Market Overview: High-Durability Polycarbonate & Sustainable Materials Redefining Smart Card Lifecycles

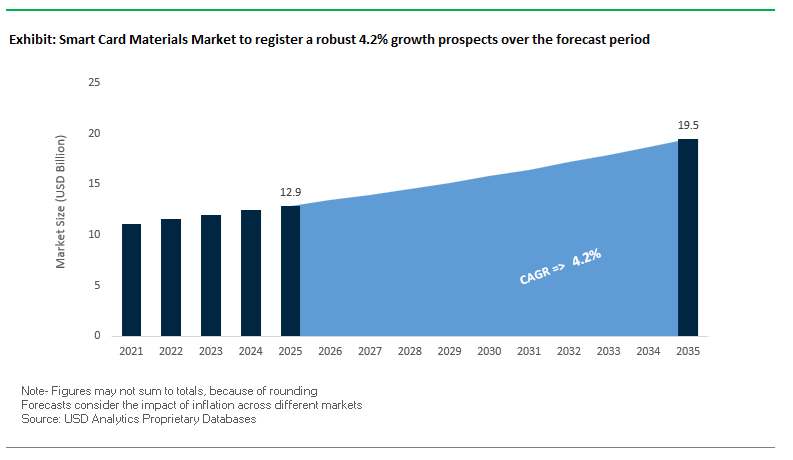

The Smart Card Materials Market, valued at USD 12.9 billion in 2025, is forecast to reach USD 19.5 billion by 2035, expanding at a steady CAGR of 4.2%. Demand is strongly driven by national identity programs, e-passports, next-generation payment cards, biometric authentication solutions, and mass transit systems. As governments and financial institutions shift toward high-security formats and long-life card architectures, manufacturers are prioritizing polycarbonate (PC) durability, chip and antenna protection, and environmentally responsible polymer sourcing. The migration from low-cost PVC to PETG, polycarbonate, rPVC, and bio-based alternatives represents one of the most significant material transitions in the security document ecosystem.

High-performance polycarbonate smart cards—particularly those used for government IDs—are engineered to survive 1 million flex cycles, delivering reliable service life beyond 10 years, far superior to the typical 3–5-year lifecycle of PVC banking cards. Temperature stability also shapes material selection: PVC begins to warp at ~60°C, whereas polycarbonate structures remain stable at >120°C and up to 145°C, essential for automotive access systems, harsh outdoor environments, and high-heat personalization processes. As smart card architectures integrate advanced biometric sensors, Secure Elements, and cryptoprocessors, ISO/IEC 7816 compliance is pushing manufacturers to use lamination films that prevent delamination, resist tampering, and protect embedded semiconductor components. Meanwhile, sustainability mandates are accelerating adoption of rPVC, PLA, bamboo, and recycled PC, positioning eco-materials as a strategic differentiator for financial institutions pursuing net-zero commitments.

Key insights for manufacturers and material suppliers

- Polycarbonate ID cards engineered for 1 million flex cycles are rapidly becoming the global standard for National ID and e-Passport programs.

- Heat resistance above 120–145°C is essential for next-generation automotive and industrial smart card deployments.

- Biometric cards require tamper-resistant lamination materials that protect embedded processors without compromising structural integrity.

- Recycled PVC (rPVC) and bio-based materials are gaining share due to financial-sector carbon reduction targets.

- PETG and hybrid PET/PC structures are rising as sustainable, durable replacements for PVC in mass-issued payment cards.

Market Analysis: Technological Advancements and Sustainability-Driven Transitions Reshape Global Smart Card Material Demand

The Smart Card Materials industry is undergoing a rapid evolution influenced by product innovation, national digital identity rollouts, and a large-scale sustainability shift across financial and access control ecosystems. In July 2024, IDEMIA introduced the Starlight payment card, the world’s first network-approved OLED-integrated card powered wirelessly through NFC fields. This innovation has spurred material suppliers to engineer high-transparency, high-thermal-stability films capable of supporting embedded lighting and aesthetic functionalities. Similarly, the launch of the Mumbai 1 transport card in April 2025 strengthened demand for PETG and polycarbonate composites designed for continuous high-speed tap-and-go operations, abrasion resistance, and stable RF performance across millions of transactions.

