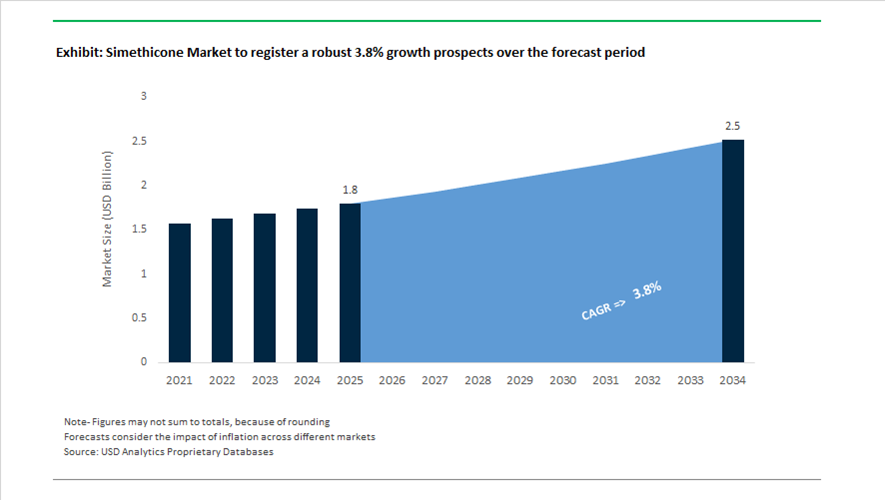

Simethicone Market Valuation 2025–2034: $1.8 Billion to $2.5 Billion at 3.8% CAGR Driven by OTC Expansion and Clean-Label Reformulation

The global simethicone market is valued at $1.8 billion in 2025 and is projected to reach $2.5 billion by 2034, expanding at a CAGR of 3.8%. Growth is supported by steady demand for over-the-counter (OTC) anti-flatulent formulations, combination digestive health products, pediatric dosage forms, and pre-diagnostic medical preparations. Simethicone, a silicone-based anti-foaming agent, remains a first-line therapy for gas relief due to its inert chemical profile, low systemic absorption, and compatibility with antacids and proton pump inhibitor regimens. Market expansion is being influenced by clean-label reformulation trends, multi-symptom product development, digital pharmacy integration, and supply chain localization strategies.

In 2024, Procter & Gamble expanded its pediatric digestive portfolio with child-friendly chewable simethicone tablets designed for improved taste masking and patient compliance. The same period saw Sanofi advance plans to separate its Consumer Healthcare division, including gas-relief products, culminating in an IPO-focused spinoff strategy by late 2025 to sharpen focus on immunology and vaccine pipelines. In 2024–2025, KCC Corporation completed the integration of Momentive Performance Materials into its global silicone operations, streamlining production of medical-grade simethicone fluids used in OTC and prescription formulations. These developments underscore vertical integration in silicone active ingredients and portfolio restructuring among leading consumer health players.

Throughout 2025, digital transformation and geographic expansion reshaped distribution models. In June 2025, Haleon completed acquisition of the remaining 12% stake in its China joint venture, securing full operational control over its digestive health brands in a key growth market. In October 2025, Haleon selected Salesforce’s Agentforce Life Sciences Cloud to implement AI-driven pharmacy engagement tools aimed at optimizing supply and demand forecasting during seasonal digestive health spikes. Early 2025 U.S. tariffs on chemical precursors triggered supply chain reassessment, with producers diversifying sourcing to mitigate a 10–15% increase in raw material and packaging costs. In December 2025, Biolab launched LISTOGAS Gotas in Brazil, a high-concentration 150 mg/mL simethicone formulation positioned for rapid relief and pre-endoscopy preparation.

Strategic acquisitions and operating model shifts intensified in 2026. In late 2025, Procter & Gamble announced the acquisition of Wonderbelly, finalizing the transaction in January 2026, integrating clean-label digestive health products alongside established brands such as Pepto Bismol and Rolaids. In January 2026, Haleon introduced a revised operating model with the creation of a Chief Growth Officer role to accelerate innovation in the Digestive Health category. In February 2026, Kenvue reported increased penetration of its gas-relief portfolio, including Gas-X, supported by new multi-symptom combination offerings addressing both gas and heartburn. These strategic maneuvers reflect a market characterized by brand portfolio optimization, clean-label positioning, pediatric compliance innovation, and operational digitization, shaping competitive dynamics in the global simethicone market through 2034.

