Specialty and Fine Chemicals Market Valuation 2025–2034: $714.5 Billion to $1,176.7 Billion at 5.7% CAGR Driven by Custom Manufacturing, Sustainable Dispersions, and Portfolio Optimization

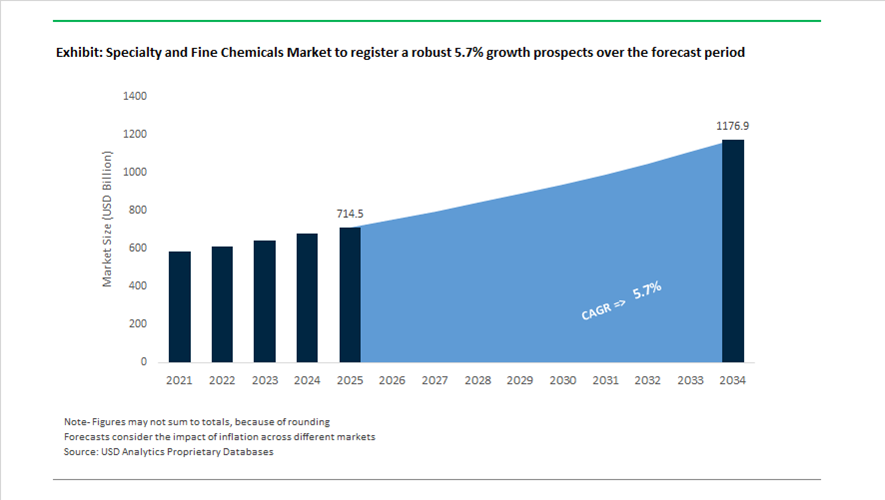

The global specialty and fine chemicals market is valued at $714.5 billion in 2025 and is projected to reach $1,176.7 billion by 2034, expanding at a CAGR of 5.7%. Growth is supported by rising demand for high-value performance chemicals, custom intermediates, polymer dispersions, electronic-grade materials, agrochemical actives, aroma chemicals, and advanced coatings additives across agriculture, pharmaceuticals, packaging, automotive, and electronics. Unlike commodity chemicals, specialty and fine chemicals are characterized by performance specificity, regulatory compliance, and application-driven innovation. Increasing localization of manufacturing, sustainability certification, and portfolio realignment toward higher-margin, technology-intensive segments are reshaping global competitive structures.

In May 2024, LyondellBasell divested its ethylene oxide and derivatives business to INEOS, enabling LyondellBasell to prioritize circularity and specialty polyolefins while strengthening INEOS’s integrated fine chemical value chain. In October 2024, Sudarshan Chemical Industries announced its acquisition of Germany-based Heubach Group, forming a global pigment and fine chemicals platform integrating advanced technological intellectual property with cost-efficient manufacturing. During 2024–2026, Matrix Fine Chemicals expanded its portfolio with specialized intermediates such as 3-Methyl-5-Nitrobenzoisothiazole and 1-Pyreneboronic Acid, targeting high-end life sciences R&D applications. These developments reflect consolidation and product line deepening in niche, high-complexity chemistries.

Strategic restructuring and green chemistry initiatives intensified in 2025. In January 2025, Evonik announced asset optimization within its silica business, including closure of its Waterford, NY site in mid-2025 and Havre de Grace, MD production in mid-2026, consolidating output into larger hubs to improve cost efficiency and supply resilience. In March 2025, Cosmo Specialty Chemicals launched COSEAL-601, a high-performance heat-seal coating engineered for aluminum foil laminates operating at 120–160°C, enhancing throughput in high-speed packaging lines. In May 2025, UPL launched Superform as a standalone specialty chemistries subsidiary focused on agriculture, healthcare, and flame retardant solutions, emphasizing green chemistry and custom manufacturing capabilities. The same month, Novopor Advanced Science acquired Pressure Chemical Company, strengthening its position in complex custom manufacturing for niche specialty applications. In September 2025, BASF India achieved REDcert2 certification at its Dahej and Mangalore dispersion plants, enabling supply of biomass-balanced polymer dispersions with reduced carbon footprint credentials.