Sustainability remains a decisive industry driver. In May 2024, HID Global unveiled Seos Bamboo access cards, demonstrating mainstream adoption of renewable materials and aligning with LEED and corporate ESG requirements. By Q3 2024, major European banks accelerated initiatives to convert their portfolios to cards with at least 85% recycled content, creating substantial momentum for rPVC, rPETG, and recycled polycarbonate supply chains. This movement gained further support when SABIC expanded its recyclable polymer technologies in November 2025, enabling government ID programs to shift toward circular-economy-certified PC feedstocks.

Downstream electronics and semiconductor advancements are also impacting material selection. Infineon’s expansion of secure microcontroller production in May 2025 heightened demand for polymer substrates capable of precision antenna embedding, dual-interface module stability, and chip-protective lamination. At the same time, Eastman’s December 2024 launch of advanced PETG resins for ID card lamination is improving personalization throughput and reducing chip-damage risk during high-temperature processing. On the policy front, GCC government programs in Q1 2025 introduced pilots for monolithic polycarbonate e-IDs, accelerating regional transitions toward tamper-resistant, laser-engraved identity documents with enhanced fraud-protection thresholds.

High-Durability Polycarbonate Architectures, Metal-Hybrid Antenna Designs, Sustainable Substrate Innovation, and Advanced Conductive Adhesives Redefining Smart Card Engineering

Market Trend 1: Transition Toward High-Durability Polycarbonate and ABS Blends for Next-Generation Multi-Layer Identity Documents

The Smart Card Materials Market is undergoing a major shift from legacy PVC constructions to polycarbonate (PC) and ABS blends, driven by rising global requirements for long-term identity durability, anti-tampering security, and environmental resilience. While PVC cards typically provide a service life of only 2–3 years, PC-based ID documents deliver 5–10+ years of operational lifespan, enabled by their superior mechanical and thermal properties. PC offers extreme robustness—up to 250× the impact resistance of glass—which dramatically reduces breakage rates under mechanical stress, high-volume usage, or accidental drops.

Temperature resilience is another defining performance factor. PC supports a Heat Deflection Temperature (HDT) of ~131–135°C, far exceeding PVC’s deformation threshold of 60–70°C, a critical advantage for biometric passports, eIDs, and transportation cards exposed to high ambient or operational temperatures. Additionally, PC’s monolithic structure—created by high-temperature lamination without adhesives—prevents layer separation and provides inherent anti-tampering protection, as any attempt to delaminate the card visibly destroys it. This design has become a global benchmark for security credentials, driving PC adoption across government-issued identity documents, border control systems, and banking institutions.

Market Trend 2: High-Performance Metal Inlays and Antenna Materials Supporting Next-Generation RF Smart Card Applications

Smart card manufacturers are increasingly integrating metal inlays, optimized antenna structures, and miniaturized chip modules to support the rapidly expanding ecosystem of contactless payment, transportation, mobile ID, and authentication systems. The presence of metal components creates RF attenuation challenges, addressed through precisely engineered insulating layers—typically 10 μm to 350 μm thick—to preserve RF amplitude and maintain the stability of communication channels.

The industry is moving from traditional aluminum wire antennas toward etched copper (Cu) and silver-palladium (AgPd) antennas, which offer superior conductivity, fatigue resistance, and long-term electrical stability. These materials support high-frequency RF protocols, reduce failure rates, and significantly improve transaction reliability in EMV and NFC environments. Module form factors are also evolving: chip thickness has decreased from 330–400 μm to 200 μm, enabling multi-layered card stacks, inclusion of metal cores, and compliance with the ISO CR-80 standard thickness of 0.76 mm. These advances allow manufacturers to incorporate biometric sensors, dynamic CVV modules, and multi-application circuitry without compromising card flexibility or reliability.