Strategic Trends and High-Value Opportunities Shaping the Global Simethicone Market

Brand Ecosystem Expansion Integrating Simethicone into Gut Wellness Platforms

The simethicone market is undergoing a strategic repositioning as leading consumer health companies move beyond single-symptom gas relief toward holistic gut wellness ecosystems. This evolution reflects changing consumer behavior, particularly among younger demographics, who increasingly favor self-care routines, premium delivery formats, and multi-benefit digestive solutions. As a result, simethicone is being reformulated into fast-melt crystals, chewables, and combination products designed to deliver rapid relief while fitting seamlessly into daily wellness regimens.

In July 2025, Haleon outlined its Win as One strategy in its half-year results, highlighting a disciplined portfolio optimization that reduced total SKUs by 16% since early 2024 to concentrate on higher-margin innovations. Within its Gas-X franchise, this approach includes rolling out combination formats that position simethicone as part of total digestive health solutions across more than 40 countries. A parallel innovation signal is emerging from Procter & Gamble, which intensified its Connect and Develop initiatives in 2025 to source external technologies that enhance its Metamucil and Align brands. P&G is actively evaluating market-ready combination actives and differentiated delivery systems that integrate simethicone into broader bloating and digestive wellness offerings, reinforcing its role as a platform ingredient rather than a standalone OTC molecule.

Clinical Mandates Standardizing Simethicone Use in Endoscopic Procedures

In clinical settings, simethicone is transitioning from discretionary adjunct to protocol-driven standard of care, particularly in gastrointestinal endoscopy. Hospital systems and medical associations are increasingly codifying its use to improve mucosal visualization, reduce procedure time, and enhance lesion detection rates. Clinical evidence continues to consolidate around the conclusion that pre-procedural simethicone significantly reduces bubble interference, a key impediment to diagnostic accuracy.

As of November 2025, the NACSIMET multicenter clinical trial registered as NCT07245095 is evaluating a pre-endoscopy regimen combining 600 mg of N-acetylcysteine with 100 mg of simethicone administered 20 to 60 minutes before upper endoscopy. Using the Toronto Upper Gastrointestinal Cleaning Score as a primary endpoint, the study aims to demonstrate that simethicone is essential for achieving complete esophageal visualization. In the United States, a national guidance update issued by the U.S. Department of Veterans Affairs on January 1, 2024, mandated administering simethicone via 10 mL aliquots through the endoscope biopsy port rather than the water reservoir. Data presented at DDW 2025 confirmed that this protocol maintains adenoma detection rates and procedural efficiency while addressing infection control concerns, further embedding simethicone into standardized hospital workflows.

High-Purity Pediatric Simethicone Formulations and Advanced Delivery Systems

The pediatric segment represents a structurally attractive growth opportunity for simethicone manufacturers as regulators and clinicians emphasize safer, alcohol-free, and palatable treatments for infant colic and pediatric aerophagia. This demographic requires exceptionally high purity standards, driving demand for pharmaceutical-grade simethicone that minimizes the risk of impurities and adverse reactions.

In 2024, Dow launched a new high-purity simethicone grade engineered specifically for sensitive pharmaceutical applications. The product is designed to meet stringent USP and EP specifications, making it suitable for pediatric and geriatric formulations where physiological sensitivity is highest. Regulatory clarity is further reinforcing this opportunity. In October 2024, the U.S. Food and Drug Administration issued draft product-specific guidance for loperamide hydrochloride and simethicone chewable tablets. The guidance establishes mandatory in vitro defoaming studies under USP <1150>, requiring demonstrable bubble collapse within 30 seconds. This creates a clear, compliance-driven pathway for manufacturers targeting pediatric and adolescent digestive health markets.

