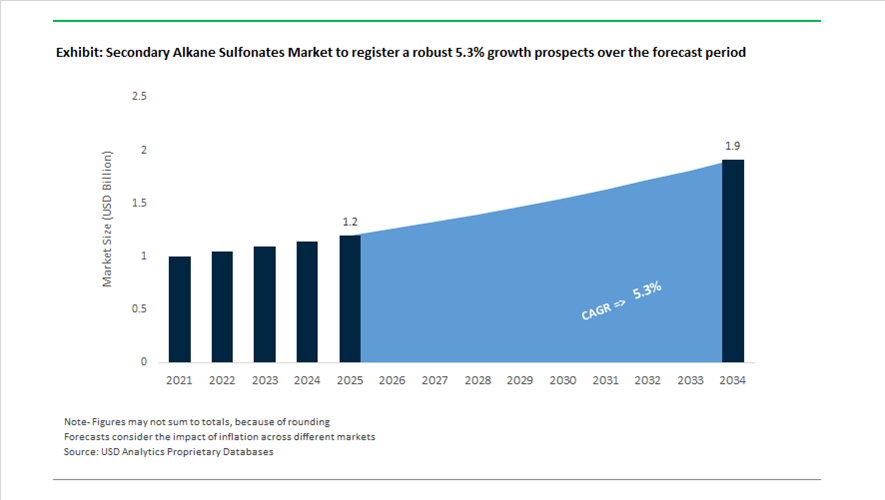

Secondary Alkane Sulfonates Market Valued at $1.2 Billion in 2025, Projected to Reach $1.9 Billion by 2034 at 5.3% CAGR

The global secondary alkane sulfonates (SAS) market is valued at $1.2 billion in 2025 and is projected to reach $1.9 billion by 2034, expanding at a CAGR of 5.3%. Growth is driven by increasing demand for biodegradable anionic surfactants, high-foaming detergent actives, cold-water laundry surfactants, industrial cleaning formulations, and PFAS-free specialty surfactants used in home care, dishwashing liquids, hard-surface cleaners, and institutional sanitation products. SAS continues to gain share against linear alkylbenzene sulfonates (LAS) due to its superior biodegradability, calcium tolerance, and stable foaming profile under varying water hardness conditions. Regulatory pressure under EU REACH and North American environmental frameworks is accelerating the transition toward surfactants with favorable ecotoxicological and wastewater treatment profiles.

Capacity expansion and sustainability repositioning shaped 2024–2025. In December 2024, Clariant announced an investment of approximately CHF 80 million to expand its Care Chemicals production at its Dayawan, China site, strengthening output of high-performance surfactants including SAS to serve Asia’s fast-growing personal and home care segments. By the end of 2024, Clariant completed its transition to a fully PFAS-free additive portfolio, reinforcing SAS positioning within green chemistry frameworks. Throughout 2025, WeylChem Performance Products upgraded its European facilities to optimize Hostapur® SAS production, focusing on lowering energy intensity in the sulfoxidation process and improving feedstock utilization efficiency. Simultaneously, stricter EU REACH compliance contributed to a measurable uptick in biodegradable surfactant demand, with SAS emerging as a preferred alternative in both consumer and institutional formulations.

Technological and regional shifts intensified in 2025–2026. In September 2025, a major global chemical producer entered a biotechnology partnership to develop bio-based SAS derived from renewable paraffin substitutes, targeting partial decoupling from fossil-based n-paraffins. Advancements in 2025 also included the commercialization of low-temperature optimized SAS grades engineered for effective performance at 20°C, aligning with global energy conservation initiatives and cold-wash detergent reformulation trends. In early 2026, North American manufacturers accelerated supply chain regionalization strategies in response to trade realignments and tariffs on intermediates, reinforcing domestic SAS production for dishwashing and industrial cleaner applications.

Broader specialty chemical consolidation also influenced the value chain. In February 2026, Henkel announced the acquisition of Stahl Holdings, indirectly impacting surfactant procurement dynamics due to Henkel’s scale in detergent and cleaning formulations. Meanwhile, Clariant’s development of titanium-based AddWorks™ solutions in 2026 reflected a parallel industry-wide movement toward heavy-metal-free processing technologies that complement SAS’s environmentally favorable profile.