Market Opportunity 1: Growth of Bio-Based and Ocean-Bound Plastic Substrates for Sustainable Smart Card Manufacturing

Sustainability mandates across governments, payment networks, and OEMs are accelerating the adoption of bio-based, recycled, and ocean-bound plastic substrates within the Smart Card Materials Market. Bio PVC, rPETG, and PLA-based cards are engineered to match the printability and physical performance of standard PVC—including high-resolution offset, retransfer, and UV printing compatibility—ensuring seamless integration into established card production workflows.

These materials meet global durability standards such as ISO 7810, maintaining performance across –10°C to +50°C operating ranges while retaining IP68-level environmental resistance. PLA bioplastics introduce a significant end-of-life advantage due to their ability to decompose under industrial composting conditions, positioning them as a viable alternative for eco-conscious markets and brands pursuing circular-economy goals. Meanwhile, enhanced Bio PVC variants incorporate controlled degradation mechanisms that activate only in microbe-rich disposal environments—allowing the card to maintain full durability during use while supporting waste reduction initiatives afterward.

As sustainability moves from optional to mandatory across consumer banking, telecom, and government identity segments, demand for high-performance eco-friendly substrates is becoming one of the strongest commercial opportunities in the global smart card ecosystem.

Market Opportunity 2: Engineering Conductive Adhesives and Encapsulants for High-Reliability Chip Attachment and RF Module Integration

As smart cards become more complex—integrating biometric sensors, dynamic security modules, and multi-frequency antennas—the role of advanced conductive adhesives and encapsulants is becoming critical. These materials must withstand extreme temperature fluctuations and constant flexing while maintaining mechanical and electrical integrity. High-performance adhesive systems offer exceptional thermal shock resistance, enabling reliable operation in automotive, industrial IoT, and outdoor payment applications.

Conductive adhesives must also deliver strong bonding performance across diverse materials, providing high shear strength when coupling chips to substrates such as PC, PETG, and plated metals including Pd, Cu, Ag, and Au. Their electrical performance is engineered to match solder-level contact resistance, meeting stringent requirements for EMV modules and high-frequency antennas. Unlike solder—which is brittle and prone to fatigue failure—conductive adhesives provide superior flexibility, enabling the chip module to survive repeated bending stresses that occur during everyday card handling. This mechanical adaptability is becoming increasingly important as card architectures incorporate multi-layer constructions, embedded batteries, and ultra-thin chip modules.

The move toward solder-less electronic integration is positioning conductive adhesives as an enabling technology for next-generation smart card design, particularly in biometric payment cards, secure authentication tokens, and rugged industrial RFID systems.

Smart Card Materials Market Share Analysis

Market Share by Material Type: Polycarbonate Leads Due to Security-Centric Performance Advantages

Polycarbonate (PC) holds the dominant share of the global smart card materials market—approximately 45%—because it delivers the optimal balance of durability, security, and personalization performance required for next-generation high-assurance smart cards. PC’s monolithic, fusion-laminated structure provides exceptional resistance to delamination, tampering, heat, and mechanical wear, making it the material of choice for mission-critical identity documents and financial cards. Its compatibility with laser engraving, a cornerstone of secure credential issuance, positions it uniquely for high-security applications such as national ID programs, e-passports, driver’s licenses, and premium EMV payment cards that demand long service lifespans and forensic-level anti-counterfeiting protection. Rapid global adoption of multi-application ID systems, contactless banking cards, and biometric authentication interfaces further amplifies PC’s market leadership, as the material reliably maintains structural integrity around embedded chips, antennas, and biometric sensor modules. The continued rise of government-issued digital identity schemes, along with BFSI’s push for high-end metal-core and eco-enhanced premium cards, ensures PC’s sustained dominance across both volume and revenue metrics within the smart card materials ecosystem.

