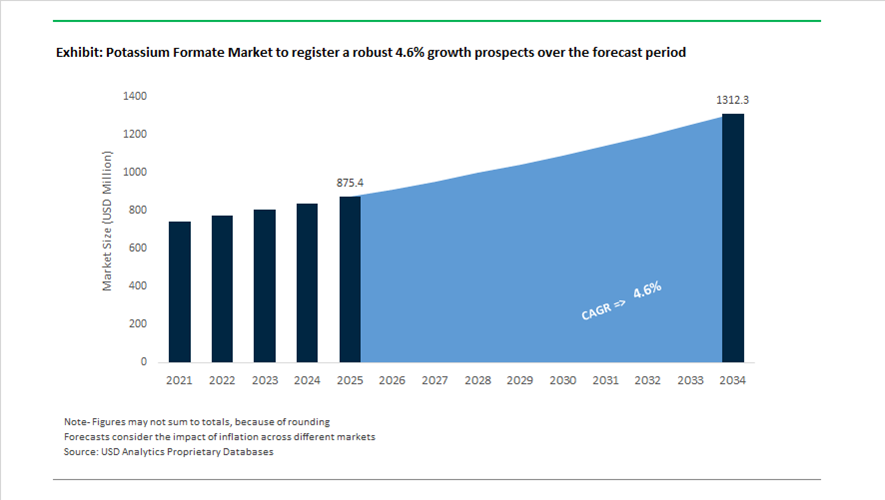

Potassium Formate Market Valued at $875.4 Million in 2025, Projected to Reach $1,312.2 Million by 2034 at 4.6% CAGR

The global potassium formate market is valued at $875.4 million in 2025 and is projected to reach $1,312.2 million by 2034, expanding at a CAGR of 4.6%. Demand is being driven by increasing adoption of potassium formate brines in offshore drilling, eco-friendly runway de-icing fluids, high-performance drilling mud additives, semiconductor-grade solvents, and advanced renewable energy applications. The market is benefiting from tightening environmental regulations that favor low-toxicity, biodegradable alternatives to chloride-based salts and fossil-derived de-icers. Rising offshore exploration in the North Sea and Permian Basin, along with decarbonization mandates in aviation and infrastructure, is reshaping long-term demand for high-purity and low-carbon formate grades.

In 2024, Addcon GmbH confirmed that its Norway and Germany facilities reached a combined production capacity of 800,000 barrels per annum for potassium formate brines, reinforcing supply security for offshore oilfield services. In June 2024, a validated research breakthrough demonstrated that potassium formate significantly reduces iodine impurities in perovskite solar cells, improving efficiency to 23.8%, stimulating interest from photovoltaic and electronics manufacturers in ultra-pure HCOOK grades. In late 2024, Perstorp partnered with TSMC on a pilot project evaluating ultra-high-purity potassium formate as a solvent in semiconductor etching, offering improved thermal stability over glycol-based alternatives in advanced 5G chipset fabrication. Throughout 2024 and into early 2025, Perstorp expanded commercialization of its TurboKlear™ potassium formate drilling fluid, which gained traction in North American horizontal wells due to its clay inhibition properties without requiring solid weighting agents such as barite.

Structural and regulatory drivers intensified in 2025. In January 2025, Quebec-based Electro Carbon delivered industrial-scale volumes of ECOWAY50, the first runway de-icer produced via CO2 electrolysis, marking the commercial debut of carbon-capture-derived potassium formate. This milestone introduces a new low-carbon production pathway for aviation de-icing fluids. In early 2025, Cabot Corporation announced a $75 million investment in a Texas facility capable of producing 50,000 tons per year of potassium formate by 2026 to meet rising demand for environmentally compliant brines in the Permian Basin. In July 2025, BASF initiated expanded operations at its Nanjing site powered by 100% renewable electricity, indirectly lowering the carbon intensity of downstream organic acid derivatives including formates. In August 2025, Perstorp launched a global rightsizing initiative aimed at optimizing energy-intensive business units, including its potassium formate production segment amid elevated European energy costs.