The secondary alkane sulfonates market is increasingly defined by PFAS-free surfactant portfolios, renewable feedstock development, energy-efficient sulfoxidation processes, cold-water detergent compatibility, regional supply localization, and strict EU REACH-driven biodegradability compliance. As formulators prioritize performance under sustainability constraints, SAS remains a structurally advantaged surfactant within the global detergent and specialty cleaning chemicals ecosystem.

Key Trends and High-Value Opportunities in the Secondary Alkane Sulfonates Market

Strategic Shift Toward I&I Hard Surface Cleaners and Professional Hygiene Systems

The industrial and institutional cleaning segment has become the most structurally resilient demand pillar for Secondary Alkane Sulfonates, driven by stricter hygiene protocols across food processing, healthcare, and public infrastructure. Compared with Linear Alkylbenzene Sulfonate, SAS offers superior chemical robustness, enabling consistent performance in aggressive clean in place systems where exposure to both acidic and alkaline conditions is routine. This resilience is particularly valuable for food and beverage plants and hospital sterilization environments, where formulation failure directly translates into compliance and safety risks.

Performance validation has accelerated adoption. Updated 2025 performance data from Clariant confirms that SAS retains structural stability across a pH window of 1.0 to 12.0, allowing formulators to develop highly concentrated degreasers without compromising efficacy. These concentrates enable up to a 35% reduction in plastic packaging volumes, aligning with enterprise-level ESG targets that now extend beyond consumer products into B2B hygiene procurement. As multinational facility managers move toward fewer, stronger formulations that can be diluted on site, SAS-based systems are increasingly specified as default surfactant platforms.

Another accelerant is disinfectant compatibility. Following the European Parliament’s detergent safety resolution in early 2024, formulators have prioritized surfactants that do not inhibit antimicrobial actives. SAS has demonstrated strong synergy with quaternary ammonium compounds, functioning as an effective wetting agent that improves surface contact and uniform coverage on non-porous substrates. This compatibility is reinforcing SAS adoption in hospital-grade disinfectants, where achieving 99.9% surface contact is now a baseline expectation rather than a premium feature.

Dominance in Cold-Wash and Water-Scarce Laundry Markets

Rising energy prices and chronic water stress are reshaping global laundry habits, particularly in Asia-Pacific, the Middle East, and parts of Africa. These conditions are accelerating the shift toward cold-water detergency, where SAS has emerged as one of the most technically advantaged anionic surfactants. Its molecular structure prevents calcium salt precipitation, allowing it to maintain cleaning efficiency even at low temperatures and high water hardness.

Industry briefs published in 2025 indicate that SAS remains fully soluble at wash temperatures as low as 15°C, a threshold where LAS-based formulations frequently leave residues and dull fabrics. This characteristic enables detergent manufacturers to market cold-wash and eco-mode compatible products capable of cutting household laundry energy consumption by approximately 60%. As appliance manufacturers increasingly promote low-temperature cycles as default settings, surfactant performance at reduced thermal input has become a decisive formulation criterion.

Hard-water resilience further strengthens SAS economics. In markets such as India and the Gulf Cooperation Council, where water hardness often exceeds 300 ppm, SAS is being deployed as a primary or co-surfactant to reduce dependence on costly builders like phosphates and zeolites. Strategic capacity expansion in China’s Daya Bay region, including a CHF 80 million investment completed by late 2025, underscores the industry’s focus on supplying Asia-Pacific markets where detergent cost optimization and performance consistency under mineral stress are critical competitive levers.

Expansion into High-Purity Personal Care and Skin-Friendly Cosmetic Formulations

A structurally attractive opportunity is emerging in cosmetic-grade and ultra-high-purity SAS for personal care applications. As clean beauty and skin-sensitivity concerns reshape formulation strategies, SAS is being repositioned as a biodegradable, low-irritancy alternative to harsher anionic surfactants in shampoos and body washes. This repositioning is supported by a growing body of regulatory-aligned toxicological evidence.

Updated 2024–2025 studies published in peer-reviewed journals demonstrate that secondary alkane sulfonates exhibit significantly lower aquatic toxicity than legacy branched surfactants. This data is increasingly being used by global personal care brands such as L’Oréal and Beiersdorf to justify reformulation decisions that align with ISO 16128 natural-origin benchmarks while maintaining cleansing performance. For formulators, SAS offers a rare balance of regulatory defensibility and technical reliability.

