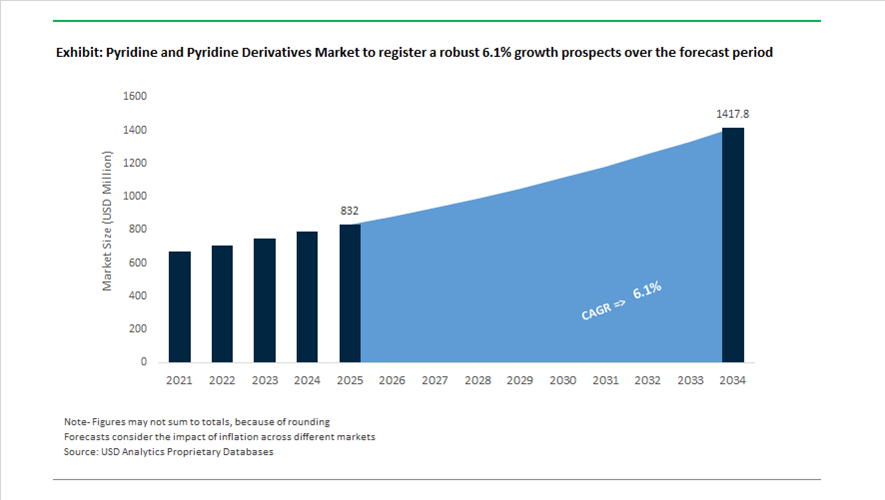

Pyridine and Pyridine Derivatives Market Valued at $832 Million in 2025, Projected to Reach $1,417.6 Million by 2034 at 6.1% CAGR

The global pyridine and pyridine derivatives market is valued at $832 million in 2025 and is projected to reach $1,417.6 million by 2034, expanding at a CAGR of 6.1%. Growth is driven by increasing demand for pyridine, alpha-picoline, beta-picoline, gamma-picoline, niacinamide (Vitamin B3), agrochemical intermediates, pharmaceutical building blocks, electronic-grade pyridine derivatives, and ionic liquid precursors. Applications span crop protection, APIs, animal nutrition, personal care actives, and semiconductor-related specialty chemicals. The market is transitioning toward higher-value downstream derivatives and sustainable synthesis technologies as feedstock optimization and environmental compliance gain priority.

Market stabilization became visible in late 2024, when global pyridine price volatility narrowed to approximately 5%, down from 12% in previous years. This shift reflected normalized logistics, improved regional stockpiling strategies, and reduced post-pandemic supply chain disruptions. In January 2024, Lonza launched a sustainable pyridine derivative line for pharmaceutical applications, utilizing greener synthesis pathways to reduce carbon intensity in API intermediates. In 2024, the World Economic Forum recognized Jubilant Ingrevia’s Bharuch facility as part of its Global Lighthouse Network, marking the first Indian chemical site acknowledged for deploying AI-driven process optimization and real-time analytics in pyridine synthesis. These advancements improved yield consistency, process safety, and energy efficiency.

Capacity and derivative expansion accelerated in 2025. In early 2025, Jubilant Ingrevia commissioned a new cGMP-compliant Niacinamide plant at Bharuch, targeting high-purity Vitamin B3 for human nutrition and cosmetic formulations. In May 2025, the company reported a 37% increase in annual profit, citing volume recovery in its pyridine and picoline portfolio following a global destocking phase. Jubilant also strengthened its CDMO pipeline in 2025, securing two new agro-CDMO contracts and advancing pyridine-based molecules across 8–10 semiconductor-related projects, signaling diversification beyond traditional agrochemical intermediates. In April 2025, Koei Chemical introduced its “KX2027” mid-term strategy, focusing on boosting profitability in core pyridine and pyrazine segments while accelerating development of high-value derivatives for advanced electronics and ionic liquid applications. In June 2025, Black Rose and Koei initiated a feasibility study for establishing new manufacturing hubs for specialized amine and pyridine products in South Asia.

