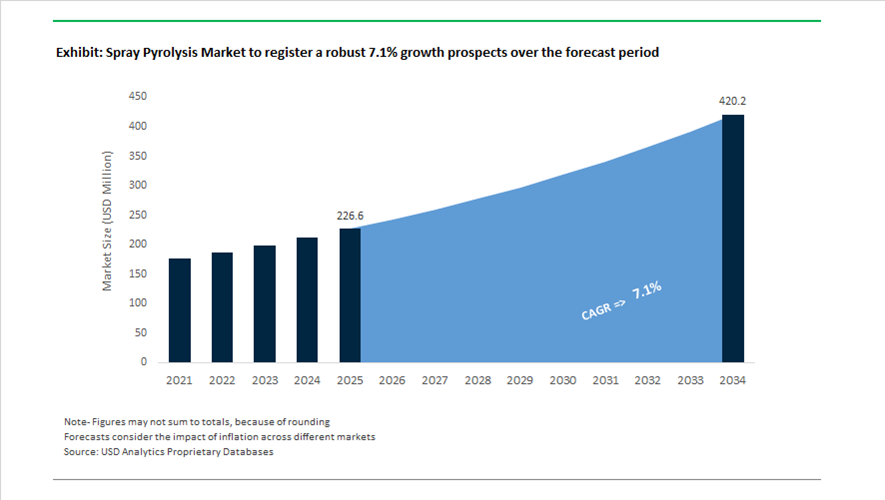

Spray Pyrolysis Market Valuation 2025–2034: $226.6 Million to $420.1 Million at 7.1% CAGR Accelerated by Battery Materials, Catalyst Engineering, and Waste-to-Energy Systems

The global spray pyrolysis market is valued at $226.6 million in 2025 and is projected to reach $420.1 million by 2034, expanding at a CAGR of 7.1%. Growth is underpinned by rising adoption of ultrasonic spray pyrolysis systems, nanoparticle synthesis platforms, catalyst precursor production, battery electrode coatings, and waste-to-energy pyrolytic conversion technologies. High-purity metal oxide powders, spherical nanoparticles, thin-film functional coatings, and advanced ceramic materials produced via spray pyrolysis are increasingly critical in lithium-ion batteries, solid oxide fuel cells, aerospace composites, semiconductors, and environmental remediation. The technology’s ability to deliver uniform particle morphology, controlled droplet size distribution, and scalable inline processing makes it a preferred route for next-generation materials engineering and decarbonized industrial systems.

Commercialization momentum strengthened through 2024 and 2025. In May 2024, Nanosonic launched a new commercial nanoparticle synthesis product line utilizing spray pyrolysis to produce specialized metal-oxide materials for military and aerospace coatings. In late 2024, Macrotek delivered an advanced pyrolysis cleanup equipment set for a large-scale biosolid-to-syngas project in the United States, integrating spray towers and heat exchangers to purify pyrolysis-derived syngas streams. In early 2025, Sono-Tek expanded its manufacturing capacity to meet growing demand for its Impact ARRAY ultrasonic spray pyrolysis systems deployed in wide-area energy coating pilot lines. In March 2025, Sono-Tek introduced a dedicated ultrasonic spray pyrolysis platform engineered for nanoparticle coatings on battery electrodes and fuel cells, offering advanced droplet size control optimized for high-capacity nickel-rich cathodes. In June 2025, Hexion opened its centralized Global Innovation Lab in Ohio, incorporating spray pyrolysis-derived powders into high-performance thermoset resin formulations for aerospace composites.

Battery manufacturing and energy transition applications accelerated in late 2025 and 2026. In July 2025, Sihai Energy Technology launched upgraded pyrolysis machines delivering a 30% efficiency improvement and reducing processing cycles to under six hours while lowering industrial emissions. By October 2025, Ola Electric commissioned 1.4 GWh of battery manufacturing capacity under India’s ACC PLI scheme, integrating advanced material synthesis processes including pyrolytic techniques. In January 2026, France formally recognized tyre pyrolysis oil as a legitimate raw material for the chemical industry, catalyzing industrial-scale pyrolysis system deployment across Europe. In February 2026, Felix Industries expanded hazardous waste treatment capacity in India using specialized pyrolysis systems aligned with Zero Liquid Discharge regulations. During the same month, Axens completed its acquisition of Eurecat, strengthening lifecycle management of advanced catalysts frequently synthesized using high-purity spray pyrolysis methods. Also in February 2026, Shin-Etsu scheduled the opening of its Zhejiang specialty plant producing alumina-based emulsions and pyrolytic additives for semiconductor applications. These battery-driven investments, catalyst lifecycle integrations, waste-to-energy expansions, and regulatory endorsements are reinforcing structural growth in the spray pyrolysis market through 2034.