The premiumization opportunity lies in ultra-high-purity and salt-free SAS variants. These grades are being positioned for sulfate-free hair care products, where foam quality and mildness are critical purchase drivers. With the personal care ingredients market valued at approximately USD 21.8 billion in 2025 and sulfate-free formulations growing around 1.2 times faster than conventional hair care, suppliers that can deliver cosmetic-grade SAS with consistent purity profiles are well placed to capture above-average margins.

Cost-Effective Surfactant Platform for Chemical Enhanced Oil Recovery

Beyond detergents and personal care, SAS is gaining strategic relevance in the energy sector as a value-engineered surfactant for Chemical Enhanced Oil Recovery. In mature onshore reservoirs, particularly across the Middle East and parts of Asia, operators are seeking alternatives to expensive specialty surfactants that can still deliver meaningful recovery uplift.

Pilot projects conducted during 2024 and 2025 demonstrate that SAS, when deployed in Alkali-Surfactant-Polymer flooding systems, can reduce interfacial tension to the order of 10⁻³ mN/m. This level of performance enables mobilization of residual oil that is otherwise uneconomic to recover, with incremental recovery improvements estimated between 12 and 18% in sandstone reservoirs. For operators managing late-life assets, these gains materially extend field economics without large capital outlays.

Thermal and salinity resilience further enhance SAS competitiveness. Unlike many bio-based surfactants that degrade under reservoir conditions, SAS maintains stability at temperatures up to 90°C and performs reliably in high-salinity formations. Combined with a production cost structure that is roughly 20% lower than premium EOR surfactants, SAS is increasingly viewed by national oil companies as a pragmatic solution for maximizing asset value amid volatile crude price environments.

Secondary Alkane Sulfonates Market Share and Segmentation Insights

Industrial Grade Secondary Alkane Sulfonates Lead Market Consumption Across Detergent and Industrial Cleaning Applications

Industrial grade secondary alkane sulfonates accounted for 48.60% of the secondary alkane sulfonates market in 2025, reflecting their dominant use in high-volume cleaning formulations. Industrial grade SAS are widely utilized in household detergents, industrial and institutional cleaning products, and textile processing chemicals, where cost efficiency and proven surfactant performance are essential. These anionic surfactants deliver strong wetting, emulsification, and detergency performance across a wide pH range, making them highly suitable for large-scale cleaning applications. A key 2025 industry shift is the grade migration toward higher purity SAS, particularly for personal care applications. While industrial grade continues to lead by volume, manufacturers are expanding purification capacity to produce cosmetic grade SAS for mild surfactant systems in premium personal care formulations.

Household Detergents & Cleaners Drive Global Demand for Secondary Alkane Sulfonates

Household detergents and cleaners represent the largest application segment in the secondary alkane sulfonates market, accounting for 42.80% of total demand in 2025 due to the extensive use of SAS in laundry detergents, all-purpose cleaners, and specialty household cleaning products. SAS surfactants provide strong hard water tolerance, biodegradability, and effective grease removal, making them widely adopted in both liquid and powder detergent formulations. Demand continues to grow alongside global consumption of liquid laundry detergents and multi-surface cleaning products. A major 2025 product development trend is the rise of concentrated detergent formulations and unit-dose pods, where SAS surfactants are optimized for higher active content and compatibility with water-soluble film packaging, enabling efficient cleaning performance in compact detergent formats.

Secondary Alkane Sulfonates Market Competitive Landscape

The 2026 secondary alkane sulfonates (SAS) market is driven by biodegradable n-paraffin surfactants, cosmetic-grade C14–C17 formulations, and halogen-free sulfoxidation processes. Growth is supported by REACH and EPA regulations, increasing demand for label-friendly detergents, and high-purity emulsifiers in polymer and personal care applications.

Clariant leads high-purity SAS innovation with Hostapur platform and halogen-free sulfoxidation technology

Clariant AG maintains technical leadership in the SAS market through its Hostapur® portfolio of high-active, biodegradable surfactants. Hostapur® SAS 93 is widely used as an emulsifier in E-PVC, SBR, and nitrile rubber production, offering stability in high-electrolyte systems. The Hoechst light/water sulfoxidation process eliminates chlorinated intermediates, supporting green chemistry compliance. Expansion of Hostapur™ OS and OSB grades targets crop protection formulations requiring superior wetting performance. All SAS grades meet strict biodegradability standards for household and industrial cleaning applications. Focus on high-purity, label-friendly surfactants supports demand across detergents and polymer emulsification.