Capacity additions and further streamlining shaped early 2026. In early 2026, BASF inaugurated its second dispersions production line at Daya Bay in Huizhou, China, addressing growing regional demand for specialty coatings and adhesive materials. In January 2026, BASF introduced a Near-Zero SVOC dispersion technology designed to improve indoor air quality performance in architectural coatings used in schools and healthcare facilities. LANXESS announced plans to shut down its aroma chemicals plant at Widnes in 2026 as part of a global efficiency program aimed at counteracting demand softness and high localized operating costs. These expansions, divestitures, sustainability certifications, and custom chemistry investments highlight how portfolio optimization, green manufacturing standards, and application-driven R&D are shaping the specialty and fine chemicals market toward $1.18 trillion by 2034.

Strategic Trends and High-Impact Opportunities in the Specialty and Fine Chemicals Market

Strategic Portfolio De-commoditization and Downstream Integration

The global specialty and fine chemicals market is undergoing a decisive structural shift away from volume-driven petrochemicals toward margin-rich, performance-led products. Large integrated chemical companies are actively pruning low-return commodity assets and reallocating capital toward downstream specialty platforms where formulation know-how, customer intimacy, and regulatory complexity act as durable entry barriers. This transition is not cyclical but strategic, reflecting investor pressure for capital discipline and resilience against feedstock volatility.

As of late 2024, BASF formally reinforced this direction under its “Winning Ways” strategy, committing between €1.5 billion and €2 billion annually to the Ludwigshafen site. These investments are focused on high-value intermediates, specialty polymers, and sustainable process innovations, signaling a clear pivot toward differentiated chemistries with pricing power rather than scale-driven commodities.

A parallel transformation is underway in emerging markets. In May 2025, the Government of India articulated a roadmap to build a $1 trillion petrochemical economy by 2040, explicitly identifying specialty chemicals as the primary growth engine, targeted to expand at a 10%–11% CAGR and reach 20% of total output. This policy clarity has accelerated private-sector action. Himadri Speciality Chemical announced a ₹4,800 crore investment program to pivot away from traditional carbon black toward advanced battery materials and specialty carbon derivatives, highlighting how downstream integration is becoming the preferred pathway for long-term value creation.

Policy-Driven Security Sourcing for Pharmaceutical Intermediates

Fine chemicals, particularly pharmaceutical intermediates, have moved from a cost-optimization discussion to a national security priority. Repeated supply chain disruptions and geopolitical tensions have exposed the strategic vulnerability created by concentrated API and KSM production, prompting governments to actively reshape sourcing economics through regulation and incentives.

In August 2025, the United States established the Strategic API Reserve (SAPIR) via executive order, creating a domestic stockpile of critical APIs while offering regulatory fast-tracking mechanisms such as FDA PreCheck for companies investing in local manufacturing. This policy effectively lowers time-to-market and compliance friction for domestic fine chemical producers, reshaping competitive dynamics in favor of high-complexity, onshore synthesis capabilities.

Trade policy has further reinforced this shift. The introduction of 15% surcharges on selected chemical imports from Europe and Asia in 2025 materially altered procurement economics for pharmaceutical companies. By September 2025, more than two dozen drug manufacturers had announced concrete U.S.-based expansion plans, creating a structurally captive market for domestic fine chemical suppliers capable of multi-step synthesis, stringent impurity control, and regulatory documentation. This environment is elevating fine chemical producers from transactional vendors to strategic partners in national healthcare resilience.

High-Purity Additives for Next-Generation Energy Storage

Energy storage has emerged as one of the most attractive growth vectors within specialty chemicals, transitioning from a niche opportunity into a critical global supply constraint. The shift toward Lithium Iron Phosphate and silicon-anode batteries is fundamentally changing additive requirements, with performance increasingly dependent on highly specialized conductive and interfacial materials that remain supply-constrained outside China.

This gap is catalyzing strategic capacity investments. Himadri Speciality Chemical is developing the first commercial LFP cathode plant outside China, with Phase I targeted for Q3 FY2027. Such projects are strategically significant, as they localize access to battery-grade materials while reducing exposure to geopolitical risk.

At the same time, battery manufacturers are demanding advanced conductive additives that improve electron mobility and stabilize the solid electrolyte interface under high cycling stress. PCBL Chemical, part of the RP-Sanjiv Goenka Group, recently commissioned a 4,000 MTPA acetylene black facility specifically aimed at this high-margin segment. These developments underscore how fine chemical capabilities in nanomaterials and purity control are becoming decisive enablers of the global energy transition.