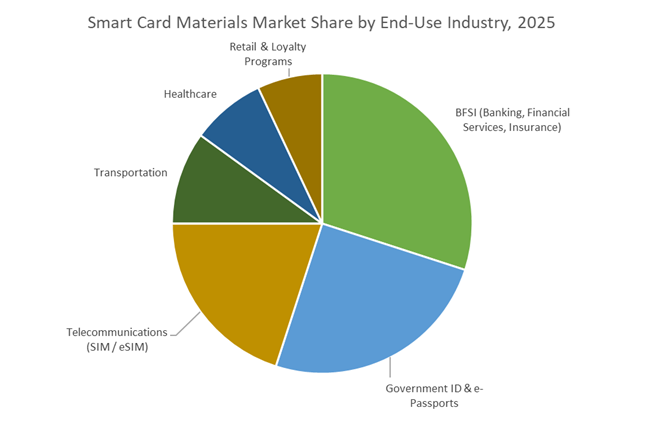

Market Share By End-Use Industry: BFSI Leads as Financial Digitalization Accelerates Smart Card Demand

The BFSI (Banking, Financial Services, and Insurance) sector accounts for the largest share of the global smart card materials market—approximately 30%—driven by continuous global issuance of EMV-compliant debit, credit, and prepaid cards and the rapid shift toward secure, contactless financial transactions. As financial institutions prioritize fraud reduction, cybersecurity, and frictionless customer authentication, smart cards—particularly those built with robust materials such as Polycarbonate and PETG—have become indispensable for embedding secure elements, dual-interface antenna modules, biometric sensors, and advanced cryptographic capabilities. The BFSI sector’s leadership is further reinforced by the rising frequency of card replacement cycles, the expansion of fintech ecosystems, and regulatory mandates pushing EMV and NFC adoption even in emerging economies. Meanwhile, premium and metal-hybrid payment cards, digital-first banking programs, and tokenization-enabled multi-interface cards all require materials with high stability, environmental resistance, and long-term durability, sustaining BFSI’s dominant use of advanced smart card substrates. This strong and recurring demand ensures that BFSI remains the highest-value and most influential end-use category shaping material innovation across the smart card industry.

Country Analysis: Global Smart Card Materials Leadership and Regional Material Innovation Patterns

China: Global Smart Card Manufacturing Powerhouse and Rapid Shift Toward High-Security Polycarbonate Substrates

China remains the largest and most influential hub in the global smart card materials market, driven by unmatched manufacturing scale and rapid government-led transitions to higher-security polymers. In 2025, China issued more than 3 billion smart cards, maintaining its global lead in SIM card and transit card production. This unprecedented output continues to push Chinese suppliers to expand production capabilities for PVC alternatives, especially Polycarbonate (PC) and PETG, which offer superior laser-engraving resolution, tamper resistance, and durability—key attributes for national identity cards and high-security credentials.

A major shift in material composition across Chinese ID programs is accelerating the adoption of high-durability PC substrates, reducing reliance on traditional PVC cards and enhancing the nation’s anti-counterfeiting ecosystem. Leading manufacturers—including Eastcompeace, Watchdata, and Hengbao—together shipped more than 200 million contactless EMV-certified payment cards in 2025, reinforcing China’s dominance in polymer substrate fabrication and dual-interface smart card assembly. China’s rapid growth in metro transit systems and nationwide digital ID expansion continues to generate sustained demand for advanced polymer substrates that support secure, high-volume personalization.

India: Large-Scale National ID Deployment and Transit Digitization Fueling High-Volume Polymer Substrate Consumption

India represents one of the world’s largest and fastest-growing markets for smart card materials, driven by enormous public-sector programs and nationwide digital transformation. The Aadhaar ecosystem, supporting authentication for 1.2+ billion citizens, generates continuous demand for robust, cost-effective substrates capable of sustaining intensive daily usage. These large deployments increasingly rely on durable polymer materials such as PVC, Composite PVC, and PETG to ensure long-term readability and security across authentication points, banking touchpoints, and welfare distribution systems.