Fixed-Dose Combination Therapies Targeting IBS and Functional GI Disorders

A second high-value opportunity lies in the development of fixed-dose combination therapies where simethicone acts as a synergistic co-active rather than a standalone agent. Pharmaceutical developers are increasingly exploring combinations with antispasmodics or probiotics to address the multifactorial nature of irritable bowel syndrome and other functional gastrointestinal disorders. This strategy supports a shift from low-margin OTC positioning toward prescription or pharmacist-only categories.

Clinical evidence supports this approach. Studies published in 2024 examining combinations of alverine citrate at 60 mg with simethicone at 300 mg demonstrated a significantly higher responder rate of 46.8% compared with 34.3% for placebo in relieving IBS-related abdominal pain. Further research updated in February 2025 indicates that simethicone combined with probiotic strains such as Bifidobacterium achieved a 92.5% total efficacy rate in treating pediatric aerophagia, alongside improvements in gastric emptying and lower Gastrointestinal Symptom Rating Scale scores. These data points underscore a compelling opportunity for synbiotic-simethicone hybrids and prescription-grade combination therapies positioned for long-term management of functional GI conditions.

Simethicone Market Share and Segmentation Insights

USP NF Grade Simethicone Leads Market Demand Driven by Pharmaceutical Quality Standards

USP NF grade simethicone accounted for 58.60% of the simethicone market in 2025, reflecting its dominant role in pharmaceutical formulations. This grade complies with United States Pharmacopeia and National Formulary purity standards, ensuring consistent quality, safety, and efficacy required for medicinal use. Simethicone is widely used as the active ingredient in over-the-counter antiflatulent medications, including tablets, capsules, liquids, and pediatric drops designed to relieve gas pressure and bloating. A major 2025 industry trend is the growing demand for globally harmonized pharmaceutical grades, where manufacturers increasingly supply simethicone meeting multiple pharmacopoeia standards such as USP, EP, and JP. This harmonization enables pharmaceutical companies to streamline regulatory compliance and utilize a single high-purity grade across multiple international markets.

Pharmaceuticals Drive Global Simethicone Consumption Across Over-the-Counter Gastrointestinal Treatments

Pharmaceutical applications represent the largest segment in the simethicone market, accounting for 68.40% of total demand in 2025 due to the widespread use of simethicone in gastrointestinal relief products. Simethicone acts as an anti-foaming agent that reduces surface tension in gas bubbles within the digestive tract, helping relieve symptoms such as bloating, gas pressure, and abdominal discomfort. The strong safety profile and long-standing clinical use have made simethicone a staple ingredient in global over-the-counter digestive health products. A key 2025 market development is the expansion of combination pharmaceutical formulations, where simethicone is incorporated with antacids, laxatives, and other gastrointestinal actives to create multi-symptom treatments addressing conditions such as heartburn, indigestion, constipation, and gas-related discomfort.

Simethicone Market Competitive Landscape

The global simethicone market in 2026 is defined by ultra-high-purity silicone innovation, GMP-compliant production, and expanding OTC gastrointestinal therapeutics demand. Leading players are optimizing supply chains, advancing low-volatile siloxane formulations, and integrating simethicone into drug delivery systems and medical-grade applications.

Wacker Chemie AG Strengthens GMP-Certified SILFAR® Portfolio and Cost Leadership via Project PACE

Wacker Chemie AG maintains leadership in the pharmaceutical-grade simethicone market through its SILFAR® portfolio, engineered for high-purity, low volatile siloxane content aligned with ICH Q7 GMP standards. Its SILFAR® 100 series directly targets high-growth OTC applications such as infant colic and adult anti-flatulent formulations, reinforcing its presence in GI therapeutics. The Project PACE initiative, targeting €300 million annual savings by 2026, is structurally reallocating capital toward high-margin life sciences silicones, enhancing EBITDA resilience. Expanded production capacities in Jincheon and Zhangjiagang strengthen localized supply chains for Asia-Pacific pharmaceutical demand. Wacker’s 2026 fiscal guidance reflects stable specialty siloxane recovery despite elevated European energy costs. The company’s integrated GMP-certified manufacturing and cost optimization strategy ensures sustained competitiveness in medical-grade simethicone.