Process-Led Trends and Commercial Opportunities in the Spray Pyrolysis Market

Scaling Pilot-to-Commercial Production of Cathode Active Materials for Solid-State and LFP Batteries

The Spray Pyrolysis Market is entering a decisive scale-up phase as battery manufacturers seek production routes that deliver consistent particle morphology, narrow size distributions, and precise stoichiometric control. Spray pyrolysis has emerged as a preferred alternative to conventional co-precipitation for Cathode Active Materials because it enables single-crystal and spherical particle formation, directly improving cycle life, thermal stability, and safety performance in next-generation electric vehicle platforms. These attributes are especially critical for solid-state batteries and Lithium Iron Phosphate chemistries, where uniformity and defect control directly influence energy density and fast-charging capability.

Policy-linked incentives are accelerating this transition. In April 2024, 6K Energy confirmed that its UniMelt microwave plasma system, a high-throughput spray pyrolysis variant, is producing NMC811 and LFP powders that meet Inflation Reduction Act domestic content thresholds. The company’s PlusCAM manufacturing facility in Jackson, Tennessee is scheduled for mid-2025 start of production and is designed to output thousands of tons of cathode material annually. Complementing this industrial momentum, techno-economic assessments released by the U.S. Department of Energy in late 2024 indicate that Flame-Assisted Spray Pyrolysis can reduce the minimum carbonate selling price of cathode materials by up to 17% compared with legacy routes. This cost advantage is directly linked to eligibility for the $7,500 EV tax credit, including the 10% production credit for electrode active materials, positioning spray pyrolysis as both a technical and regulatory enabler in the North American battery supply chain.

High-Purity Doped Metal Oxides for MicroLED and Transparent Display Architectures

Beyond batteries, spray pyrolysis is gaining strategic importance in the display materials ecosystem as manufacturers pivot toward MicroLED and transparent OLED technologies. These platforms require Transparent Conductive Oxides with exceptional crystallinity, low sheet resistance, and uniform optical transmission, characteristics that are difficult to achieve at scale using vacuum-based sputtering alone. Spray pyrolysis offers a vacuum-free, cost-efficient deposition pathway for doped oxides such as antimony-doped tin oxide and aluminum-doped zinc oxide, supporting high-volume manufacturing without compromising electrical performance.

At SID 2025, panel makers including AUO and Tianma demonstrated transparent MicroLED displays exceeding 50% transparency with brightness levels ranging from 1,000 to 10,000 nits. These performance benchmarks are underpinned by spray-pyrolyzed TCO layers achieving sheet resistances as low as 10–20 ohms per square, enabling seamless large-area tiling and automotive head-up display integration. Geopolitical and industrial policy factors further reinforce this trend. China’s Made in China initiative targets 80% domestic sourcing of transparent conductive films by 2030, prompting regional investments in high-throughput spray pyrolysis lines as a replacement for capital-intensive sputtering. This shift is also driven by tariff pressures that have pushed duties on certain display components to levels approaching 170%, making localized spray pyrolysis capacity a strategic necessity rather than a cost optimization.

Green Hydrogen Catalysts for Large-Scale Electrolyzer Deployment

The global push toward green hydrogen production is unlocking a high-value opportunity for spray-pyrolyzed catalyst powders. Electrolyzer economics increasingly depend on reducing precious metal loading while maintaining catalytic efficiency and durability, a balance that spray pyrolysis can achieve through the continuous synthesis of doped oxide spinels and perovskite structures with high surface area. This capability positions spray pyrolysis as a cornerstone technology for next-generation PEM and alkaline electrolyzers.

