

The polymer reinforcing filler market is increasingly defined by sustainable carbon black production, graphene-enhanced polymer composites, conductive fillers for battery systems, hyperdispersant technologies, and advanced filler surface engineering. Capacity expansion, M&A-driven vertical integration, and nano-scale material innovation are reshaping competitive positioning across automotive, energy storage, packaging, coatings, and infrastructure reinforcement segments.

Strategic Trends and High-Value Opportunities in the Polymer Reinforcing Filler Market

Strategic Shift Toward High-Performance, Surface-Modified Reinforcing Fillers for Lightweighting

The polymer reinforcing filler market is undergoing a structural transition from commodity mineral loading toward engineered, surface-modified fillers that enable lightweighting without compromising mechanical integrity. Automotive and industrial OEMs are increasingly specifying High Aspect Ratio talc and acicular wollastonite to replace heavier metal components or glass fiber reinforced plastics, supporting compliance with stringent efficiency and emissions frameworks such as U.S. CAFE targets of 54.5 mpg and upcoming Euro 7 regulations.

Recent material innovation has moved beyond stiffness enhancement to balanced property optimization. In late 2024, Imerys introduced a next-generation HAR talc platform for polypropylene automotive compounds. Independent performance evaluations confirmed impact resistance improvements of 40 to 60% versus conventional mineral reinforcements, enabling thinner wall sections in bumpers, dashboards, and interior trims while maintaining crash performance. This shift directly reduces vehicle mass and resin consumption, creating measurable cost and carbon benefits at scale.

Thermal and dimensional stability are reinforcing this trend in high-heat environments. Wollastonite, with its acicular morphology, is increasingly displacing glass fiber in under-the-hood components where warpage control and heat resistance are critical. Production trials conducted in mid-2025 demonstrated that a 20 to 30% loading of wollastonite increased the heat deflection temperature of polypropylene from approximately 110°C to above 150°C, while reducing part distortion by up to 20%. This performance consistency improves assembly precision for engine covers, electronic housings, and fluid management systems, where tolerance drift directly impacts reliability.

Accelerated Adoption of Bio-Based and Recycled-Content Circular Reinforcing Fillers

Circularity mandates are transforming reinforcing filler qualification criteria across packaging, automotive, and industrial composites. The implementation of EU Regulation 2025/40 under the Packaging and Packaging Waste framework, which requires 30% recycled content in contact-sensitive PET packaging by 2030, has forced compounders to rapidly validate recycled and bio-derived reinforcing agents that can integrate seamlessly into existing processing lines.

Industrial-scale validation is already underway. The EU-funded ECOXY project successfully demonstrated bio-based epoxy systems reinforced with flax and lignin-derived fibers for automotive rear seat back panels. By 2025, these materials achieved Technology Readiness Level 5, confirming that renewable fillers can meet Tier-1 durability, fatigue, and impact requirements. The ability to repair, recycle, and reprocess these composites aligns closely with OEM sustainability roadmaps and extended producer responsibility targets.

Waste valorization is expanding into adjacent applications such as structural adhesives. Research published in November 2025 highlighted the incorporation of recycled mineral wool and recycled carbon fiber into bio-based thermosetting adhesive systems. At filler loadings of up to 50 parts per hundred resin, these formulations delivered bonding strengths comparable to petroleum-derived benchmarks. This development opens a scalable pathway for reducing embedded carbon in construction, transportation, and aerospace assembly processes without sacrificing structural performance.

High-Thermal-Conductivity Reinforcing Fillers for EV Power Electronics

Rising power densities in electric vehicle power electronics have exposed the thermal limitations of unfilled engineering polymers. This has created a high-margin opportunity for thermally conductive yet electrically insulating reinforcing fillers such as hexagonal boron nitride and engineered aluminas, particularly in 800-volt architectures.

In January 2024, Momentive Technologies demonstrated that polymer composites reinforced with hexagonal boron nitride achieved thermal conductivity levels approaching 15 W/mK, representing nearly a thirty-fold improvement over unfilled polymers. These materials are increasingly specified for traction inverters, onboard chargers, and power control units, where they enable heat dissipation without the weight and design constraints of aluminum heat sinks.