Policy-driven growth in Asia further supports expansion. In August 2025, India enhanced its Production-Linked Incentive scheme with ₹1.97 lakh crore allocated across key sectors, including environmentally benign pyridine derivatives and APIs to promote domestic self-reliance. In September 2025, China’s Ministry of Industry and Information Technology announced a 2025–2026 growth stabilization plan targeting a 6% annual increase in chemical added value, encouraging expansion of high-efficiency pyridine synthesis facilities to support agrochemical demand.

The pyridine and pyridine derivatives market is increasingly defined by high-purity niacinamide production, agrochemical intermediate expansion, CDMO-driven specialty synthesis, AI-optimized pyridine manufacturing, semiconductor-related molecule development, sustainable pharmaceutical-grade derivatives, and policy-backed capacity growth in India and China. As derivative complexity increases and end-use industries diversify, regional manufacturing hubs and value-added downstream integration are reshaping competitive dynamics across the global pyridine value chain.

Key Trends and High-Value Opportunities in the Pyridine and Pyridine Derivatives Market

Environmental-Led Capacity Consolidation and Onshoring in China

The global pyridine and pyridine derivatives market is undergoing a structural reset as China tightens environmental enforcement under its “1+N” carbon peak and neutrality framework. Pyridine production has historically been fragmented, energy-intensive, and concentrated among small and mid-sized producers operating with limited waste treatment infrastructure. Between 2024 and 2025, the Chinese government’s Green and Low-Carbon Transition Industry Guidance Catalogue accelerated the shutdown or forced upgrading of non-compliant facilities, triggering rapid capacity consolidation into large, integrated chemical parks.

This regulatory tightening has had a direct cost and supply impact. The introduction of the “One Certificate for One Product” policy for high-toxicity pesticide intermediates has sharply reduced the number of approved pyridine-based registrations, eliminating inefficient producers and increasing pricing power for integrated leaders such as Nanjing Red Sun and Vertellus. As a result, pyridine pricing volatility is now increasingly linked to compliance-driven capacity rationalization rather than demand cycles alone.

At the same time, Chinese producers are actively decarbonizing their operations. Industrial output growth in China exceeded 5% annually between 2021 and 2024, while energy consumption growth remained close to 3%, reflecting a decoupling trend that has extended into pyridine manufacturing. By late 2025, leading producers had issued carbon-neutral bonds to finance renewable energy integration into ammonolysis and cyclization processes. These investments are reducing the carbon intensity of bulk pyridine and positioning compliant Chinese producers as preferred suppliers to multinational agrochemical and pharmaceutical customers facing Scope 3 emission disclosures.

Functional Pivot Toward Complex Intermediates for Next-Generation Agrochemicals

Demand growth in pyridine is increasingly being driven by functional complexity rather than bulk volume. As resistance management and environmental safety become central to crop protection strategies, agrochemical innovators are shifting toward pyridine-based “privileged scaffolds” that deliver higher target specificity at lower application rates. This pivot is reinforced by the European Union’s Regulation 2023/1234, which tightens thresholds on toxicity, persistence, and off-target impact.

China’s regulatory data underscores this shift. In 2024 alone, 167 pesticide Technical Concentrate registrations were recorded, nearly matching the combined total of the previous four years. A significant share of these new actives rely on pyridine derivatives such as alpha- and beta-picolines to enhance molecular selectivity and reduce environmental load. This surge has transformed pyridine derivatives from commodity intermediates into strategic inputs within global agrochemical R&D pipelines.

India is emerging as a complementary manufacturing hub for these higher-value derivatives. In late 2023, Jubilant Ingrevia commissioned a multipurpose agro-intermediate facility in Bharuch with fully backward-integrated pyridine capacity. The plant is designed to support customized, high-purity derivatives under long-term contracts, allowing the company to move away from cyclical spot markets and into more stable, innovation-driven supply relationships with multinational agrochemical companies.

