Sachet Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Sachet Packaging Market Expected to Reach $16.4 Billion by 2034 Driven by Convenience and Sustainability Demands

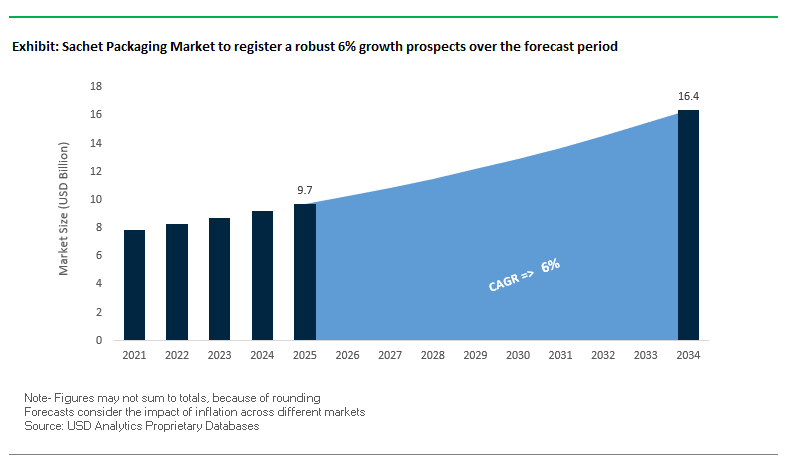

The global sachet packaging market is projected to grow from $9.7 billion in 2025 to $16.4 billion by 2034, at a CAGR of 6%. This growth is driven by single-serve convenience trends, innovative paper-based sachets, cost-effective market penetration strategies, and advanced protective features. Industry professionals can leverage these insights to identify growth opportunities, optimize packaging solutions, and respond to evolving consumer and regulatory demands.

Key Insights for industry decision-makers:

- Single-Serve Convenience: Around 50% of consumers in urban Asia-Pacific and Latin America frequently purchase single-serve or trial-size sachets, with adoption rising globally.

- Paper-Based Innovation: Leading companies are launching recyclable paper-based sachets compatible with existing form-fill-seal (FFS) lines, enhancing sustainability.

- Cost-Effectiveness: Sachets allow brands to enter emerging markets affordably, making products like shampoo, coffee, and condiments accessible to wider audiences.

- Durability and Protection: Advanced laminates provide oxygen, moisture, and grease barriers, ensuring longer shelf life for items like powdered beverages and instant coffee.

- Sustainability Focus: Transition to paper-based and mono-material sachets aligns with circular economy goals.

- Market Expansion Opportunities: Growth is supported by food, beverage, personal care, and pharmaceutical applications, with increasing demand for eco-friendly packaging solutions.

The sachet packaging market presents a convergence of consumer convenience, sustainability, and product protection, creating significant opportunities for global packaging manufacturers.

Market Analysis: Industry Consolidation, Sustainability Investments, and Paper-Based Innovations Are Redefining Sachet Packaging

The sachet packaging sector has experienced significant consolidation and sustainability-led innovation. In August 2025, Mondi ramped up production of its FunctionalBarrier Paper Ultimate, a high-barrier paper-based solution for sachets and stickpacks, following a €16 million investment in its Solec plant. In the same month, Constantia Flexibles completed the acquisition of Aluflexpack, enhancing its presence in high-value segments, including pharmaceuticals and food. The Amcor-Berry Global merger in August 2025 created a diversified packaging leader with strong global reach in both flexible and rigid formats.

Sustainability innovations have driven the shift toward paper-based and recyclable materials. In June 2025, Mondi launched a sustainable sachet solution for pet food, reflecting the increasing emphasis on environmentally friendly packaging. Similarly, ProAmpac’s April 2025 PRO-POUCH® line offers eco-friendly rollstock and pre-made pouches, aligning with the broader push toward circular packaging.

Strategic divestments and partnerships are further shaping market dynamics. Sonoco’s April 2025 sale of Thermoformed and Flexibles Packaging to TOPPAN Holdings for US$1.8 billion allowed the company to concentrate on core paper and flexible packaging businesses, while February 2025 Mondi-Proquimia collaboration on paper-based stand-up pouches for dishwashing tabs underscores innovation in plastic replacement for household products.