The Bio-Revolution in Flavors, Fragrances, and Active Ingredients

Synthetic biology is redefining the economics of fine chemicals by enabling “natural-equivalent” molecules that combine the sustainability narrative of natural ingredients with the consistency and scalability of chemical synthesis. This convergence is creating a new premium segment across flavors, fragrances, and cosmetic actives, where brand owners demand traceability, low carbon intensity, and sensory consistency.

R&D investment patterns highlight the scale of this shift. International Flavors & Fragrances reported an R&D spend of $671 million in late 2025, with a significant allocation to its Polymer Bio-Revolution platform and IFF NEO™, a natural flavor portfolio produced without traditional citrus feedstocks. These initiatives demonstrate how fine chemistry and biotechnology are being integrated to future-proof ingredient supply chains.

Peers are following similar paths. Givaudan and IFF are increasingly deploying microbial fermentation to produce high-value molecules such as squalane and vanillin at commercial scale. Notably, IFF’s green hydrogen facility at its Benicarló site illustrates how carbon-neutral energy inputs are being embedded directly into specialty chemical production. Collectively, these moves position bio-enabled fine chemicals as one of the most structurally attractive growth opportunities in the global specialty and fine chemicals market.

Specialty and Fine Chemicals Market Share and Segmentation Insights

Pharmaceutical Fine Chemicals Lead the Specialty Chemicals Market with High-Value Drug Manufacturing Applications

Pharmaceutical fine chemicals accounted for 28.40% of the specialty and fine chemicals market in 2025, reflecting the strong demand for high-purity active pharmaceutical ingredients, advanced intermediates, and specialized excipients used in drug manufacturing. These chemicals require complex synthesis processes and strict compliance with global pharmaceutical quality standards, making them one of the highest value segments within the specialty chemicals industry. Pharmaceutical companies depend on reliable suppliers of fine chemicals to support drug development, clinical production, and commercial manufacturing. A key 2025 industry shift is the growing adoption of continuous manufacturing technologies in pharmaceutical production, where fine chemical manufacturers are investing in continuous flow synthesis systems to improve production efficiency, enhance quality control, and support rapid scale-up for new therapeutic compounds.

Pharmaceutical & Healthcare Sector Drives Global Demand for Specialty Chemicals

Pharmaceutical and healthcare represent the largest end-use segment in the specialty and fine chemicals market, accounting for 32.80% of total demand in 2025 due to the broad range of specialized chemicals required in modern pharmaceutical manufacturing. Drug production relies on active pharmaceutical ingredients, intermediates, formulation excipients, reagents, and purification materials, creating strong demand for high-value specialty chemical inputs. The sector’s stringent regulatory standards and complex manufacturing requirements support the development of advanced chemical technologies. A major 2025 industry trend is the rapid growth of biologics and cell-based therapies, which require specialized materials including cell culture media components, purification resins, stabilizers, and formulation excipients, creating new high-value opportunities within the pharmaceutical fine chemicals ecosystem.

Specialty and Fine Chemicals Market Competitive Landscape

The global specialty and fine chemicals market in 2026 is shaped by decarbonization strategies, portfolio streamlining, and expansion into high-growth sectors such as battery materials, semiconductors, and specialty additives. Leading players are focusing on cost optimization, regional production, and high-margin specialty chemical innovation.

BASF Strengthens Verbund Integration and Cost Optimization with €2.3 Billion Savings Target and Zhanjiang Expansion

BASF SE continues to dominate the specialty and fine chemicals market through its “Winning Ways” strategy, achieving €1.7 billion in cost reductions and targeting €2.3 billion in annual savings by 2026. The commissioning of its Zhanjiang Verbund site strengthens localized production for Asia-Pacific markets. Portfolio optimization includes divestments such as the Softex business and decorative paints unit to focus on high-margin segments. BASF’s integrated Verbund model enhances operational efficiency and feedstock utilization across specialty chemical value chains. Growth is concentrated in Agricultural Solutions and Nutrition & Care segments, which are expected to drive earnings expansion. Its scale, integration, and restructuring strategy reinforce leadership in global specialty chemicals.