Electrical safety considerations further reinforce adoption. Boron nitride’s stable dielectric properties make it well suited for battery pack encapsulation and insulation systems. Industry assessments from mid-2025 confirm its effectiveness as a passive thermal management filler that also serves as a non-reactive barrier against thermal runaway propagation, extending lithium-ion cell service life and improving overall pack reliability.

Low-Density Reinforcing Fillers for Advanced Additive Manufacturing Feedstocks

Industrial additive manufacturing is emerging as a distinct growth channel for polymer reinforcing fillers, particularly those that enhance inter-layer bonding and mechanical consistency. Conventional 3D printed polymers often suffer from anisotropic strength due to weak fusion between printed layers, creating demand for functionalized nanoparticles and hollow microspheres.

A December 2025 study demonstrated that incorporating 2 to 10% silicon nitride nanoparticles into polyamide-12 feedstocks increased tensile strength and elastic modulus by more than 20%. This improvement enables the production of lightweight, load-bearing components suitable for aerospace prototyping and industrial tooling, applications traditionally limited to injection-molded parts.

In high-performance thermoplastics, filler innovation is addressing processing constraints. The addition of inorganic fullerene-like tungsten disulfide nanoparticles to PEEK has been shown to reduce melt viscosity during fused deposition modeling. This enhances polymer chain inter-diffusion between layers, narrowing the mechanical performance gap between printed and molded parts. As a result, reinforcing fillers are becoming essential enablers for medical implants, aerospace brackets, and space-grade components manufactured via additive processes.

Polymer Reinforcing Filler Market Share and Segmentation Insights

Inorganic Fillers Lead Reinforced Polymer Compounding Across Automotive and Industrial Applications

Inorganic fillers accounted for 48.60% of the Polymer Reinforcing Filler Market by material type in 2025, reflecting their widespread use in reinforced polymer compounds across automotive components, construction materials, and consumer goods manufacturing. Calcium carbonate, talc, kaolin, silica, and glass fibers are widely incorporated into thermoplastics and engineering plastics to improve stiffness, dimensional stability, impact resistance, and thermal performance while maintaining cost efficiency in high-volume polymer compounding. Established compounding infrastructure and broad compatibility with polypropylene, polyethylene, and nylon systems continue to support inorganic filler dominance. In 2025, surface-functionalized inorganic fillers are gaining market traction, with silane and titanate treatments improving polymer filler adhesion, dispersion quality, and mechanical reinforcement performance in advanced polymer composite formulations.

Automotive Industry Drives Demand for Reinforced Polymer Materials in Lightweight Vehicle Components

Automotive applications represented 34.80% of the Polymer Reinforcing Filler Market by application in 2025, supported by extensive use of reinforced thermoplastics and composite materials in modern vehicle design. Glass fiber reinforced polypropylene and nylon compounds are widely used in under-hood components, structural parts, and interior modules, while talc-filled polyolefins provide dimensional stability and surface quality for automotive panels and trims. Global vehicle production volumes and the transition toward lightweight vehicle architectures continue to drive demand for reinforced polymer materials. In 2025, electric vehicle lightweighting strategies are accelerating adoption of reinforced polymer composites, including glass fiber, carbon fiber, and natural fiber reinforced materials used in battery enclosures, structural components, and interior systems designed to improve vehicle efficiency and range.

Polymer Reinforcing Filler Market Competitive Landscape

The global polymer reinforcing filler market is transitioning toward high-aspect-ratio minerals, nano-silica, and circular reinforcing carbons. Competitive intensity is driven by EV lightweighting, sustainable tire architectures, and high-performance fillers that enhance tensile strength, thermal stability, and recyclability in advanced polymer systems.