Sachet Packaging Market: Trends and Opportunities Reshaping Single-Use Formats

Regulatory Scrutiny and Pending Bans on Single-Use Plastics

One of the most defining trends in the sachet packaging market is the growing regulatory scrutiny surrounding single-use plastics. In India, the Plastic Waste Management (Amendment) Rules, 2021 and 2022 banned the manufacture, sale, and distribution of several single-use plastic products deemed to have low utility and high littering potential. While sachets for shampoos and similar products were initially excluded, the legislative framework has set a clear precedent for future bans, with State and Union Territory governments already developing elimination plans. Globally, this momentum is accelerating. The European Union’s directive on single-use plastics has become a cornerstone of regulatory policy, while negotiations for a UN Global Plastics Treaty are amplifying international pressure on corporations. This policy environment is forcing FMCG leaders to reconsider the viability of multi-laminate sachets, which remain notoriously difficult to recycle, and explore circular, compliant alternatives.

Corporate Pilots of Reusable and Refillable Systems as Alternatives

Parallel to regulatory developments, FMCG corporations are piloting large-scale refill and reuse systems to reduce dependence on sachets. Since 2018, Unilever has initiated over 50 refill pilots globally, including projects in Indonesia, Bangladesh, and Sri Lanka. These pilots range from in-store refill machines to door-to-door motorcycle refill services, designed to address local infrastructure challenges. In 2025, Unilever expanded efforts by deploying manual refill stations across 1,000 retail outlets in Indonesia, serving an estimated 6,000 customers and reducing plastic use by approximately 6 metric tons annually. These initiatives demonstrate a growing industry shift toward scalable alternatives that not only align with regulatory frameworks but also build stronger consumer loyalty through sustainable engagement. The expansion of refill and reuse is likely to accelerate as companies seek to align with corporate ESG goals and evolving consumer expectations.

Development of Certified Home-Compostable Material Structures

The absence of formal recycling infrastructure in many sachet-heavy markets presents a significant opportunity for certified home-compostable packaging solutions. Manufacturers are investing in bio-based material blends derived from eucalyptus, cassava root, and other renewable sources, designed to decompose fully in a home composting environment within 12 months. These structures are certified for compostability and engineered with high-barrier properties to protect moisture- and oxygen-sensitive products such as coffee, condiments, and snack foods. A technical overview from a leading supplier highlights compostable sachets capable of achieving barrier performance equivalent to conventional plastic laminates, but without contributing to persistent waste. For brands, adopting these materials provides a differentiated sustainability narrative in markets where consumers increasingly value environmental responsibility, while also ensuring compliance with pending bans and EPR-driven mandates.

Integration of Digital and Smart Features for Consumer Engagement

Another major opportunity lies in transforming sachets into digital engagement tools through smart technologies. With limited physical surface area, sachets are now being used as digital portals via embedded QR codes or digital watermarks. A 2025 report on digital product passports highlights that consumers can scan codes to access detailed ingredient disclosures, recycling instructions, and brand sustainability commitments, building trust and transparency. Beyond consumer engagement, unique IDs serve as tools for anti-counterfeiting and supply chain visibility. According to the Alliance to End Plastic Waste, watermark-enabled sachets can capture valuable data on product movement, helping brands optimize logistics and personalize marketing. This convergence of smart technology with packaging sustainability presents a dual opportunity: reducing environmental impact while enhancing consumer-brand interaction in emerging and developed markets alike.

Competitive Landscape: Leading Sachet Packaging Companies Are Driving Innovation, Sustainability, and Market Diversification

The sachet packaging market is highly competitive, with top players leveraging mergers, sustainability, and innovation to meet growing consumer and regulatory demands. Companies excel in producing durable, recyclable, and high-barrier sachets for food, personal care, and pharmaceutical applications.