Evonik Advances High-Performance Specialty Chemicals with Focus on ROCE Improvement and Advanced Technologies Growth

Evonik Industries AG is sharpening its specialty chemicals portfolio by prioritizing high-margin Advanced Technologies and Custom Solutions segments. The company reported €1.87 billion adjusted EBITDA in 2025 despite a 7% decline in sales, reflecting resilience in specialty additives and high-performance polymers. Its new dividend policy tied to 40–60% of adjusted net income signals disciplined capital allocation. Evonik is targeting an 11% ROCE, up from 6.1%, by focusing on innovation-driven, value-added chemical solutions. Its offerings include materials for 3D printing, membranes, and consumer care applications. The company’s strategic pivot away from commodity chemicals strengthens profitability and long-term competitiveness.

Clariant Expands Sustainable Specialty Chemicals and APAC Production with Strong Care Chemicals Performance

Clariant AG is positioning itself as a sustainability-driven specialty chemicals leader, achieving CHF 50 million in savings in 2025 with a target of CHF 80 million by 2026. Its Care Chemicals segment delivers strong margins of 18.3%, focusing on high-value personal and home care applications. Expansion of local production in China to over 50% supports regional demand and supply chain resilience. Investments in catalyst plants and innovation hubs enhance R&D capabilities in Asia-Pacific markets. Clariant’s commitment to reducing Scope 1 and 2 emissions by 40% aligns with global ESG requirements. Its focus on sustainable chemistry and regional growth strengthens its competitive positioning.

Arkema Strengthens Specialty Materials Portfolio with Battery Technology Partnerships and Strategic Divestments

Arkema S.A. is accelerating its transition to a pure-play specialty materials company through targeted partnerships and portfolio restructuring. The MoU with Senior focuses on next-generation battery separator technologies and advanced adhesion systems, reinforcing its position in energy storage markets. The company achieved 16% sales growth in high-value segments such as batteries, healthcare, and 3D printing in 2025. Divestment of its Plastic Additives business enables greater focus on core specialty materials. Arkema’s Kynar® PVDF remains a benchmark material for lithium-ion batteries and semiconductor processing. Its strategic alignment with energy transition trends enhances its market relevance.

Solvay Focuses on Essential Chemistry and Bio-Circular Innovation with Strong Cost-Saving Initiatives

Solvay S.A. is reinforcing its position in specialty and fine chemicals through its “Essential Chemistry” focus, supported by €101 million in cost savings in 2025. Strategic restructuring includes site closures and capacity optimization in Europe to improve efficiency. The launch of Europe’s first bio-circular silica facility supports sustainable applications in tires and rubber. Solvay is scaling production of electronic-grade hydrogen peroxide to meet semiconductor industry demand. Its integration capabilities across key chemical intermediates strengthen its role in high-growth sectors. The company’s emphasis on sustainability and operational efficiency supports long-term competitiveness.

LANXESS Strengthens Specialty Additives and Consumer Protection Portfolio Through Cost Discipline and Strategic Divestments

LANXESS AG is executing a rigorous consolidation strategy to enhance profitability and focus on high-margin specialty chemicals. The company reduced net financial liabilities by 15% in 2025, supported by divestment of its Urethane Systems business. Additional cost-saving measures target €100 million in annual savings by 2028 through organizational streamlining. Its Consumer Protection segment achieved a 15.9% margin despite lower volumes, highlighting resilience in specialty applications. LANXESS is expanding into flavor and fragrance and water treatment technologies to diversify its portfolio. Its focus on specialty additives and disciplined capital management strengthens its competitive position.

China Specialty and Fine Chemicals Market Rebalanced Toward High-End Self-Sufficiency

China’s specialty and fine chemicals industry is transitioning from volume-led expansion to value-stabilized growth under direct state coordination. In September 2025, the Ministry of Industry and Information Technology issued the Growth Stabilization Plan for 2025–2026, targeting annual chemical value-added growth above 5% while prioritizing high-end polyolefins, electronic chemicals, and performance materials. A central pillar of this strategy is semiconductor independence. China has mandated an increase in domestic self-sufficiency for critical lithography and etching intermediates from 85% to over 90% by the end of 2026, driving accelerated investment in electronic-grade reagents and purification technologies.

Feedstock and infrastructure policy are reinforcing resilience. New directives tightly control traditional refining capacity while incentivizing coal-to-methanol integration and CCUS demonstration projects to stabilize domestic raw material chains. State-backed innovation centers for advanced fine chemicals are being established to move producers toward integrated chemical solutions rather than commodity sales. This shift is exemplified by BASF SE, which operationalized new specialty surfactant and high-performance polyamide lines at its Zhanjiang Verbund site in 2025. Concurrently, Green Manufacturing standards implemented in 2025 have phased out small, high-emission batch plants in the Yangtze River Delta, consolidating output into digitally enabled Smart Chemical Parks.