WeylChem strengthens SAS supply reliability with advanced manufacturing and multifunctional surfactant solutions

WeylChem Group is expanding its SAS footprint through custom manufacturing and high-performance cleaning formulations. WeylClean® SAS 30 delivers strong degreasing performance with dermatological compatibility for both personal care and industrial applications. A €7 million multi-purpose plant in France enhances production of complex sulfonates using automated and corrosion-resistant systems. Integration of Catexel improves catalyst efficiency in bleaching and cleaning systems where SAS plays a central role. Focus on European supply chain stability positions its SAS portfolio as an alternative to imports. Emphasis on I&I cleaning applications supports demand for high-efficiency surfactants.

LANXESS optimizes sulfonation capabilities with cost-efficiency strategy and high-purity specialty applications

LANXESS AG is refining its SAS-related portfolio through cost optimization and specialty chemical focus under its FORWARD! program. The company targets €150 million in annual savings while improving operational agility in its intermediates segment. Sulfonation expertise supports production of alkane sulfonic derivatives for food-contact and medical applications with low migration profiles. Workforce restructuring enhances efficiency in delivering high-purity surfactants. Expanded benzyl alcohol and intermediates capacity strengthens its position in North American hygiene and personal care markets. Focus on regulated, high-purity applications aligns with evolving compliance requirements.

Stepan integrates SAS into hybrid bio-surfactants and consumer-focused detergent formulations

Stepan Company is leveraging its global surfactant platform to integrate SAS into sustainable detergent and cleaning solutions. Replacement of LAS with SAS supports premium laundry formulations with improved biodegradability. Hybrid surfactants combining SAS with rhamnolipids and sophorolipids address growing demand for eco-friendly cleaning agents. Stepwet and Stepan-Mild product lines incorporate SAS to enhance grease removal in dishwashing liquids, a segment accounting for significant global demand. Investments in sulfoxidation efficiency reduce energy consumption and support ESG targets. Focus on consumer-driven sustainability strengthens its market position.

Sasol secures upstream SAS feedstock advantage with integrated n-paraffin production and decarbonization strategy

Sasol Limited provides critical upstream integration through high-purity C14–C17 n-paraffin production, ensuring stable feedstock supply for SAS manufacturing. Coal-to-liquids technology supports consistent paraffin output amid crude volatility. Development of renewable paraffin feedstocks targets mass-balance certified SAS production. Renewable energy integration into fractionation units aligns with decarbonization goals under its 2030 strategy. Paraffin sulfonates are widely used in enhanced oil recovery and textile processing due to thermal and salinity resistance. Strong upstream control enhances reliability for downstream surfactant producers.

BASF delivers integrated clean-label surfactant systems with low-foaming SAS and regulatory leadership

BASF SE is strengthening its SAS market position through integrated detergent systems and bio-based surfactant innovation. SAS is combined with Trilon® M chelating agents and Sokalan® polymers to create phosphate-free, high-performance cleaning formulations. Research into low-foaming SAS variants addresses requirements in automated industrial cleaning systems. The company reported €6.6 billion EBITDA in 2025, supporting continued investment in sustainable surfactants. Leadership in REACH regulatory processes ensures compliance and safe usage of SAS in personal care applications. Focus on green transformation supports demand for eco-friendly, high-efficiency surfactants.

Germany: Premium SAS Scale-Up Anchored in Sustainability and Performance

Germany represents the most technically advanced and regulation-driven market for Secondary Alkane Sulfonates, with growth shaped by premium home care demand, circular feedstock integration, and low-temperature wash performance. In 2024, BASF completed a major debottlenecking project at its Ludwigshafen Verbund, materially increasing the throughput of high-purity SAS grades used by leading European detergents and I&I cleaning brands. This capacity optimization aligns with the accelerated shift toward SAS under the EU Strategy for Sustainability, where rapid aerobic and anaerobic biodegradability in wastewater treatment gives SAS a structural advantage over less compliant surfactants.