Amcor plc: Advancing Sustainable Sachets and Flexible Packaging Solutions Globally

Amcor offers a broad portfolio of sachet and stickpack solutions for food, personal care, and healthcare products. The August 2025 merger with Berry Global created a global powerhouse with diversified product offerings and geographic reach. Amcor’s AmFiber Performance Paper heat-seal sachets and recycle-ready stickpacks combine sustainability with high-performance barrier properties. Its films are engineered for high-speed sachet machines, enabling features like easy-open tears and contamination-resistant seals.

Mondi Group: Pioneering Paper-Based High-Barrier Solutions for Eco-Friendly Sachets

Mondi provides FunctionalBarrier Paper Ultimate, a sustainable alternative to multi-layer plastics and aluminum. In August 2025, production ramped up following a €16 million investment. Mondi’s MAP2030 commitments aim for 100% reusable, recyclable, or compostable products by 2025. Its integrated value chain and FlexStudios innovation hubs ensure secure raw material supply and collaboration with customers on sustainable sachet solutions.

Huhtamaki Oyj: Delivering Mono-Material Sachets for Circular Economy Packaging

Huhtamaki specializes in sustainable sachet and pouch solutions for food and personal care. Its blueloop™ platform provides mono-material solutions in paper, PE, and PP Retort, simplifying recycling. The company targets 100% recyclable, compostable, or reusable packaging by 2030, combining sustainability with affordability and robust product protection. Huhtamaki’s solutions include juice, milk-based drinks, and powdered beverages, offering high-quality printing and lightweighting benefits.

Sonoco Products Company: Strengthening Recyclable Flexible Packaging Capabilities

Sonoco offers flexible sachets for snacks, coffee, and powdered beverages, emphasizing recyclability and high-barrier protection. In August 2025, it invested $30 million in Orlando, Florida, enhancing paper and recycling capabilities. Divestment of non-core businesses in April 2025 allowed focus on core sachet solutions, supporting advanced barrier technologies crucial for food and beverage shelf life.

Constantia Flexibles: Expanding High-Performance Mono-Material Sachets Across Europe

Constantia Flexibles delivers a broad portfolio of sachets and stickpacks for food, pharmaceuticals, and personal care. The August 2025 acquisition of Aluflexpack strengthened its European footprint. Innovations include retortable mono PP pouches for high-heat applications like wet pet food and ready meals, aligning with European PP recycling streams. Constantia focuses on reducing material use while maximizing recyclability, enhancing its leadership in sustainable flexible packaging.

Sachet Packaging Market Share Insights, 2025-2034

Three-Side Seal Sachets Hold the Largest Share by Product Type in the Sachet Packaging Industry

Three-side seal sachets dominate the sachet packaging market with a 40% share, reflecting their unmatched efficiency and cost-effectiveness across high-volume product categories. Leveraging vertical form-fill-seal (VFFS) machinery, these sachets deliver unparalleled throughput for food, pharmaceuticals, and personal care applications. Their balance of material efficiency, branding space, and durability secures their leadership, especially in emerging markets where affordability is paramount. This format’s adaptability across product categories—from condiments and instant beverages to topical creams and medicines—ensures it remains the global standard for sachet packaging production.

Food & Beverages Lead Market Share by End-Use in the Sachet Packaging Industry

The food and beverages sector commands 45% of sachet packaging demand, making it the single largest end-use driver. Sachets are widely adopted for portion-controlled products such as sauces, ketchup, instant coffee, spices, and cooking oils, where affordability, convenience, and food waste reduction are key. Their role in foodservice and takeaway ecosystems reinforces their dominance, while the affordability of sachets continues to expand market penetration in emerging economies. The combination of high consumer turnover, convenience-driven lifestyles, and retail demand for single-serve packaging cements food and beverages as the growth anchor of the sachet packaging industry.

European Union: PPWR, ESPR, and Investment in Plant-Based Alternatives Reshaping Sachet Packaging

The European Union sachet packaging market is undergoing rapid transformation under the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. The legislation is pushing brands to move away from multi-material plastics, traditionally used in sachets, toward mono-material and paper-based formats that can be more easily recycled. With mandatory recycled content targets and reuse requirements, sachet packaging manufacturers are increasingly re-engineering barrier films to balance performance with recyclability.