United States Specialty and Fine Chemicals Market Defined by Reshoring and Purity Standards

The United States specialty and fine chemicals sector is being reshaped by reshoring dynamics, semiconductor-driven purity requirements, and regulatory substitution. According to the 2026 Outlook from the Society of Chemical Manufacturers & Affiliates, contract manufacturing has pivoted sharply toward higher-value processes, with esterification now representing over 50% of specialized operations, more than double the 2024 level. This reflects a broader shift toward resilient domestic supply for pharmaceuticals, coatings, and functional intermediates.

Technology and compliance are converging as competitive levers. CHIPS Act incentives have driven heavy investment in 5N-purity reagents to support 2 nm and 3 nm chip fabrication, elevating entry barriers across electronic chemicals. Automation is accelerating, with more than 65% of U.S. fine chemical plants deploying AI-based process optimization and hazard detection systems by late 2025 to offset skilled labor constraints. Regulatory pressure is also material. The Environmental Protection Agency finalized TSCA risk management rules in 2025 covering several specialty solvents, forcing rapid transitions toward low-VOC and halogen-free alternatives. Regionally, Georgia and Michigan have emerged as focal points for investment, jointly securing over USD 50 billion in funding for EV battery chemicals and advanced material manufacturing.

India Specialty and Fine Chemicals Market Accelerated by Policy Scale and Export Orientation

India’s specialty and fine chemicals industry is scaling rapidly through coordinated policy frameworks and export competitiveness. The Petroleum, Chemicals and Petrochemical Investment Regions policy targets USD 420 billion in cumulative investment by 2030, anchoring large, integrated specialty clusters. Complementing this, the Production-Linked Incentive scheme for bulk drugs has enabled domestic manufacturing of 41 key starting materials, materially reducing dependence on imported intermediates and strengthening pharmaceutical supply security.

Exports are now structurally dominant. Specialty chemicals account for roughly 80% of India’s chemical exports, with 2025 marked by record shipments of agrochemical intermediates and performance dyes. Bio-based innovation is gaining momentum under the BioE3 Policy launched in late 2024, which provides capital subsidies for bio-foundries producing specialty polymers from agricultural waste. Feedstock diversification is evident in starch-to-polyol investments. Domestic leaders such as Gulshan Polyols expanded sorbitol and specialty sweetener capacity in 2025, targeting pharmaceutical excipients and oral care formulations with higher margin profiles.

Germany Specialty and Fine Chemicals Market Anchored by Energy Transition and Niche Leadership

Germany’s specialty and fine chemicals sector is demonstrating resilience through niche dominance, despite energy cost pressures. In October 2025, Alzchem Group AG reported a 9% increase in specialty segment sales, driven by demand for high-purity creatine under the Creapure brand and defense-related nitroguanidine applications. To address energy volatility, German producers have introduced Green Surcharges for products manufactured using renewable electricity, a strategy aligned with the EU Carbon Border Adjustment Mechanism implemented in 2025.

Capacity expansion is selectively targeted. Alzchem is preparing to commission a world-scale guanidine nitrate plant in the second half of 2026, serving automotive airbag and pharmaceutical intermediate markets. Elsewhere, Evonik Industries AG expanded POLYVEST polybutadiene output at its Marl site to secure supply for high-performance rubber processing. Sustainability is extending into water treatment, where German specialists have transitioned 30% of flocculant portfolios to bio-based solutions to comply with upcoming 2026 EU Water Framework Directive requirements.

Brazil Specialty and Fine Chemicals Market Boosted by Fiscal Incentives and Bio-Agriculture

Brazil’s specialty and fine chemicals industry is entering an incentive-driven expansion phase. The approval of the Special Programme for the Sustainability of the Chemical Industry in November 2025 provides up to USD 555 million annually in tax credits for companies reinvesting at least 8% of revenues into R&D. The program explicitly promotes a shift from naphtha toward natural gas and bio-based feedstocks, positioning Braskem as a primary beneficiary, with potential annual gains estimated at USD 380 million from 2026.