High-Purity Pyridine Derivatives for the Antibody-Drug Conjugate Pipeline

The rapid expansion of targeted oncology therapies is creating one of the most attractive margin opportunities in the pyridine derivatives market. Antibody-drug conjugates have moved firmly into the commercial and late-stage development spotlight, with global ADC sales projected to exceed USD 16 billion in 2025. These therapies rely on highly specialized linker and payload chemistries, many of which incorporate pyridine rings to stabilize covalent bonds and control drug release.

By late 2025, more than 40 ADC candidates had entered Phase III clinical trials globally. Many of these programs utilize camptothecin-based payloads and peptide linkers where pyridine derivatives are critical for maintaining structural integrity and therapeutic index. Purity requirements frequently exceed 99.5%, shifting supplier selection toward manufacturers capable of cGMP production, full impurity profiling, and regulatory-grade documentation. This has allowed pyridine derivative suppliers in the pharmaceutical segment to command multiples of industrial-grade pricing.

Beyond oncology, pyridine remains a foundational building block in the synthesis of niacin and anti-tuberculosis drugs, sustaining baseline demand. However, capital deployment is increasingly concentrated in oncology-grade and rare-disease small molecules. Regulatory data from the U.S. FDA shows a continued increase in small-molecule drug approvals in 2024, reinforcing pyridine’s strategic relevance in advanced medicinal chemistry.

Electronic-Grade Pyridines for OLED Displays and Advanced Battery Materials

A greenfield opportunity is emerging for electronic-grade pyridine derivatives as organic electronics and next-generation energy storage scale globally. In OLED manufacturing, pyridine-based ligands play a critical role in phosphorescent emitters, particularly for deep-blue pixels where stability remains a bottleneck for device lifetime.

Research published in December 2025 demonstrated that substituted pyridine fluorophores can increase deep-blue OLED device lifetime by more than threefold by precisely tuning triplet and singlet excited state energies. This breakthrough is particularly relevant for smartphone displays, micro-displays, and emerging augmented reality applications, where durability directly influences product economics and warranty costs.

Parallel demand is developing in advanced battery materials. High-purity pyridine derivatives are being evaluated as electrolyte additives and coordination ligands in solid-state and moisture-sensitive battery chemistries. To support these applications, patent activity has intensified around advanced purification techniques, including amide-alkali metal pretreatment processes that remove trace pyrazine and water impurities. These refining routes enable the production of electronic-grade pyridine suitable for thin-film deposition and semiconductor-adjacent manufacturing, opening a premium niche well beyond traditional agrochemical and pharmaceutical uses.

Pyridine and Pyridine Derivatives Market Share and Segmentation Insights

Pyridine Dominates as Core Feedstock Driving Agrochemical and Pharmaceutical Intermediates Demand

Pyridine accounted for 48.60% of the Pyridine and Pyridine Derivatives Market by type in 2025, reflecting its foundational role as the parent heterocyclic compound used to synthesize picolines and downstream derivatives. It is widely utilized as an intermediate in agrochemicals, pharmaceuticals, industrial solvents, and denaturants, supported by large scale global production infrastructure. Pyridine serves as the backbone of the pyridine value chain, enabling production of alpha picoline, beta picoline, and gamma picoline for vitamins, crop protection chemicals, and specialty intermediates. In 2025, agrochemical demand remains the key consumption driver, with pyridine usage closely linked to paraquat and diquat herbicide production, particularly in Asia, influencing global supply demand dynamics and seasonal production patterns.

Pyridine and Pyridine Derivatives Market Competitive Landscape

The 2026 pyridine and pyridine derivatives market is transitioning toward high-purity pharmaceutical intermediates, CDMO services, and bio-based feedstocks. Competitive dynamics are shaped by cGMP manufacturing, zero-liquid-discharge systems, and continuous flow chemistry adoption across pharmaceutical, agrochemical, and nutritional applications.