In November 2025, India’s Ministry of New and Renewable Energy awarded 3,000 MW of annual electrolyzer manufacturing capacity under the National Green Hydrogen Mission, supported by a budget of INR 19,744 crore. The program explicitly promotes scalable production routes for low-cost catalyst powders, highlighting spray pyrolysis as a preferred method to meet India’s 5 million metric ton per year green hydrogen target by 2030. Parallel research collaboration under the EU–India Trade and Technology Council in July 2025 demonstrated that spray pyrolysis enables one-step synthesis of multicomponent nanoparticles at production rates of up to 10 kilograms per hour. This continuous processing advantage supports the rapid deployment of smart catalysts with long-term stability, aligned with the more than 800,000 tonnes of annual green hydrogen capacity allocated globally by mid-2025.

Microencapsulated Phase Change Materials for Net-Zero Building Envelopes

Energy-efficient construction is emerging as a secondary growth vector for the Spray Pyrolysis Market, driven by the integration of Phase Change Materials into building envelopes. Spray pyrolysis offers a differentiated encapsulation mechanism that surrounds paraffin or salt-hydrate cores with silica or alumina shells, preventing leakage, enhancing thermal cycling durability, and enabling long service life in architectural applications.

In January 2024, Armstrong World Industries introduced ceiling systems incorporating PCM technology, demonstrating up to 15% reductions in building energy consumption. These results have intensified demand for scalable microencapsulation techniques capable of supporting large construction projects. Between 2023 and 2025, DIC Corporation and Phase Change Solutions advanced commercial partnerships to deploy bio-based PCM systems across office and logistics facilities in Japan. As net-zero building codes tighten globally, spray pyrolysis-based encapsulation is gaining traction as a reliable route to produce thermoplastic- and polymer-stabilized PCMs. With this segment projected to expand at a high double-digit growth rate, spray pyrolysis suppliers are positioned to capture value at the intersection of construction, energy efficiency, and specialty materials innovation.

Spray Pyrolysis Market Share and Segmentation Insights

Ultrasonic Spray Pyrolysis Systems Lead the Market Through Precise Thin Film and Nanoparticle Production

Ultrasonic spray pyrolysis systems accounted for 38.60% of the spray pyrolysis market in 2025, reflecting their strong performance in controlled thin-film deposition and nanoparticle synthesis. These systems utilize ultrasonic atomization to generate uniform droplets, enabling precise control over particle size distribution, film thickness, and material morphology. They are widely used in electronics manufacturing, advanced materials synthesis, and biomedical coatings. A key 2025 industry development is the advancement of industrial-scale ultrasonic spray pyrolysis systems, where multi-nozzle arrays and continuous processing configurations enable high-volume production of functional coatings and nanomaterials suitable for commercial manufacturing environments.

Metal Oxides Dominate Spray Pyrolysis Materials for Electronics and Energy Applications

Metal oxides accounted for 42.80% of materials produced using spray pyrolysis in 2025, making them the leading material category across advanced material synthesis. Materials such as titanium dioxide, zinc oxide, tin oxide, indium tin oxide, and aluminum oxide are widely produced using spray pyrolysis due to their well-established precursor chemistry and strong functional properties. These materials are used in transparent conductive films, sensors, catalysts, and battery components. A major 2025 market driver is the increasing demand for battery materials in lithium-ion energy storage systems, where spray pyrolysis is used to synthesize cathode materials such as NMC and LFP with controlled particle morphology and composition.

Electronics and Semiconductors Drive Spray Pyrolysis Adoption for Advanced Thin-Film Deposition

Electronics and semiconductors represented 38.60% of spray pyrolysis market applications in 2025, reflecting the technology’s ability to produce high-quality functional thin films required for modern electronic devices. Spray pyrolysis is used to deposit transparent conductive oxides, dielectric layers, sensor coatings, and antireflective films for applications including displays, photovoltaic cells, and semiconductor devices. Its ability to operate at atmospheric pressure and relatively low processing temperatures makes it compatible with emerging manufacturing techniques. A significant 2025 industry trend is the growth of flexible and printed electronics, where spray pyrolysis enables deposition of functional materials on flexible polymer substrates used in wearable electronics, sensors, and Internet of Things devices.

Spray Pyrolysis Market Competitive Landscape

The spray pyrolysis market in 2026 is driven by ultrasonic atomization, AI-enabled process control, and scalable thin-film deposition for semiconductors, solid-state batteries, and TCO coatings. Industry leaders are advancing open-architecture systems to bridge R&D and industrial production while improving uniformity, purity, and energy efficiency.