The Ecodesign for Sustainable Products Regulation (ESPR), effective mid-2024, is also a game-changer, as it requires a Digital Product Passport (DPP) disclosing material composition, recyclability, and compliance. Additionally, PFAS restrictions in food-contact sachet packaging from August 2026 are spurring innovation in new barrier coatings. Investment flows are accelerating this shift—Xampla (UK) secured $14 million to commercialize plant-based alternatives for sachets, while Paptic Ltd (Finland) raised EUR 27.5 million to scale wood-fiber-based sachet materials. These developments highlight how regulatory pressure and sustainable material funding are reshaping sachet formats in food, personal care, and household applications across the EU.

United States: EPR Expansion, EPS Bans, and Smart Sachet Innovations Driving Market Growth

The United States sachet packaging market is being reshaped by regulatory, technological, and consumer forces. Seven states now have Extended Producer Responsibility (EPR) laws, including Maryland, which requires Producer Responsibility Organizations (PROs) to cover 90% of packaging waste costs by 2030, compelling FMCG companies to redesign sachets for recyclability. At the federal level, the U.S. EPA’s national recycling target of 50% by 2030 is directly influencing investments in recycling-friendly sachet materials.

Market demand for single-serve and portion-controlled sachets remains strong, particularly in foodservice and pharmaceuticals, where sachets provide affordability, hygiene, and convenience. Regulatory measures are also shaping the landscape; California’s January 1, 2025 ban on EPS foodservice ware is accelerating adoption of alternative sachet packaging materials. On the innovation side, startups in healthcare are introducing smart sachets with printed electronics and sensors, designed to track medication adherence and improve patient outcomes. These factors make the U.S. a leader in blending sustainability mandates with digital innovation in sachet packaging.

China: E-Commerce Growth and Regulatory Enforcement Boosting Eco-Friendly Sachets

The China sachet packaging market is benefiting from the country’s 14th Five-Year Plan, which prioritizes plastic pollution reduction and green growth. From June 1, 2025, express delivery companies are legally required to adopt eco-friendly and reusable packaging solutions, a move that has strong implications for sachets used in logistics, e-commerce, and foodservice.

China’s booming e-commerce sector is fueling the need for lightweight, flexible sachet packaging that ensures cost efficiency while reducing environmental impact. Domestic players such as JDL Express and SF Express are increasingly shifting to reusable formats and recyclable laminates. At the same time, the government is promoting remanufacturing industries and tax incentives for companies investing in green technologies. Together, these measures are aligning China’s sachet packaging industry with broader circular economy objectives, especially for high-volume FMCG products.

India: EPR Regulations and Cost-Sensitive Demand Expanding Sachet Packaging Applications

The India sachet packaging market is shaped by the Plastic Waste Management (Amendment) Rules, 2024, which reinforce Extended Producer Responsibility (EPR) for producers and brand owners. Unlike earlier frameworks, PIBOs (Producers, Importers, Brand Owners) are no longer required to collect back multi-layered plastic sachets, but they must still meet EPR obligations through recycling credits and partnerships.

The Food Safety and Standards Authority of India (FSSAI) has intensified scrutiny on food-grade sachet packaging by mandating migration testing for flexible materials, while from July 1, 2025, all sachets must carry traceable barcodes or QR codes to enhance accountability. Despite these regulatory pressures, sachets remain a staple in India’s price-sensitive market, covering categories like snacks, condiments, shampoos, and personal care items. Local SMEs benefit from exemptions under EPR, but large FMCG brands face mounting compliance and material innovation challenges. Overall, India represents a high-volume, regulation-driven sachet packaging market with a strong emphasis on balancing affordability with environmental accountability.

Japan: Plastic Resource Circulation Laws and Paper-Based Sachet Innovations

The Japan sachet packaging market is progressing under the Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, also effective 2025, specifically mandates the reduction or redesign of 12 single-use plastic categories, directly influencing sachet packaging manufacturers.