Agricultural biosolutions are a core growth vector. Brazil has become the fastest-growing global market for biopesticides, with firms such as FMC Corporation and Life Biological Control launching fungi-based bioinsecticides during 2024–2025 for corn and soybean protection. Infrastructure investment is also advancing, as Braskem approved a BRL 4.2 billion expansion of its Rio de Janeiro complex in October 2025, modernizing ethylene and polyethylene assets to improve energy efficiency and specialty integration.

South Korea Specialty and Fine Chemicals Market Powered by Semiconductors and Biopharma

South Korea’s specialty and fine chemicals market is closely coupled with semiconductor leadership and biohealth ambitions. The K-Bio Leap Strategy unveiled in late 2025 aims to double biohealth exports by 2030, targeting the creation of three blockbuster drugs and establishing the country as a top-three global clinical trial hub. This has intensified demand for high-value pharmaceutical intermediates and fine chemicals used in biologics manufacturing.

Semiconductors remain the primary pull factor. Industrial data from July 2025 showed a 20.5% increase in semiconductor output, directly lifting demand for ultra-high-purity photoresists and specialty etching gases. Investment momentum is visible in contract manufacturing. Celltrion announced a USD 330 million acquisition of a U.S. manufacturing facility in late 2025 as part of a KRW 1.4 trillion investment plan to expand biopharmaceutical fine chemical capabilities.

Comparative Snapshot: Country-Level Specialty and Fine Chemicals Dynamics

Specialty and Fine Chemicals Market County Level Snapshot

|

Country

|

Core Policy Driver

|

Strategic Focus Areas

|

Structural Impact

|

|

China

|

Growth stabilization, self-sufficiency

|

Electronic chemicals, smart parks

|

Value-focused consolidation

|

|

United States

|

Reshoring, CHIPS Act, TSCA

|

High-purity reagents, automation

|

Resilient domestic supply

|

|

India

|

PCPIR, PLI, BioE3

|

Exports, bio-based specialties

|

Rapid scale and cost advantage

|

|

Germany

|

CBAM, niche specialization

|

Guanidines, bio-flocculants

|

Premium, energy-adjusted output

|

|

Brazil

|

PRESIQ incentives

|

Bio-feedstocks, biopesticides

|

R&D-led expansion

|

|

South Korea

|

K-Bio Leap, semiconductors

|

Photoresists, CDMO chemicals

|

Technology-driven demand

|

Specialty and Fine Chemicals Market Report Scope

Specialty and Fine Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$714.5 Billion

|

|

Market Size (2034)

|

$1176.7 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Specialty Chemical Type (Agrochemicals, Electronic Chemicals, Pharmaceutical Fine Chemicals, Specialty Polymers, Construction Chemicals, Water Treatment Chemicals, Food & Feed Additives, Personal Care & Cosmetic Chemicals), By End-Use Industry (Pharmaceutical & Healthcare, Electronics & Semiconductors, Agriculture, Automotive & Transportation, Building & Construction, Consumer Goods, Oil & Gas & Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Evonik Industries AG, DuPont de Nemours Inc., Solvay S.A., Eastman Chemical Company, Clariant AG, Lanxess AG, Mitsubishi Chemical Group, Sumitomo Chemical Co. Ltd., Arkema S.A., Nouryon, Albemarle Corporation, Huntsman Corporation, Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty and Fine Chemicals Market Segmentation

By Specialty Chemical Type

- Agrochemicals

- Electronic Chemicals

- Pharmaceutical Fine Chemicals

- Specialty Polymers

- Construction Chemicals

- Water Treatment Chemicals

- Food & Feed Additives

- Personal Care & Cosmetic Chemicals

By End-Use Industry

- Pharmaceutical & Healthcare

- Electronics & Semiconductors

- Agriculture

- Automotive & Transportation

- Building & Construction

- Consumer Goods

- Oil & Gas & Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty and Fine Chemicals Industry

- BASF SE

- Dow Inc.

- Evonik Industries AG

- DuPont de Nemours Inc.

- Solvay S.A.

- Eastman Chemical Company

- Clariant AG

- Lanxess AG

- Mitsubishi Chemical Group

- Sumitomo Chemical Co. Ltd.

- Arkema S.A.

- Nouryon

- Albemarle Corporation

- Huntsman Corporation

- Wacker Chemie AG

*- List not Exhaustive