Jubilant Ingrevia accelerates CDMO transformation with high-purity niacinamide and large-scale CapEx

Jubilant Ingrevia Limited is expanding its pyridine value chain through a ₹20 billion CapEx program focused on CDMO-driven growth and specialty intermediates. The company reported strong volume growth in FY26, with CDMO revenue projected to scale from ₹3 billion to ₹12 billion by FY28. Commissioning of a human-grade Vitamin B3 (niacinamide) facility in 2025 supports entry into high-spec infant nutrition and cosmetic markets. A $300 million multi-year agrochemical contract strengthens demand for pyridine-based intermediates. Organizational restructuring included significant leadership renewal and expansion of R&D talent to 150 scientists. Focus on complex heterocyclic chemistry enhances competitiveness in pharmaceutical and specialty chemical synthesis.

Aurorium strengthens high-purity pyridine derivatives portfolio for regulated pharmaceutical and agrochemical markets

Aurorium is focusing on specialty pyridine derivatives and cGMP-grade intermediates to serve regulated pharmaceutical and life sciences markets in North America and Europe. Strategic pricing adjustments implemented in late 2025 address feedstock volatility and margin pressures across beta picoline and derivative portfolios. The company remains a key supplier for FDA-regulated APIs and antihistamine production chains. Strong presence in agrochemical intermediates such as 2,6-dichloropyridine supports demand for precision herbicides in 2026. Integrated production and purification capabilities enable consistent supply of high-purity Vitamin B3 intermediates. Portfolio positioning emphasizes niche chemistries and regulatory-compliant manufacturing standards.

Nanjing Red Sun expands integrated pyridine chain to strengthen agrochemical dominance and cost leadership

Nanjing Red Sun Co., Ltd. is reinforcing its global position through vertical integration and expansion of low-cost pyridine production capacity. The Qujing High-Tech Zone project enhances supply of pyridine alkali and derivatives targeting Southeast Asian agrochemical markets. The company maintains over 45% global production share in paraquat and diquat, supported by capacity optimization and scale advantages. Integration across the pyridine method enables seamless production of chlorpyrifos and related intermediates. Strategic focus on economies of scale addresses pricing pressures, with Northeast Asia pyridine prices around $2.68/kg in early 2026. Industrial chain control supports competitiveness in large-volume herbicide applications.

Lonza advances pharma-grade pyridine derivatives with flow chemistry and sustainable sourcing

Lonza Group Ltd. is focusing on high-purity pyridine derivatives within its Small Molecules and Biologics segments, supported by 2025 revenue of CHF 6.7 billion. The company maintains a strong position in Vitamin B3 production, emphasizing human-grade niacinamide and sustainable sourcing practices. Adoption of precision catalysis and continuous flow chemistry improves yield efficiency and reduces environmental impact in European facilities. Strategic alignment with outsourced innovation trends supports demand from biotech firms requiring specialized intermediates. Optimization of small molecule capabilities enhances production of nitrogen heterocyclic compounds. Focus on green chemistry and pharma-grade purity supports growth in regulated markets.

Koei Chemical expands specialty pyridine derivatives with ionic liquids and custom synthesis capabilities

Koei Chemical Company, Limited is leveraging its expertise in nitrogen chemistry to expand into high-value pyridine derivatives and ionic liquid applications. The company reported steady recovery in its fine chemicals segment while diversifying into electrolytes and anti-static agents. Expansion of gas-phase and high-pressure reaction facilities supports rising demand for custom synthesis of specialized pyridine bases. Product portfolio includes amino-pyridines and 2-Methyl-5-Ethylpyridine (MEP) targeting catalysts in pharmaceuticals and food processing. Sustainability initiatives under the Responsible Care program focus on energy-efficient distillation and waste reduction. Technical specialization supports growth in electronics, advanced materials, and fine chemical applications.