Regulatory shifts in Northern Europe are reinforcing long-term demand. Beginning in 2025, Norway implemented new offshore drilling mandates requiring low-impact drilling fluids, prompting multi-year supply contracts between North Sea operators and suppliers such as Cabot and Addcon. In parallel, Honeywell’s $2.3 billion acquisition of Johnson Matthey’s catalyst business, expected to close in 2026, strengthens catalytic pathways linked to formic acid and derivative production, enhancing upstream integration across the formate supply chain. Arclin’s 2025 acquisition of Polymer Solutions Group also expands distribution channels for potassium formate as a performance additive in industrial resins and construction materials.

The potassium formate market is increasingly characterized by carbon-capture-derived de-icers, ultra-pure semiconductor-grade formates, perovskite solar cell additives, low-toxicity offshore drilling brines, renewable-energy-integrated production sites, and strategic capacity expansions in North America and Europe. Environmental compliance mandates, decarbonization initiatives, and high-purity application development across energy, electronics, and aviation sectors are driving sustained growth across the global potassium formate value chain.

Trends and Opportunities in the Potassium Formate Market

Strategic Adoption as a Premium, Solids-Free HPHT Drilling Fluid

Potassium formate is increasingly positioned as a premium drilling and completion fluid in high-pressure high-temperature oil and gas environments, particularly where reservoir integrity and productivity are mission critical. Traditional barite-weighted and chloride-based mud systems are progressively being displaced due to their tendency to induce formation damage, clay swelling, and unstable Equivalent Circulating Density profiles. In contrast, potassium formate brines offer a solids-free chemistry that minimizes pore plugging and preserves permeability in carbonate and sandstone reservoirs.

A defining milestone was achieved in 2025 during offshore drilling operations in Indonesia’s Madura region, where a 14.9 ppg potassium formate system was deployed to access the Kujung-1 carbonate reservoir. The use of a high-density, solids-free brine delivered Absolute Open Flow rates above pre-drill expectations, significantly reducing the need for acidizing or stimulation interventions post drilling. From an operational standpoint, this translated into lower non-productive time and improved well economics, reinforcing potassium formate’s value proposition in premium offshore developments.

Thermal resilience has further accelerated adoption. Field data from 2025 confirms that potassium formate systems remain rheologically stable at bottom-hole temperatures exceeding 180°C. Unlike polymer-thickened fluids that degrade under prolonged thermal exposure, formate brines maintain lubricity and hole-cleaning efficiency in extended-reach horizontal wells. Operators have reported reductions in torque and drag of up to 15%, a material advantage as drilling trajectories become longer and more complex in deepwater and unconventional plays.

Vertical Integration and Capacity Expansion by Chemical Majors

As demand shifts toward high-purity potassium formate grades, producers are investing heavily in capacity expansion and vertical integration to secure supply reliability and cost control. Purity levels above 95% are increasingly required not only for oilfield applications but also for electronics, specialty energy fluids, and environmentally sensitive industrial uses.

In January 2024, BASF SE announced a 20% expansion of its potassium formate production capacity, targeting both oilfield fluids and aviation de-icing markets. Perstorp Holding AB implemented a similar capacity increase, emphasizing backward integration to stabilize raw material sourcing as demand for performance brines and specialty formates tightened in 2025. These investments reflect a strategic move away from commoditized salts toward value-added organometallic and functional fluid chemistries.

Regional supply security has also become a competitive differentiator. ADDCON GmbH operates one of Europe’s largest potassium formate production clusters, with dedicated annual output equivalent to approximately 800,000 barrels of formate brine. This centralized model enables rapid response to seasonal demand surges from North Sea offshore operations and Northern European aviation hubs, ensuring uninterrupted supply during peak winter and drilling cycles.

Penetration into the Aviation De-Icing Market as a Corrosion-Inhibited Alternative

Environmental regulation is fundamentally reshaping the aviation de-icing chemicals market, creating a strong pull for potassium formate-based runway and aircraft de-icers. Regulatory frameworks such as the U.S. EPA’s Effluent Limitation Guidelines and increasingly stringent airport runoff controls in Europe are forcing operators to move away from urea and glycol-heavy formulations that contribute to aquatic toxicity and infrastructure corrosion.