Dow Inc. Expands Low-Volatile DOWSIL™ Simethicone Integration Across Drug Delivery Platforms

Dow Inc. is reinforcing its position in the global simethicone industry through its DOWSIL™ portfolio, particularly the Q7-2243 LVA grade engineered for minimal cyclic siloxane content in pharmaceutical APIs. Its “Transform to Outperform” program is driving AI-enabled manufacturing optimization, enhancing PDMS-silica blending precision for consistent antifoaming performance in OTC formulations. Dow’s strong Drug Master File (DMF) infrastructure accelerates regulatory approvals across U.S. and EU pharmaceutical markets, providing a competitive edge in compliance-heavy environments. The Shanghai Cooling Science Studio acts as a regional innovation hub supporting advanced silicone emulsions for diagnostic imaging and endoscopy. Integration of simethicone into complex drug delivery and medical device platforms positions Dow as a total solutions provider. Its focus on regulatory integration and scalable production strengthens its role in high-performance pharmaceutical silicones.

KCC Basildon Advances High-Performance Simethicone Antifoams for Pharmaceutical Processing Efficiency

KCC Basildon is positioning itself as a niche leader in simethicone antifoam technology, with its C100EP, C100LV, and newly introduced C100F grades addressing pharmaceutical formulation and processing challenges. These 100% silicone-based compounds enable rapid bubble coalescence, improving the efficiency and stability of antacid and anti-flatulent dosage forms. The launch of translucent, high-purity viscous simethicone enhances optical clarity and dispersion in liquid suspensions, critical for product aesthetics and efficacy. Its strategic pivot toward processing aids expands simethicone usage into fermentation and beverage manufacturing, where foam control directly impacts throughput. Leveraging over four decades of expertise, the company capitalizes on UK-based manufacturing to support European pharmaceutical supply chain resilience. KCC Basildon’s specialization in high-performance antifoaming solutions differentiates it within the global simethicone market.

Avantor Inc. Elevates Ultra-High-Purity Simethicone Applications in Medical Devices and Biologics

Avantor, through its NuSil™ technology platform, is advancing ultra-high-purity simethicone applications at the intersection of pharmaceuticals and medical devices. Its 2026 innovation pipeline includes biocompatible silicone additives that enhance elastomer performance, with simethicone-based lubricants reducing friction in drug delivery systems. Serving over 300,000 global customer locations, Avantor enables customization of viscosity and silica loading for targeted therapeutic outcomes in GI and specialty drug formulations. ISO 13485 certification across its manufacturing sites ensures compliance with stringent medical device standards, particularly for implantable and long-term applications. The company’s focus on impurity-free silicone production supports next-generation biologics and high-potency APIs. Avantor’s positioning as a mission-critical supplier reinforces its leadership in UHP healthcare silicones.

Shin-Etsu Chemical Accelerates Green Simethicone Innovation and Large-Scale Capacity Expansion

Shin-Etsu Chemical is redefining the competitive landscape through its Green Silicones™ initiative, introducing biomass-derived and carbon-neutral simethicone aligned with global ESG mandates. Its ¥100 billion investment in silicone capacity expansion across Japan and Thailand is strengthening supply for the rapidly growing Asian pharmaceutical and healthcare markets. The company’s development of recyclable thermoplastic silicones is enabling innovation in sustained-release simethicone delivery systems for chronic gastrointestinal conditions. With projected net sales of ¥2.4 trillion and strong operating income targets, Shin-Etsu demonstrates robust financial backing for its specialty materials segment. Its focus on green chemistry, high-performance silicone fluids, and advanced material science positions it at the forefront of sustainable pharmaceutical-grade silicones. The integration of eco-friendly production with high-purity output enhances its competitive advantage in the evolving simethicone market.

United States Simethicone Market Reshaped by Tariff Realignment and Pediatric-Focused Innovation

The United States simethicone market is experiencing a structural shift driven by tariff policy changes, regulatory tightening, and formulation-led differentiation. Following revised pharmaceutical tariffs implemented in early 2025, U.S. manufacturers have actively diversified sourcing strategies for siloxane derivatives. This has resulted in an estimated 15% increase in domestic capacity dedicated to pharmaceutical-grade simethicone, aimed at reducing exposure to imported intermediates and improving supply chain resilience. Capacity expansion has been particularly pronounced around established pharmaceutical corridors in Pennsylvania and New Jersey, where more than USD 1.2 billion in combined R&D investments were reported in 2025 for advanced digestive health formulations, including simethicone-coated tablets engineered for rapid-release and improved bioavailability.