Imerys Accelerates EV-Grade HAR Talc and Circular Kaolin Adoption Through Project Horizon Strategy

Imerys S.A. is repositioning its portfolio toward high-performance reinforcing fillers under Project Horizon, focusing on energy transition materials. The launch of Polwhite™ LOOP introduces ISCC PLUS-certified circular kaolin for tire inner liners, improving barrier performance with recycled feedstocks. The Wuhu talc plant in China operates at full capacity, supplying high-aspect-ratio talcs for EV lightweight automotive plastics. Strategic capital reallocation toward the EMILI lithium project, backed by a €50 million French government investment, strengthens its battery materials integration. Jetfine® and Steashield® talc brands deliver optimized stiffness and toughness for thin-wall injection molding. Strategy emphasizes specialty minerals, EV integration, and circular filler innovation.

Cabot Expands Circular Carbon Leadership with ISCC PLUS Network and Regionalized Supply Chains

Cabot Corporation leads reinforcing filler innovation through circular carbon technologies and sustainable supply chains. Validation of circular reinforcing carbon production in Indonesia and China enables regional manufacturing and distribution across key markets. The company operates 14 ISCC PLUS-certified sites, ensuring traceability for recovered carbon materials used in tire production. A global price increase of up to 20% reflects rising energy costs and ongoing investments in sustainable manufacturing. EVOLVE® solutions provide drop-in replacements for conventional carbon black, supporting OEM targets of 40% sustainable material usage by 2030. Strategy focuses on circular reinforcement, supply chain localization, and performance-grade carbon fillers.

Omya Builds Integrated Reinforcing Filler Platform with Recycled Minerals and Lightweight Microspheres

Omya AG is transforming into a comprehensive solution provider through its Omya Performance Polymers Distribution (OPPD) platform. The integration of Distrupol enhances its ability to deliver tailored reinforcing filler solutions to polymer compounders. Omyaloop FC offers pre-consumer recycled calcium carbonate for food-contact applications, supporting circular packaging regulations. The Omyasphere 900 series introduces hollow glass microspheres that reduce weight while maintaining mechanical strength in automotive and aerospace components. Advanced surface-treatment technology enables calcium carbonate use in engineering polymers like PET. Strategy emphasizes lightweighting, recycled fillers, and integrated material solutions.

Evonik Optimizes Silica Network for High-Performance Reinforcing Fillers and Recycling Integration

Evonik Industries AG is restructuring its silica production network to focus on world-scale facilities for reinforcing filler applications. Closure of smaller plants in the U.S. centralizes production into more efficient, large-scale hubs, improving supply resilience. The company reported €1.87 billion EBITDA in 2025, supporting continued investment in advanced polymer additives. Collaboration with Schneider Electric enables automated recycling processes that integrate reinforcing fillers into recycled thermoplastics. Its Advanced Technologies segment generated €5.97 billion in revenue, driven by high-performance plastics and membrane applications. Strategy centers on silica innovation, recycling integration, and high-value reinforcing additives.

Sibelco Strengthens Recycled Glass Fillers with Large-Scale Processing and Low-Carbon Strategy

Sibelco is expanding its position in sustainable reinforcing fillers through large-scale glass recycling operations. The acquisition of Strategic Materials adds over 40 plants and significantly increases processing capacity. The company now operates more than 60 facilities, processing approximately 5 million tonnes of recycled glass annually. A 21% reduction in CO₂ emissions intensity demonstrates its commitment to low-carbon mineral production. Recycled glass cullet is increasingly used as reinforcing fillers in polymer composites and coatings. Strategy focuses on circular materials, large-scale recycling, and sustainable filler solutions.

Minerals Technologies Scales PCC Reinforcing Fillers with Satellite Plant Model and Packaging Focus

Minerals Technologies Inc. (MTI) leverages its satellite plant model to deliver on-site precipitated calcium carbonate (PCC) reinforcing fillers. The company reported $2.07 billion in 2025 revenue, supported by strong demand in sustainable packaging applications. Expansion of satellite plants in Asia enhances localized production and reduces logistics costs. PCC technology improves opacity, strength, and filler dispersion in polymer and paper applications. The establishment of a $215 million trust resolves legacy liabilities, enabling focus on high-performance filler technologies. Strategy emphasizes decentralized production, packaging innovation, and engineered reinforcing fillers.