India: API Self-Reliance, Agrochemical Exports, and Bio-Integrated Synthesis

India has emerged as a structurally strategic hub for pyridine and pyridine derivatives, driven by pharmaceutical security objectives and export-led agrochemical growth. Under the Production Linked Incentive Scheme for Bulk Drugs, the government has explicitly prioritized domestic synthesis of pyridine intermediates required for essential APIs such as isoniazid and amlodipine. This policy focus has accelerated capital deployment across Gujarat and Uttar Pradesh, enabling local producers to replace historically import-dependent intermediates with domestically manufactured, pharmacopeia-compliant pyridine derivatives. The commissioning of a new specialty pyridine derivatives plant by Jubilant Ingrevia in Bharuch during Q1 2024–2025 exemplifies this shift. The facility was designed to absorb a 15% increase in domestic demand from electronics, fine chemicals, and pharmaceutical synthesis while meeting tighter emission and solvent recovery norms.

Structural competitiveness is increasingly reinforced through vertical integration and sustainability alignment. By late 2025, Indian manufacturers achieved full backward integration for several pyridine-based intermediates using bio-ethanol-derived acetaldehyde, materially reducing carbon-to-product intensity and exposure to volatile petrochemical feedstocks. Parallel growth in agrochemical exports has been notable. Installed pesticide capacity reached 444,000 metric tons in 2024–2025, with pyridine-based herbicides such as paraquat and diquat contributing materially to shipments into Latin America. Environmental compliance has become a baseline rather than a differentiator, as leading hubs transitioned to Zero Liquid Discharge-certified operations using advanced oxidation to manage heterocyclic waste streams. India also retains global leadership in beta picoline processing, with Jubilant Ingrevia supplying niacinamide-grade picolines to more than 275 customers worldwide by early 2026, anchoring the country’s role in vitamin B3 value chains.

China: Capacity Rationalization, Integrated Chains, and Trade Defense

China continues to exert decisive influence over global pyridine supply through scale, integration, and regulatory control. In September 2025, the Ministry of Industry and Information Technology mandated an Equipment Renewal program targeting chemical reactors, compelling producers to retire high-emission pyridine synthesis units in favor of catalytic gas-phase condensation technologies. This regulatory intervention has tightened effective capacity while improving yield consistency and lowering byproduct toxicity. Supply chain integration has progressed in parallel. Shandong Luba Chemical completed a fully integrated pyridine-based route for chlorpyrifos production in 2025, establishing a domestic benchmark for purity and process efficiency under the specialized pyridine method.

China’s dominance in agrochemicals remains a structural driver. The country accounts for nearly 35% of global pesticide demand, with policy support directed toward intermediates such as 2,6-dichloropyridine for selective herbicides. Trade policy has been used to stabilize domestic pricing. In 2025, the Ministry of Commerce extended anti-dumping duties on pyridine imports from select Western regions, insulating local producers from price compression. Favorable feedstock economics have further reinforced margins. A sustained propylene surplus through late 2025 enabled producers to offset global petrochemical volatility, supporting competitive export pricing even amid environmental compliance tightening.

United States: Semiconductor Purity, Pharmaceutical Expansion, and Regulatory Tightening

The United States pyridine market is increasingly shaped by semiconductor manufacturing, pharmaceutical innovation, and regulatory scrutiny. As domestic chip fabrication accelerated under the CHIPS Act, demand for ultra-pure pyridine exceeding 99.9% purity rose by 11% through mid-2025, driven by its use as a solvent in advanced photolithography processes. This purity-driven demand has shifted procurement toward tightly controlled supply chains and closed handling systems. In pharmaceuticals, Veranova initiated a $30 million expansion at its Massachusetts facility during 2024–2025 to meet rising requirements for pyridine-based therapeutic intermediates and high-potency compounds.