Product innovation has increasingly targeted pediatric and lifestyle-driven use cases. Concentrated simethicone micro-drops with Smart-Dose calibrated droppers were introduced to enhance dosing accuracy for infant colic, aligning closely with the FDA Pediatric Health Initiative priorities for 2025. Regulatory oversight has intensified in parallel. The FDA’s 2025 Guidance Agenda introduced new stability testing requirements for simethicone emulsions, mandating secondary containment for liquid-filled capsules to mitigate leaching risks during extended storage. On the supply side, Dow expanded its specialized pharmaceutical silicone facility to support growing demand for USP-grade simethicone used as an active ingredient in private-label retail brands. Demand diversification is also visible in sports nutrition, where simethicone is increasingly incorporated into endurance athlete supplements to manage exercise-induced gastrointestinal distress, following high-visibility clinical studies published in late 2024.

Germany Simethicone Market Anchored by Ultra-Clean Chemistry and Sustainable Synthesis

Germany’s simethicone industry is defined by stringent purity benchmarks, sustainability-led process innovation, and advanced drug delivery formats. In November 2025, Wacker Chemie AG launched the SILPURAN® eco series, produced using biogenic methanol rather than fossil-based feedstocks. This transition enables the production of simethicone with a materially lower carbon footprint while preserving compliance with pharmaceutical-grade performance requirements. German producers have simultaneously standardized tin-free catalysts in the synthesis of PDMS backbones for simethicone, ensuring alignment with European Pharmacopoeia purity thresholds and minimizing trace metal contamination.

Manufacturing precision has become a competitive differentiator. Evonik completed a digital transformation of its Essen surfactant and siloxane facility in mid-2025, deploying AI-driven batch controls to achieve 99.9% consistency in simethicone emulsion droplet size. This level of control supports uniform efficacy across liquid antacid and chewable dosage forms. Regulatory alignment continues to influence portfolio strategy, as Germany positions itself ahead of the 2026 EU REACH roadmap enforcing stricter limits on D4 and D5 siloxane residuals. Beyond core formulations, German firms are also innovating in patient-centric delivery, including simethicone-infused chewable films for geriatric patients with dysphagia, supported by federal healthcare innovation grants awarded in late 2025.

India Simethicone Market Accelerated by Generic Manufacturing and Regulatory Quality Enforcement

India has emerged as a critical production and export hub for simethicone, supported by cost-efficient manufacturing and policy-backed localization. Under Make in India initiatives, domestic companies such as RioCare India and Gepach International have expanded simethicone production capacity to meet rising demand for affordable gastrointestinal remedies across domestic and export markets. India is now a leading supplier of simethicone emulsions to Africa and Southeast Asia, aided by Export Promotion Council subsidies during the 2025 to 2026 period.

Regulatory scrutiny has intensified following quality-related incidents. After the 2025 recall of Papazyme tablets linked to strip-pack bulging caused by gas release, the Drug Controller General of India mandated enhanced gas-permeability testing for all simethicone-containing multi-active tablets. This has driven investments in analytical rigor, including the introduction of High-Performance Liquid Chromatography as a mandatory identification test for simethicone batches to prevent mislabeling in complex enzyme formulations. Collectively, these measures are elevating India’s credibility as a reliable source of compliant pharmaceutical-grade simethicone for regulated and semi-regulated markets.

Japan Simethicone Market Defined by Material Science Synergy and High-Purity Applications

Japan’s simethicone industry benefits from advanced materials expertise and cross-sector technology transfer. In late 2025, Shin-Etsu Chemical announced the development of a thermoplastic silicone designed to simplify the manufacturing of simethicone-based delivery devices, improving recyclability and reducing waste in pharmaceutical packaging. This innovation reflects Japan’s broader emphasis on material resilience and circular design within regulated healthcare products.