India – Reinforcement Technologies Anchored in Recycling, Infrastructure, and Localization

India’s polymer reinforcing filler landscape in 2025–2026 is being reshaped by regulatory pressure on recycled plastics and targeted investments in compounding infrastructure. The April 2025 recycled content mandate issued by the Ministry of Environment, Forest and Climate Change has materially altered filler demand profiles. Packaging converters increasingly require high-performance mineral and hybrid reinforcing fillers that can restore tensile strength, impact resistance, and melt stability in post-consumer resin streams. This has accelerated the adoption of ultra-fine talc, calcined clay, and flame-retardant reinforcing masterbatches designed specifically for PCR-rich formulations.

Structural support for this transition is coming from policy-backed infrastructure. As of December 2025, the Department of Chemicals and Petrochemicals has approved nine Plastic Parks with shared R&D and pilot compounding facilities, enabling domestic producers to scale high-loading reinforcing fillers under controlled quality environments. The extension of the Polypropylene Quality Control Order to April 2026 provides critical lead time for filler suppliers to standardize grades and secure certification. Parallel investments by Indian Oil at the Paradip complex are strengthening domestic availability of reinforcing additives and engineered resins. Skill development is also being institutionalized, with CIPET centers launching NBA-accredited polymer nanotechnology programs to build expertise in nano-silica and hybrid filler systems.

Germany – Circularity, Automotive Engineering, and Decarbonized Mineral Processing

Germany continues to set the global benchmark for advanced and sustainable polymer reinforcing fillers. At K 2025 in Düsseldorf, German manufacturers introduced circular fillers engineered for efficient separation during chemical recycling, directly addressing EU circular economy mandates. This innovation trajectory is reinforced by long-term capital commitments from BASF, which is investing up to €2 billion annually through 2028 at Ludwigshafen to modernize production of high-performance fillers for automotive and engineering plastics.

Sustainability is extending beyond materials into processing technologies. Mineral filler specialists such as Quarzwerke have integrated hydrogen-powered calcination kilns, reducing the carbon footprint of silica and silicate fillers by up to 35%. Downstream, application-driven innovation is visible in products such as carbon-zero synthetic turf developed by Polytan and reinforced polyurethane systems like PermaQure® EPU from Stahl, which leverage filler reinforcement to deliver durability and embossing precision. Germany’s reinforcing filler ecosystem is thus tightly aligned with automotive electrification, recycling, and low-carbon manufacturing.

United States – High-Performance Fillers for Aerospace, Infrastructure, and PFAS-Free Processing

The U.S. polymer reinforcing filler market in 2025 is increasingly driven by federal innovation funding, aerospace requirements, and regulatory-driven material substitution. In November 2025, the U.S. Economic Development Administration allocated $51 million to the Sustainable Polymers Tech Hub, with a mandate to scale bio-based reinforcing agents and establish lifecycle management frameworks. This initiative reflects a broader push to diversify away from conventional mineral fillers toward renewable and nano-enabled alternatives.

Performance-driven demand is particularly visible in aerospace and defense. The 2025 TechConnect Critical Challenge prioritized the integration of carbon nanotubes and graphene into polymer matrices to enhance lightning-strike protection and structural integrity in composite airframes. At the same time, tightening state-level PFAS bans have accelerated the transition toward boron nitride and ceramic-based reinforcing fillers as substitutes for fluoropolymer processing aids. Cost pressures remain a factor, with producers such as Eastman implementing price increases linked to energy-intensive surface treatment processes, reinforcing the premium positioning of high-performance fillers in the U.S. market.

Brazil – Bio-Based Reinforcement and Import Substitution Dynamics

Brazil’s reinforcing filler market is being shaped by bio-based innovation and trade protection measures. In late 2025, Braskem expanded its I’m green™ portfolio to include high-density polyethylene reinforced with sugarcane-derived fillers for hygiene and nonwoven applications. This aligns reinforcing filler development with Brazil’s renewable feedstock advantage and sustainability positioning.