India’s transit digitization is another major catalyst. The launch of the Mumbai 1 card in April 2025, designed for seamless tap-and-pay mobility across city transport networks, marks the beginning of expanded multi-modal smart transit rollouts across major metros. These programs are significantly increasing demand for ABS, PETG, and dual-interface compliant materials. Domestic suppliers such as Rosmerta Technologies and CardTec are scaling local manufacturing capacity to support PCI-compliant banking cards, including RuPay, Mastercard, and Visa credentials. India’s strategic manufacturing ambitions and policy incentives continue to position the country as a long-term growth engine for the global smart card materials supply chain.

United States: Biometric EMV Adoption and Sustainable Access Control Cards Reshaping Material Requirements

The United States smart card materials market is undergoing a decisive shift driven by biometric security adoption, high-assurance access control systems, and sustainability commitments. In 2025, major card issuers expanded their portfolio of biometric EMV cards, integrating fingerprint sensors directly into the card body. These next-generation payment cards require reinforced dual-interface layers, specialized antenna structures, and more thermally stable polymer substrates capable of withstanding the lamination complexity introduced by biometrics and microcontroller integration.

Sustainability innovation is also reshaping material choices. HID Global’s Seos Bamboo cards, introduced in May 2023, marked a landmark shift away from PVC-based materials toward renewable non-petroleum card bodies. This trend is influencing corporate access control adoption, encouraging the replacement of legacy PVC with more environmentally conscious materials including bamboo cores, recycled PETG, and advanced composite laminates. Meanwhile, price dynamics within the U.S. market remain sensitive to tariffs affecting security chip imports from Asia and Europe, creating volatility in material costs for high-end card assemblies and spurring interest in domestic semiconductor integration.

European Union/Germany: Biometric ID Standardization and the Rapid Transition to Recycled and Bio-Based Card Materials

The European Union, with Germany at the forefront, is steering a major transformation toward high-security, sustainable smart card materials guided by regulatory mandates and widespread biometric ID adoption. By 2025, the European Commission confirmed that 450 million EU citizens transitioned to biometric smart ID cards, driving large-scale demand for laser-engraveable Polycarbonate (PC)—the gold standard for tamper-resistant government credentials. This surge has catalyzed growth in multi-layer PC substrate production and secure laminate technologies used in national ID cards, residence permits, and driving licenses.

Sustainability is equally influential. Mastercard's commitment to eliminate first-use PVC across its global payment card network by 2028 has accelerated European suppliers’ investments into rPETG, PLA-based cards, and ocean-recovered plastics. Leading European companies like Giesecke+Devrient, IDEMIA, and Thales are scaling high-security, eco-friendly polymer lines designed for EMV cards, ePassports, and biometric credentials. Thales’ involvement in EU e-passport programs, serving 50+ million citizens, underscores the region's leadership in high-performance PC laminates, anti-counterfeit layers, and chip-embedded identity documents. The EU’s sustainability-first regulatory environment continues to reshape global sourcing strategies for smart card materials.

Japan: High-Temperature Laminates and Precision Materials for Advanced Contactless Smart Cards

Japan maintains a technical edge in high-performance smart card materials, especially in polymer engineering, high-temperature laminates, and advanced card-body composites used in e-IDs and secure transit systems. Material science leaders such as Teijin Ltd. continue to innovate in ultra-durable Polycarbonate films, engineered for precision lamination, optical clarity, and resistance to warping during high-temperature processing. These materials are critical for next-generation e-ID cards, transit cards, and hybrid display-smart card technologies emerging in Japan’s mobility and enterprise sectors.

Japan also plays a vital role in the global supply chain for smart card modules. Infineon Technologies’ Coil-on-Module (CoM) solutions—widely adopted in the Japanese market—enable thinner, more reliable dual-interface cards. The CoM architecture uses a specialized copper inlay compatible with both traditional PC substrates and sustainable alternatives such as ocean-recovered plastics, reducing mechanical stress during bending and improving long-term durability. Japan’s precision manufacturing ecosystem positions it as a key innovator in high-quality, thermally stable materials designed for next-generation contactless and biometric cards.