Potassium formate de-icers have emerged as a preferred solution under total-cost-of-ownership evaluations. Operational data from Avinor at Oslo Airport in 2025 demonstrated that switching to potassium formate-based runway de-icing fluids resulted in approximately 80% lower corrosion compared to urea-based alternatives. Reduced chemical attack on aircraft landing gear, electrical systems, and ground infrastructure has translated into longer maintenance intervals and improved asset availability for airlines operating in cold-climate regions.

From an environmental compliance perspective, potassium formate offers over 60% biodegradability and substantially lower Biological Oxygen Demand relative to acetate and glycol systems. These attributes align with FAA-approved airport de-icing programs for the 2025 to 2026 winter season, where controlling contaminated runoff has become a decisive factor in chemical selection.

Low-Corrosion Heat Transfer Fluids for Renewable Energy and Industrial Cooling

The expansion of Concentrated Solar Power capacity and hybrid renewable energy systems is opening a high-value niche for potassium formate as a non-flammable, low-corrosion heat transfer fluid. Traditional synthetic oils present fire risks, while molten salt systems require extensive heat tracing and are highly corrosive at operating temperatures.

China’s 14th Five-Year Plan has accelerated deployment of CSP and hybrid CSP-plus projects, with 34 large-scale installations initiated during 2024 and 2025. These projects are driving evaluation of potassium formate-based fluids due to their high specific heat capacity, thermal stability, and ability to remain liquid at low ambient temperatures. Eliminating freeze protection and heat-tracing infrastructure can materially reduce capital and operating costs in large solar thermal installations.

Beyond renewables, potassium formate is gaining traction in industrial HVAC, refrigeration, and secondary cooling systems, including food processing and pharmaceutical manufacturing. With the U.S. heat transfer fluid segment holding a 28.3% share of global demand in 2024, the shift toward non-toxic, food-safe coolants is accelerating adoption. Potassium formate’s low corrosivity and favorable safety profile position it as a scalable solution across cold-chain logistics, data centers, and temperature-sensitive industrial operations.

Potassium Formate Market Share and Segmentation Insights

Liquid Potassium Formate Leads Global Market Due to Compatibility with Industrial Fluid Handling Systems

Liquid potassium formate accounted for 68.40% of the Potassium Formate Market by form in 2025, reflecting its suitability for industrial applications that require ready to use fluid solutions. Potassium formate solutions in the concentration range of 50 to 75% are widely used in drilling fluids, de icing agents, and heat transfer systems where accurate concentration control and rapid deployment are required. Liquid formulations eliminate the need for dissolution processes and integrate easily into existing fluid handling and pumping systems used in industrial operations. In 2025, engineering of high density potassium formate brines for oilfield operations has advanced, enabling customized fluid formulations with densities up to 1.57 specific gravity for improved well pressure control and shale stabilization in drilling environments.

Drilling and Completion Fluids Drive Potassium Formate Demand in Oil and Gas Well Construction

Drilling and completion fluids represented 42.80% of the Potassium Formate Market by application in 2025, reflecting the chemical's critical role in advanced oil and gas drilling operations. Potassium formate brines provide excellent shale inhibition, low corrosion potential, and reduced formation damage compared with traditional completion fluids, making them suitable for high pressure and environmentally sensitive drilling environments. Oilfield operators increasingly use potassium formate fluids to maintain wellbore stability and protect reservoir integrity during drilling and completion stages. In 2025, growing exploration of high pressure high temperature reservoirs has increased demand for potassium formate fluids, as these brines remain stable at temperatures exceeding 180°C while providing the density and performance required for complex deep well drilling operations.

Potassium Formate Market Competitive Landscape

The global potassium formate market in 2026 is driven by demand for high-density HPHT drilling fluids, biodegradable de-icing solutions, and semiconductor-grade heat transfer fluids. Industry leaders are focusing on low-carbon production, supply chain integration, and high-purity liquid formate brines to meet stringent environmental and performance standards.