Agrochemical demand has also rebounded. FMC Corporation reported a 23% improvement in North American crop protection sales in February 2025, supported by higher volumes of pyridine-derived insecticides. Regulatory pressure has intensified concurrently. The Environmental Protection Agency implemented stricter TSCA risk management rules for several pyridine derivatives in 2025, prompting widespread adoption of closed-loop synthesis and solvent recovery. Strategic sourcing has become a policy priority as well. Under the 2025 Executive Order on Supply Chain Resilience, the U.S. has encouraged friend-shoring of pyridine intermediates from India and Japan to secure supplies of essential vitamins and pharmaceutical precursors.

Germany and European Union: Compliance Economics and Selective Capacity Expansion

Within Europe, Germany anchors the pyridine and derivatives market through regulatory leadership and selective capacity investment. New REACH-aligned emission control mandates introduced in 2025 increased production costs for compliant manufacturers by an estimated 12 to 15%, structurally favoring large, integrated players such as BASF and Bayer. In response to rising demand for low-toxicity crop protection intermediates, Bayer expanded pyridine-based capacity at its Leverkusen site in 2024, aligning synthesis routes with next-generation formulation strategies.

Trade protection has reinforced domestic positioning. In July 2025, the European Commission imposed provisional anti-dumping duties of up to 120.8% on Chinese choline chloride imports, stabilizing pricing for EU-based feed additive producers. Energy transition measures are increasingly embedded in cost structures. By January 2026, more than 60% of German pyridine synthesis facilities had integrated renewable electricity or green hydrogen into thermal processes, reducing exposure to fossil energy volatility while supporting compliance with the EU Green Deal’s Chemicals Strategy for Sustainability.

Comparative Snapshot: Pyridine and Pyridine Derivatives by Country

Pyridine and Pyridine Derivatives Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Structural Industry Shift

|

|

India

|

APIs and agrochemical exports

|

PLI-driven localization, bio-ethanol feedstocks, ZLD compliance

|

|

China

|

Agrochemical scale and integration

|

Capacity rationalization, trade protection, feedstock advantage

|

|

United States

|

Semiconductors and pharmaceuticals

|

Ultra-pure grades, closed-loop compliance, friend-shoring

|

|

Germany / EU

|

Regulatory leadership and crop protection

|

Cost-driven consolidation, renewable energy integration

|

Pyridine and Pyridine Derivatives Market Report Scope

Pyridine and Pyridine Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$832 Million

|

|

Market Size (2034)

|

$1417.6 Million

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Type (Pyridine, Alpha Picoline, Beta Picoline, Gamma Picoline, Pyridine Derivatives), By Application (Agrochemicals, Pharmaceuticals, Industrial Solvents, Electronics, Food & Feed Additives)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Jubilant Ingrevia Limited, Vertellus Holdings LLC, Lonza Group AG, Koei Chemical Company Limited, Shandong Luba Chemical Co. Ltd., Bayer AG, Nippon Steel Chemical & Material Co. Ltd., Resonance Specialties Limited, Weifang Sunwin Chemicals Co. Ltd., Imperial Chemical Corporation, BASF SE, Red Sun Group, Mitsubishi Chemical Group, Novasyn Organics Pvt. Ltd., Trinseo PLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pyridine and Pyridine Derivatives Market Segmentation

By Type

- Pyridine

- Alpha Picoline

- Beta Picoline

- Gamma Picoline

- Pyridine Derivatives

By Application

- Agrochemicals

- Pharmaceuticals

- Industrial Solvents

- Electronics

- Food & Feed Additives

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Pyridine and Pyridine Derivatives Industry

- Jubilant Ingrevia Limited

- Vertellus Holdings LLC

- Lonza Group AG

- Koei Chemical Company Limited

- Shandong Luba Chemical Co. Ltd.

- Bayer AG

- Nippon Steel Chemical & Material Co. Ltd.

- Resonance Specialties Limited

- Weifang Sunwin Chemicals Co. Ltd.

- Imperial Chemical Corporation

- BASF SE

- Red Sun Group

- Mitsubishi Chemical Group

- Novasyn Organics Pvt. Ltd.

- Trinseo PLC

*- List not Exhaustive