South Korea: Healthcare Digitization and High-Density Chip Lamination Driving Advanced Smart Card Materials

South Korea stands out for its advanced integration of smart card technologies into nationwide digital healthcare platforms and its continued breakthroughs in chip lamination and card durability. The country’s healthcare networks extensively use smart health insurance cards and patient identity credentials, requiring polymer substrates with high thermal stability and multi-layer lamination strength to support embedded secure-access chips and contactless antennas. This sustained demand drives South Korea’s focus on advanced PETG and PC composites that offer long lifecycle performance under heavy daily usage.

South Korean manufacturers are also pioneering high-density chip lamination techniques, essential for next-generation dual-interface banking cards and secure government credentials. These materials must support precise bonding of ultra-thin chips, antennas, and biometric elements without delamination. The country’s role as a hub for advanced electronics manufacturing accelerates its adoption of high-rigidity PC sheets, specialty adhesives, and hybrid card structures enabling ultra-thin, high-durability smart cards. With its innovation in medical, financial, and enterprise card technologies, South Korea continues to exert global influence on smart card material design and high-reliability lamination processes.

Competitive Landscape: Global Leaders Driving High-Security Polymers, Recycled Materials, and Advanced ID Technologies

The Smart Card Materials industry is defined by deep capabilities in polycarbonate chemistry, PETG engineering, recycled polymer integration, microcontroller security, and multilayer lamination technologies. Companies are investing aggressively in materials that support high-security IDs, biometric payment cards, contactless transit systems, and sustainable card programs. The competitive advantage lies in both material science expertise and the ability to support secure, high-volume manufacturing ecosystems.

Covestro AG delivers high-security polycarbonate films for unforgeable identity cards

Covestro is a global leader in supplying Makrofol® ID polycarbonate films and Platilon® TPU films, engineered specifically for secure documents and biometric e-passports. Its polycarbonate systems are optimized for monolithic lamination, ensuring exceptional resistance to delamination and tampering—critical for long-life government-issued credentials. Covestro’s advanced laser-reactive films, including its super-laser PC grades, enable deep, permanent, multidimensional engraving that cannot be replicated, providing a forensic security advantage. The company’s solutions support global government ID programs requiring long-term stability under mechanical stress, heat exposure, and frequent verification cycles.

Eastman Chemical Company advances PETG and hybrid polymer blends for sustainable and durable payment cards

Eastman leads the PETG smart card segment with its Eastar™ PETG copolyesters and specialty polycarbonate resins. These materials offer superior thermal resistance compared to PVC while maintaining excellent printability and lamination compatibility. Eastman is actively expanding hybrid PET/PC formulations that blend polycarbonate-level durability with PETG flexibility, meeting the requirements of dual-interface payment cards and emerging e-ID formats. With a growing emphasis on sustainability, Eastman is supporting financial institutions transitioning toward low-carbon, high-recycled-content card bodies while ensuring that antenna embedding and chip bonding remain reliable across high-speed production lines.

Solvay SA focuses on specialty PVDF and polyamide films for chemical-resistant and secure access badges

Solvay brings strong expertise in PVDF, polyamide resins, and high-performance thermoplastics used in overlays, protective films, and industrial access control cards. Its materials are designed for superior chemical resistance, dimensional stability, and surface protection, making them well-suited for harsh industrial environments and long-lifecycle commercial ID programs. Solvay’s strategic portfolio expansion in sustainable materials aligns with growing demand for bio-based and recycled-content polymers, positioning the company to support next-generation eco-friendly access card architectures.

SABIC strengthens recycled polycarbonate supply chains for global government ID programs

SABIC plays a central role in supplying LEXAN™ polycarbonate resins and TRUCIRCLE™ recycled polymer feedstocks to the smart card industry. With large-scale investment in recycled polymer technologies announced in November 2025, SABIC enables government agencies and financial institutions to adopt circular-economy-compliant polycarbonate cards without compromising structural integrity, heat resistance, or laser personalization performance. Its global manufacturing footprint and vertically integrated supply chain allow reliable high-volume production for national ID, healthcare, and border security programs worldwide.