Perstorp Leads Low-Carbon Formate Transition with RE-Carbonization and Airport De-Icing Dominance

Perstorp is positioning itself as a sustainability leader in the potassium formate market through its RE-carbonization strategy, focusing on biogenic and recycled CO2 feedstocks. Its 2026 whitepaper outlines a pathway to low-carbon formate production aligned with EU green procurement mandates. The company commands a dominant share in Europe, supplying potassium formate to over 40% of airports due to its 80% lower corrosion profile compared to chloride-based de-icers. Its Swedish production base supports high-purity liquid formate brines widely used in automated dosing systems and offshore drilling fluids. Perstorp is also restructuring its supply chain to prioritize ESG-compliant sourcing, strengthening its appeal to North Sea operators. Its focus on sustainable, high-performance fluid solutions reinforces its premium positioning in the market.

BASF Strengthens Cost Leadership Through Verbund Integration and Hybrid Formate Technologies

BASF is leveraging its global Verbund infrastructure to maintain cost competitiveness in potassium formate production amid rising energy prices. The startup of its Zhanjiang site enhances regional supply capabilities and supports its Chemicals segment growth outlook for 2026. Its Formaplex 3.0 system integrates potassium formate with bio-based polymers, achieving a 40% reduction in freshwater usage in shale drilling applications. BASF’s strategic reorganization aligns formate production with its Performance Chemicals portfolio, enabling better value capture in specialty applications. The company is maintaining stable CO2 emissions despite capacity expansion through increased reliance on renewable electricity. Its integrated production model ensures scalability, efficiency, and compliance with evolving environmental regulations.

TETRA Technologies Expands High-Density Formate Fluids for Deepwater and HPHT Drilling Applications

TETRA Technologies is advancing its position in the potassium formate market by focusing on high-density completion fluids for deepwater and HPHT drilling environments. The company reported $631 million in 2025 revenue, with record EBITDA margins driven by strong demand in the Gulf of Mexico. Its R&D efforts are centered on ultra-high-density formate brines capable of maintaining thermal stability in reservoirs exceeding 10,000 feet. TETRA is integrating potassium formate solutions with produced water recycling and desalination projects, enhancing sustainability in oilfield operations. Its global footprint across six continents supports supply to rapidly growing markets, including China’s oil and gas sector. The company’s expertise in environmentally compliant drilling fluids positions it strongly in zero-discharge offshore operations.

Cabot Expands Specialty Formate Capacity and Targets Energy Storage Applications

Cabot is strengthening its role in the potassium formate industry through targeted investments and specialty chemical innovation. Its $75 million investment in a Texas production hub will deliver a 50,000-ton annual capacity by late 2026, focused on North American shale markets. The company reported a 2025 adjusted EPS of $7.25, reflecting steady financial performance and disciplined capital allocation. Cabot is exploring potassium formate as an electrolyte additive in lithium-ion batteries, targeting high-growth energy storage applications. Its EcoVadis Platinum rating enhances its competitiveness in environmentally sensitive offshore markets. By combining specialty chemicals expertise with sustainability credentials, Cabot is expanding beyond traditional oilfield applications into advanced energy solutions.

ADDCON Expands Green Chemistry Applications with VIAFORM De-Icing and Agricultural Integration

ADDCON is a niche leader in environmentally friendly potassium formate applications, particularly in de-icing and agriculture. Its VIAFORM® product line continues to dominate runway de-icing, with a 15% volume increase in Scandinavia as regions phase out sodium chloride. The company is expanding its presence in Asia-Pacific to meet rising demand for formate-based fertilizers that enhance nutrient uptake. ADDCON is also developing non-toxic preservation systems for animal feed, replacing conventional mineral acids with biodegradable alternatives. As part of the ICL Group, it leverages global logistics capabilities to reduce delivery times to remote industrial sites. Its focus on green chemistry and specialty applications strengthens its position in high-margin, sustainability-driven segments.

Sinochem Achieves Cost Leadership with Integrated Methanol Supply and High-Purity Formate Development

Sinochem is emerging as a low-cost leader in the potassium formate market through deep vertical integration with upstream methanol and oxo-aldehyde production. This integration has reduced variable costs by approximately 8%, enhancing competitiveness in global markets. The company is expanding into geothermal energy, supplying formate-based heat transfer fluids for projects like Kenya’s Menengai field. Its ISO tank leasing strategy enables flexible exports to Europe without heavy infrastructure investment. Sinochem is also advancing ultra-low-chloride formate grades for semiconductor cooling applications, meeting stringent impurity thresholds below 5 ppm. Its scale, cost efficiency, and innovation in high-purity applications position it strongly across both energy and electronics sectors.