Sono-Tek Advances Ultrasonic Spray Systems for High-Uniformity Thin Films and Energy-Efficient Coatings

Sono-Tek is leading innovation in ultrasonic spray pyrolysis with high-uniformity coating systems that minimize precursor waste. Its upgraded Proline systems generate sub-20 micron droplets, enabling precision deposition for perovskite solar cells and advanced electronics. The company is promoting atmospheric spray pyrolysis as a low-energy alternative to CVD/PVD, reducing energy consumption by up to 60%. Its technology achieves up to 98% coating uniformity, critical for PEM fuel cell catalysts and semiconductor thin films. Expansion into medical coatings highlights its versatility in controlled drug-release applications. Sono-Tek’s precision flow control and scalable platforms position it strongly in sustainable thin-film manufacturing.

BÜCHI Integrates AI-Driven Spray Pyrolysis and NIR Analytics for High-Purity Material Development

BÜCHI is bridging laboratory-scale spray pyrolysis with industrial pilot production through advanced instrumentation and analytics. The Mini Spray Dryer S-300 incorporates AI-assisted optimization to predict particle morphology based on process parameters, enhancing R&D efficiency. Integration of NIR sensors via the NeoSpectra platform enables real-time monitoring of moisture and composition in pyrolyzed powders. Its chromatography systems ensure ultra-high purity precursor preparation, reducing defect rates in advanced materials. Strategic partnerships are extending its encapsulation technologies into precision agriculture applications. BÜCHI’s ecosystem approach supports high-value material synthesis for semiconductors and specialty chemicals.

MTI Corporation Enables Rapid Prototyping of Battery Materials with Modular Spray Pyrolysis Systems

MTI Corporation is a key enabler of spray pyrolysis adoption in energy storage R&D through cost-effective and modular equipment. Its vertical spray pyrolysis systems feature dual-zone furnaces reaching 1200°C, supporting synthesis of ceramic powders and solid electrolytes. The introduction of electrostatic spray pyrolysis modules allows processing of air-sensitive materials under inert environments. MTI’s expanded precursor materials library accelerates lithium-sulfur battery research and advanced cathode development. Its rapid prototyping capability enables transition from design to material synthesis within 48 hours. The company’s flexible lab-scale systems are widely used in academic and industrial battery innovation programs.

Holmarc Targets TCO and Sensor Markets with Pulse Spray Pyrolysis and Optical Monitoring Integration

Holmarc is differentiating through highly customizable spray pyrolysis systems tailored for transparent conductive oxide coatings and gas sensor fabrication. Its pulse spray pyrolysis technology improves film crystallinity by maintaining consistent substrate temperature during deposition. The company’s systems support large-area coating of ITO and FTO substrates, critical for display and photovoltaic applications. Integrated optical and thermal monitoring ensures high reproducibility across production batches. Holmarc’s equipment is widely used for SnO₂ and ZnO gas sensors, offering enhanced sensitivity through nanostructured films. Its mechatronics-driven design enables precise control over deposition parameters in advanced materials manufacturing.

Yamato Scientific Expands High-Capacity Spray Pyrolysis for Pharmaceutical and Semiconductor Applications

Yamato Scientific is advancing spray pyrolysis with high-capacity systems designed for pharmaceutical powders and specialty chemicals. Its DL410 spray dryer supports fine particle production in the 10–100 micrometer range, ideal for inhalable drug formulations. The integration of solvent recovery units enables safe processing of organic precursors with up to 95% recovery efficiency. Yamato’s expansion into curing and annealing equipment supports post-pyrolysis processing for nanomaterials and coatings. The company emphasizes contamination-free processing using high-grade materials to meet semiconductor and biotech standards. Its systems are increasingly used in high-purity material production environments.

Nordson Enables Industrial-Scale Spray Pyrolysis with Precision Dispensing and High-Throughput Integration

Nordson is a critical enabler of large-scale spray pyrolysis through precision dispensing technologies and system integration. Its 781S spray valves provide consistent flat-fan patterns for uniform coating on industrial conveyor systems. The Precision Pulse control upgrade enables microsecond-level timing, essential for multi-layer thin-film deposition in photovoltaics and electronics. Nordson reported $2.6 billion in 2025 sales, with growth driven by semiconductor and advanced technology segments. Its integration with OEM furnace systems supports turnkey production lines for catalytic coatings and functional materials. Nordson’s precision engineering enhances scalability and repeatability in industrial spray pyrolysis applications.