Product innovation is reinforcing Germany’s leadership position. Clariant launched Hostapur® SAS 93 in flake form, specifically engineered for waterless and solid detergent formats that reduce logistics emissions and packaging intensity. At the same time, WeylChem Group achieved ISCC PLUS certification for its SAS lines, enabling mass-balanced bio-circular feedstock use without compromising formulation performance. R&D momentum is further supported by federal funding, with the German Federal Ministry of Education and Research backing a 2025 pilot program to synthesize SAS from non-paraffin alternative hydrocarbons, potentially reducing long-term dependence on linear paraffin streams. Application-wise, SAS penetration is strongest in low-temperature laundry detergents effective at 20°C, where its superior solubility versus LAS supports energy-efficient washing. Downstream integration has also progressed, with Lanxess expanding chemical assets in the Mannheim region to support high-electrolyte industrial cleaner formulations.

China: Scale, Policy Alignment, and Export-Oriented Transition

China is rapidly transitioning from a volume-centric SAS producer to a technology-driven and export-oriented supplier, supported by industrial clustering and policy incentives. State-linked producers including Sinopec have expanded output of C14–C17 secondary alkane sulfonates to meet domestic Green Manufacturing Initiative targets, particularly in textiles, electronics, and institutional cleaning. Regulatory tailwinds are strong. The Ministry of Ecology and Environment’s 2025 draft on Priority Controlled Chemical Substances explicitly favors SAS over nonylphenol ethoxylates in industrial washing, accelerating substitution across multiple end-use sectors.

Technological upgrading is central to this shift. Chinese manufacturers have advanced falling film sulfonation processes to minimize disulfonate formation, enabling cosmetic-grade and electronic-cleaning SAS with tighter purity control. Production remains highly concentrated in the Jiangsu and Zhejiang chemical parks, where integrated paraffin supply from adjacent refineries improves cost efficiency and logistics resilience. Environmental enforcement has intensified, with 2025 updates to the Yellow River Protection Law mandating biodegradable surfactants such as SAS in textile processing. Capital deployment is substantial, with more than $200 million invested in specialty surfactant units at the Nanjing Chemical Industrial Park, targeting electronic and precision cleaning applications. As a result, China is rapidly moving from net importer status toward becoming a global exporter of 60% active SAS solutions.

United States: Renewable Feedstocks, High-Purity Grades, and Brand-Led Demand

The United States SAS market is shaped by renewable feedstock substitution, regulatory signaling, and demand from both consumer brands and advanced manufacturing. In 2025, Shell Chemicals and Henkel expanded their partnership to replace roughly 200,000 tonnes of fossil-derived feedstocks with renewable alkanes in surfactant production, directly supporting SAS growth in home and I&I cleaning. On the supply side, Stepan Company commissioned a new alkoxylation and sulfonation asset in Pasadena, Texas, strengthening domestic SAS availability for major CPG formulators.

Regulation is a clear adoption catalyst. The EPA Safer Choice program has materially increased SAS usage in institutional and industrial cleaning due to its favorable aquatic toxicity and biodegradability profile. Beyond traditional cleaning, U.S. producers are developing ultra-pure SAS grades for semiconductor manufacturing, where SAS functions as a precision wetting agent in wafer cleaning processes. Investment patterns on the Gulf Coast increasingly integrate SAS units with carbon capture and storage infrastructure, improving lifecycle emissions metrics. Additionally, the rapid growth of direct-to-consumer cleaning brands is boosting localized demand for SAS in concentrated pods and tablet formats, while USDA BioPreferred certification continues to expand federal procurement channels for SAS-based formulations.

India: Capacity Doubling and FMCG-Led Substitution

India is emerging as a high-growth SAS market driven by FMCG demand, process modernization, and regulatory harmonization. Under the Make in India 2.0 initiative, domestic producers such as Rajvin Chemicals have doubled liquid SAS capacity to support large-volume detergent and dishwashing brands. Urbanization trends are reshaping consumption patterns, with a reported 15% year-on-year increase in SAS usage in liquid dishwash detergents as consumers shift away from traditional soap bars.