Sweden: Carbon-Negative Feedstocks and Regulatory-Driven Market Exclusivity

Sweden has emerged as a global benchmark market for potassium formate, driven by carbon utilization, regulatory leadership, and tightly integrated supply chains. Perstorp Holding AB successfully executed its Formate 2025 initiative, embedding captured carbon dioxide from steel manufacturing directly into potassium formate production. This program reduced the product carbon footprint by 4.2 tonnes of CO₂ per tonne of potassium formate, positioning Sweden at the forefront of low-carbon formate chemistry. To support rising demand from transport infrastructure, Perstorp announced a 20% capacity expansion in late 2024 across its European hubs, specifically to supply 75% aqueous potassium formate solutions used in airport and highway de-icing applications.

Innovation breadth is expanding beyond de-icing. In March 2025, Perstorp launched the Neptem™ emulsifier range for waterborne alkyd technologies, where potassium formate functions as a performance stabilizer to improve film formation and storage stability. Swedish producers have also standardized the supply of ultra-high purity grades exceeding 99% to serve the rapidly advancing perovskite solar cell sector, where potassium formate acts as a reductant enabling reported efficiency levels of 23.8%. Regulatory conditions reinforce domestic demand. Swedish groundwater protection mandates designate potassium formate as the exclusive de-icing agent above sensitive aquifers, citing its rapid mineralization of 97% within 24 hours in soil. Following the 2024 acquisition of OQ Chemicals Nederland B.V., Swedish-owned entities now control one of Europe’s most extensive liquid formate logistics networks, strengthening supply reliability across Northern Europe.

Germany: Industrial Optimization and Cross-Sector Technology Integration

Germany’s potassium formate market is shaped by industrial efficiency gains, hybrid fluid innovation, and closed-loop manufacturing systems. In Q2 2024, BASF expanded its high-purity potassium formate capacity at Ludwigshafen by 15,000 tonnes annually, responding to cost pressures associated with alternative European heat transfer fluids. Product innovation followed in 2025 with the debut of Formaplex 3.0, a hybrid formulation combining potassium formate with bio-derived polymers that reportedly reduces freshwater consumption by 40% in industrial processing environments.

Energy and process technology applications are also gaining traction. Siemens Energy completed a pilot program in 2024 demonstrating that potassium formate used as a specialty electrolyte additive improved electrolyzer efficiency to 86%, outperforming conventional formulations. On the production side, ADDCON implemented cascade purification systems in 2025, cutting synthesis waste by 50% through closed-loop recovery. A joint venture formed in 2024 between ADDCON and Clariant is focused on substituting fossil-derived formic acid with agricultural waste feedstocks. In aviation, major German airports such as Munich reported markedly lower aluminum corrosion during the 2024–2025 winter season after transitioning runway maintenance operations to potassium formate-based fluids.

United States: Oilfield Performance and Strategic Domestic Capacity Build-Up

The United States potassium formate industry is increasingly anchored in oil and gas performance, battery recycling technologies, and domestic manufacturing expansion. In the Permian Basin, ExxonMobil reported a 20% reduction in wellsite contamination incidents in 2025 after replacing chloride-based drilling fluids with potassium formate brines. Performance advantages were also demonstrated offshore. On the Chevron Anchor Project in the Gulf of Mexico, the use of potassium formate fluids delivered a 30% faster drilling rate due to enhanced shale stabilization under high-pressure, high-temperature conditions.

Supply-side dynamics are shifting in response to policy and demand. Cabot Corporation announced a $75 million investment in a Texas facility targeting 50,000 tonnes per year of potassium formate capacity by 2026, supported by revised U.S. tariff schedules introduced in January 2025 that favor domestic formate production. Beyond energy, potassium formate is gaining relevance in circular technologies. A 2024 Department of Energy assessment highlighted its use by Redwood Materials to recover lithium at 92% efficiency. Environmental compliance is reinforcing adoption, with a 2024 DNV survey indicating that 67% of U.S. offshore operators now mandate zero-discharge drilling, a condition that strongly favors biodegradable potassium formate fluids.