China Spray Pyrolysis Market Accelerated by Semiconductor Localization and Solar Glass Scale-Up

China has positioned spray pyrolysis as a strategic thin-film deposition platform within its advanced manufacturing agenda. Under the updated Made in China 2025 framework, targeted subsidies for ultrasonic spray pyrolysis equipment have materially accelerated industrial adoption. By late 2025, domestic manufacturers reported ultrasonic spray pyrolysis penetration in thin-film transistor fabrication that is roughly 30% higher than the global average, reflecting policy-backed substitution of imported vacuum-based deposition tools. This transition supports localization of display backplanes and optoelectronic components, where uniformity over large substrates is increasingly critical.

Photovoltaics remain a parallel growth engine. The Chinese Academy of Sciences documented a 40% increase in spray pyrolysis-related research activity between 2021 and 2024, with strong emphasis on transparent conducting oxide layers for domestic solar glass. Industrialization has followed research momentum. In November 2025, Siansonic Technology and HANSUN Ultrasonic commissioned automated lines capable of processing 300 mm wafers, signaling readiness for high-end optoelectronics. In parallel, Yangtze River Delta chemical clusters have scaled flame spray pyrolysis for multi-metal oxide catalysts, achieving measurable reductions in precursor waste compared with wet-chemical synthesis.

United States Spray Pyrolysis Market Driven by CHIPS Funding and Thin-Film Solar Commercialization

In the United States, spray pyrolysis has moved from laboratory-scale experimentation to a funded pillar of semiconductor and clean energy manufacturing. Federal allocations under the CHIPS and Science Act, exceeding $52.7 billion, have catalyzed widespread research into spray-based deposition for wide-bandgap semiconductors. During 2025 alone, U.S. national laboratories reported a 65% increase in projects utilizing spray pyrolysis, reflecting confidence in its scalability for compound semiconductors and power electronics.

Solar manufacturing provides additional demand depth. The U.S. Department of Energy projects domestic thin-film solar capacity surpassing 50 GW by 2025, with spray pyrolysis cited as a primary lever for reducing the cost of TCO deposition. Efficiency validation has reinforced investor interest. Data published by the National Renewable Energy Laboratory in 2024–2025 showed perovskite absorber layers deposited via spray pyrolysis reaching 23.6% efficiency, triggering private equity inflows into North American greentech startups. Equipment innovation has followed, with Sono-Tek Corporation expanding its ultrasonic systems portfolio in late 2024 for semiconductor-grade and bio-active coatings.

India Spray Pyrolysis Market Anchored in Indigenous Equipment and Semiconductor Mission

India’s spray pyrolysis ecosystem is developing along two complementary tracks: renewable energy valorization and semiconductor manufacturing. The Ministry of New and Renewable Energy extended the National Bioenergy Programme through FY 2025–26, explicitly supporting biomass-based pyrolysis and downstream syngas utilization. While this program is broader than thin films, it has strengthened institutional familiarity with pyrolysis technologies, lowering barriers for spray-based variants in materials processing.

Localization of equipment is the defining differentiator. In 2025, CSIR-NIIST partnered with Delgado Coating & Technology Solutions to launch India’s first indigenous high-precision spray pyrolysis system for fluorine-doped tin oxide coatings. This milestone directly addresses import dependence for transparent conducting substrates. Following approvals under the India Semiconductor Mission in August 2025, domestic demand for spray pyrolysis tools for dielectric layer deposition rose by an estimated 22% year over year. Equipment manufacturers such as Holmarc Opto-Mechatronics and Navson Technologies expanded cleanroom-certified automated systems to serve aerospace and medical device applications.

Japan Spray Pyrolysis Market Linked to Green Growth and Photovoltaic Performance

Japan’s spray pyrolysis market is closely aligned with national materials innovation funding and high-efficiency photovoltaics. Under the Green Growth Strategy, the Ministry of Economy, Trade and Industry allocated ¥43.2 billion between 2023 and 2025 for materials science, with approximately 15% directed toward thin-film technologies including flame-assisted spray pyrolysis. This funding has supported incremental improvements rather than disruptive scale-ups, consistent with Japan’s precision manufacturing model.