Infineon Technologies defines material requirements through secure microcontroller innovation

As one of the world’s leading suppliers of Secure Elements (SEs), microcontrollers, and CIPURSE™ transit solutions, Infineon shapes the performance and material specifications of smart card bodies, even though it is not a polymer producer. The company’s SECORA™ and OPTIGA™ security platforms require substrates that allow precise antenna embedding, robust lamination, and long-term chip protection. Infineon’s rapid expansion of secure microcontroller capacity in May 2025 increases downstream demand for high-purity polymer sheets compatible with dual-interface and biometric card architectures. Its innovations are central to the global transition toward high-security, multi-application smart cards.

Smart Card Materials Market Report Scope

Smart Card Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.9 Billion

|

|

Market Size (2035)

|

$19.5 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Material Type (PVC, Polycarbonate, ABS, PETG, Sustainable Materials), By Card Type (Contact Smart Cards, Contactless Smart Cards, Dual-Interface Smart Cards), By End-Use Application (BFSI, Government ID & e-Passports, Telecommunications, Transportation, Healthcare, Retail & Loyalty Programs)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Thales, IDEMIA, Giesecke+Devrient (G+D), Infineon Technologies, NXP Semiconductors, CPI Card Group, Eastman Chemical, Solvay, SABIC, LG Chem, Teijin, Hengbao, Westlake Chemical, Toppan Printing

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Smart Card Materials Market Segmentation

By Material Type

- Polyvinyl Chloride (PVC)

- Polycarbonate (PC)

- Acrylonitrile Butadiene Styrene (ABS)

- PETG

- Sustainable Materials (PLA, recycled PVC, wood/bamboo composites)

By Card Type

- Contact Smart Cards

- Contactless Smart Cards (NFC/RFID)

- Dual-Interface Smart Cards

By End-Use Industry

- BFSI

- Government ID & e-Passports

- Telecommunications (SIM / eSIM)

- Transportation

- Healthcare

- Retail & Loyalty Programs

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Smart Card Materials Market

- Thales

- IDEMIA

- Giesecke+Devrient (G+D)

- Infineon Technologies

- NXP Semiconductors

- CPI Card Group

- Eastman Chemical

- Solvay

- SABIC

- LG Chem

- Teijin

- Hengbao

- Westlake Chemical

- Toppan Printing.

*- List not Exhaustive

Research Coverage: Smart Card Materials Market

The latest USDAnalytics Smart Card Materials Market study delivers a comprehensive assessment of how polymer innovation, security requirements, and sustainability commitments are reshaping next-generation card architectures. Spanning payment, ID, telecom, transit, and healthcare ecosystems, this report investigates the interplay between high-durability polycarbonate platforms, PETG and hybrid structures, metal inlay designs, advanced conductive adhesives, and emerging bio-based substrates. It captures recent breakthroughs in OLED-enabled cards, bamboo and recycled polymers, and high-temperature laminates while providing in-depth analysis reviews of BFSI digitalization, national e-ID rollouts, and biometric card adoption. The study highlights material-driven trade-offs around lifecycle cost, counterfeit resistance, and environmental footprint, benchmarking performance metrics from flex-cycle endurance to lamination stability. Supported by rigorous quantitative modeling and detailed vendor positioning, this report is an essential resource for material suppliers, card manufacturers, secure document integrators, and policy stakeholders seeking to align product roadmaps with evolving smart card security, durability, and ESG standards.

Scope Highlights

- Segmentation

- By Material Type: Polyvinyl Chloride (PVC), Polycarbonate (PC), Acrylonitrile Butadiene Styrene (ABS), PETG, Sustainable Materials (PLA, recycled PVC, wood/bamboo composites)

- By Card Type: Contact Smart Cards, Contactless Smart Cards (NFC/RFID), Dual-Interface Smart Cards

- By End-Use Industry: BFSI, Government ID & e-Passports, Telecommunications (SIM / eSIM), Transportation, Healthcare, Retail & Loyalty Programs

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Includes historic data from 2021–2025 and forecast insights for 2026–2034.

- Companies Covered: Includes analysis and profiles of 15+ leading players across polymers, security module providers, and smart card manufacturers.