Manufacturing technology is advancing rapidly. Continuous sulfonation systems adopted in Mumbai-based facilities are improving batch consistency, color stability, and yield efficiency. On the regulatory front, the Bureau of Indian Standards is aligning biodegradability norms with ISO 14593, structurally favoring SAS over slower-degrading surfactants. Significant capital expenditure is flowing into the Dahej PCPIR, strengthening backward integration and export readiness. Application demand is particularly strong in textile and leather hubs such as Tirupur and Kanpur, where SAS delivers superior wetting and emulsification. Sustainability considerations are also gaining traction, with increasing interest in palm-derived alkanes as renewable SAS precursors aligned with regional feedstock availability.

Brazil: Regional Supply Hub and Agro-Industrial Applications

Brazil is consolidating its role as a regional SAS hub for the Mercosur bloc, supported by industrial expansion and feedstock innovation. Capacity additions at the Camaçari Industrial Complex have strengthened local SAS availability, reducing dependence on imported concentrates. Regulatory developments are supportive, with ANVISA tightening surfactant safety assessments in personal care, favoring dermatologically mild SAS formulations.

Feedstock research is a strategic differentiator. Brazilian producers are exploring sugarcane-derived hydrocarbons as a sustainable base for domestic SAS manufacturing, leveraging the country’s bioethanol infrastructure. Multinational detergent brands have increased investment in local production sites to secure supply and improve cost competitiveness. Beyond home care, SAS is gaining importance as an agrochemical adjuvant, enhancing leaf adhesion in pesticide formulations, and as a core component in heavy-duty degreasers used in mining and automotive maintenance. Recent investments of approximately $80 million in sulfonation technology upgrades are enabling Brazilian suppliers to meet export-grade specifications.

Secondary Alkane Sulfonates Industry: Country-Level Strategic Snapshot

Secondary Alkane Sulfonates Market County Level Snapshot

|

Country

|

Strategic Drivers

|

Market Positioning Impact

|

|

Germany

|

ISCC PLUS adoption, low-temperature detergents, R&D funding

|

Leadership in premium, sustainable SAS formulations

|

|

China

|

Green Manufacturing policy, industrial clusters, export focus

|

Transition from volume supplier to global SAS exporter

|

|

United States

|

Renewable alkanes, Safer Choice compliance, DTC brands

|

Growth in high-purity and certified SAS applications

|

|

India

|

Make in India 2.0, FMCG substitution, process modernization

|

Rapid domestic scale-up and export readiness

|

|

Brazil

|

Mercosur supply hub, bio-feedstock research, agro-use

|

Regional SAS leadership with diversified end uses

|

Secondary Alkane Sulfonates Market Report Scope

Secondary Alkane Sulfonates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2034)

|

$1.9 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Grade (Cosmetic Grade, Industrial Grade, Technical Grade), By Form (Liquid, Paste, Flakes & Granules, Powder), By Carbon Chain Length (Short Chain, Medium Chain, Long Chain), By Application (Household Detergents & Cleaners, Dishwashing Liquids, Personal Care Products, Industrial & Institutional Cleaning, Textile & Leather Processing, Emulsion Polymerization, Oilfield Chemicals, Agrochemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Clariant AG, Stepan Company, BASF SE, Lanxess AG, WeylChem Performance Products GmbH, Sasol Limited, Sinopec Group, Shell Chemicals, Big Sun Chemical Corporation, Acar Chemicals, Rajvin Chemicals, Nease Performance Chemicals, Enaspol AS, Goulston Technologies Inc., Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Secondary Alkane Sulfonates Market Segmentation

By Grade

- Cosmetic Grade

- Industrial Grade

- Technical Grade

By Form

- Liquid

- Paste

- Flakes & Granules

- Powder

By Carbon Chain Length

- Short Chain

- Medium Chain

- Long Chain

By Application

- Household Detergents & Cleaners

- Dishwashing Liquids

- Personal Care Products

- Industrial & Institutional Cleaning

- Textile & Leather Processing

- Emulsion Polymerization

- Oilfield Chemicals

- Agrochemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Secondary Alkane Sulfonates Industry

- Clariant AG

- Stepan Company

- BASF SE

- Lanxess AG

- WeylChem Performance Products GmbH

- Sasol Limited

- Sinopec Group

- Shell Chemicals

- Big Sun Chemical Corporation

- Acar Chemicals

- Rajvin Chemicals

- Nease Performance Chemicals

- Enaspol AS

- Goulston Technologies Inc.

- Huntsman Corporation

*- List not Exhaustive