China: Digitalized Logistics and Agricultural Efficiency Gains

China’s potassium formate market is defined by smart logistics deployment, production stability, and dual-use demand across agriculture and energy. In 2025, Hangzhou Focus Chemical partnered with Alibaba Cloud to implement AI-driven logistics systems, reducing emissions from domestic formate distribution by 25%. To preserve its net-zero status achieved in early 2024, Chinese producers are combining coal-to-formate production pathways with afforestation-based carbon offsets, reflecting a transitional approach to emissions management.

Production benchmarks remain stable. Shuntong Group maintained annual output of approximately 10,000 metric tonnes in 2025, supplying both domestic fertilizer applications and international oilfield markets. On the demand side, agronomy studies conducted during 2024–2025 showed that potassium formate-based foliar fertilizers improved nutrient uptake while reducing nitrogen leaching in rice paddies by 12%. These findings are reinforcing potassium formate’s role as a performance-enhancing and environmentally aligned input in Chinese agriculture.

Norway: Offshore Mandates and High-Volume Brine Specialization

Norway represents a structurally specialized market where regulatory mandates and offshore operating conditions directly shape potassium formate demand. New offshore rules effective from 2026 require all operators in Norwegian waters to deploy low-impact drilling fluids, firmly establishing potassium formate as the primary brine for high-pressure, high-temperature wells in the North Sea. This regulatory certainty has driven long-term supply alignment between operators and chemical producers.

Capacity is scaled to meet these requirements. ADDCON’s Norwegian facilities reported annual production capacity of approximately 800,000 barrels of potassium formate brine in 2025, supplying both offshore oilfield operations and Nordic aviation de-icing markets. Norway’s market profile is therefore defined by mission-critical applications where environmental compliance, fluid stability, and operational reliability are non-negotiable.

Comparative Overview of Country-Level Dynamics in the Potassium Formate Industry

Potassium Formate Market County Level Snapshot

|

Country

|

Strategic Focus Areas

|

Implications for Potassium Formate Demand

|

|

Sweden

|

CO₂-based feedstocks, de-icing regulation, solar applications

|

Leadership in low-carbon and ultra-high purity formates

|

|

Germany

|

Hybrid fluids, electrolyzer efficiency, closed-loop production

|

Growth in industrial and energy-related applications

|

|

United States

|

Oilfield performance, domestic capacity, battery recycling

|

Expanding demand across energy and circular technologies

|

|

China

|

Smart logistics, agriculture efficiency, stable capacity

|

Dual growth in fertilizers and oilfield uses

|

|

Norway

|

Offshore environmental mandates, HPHT drilling

|

Sustained high-volume demand for biodegradable brines

|

Potassium Formate Market Report Scope

Potassium Formate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$875.4 Million

|

|

Market Size (2034)

|

$1312.2 Million

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Form (Liquid, Solid), By Purity Grade (Industrial Grade, Technical Grade, Food & Feed Grade), By Application (Drilling & Completion Fluids, De-Icing & Anti-Icing Agents, Heat Transfer Fluids, Chemical Intermediates, Agriculture, Other Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Perstorp Holding AB, BASF SE, ADDCON GmbH, Clariant AG, Sinochem Group, Tetra Technologies Inc., Eastman Chemical Company, Thermo Fisher Scientific Inc., Hangzhou Focus Chemical Co. Ltd., Cabot Corporation, Roto Pumps Ltd., Shuntong Group, Evonik Industries AG, American Elements, Ava Chemicals Private Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Potassium Formate Market Segmentation

By Form

By Purity Grade

- Industrial Grade

- Technical Grade

- Food & Feed Grade

By Application

- Drilling & Completion Fluids

- De-Icing & Anti-Icing Agents

- Heat Transfer Fluids

- Chemical Intermediates

- Agriculture

- Other Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Potassium Formate Industry

- Perstorp Holding AB

- BASF SE

- ADDCON GmbH

- Clariant AG

- Sinochem Group

- Tetra Technologies Inc.

- Eastman Chemical Company

- Thermo Fisher Scientific Inc.

- Hangzhou Focus Chemical Co. Ltd.

- Cabot Corporation

- Roto Pumps Ltd.

- Shuntong Group

- Evonik Industries AG

- American Elements

- Ava Chemicals Private Limited

*- List not Exhaustive