Japanese firms are pioneering in sustainable material innovation, particularly for sachets. Nippon Paper Industries has developed SHIELDPLUS, a paper with oxygen- and odor-barrier properties, making it suitable for sachets in food and personal care applications. At the same time, Japan’s goal of doubling renewable material use by 2030 is accelerating the adoption of compostable and bio-based sachet formats. The country’s combination of regulatory enforcement and material science leadership is positioning it as a hub for next-generation paper and bio-polymer sachets.

Brazil: Reverse Logistics and Solid Waste Law Supporting Sustainable Sachet Packaging

The Brazil sachet packaging market is governed by the National Solid Waste Policy (PNRS), which emphasizes recycling, reuse, and waste reduction. A landmark development was the enactment of Law No. 15,088 in January 2025, which bans the import of plastic, paper, glass, and metal waste, thereby strengthening the domestic recycling ecosystem.

Brazil has also expanded its reverse logistics framework, making producers responsible for collecting and recycling post-consumer sachets and other packaging. The growing adoption of MAP (Modified Atmosphere Packaging) films and vacuum-sealed sachets in the food industry reflects a trend toward extending product shelf life while reducing waste. These policies and innovations underline Brazil’s movement toward a circular sachet packaging economy, with sustainability becoming a competitive advantage for FMCG manufacturers.

Sachet Packaging Market Report Scope

Sachet Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.7 Billion

|

|

Market Size (2034)

|

$16.4 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Material (Plastic, Paper, Aluminium Foil, Biodegradable Materials), By Product Type (Two-Side Seal, Three-Side Seal, Four-Side Seal, Stick Packs), By End-Use Industry (Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals, Industrial & Chemicals, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Huhtamaki Oyj, Mondi Group, Sonoco Products Company, ProAmpac, Constantia Flexibles, Sealed Air Corporation, DS Smith Plc, Tekni-Plex, Inc., WestRock Company, Pactiv Evergreen Inc., Smurfit Kappa Group Plc, Rengo Co., Ltd., Graphic Packaging Holding Company, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sachet Packaging Market Segmentation

By Material

- Plastic

- Paper

- Aluminium Foil

- Biodegradable Materials

By Product Type

- Two-Side Seal

- Three-Side Seal

- Four-Side Seal

- Stick Packs

By End-Use Industry

- Food & Beverages

- Personal Care & Cosmetics

- Pharmaceuticals

- Industrial & Chemicals

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sachet Packaging Market

- Amcor plc

- Huhtamaki Oyj

- Mondi Group

- Sonoco Products Company

- ProAmpac

- Constantia Flexibles

- Sealed Air Corporation

- DS Smith Plc

- Tekni-Plex, Inc.

- WestRock Company

- Pactiv Evergreen Inc.

- Smurfit Kappa Group Plc

- Rengo Co., Ltd.

- Graphic Packaging Holding Company

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and integrated research methodology to deliver actionable insights into the global sachet packaging market. Our approach combines in-depth secondary research, including corporate filings, industry reports, sustainability disclosures, and regulatory documents, with primary interviews involving packaging manufacturers, FMCG brand owners, recyclers, and supply chain stakeholders across food & beverages, personal care, pharmaceuticals, and industrial sectors. Market sizing and forecasts account for materials (plastic, paper, aluminium foil, biodegradable), product types (two-side, three-side, four-side seal sachets, stick packs), and regional regulations such as the EU PPWR and ESPR, U.S. EPR laws, India’s Plastic Waste Management Rules, China’s 14th Five-Year Plan, Japan’s Plastic Resource Circulation Strategy, and Brazil’s PNRS. The analysis also evaluates sustainability-led innovations including paper-based sachets, mono-material formats, home-compostable materials, and smart packaging features like QR codes and digital watermarks. Additionally, USDAnalytics assesses technological advances in barrier properties, high-speed form-fill-seal machinery, and lightweighting strategies that enhance efficiency, product protection, and environmental performance. This comprehensive methodology ensures industry professionals obtain precise, market-driven insights into competitive dynamics, regulatory impacts, growth opportunities, and investment strategies shaping the sachet packaging industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.