High-purity capabilities developed for semiconductor manufacturing are increasingly leveraged in pharmaceutical and adjacent applications. Japanese firms have introduced electronic-grade simethicone as a high-performance defoamer for semiconductor cleaning processes, drawing on EUV lithography purity standards to minimize ionic contamination. Policy support has reinforced domestic demand, as the Ministry of Health, Labour and Welfare expanded its Self-Medication Tax Deduction list in 2025 to include a wider range of high-potency simethicone anti-gas products. Outside pharmaceuticals, medical-grade simethicone is gaining traction in premium personal care formulations within J-Beauty and K-Beauty segments, where it is used as a skin-protectant additive following updated dermatologist-led efficacy assessments.

China Simethicone Market Shaped by National Standards and Industrial Consolidation

China’s simethicone market is increasingly regulated, consolidated, and infrastructure-driven. In September 2025, the National Health Commission issued GB 4806.16-2025, introducing mandatory limits on volatile substances for all silicone-based materials, including food-grade and pharmaceutical-grade simethicone. Compliance with this standard is accelerating reformulation and capital investment across domestic producers.

Environmental enforcement has also driven structural consolidation. The Ministry of Ecology and Environment’s 2025 directives have led to the closure of smaller non-compliant silicone facilities, centralizing simethicone production within integrated Green Chemical Parks in Jiangsu and Zhejiang provinces. Despite consolidation pressures, demand fundamentals remain strong. China continues to be the global volume leader in simethicone used as a processing aid in fermentation, supported by record 2025 investments in bio-pharmaceutical and industrial biotechnology infrastructure. This combination of regulatory discipline and scale-driven demand is reshaping China’s role from a fragmented producer base toward a more standardized and policy-aligned simethicone supply ecosystem.

Comparative Snapshot: Country-Level Simethicone Industry Dynamics

Simethicone Market County Level Snapshot

|

Country

|

Core Demand Drivers

|

Strategic Focus Areas

|

Regulatory and Policy Influence

|

|

United States

|

Pediatric care, retail generics, sports nutrition

|

Domestic sourcing, advanced dosage forms

|

FDA stability guidance, tariffs

|

|

Germany

|

Prescription GI drugs, geriatric care

|

Ultra-clean synthesis, sustainable feedstocks

|

EU REACH siloxane limits

|

|

India

|

Low-cost generics, export markets

|

Scale manufacturing, analytical quality control

|

DCGI packaging and testing rules

|

|

Japan

|

OTC self-medication, advanced materials

|

High-purity simethicone, recyclable delivery devices

|

MHLW self-medication incentives

|

|

China

|

Fermentation processing, pharma scale-up

|

Green chemical parks, standardized compliance

|

GB 4806.16-2025, environmental enforcement

|

Simethicone Market Report Scope

Simethicone Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$2.5 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Product Grade (USP NF Grade, EP Grade, Food Grade, Industrial Grade), By Form (Simethicone API, Simethicone Emulsions, Simethicone Powders), By Application (Pharmaceuticals, Medical Devices, Food & Beverage, Cosmetics & Personal Care, Industrial Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co. Ltd., Momentive Performance Materials Inc., Evonik Industries AG, Elkem ASA, RioCare India Pvt. Ltd., Resil Chemicals Pvt. Ltd., Nusil Technology, KCC Basildon, Gelest Inc., Jiangsu Guangcheng Chemical, Biomax, Hubei BlueSky New Material Inc., Stellapharm JV Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Simethicone Market Segmentation

By Product Grade

- USP NF Grade

- EP Grade

- Food Grade

- Industrial Grade

By Form

- Simethicone API

- Simethicone Emulsions

- Simethicone Powders

By Application

- Pharmaceuticals

- Medical Devices

- Food & Beverage

- Cosmetics & Personal Care

- Industrial Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Simethicone Industry

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co. Ltd.

- Momentive Performance Materials Inc.

- Evonik Industries AG

- Elkem ASA

- RioCare India Pvt. Ltd.

- Resil Chemicals Pvt. Ltd.

- Nusil Technology

- KCC Basildon

- Gelest Inc.

- Jiangsu Guangcheng Chemical

- Biomax

- Hubei BlueSky New Material Inc.

- Stellapharm JV Co. Ltd.

*- List not Exhaustive