Trade policy is also influencing material choices. Provisional anti-dumping duties imposed in December 2025 on U.S.-origin resins are expected to push converters toward mineral-filled PVC and polypropylene alternatives for infrastructure and construction. Braskem’s launch of a bio-based EVA with optimized filler reinforcement for premium footwear further highlights Brazil’s focus on combining flexibility, softness, and durability through tailored filler systems.

Japan – Precision Reinforcement for Semiconductors and Advanced Mobility

Japan’s polymer reinforcing filler industry is defined by high-purity materials and advanced mobility applications. In 2025, Japanese leaders including Mitsubishi Chemical and Shin-Etsu completed capacity expansions for ultra-high-purity spherical silica. These fillers are critical for reinforcing epoxy molding compounds used in AI chips and advanced semiconductor packaging, where dimensional stability and thermal reliability are paramount.

Beyond electronics, structural reinforcement is expanding into next-generation mobility. Toray Industries increased localized production of chopped carbon fiber fillers in mid-2025, targeting thermoplastic components for humanoid robots and electric vertical takeoff and landing aircraft. Japan’s reinforcing filler strategy is thus centered on precision engineering, purity, and integration into high-value electronic and aerospace systems.

Comparative Snapshot – Polymer Reinforcing Filler Industry

Polymer Reinforcing Filler Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Dominant Reinforcing Filler Types

|

Strategic Orientation

|

|

India

|

Recycled plastics, infrastructure

|

Talc, calcined clay, flame-retardant fillers

|

Localization and PCR performance

|

|

Germany

|

Automotive and circular economy

|

Circular fillers, silica, silicates

|

Decarbonization and recyclability

|

|

United States

|

Aerospace, infrastructure

|

CNTs, graphene, ceramic fillers

|

High-performance and PFAS-free

|

|

Brazil

|

Bio-based materials, import substitution

|

Sugarcane-based fillers, mineral fillers

|

Renewable feedstocks

|

|

Japan

|

Semiconductors, advanced mobility

|

High-purity silica, carbon fiber fillers

|

Precision and purity

|

Polymer Reinforcing Filler Market Report Scope

Polymer Reinforcing Filler Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$92.2 Billion

|

|

Market Size (2034)

|

$150.6 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Material Type (Inorganic Fillers, Fiber Reinforcements, Carbon-Based Fillers, Specialty Fillers), By Functionality (Reinforcing Fillers, Non-Reinforcing Fillers, Conductive & Functional Fillers), By Application (Automotive, Building & Construction, Electrical & Electronics, Packaging, Aerospace & Defense)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Imerys SA, Owens Corning, Omya International AG, Cabot Corporation, Mitsubishi Chemical Group Corporation, Toray Industries Inc., Minerals Technologies Inc., SGL Carbon SE, Solvay SA, Evonik Industries AG, Celanese Corporation, 20 Microns Limited, J.M. Huber Corporation, Shin-Etsu Chemical Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymer Reinforcing Filler Market Segmentation

By Material Type

- Inorganic Fillers

- Fiber Reinforcements

- Carbon-Based Fillers

- Specialty Fillers

By Functionality

- Reinforcing Fillers

- Non-Reinforcing Fillers

- Conductive & Functional Fillers

By Application

- Automotive

- Building & Construction

- Electrical & Electronics

- Packaging

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polymer Reinforcing Filler Industry

- BASF SE

- Imerys SA

- Owens Corning

- Omya International AG

- Cabot Corporation

- Mitsubishi Chemical Group Corporation

- Toray Industries Inc.

- Minerals Technologies Inc.

- SGL Carbon SE

- Solvay SA

- Evonik Industries AG

- Celanese Corporation

- 20 Microns Limited

- J.M. Huber Corporation

- Shin-Etsu Chemical Co. Ltd.

*- List not Exhaustive