Industry uptake is evident in solar manufacturing. The Japanese Photovoltaic Energy Association reported a 34% increase in domestic solar panel production using spray pyrolysis for efficiency enhancement during 2023–2025. Supporting analytics have advanced in parallel. Frontier Laboratories introduced advanced pyrolysis-GCMS systems in late 2024, improving characterization of polymers and nanoparticles synthesized via spray routes, which is critical for quality control in electronics and coatings.

Germany Spray Pyrolysis Market Integrated into Hydrogen and Digital Manufacturing Systems

Germany’s spray pyrolysis landscape is distinguished by its integration into hydrogen technologies and digitally controlled manufacturing. Engineering collaborations between Buhler AG and BASF have embedded flame spray pyrolysis into low-carbon hydrogen initiatives, producing alumina-based catalysts optimized for methane pyrolysis. These catalysts directly support Germany’s strategy to decarbonize hydrogen production while improving reactor efficiency.

Process control represents the second pillar. As part of the Industry 4.0 transition, German equipment suppliers introduced AI-enabled closed-loop systems in 2025 that dynamically adjust droplet size using in-situ laser diffraction feedback. This capability enhances coating uniformity and yield consistency, particularly for semiconductor and catalytic applications where micron-level deviations materially affect performance. Germany’s emphasis on digitalized spray pyrolysis positions the country as a reference market for precision deposition rather than volume-driven expansion.

Comparative Snapshot: Spray Pyrolysis Industry by Country

Spray Pyrolysis Market County Level Snapshot

|

Country

|

Primary Policy Driver

|

Core Application Focus

|

Structural Advantage

|

|

China

|

Semiconductor localization

|

TFTs, TCOs, oxide catalysts

|

High-throughput industrialization

|

|

United States

|

CHIPS Act and clean energy

|

Wide-bandgap semiconductors, perovskites

|

Federal funding and private capital

|

|

India

|

Make in India and ISM

|

FTO coatings, dielectrics

|

Indigenous equipment development

|

|

Japan

|

Green Growth Strategy

|

High-efficiency photovoltaics

|

Precision control and analytics

|

|

Germany

|

Hydrogen strategy and Industry 4.0

|

Catalysts, digital deposition

|

AI-driven process optimization

|

Spray Pyrolysis Market Report Scope

Spray Pyrolysis Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$226.6 Million

|

|

Market Size (2034)

|

$420.1 Million

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Device Type (Ultrasonic Spray Pyrolysis Systems, Flame Spray Pyrolysis Systems, Electrostatic Spray Pyrolysis Systems, Industrial-Scale Spray Pyrolysis Systems, Vacuum Spray Pyrolysis Systems), By Material Category (Metal Oxides, Ceramics and Composites, Polymer-Based Thin Films, Chalcogenides and Perovskites, Carbon-Based Nanostructures), By Application (Electronics and Semiconductors, Energy Storage and Power, Healthcare and Pharmaceuticals, Industrial Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sono-Tek Corporation, Bühler AG, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Holmarc Opto-Mechatronics Ltd., Siansonic Technology Co., Ltd., MTI Corporation, Hielscher Ultrasonics GmbH, Navson Technologies Pvt. Ltd., Cheersonic Ultrasonic Equipment Co., Ltd., Nordson Corporation, Zhengzhou CY Scientific Instrument Co., Ltd., Acmefil Engineering Systems Pvt. Ltd., Frontier Laboratories Ltd., Sonaer Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Spray Pyrolysis Market Segmentation

By Device Type

- Ultrasonic Spray Pyrolysis Systems

- Flame Spray Pyrolysis Systems

- Electrostatic Spray Pyrolysis Systems

- Industrial-Scale Spray Pyrolysis Systems

- Vacuum Spray Pyrolysis Systems

By Material Category

- Metal Oxides

- Ceramics and Composites

- Polymer-Based Thin Films

- Chalcogenides and Perovskites

- Carbon-Based Nanostructures

By Application

- Electronics and Semiconductors

- Energy Storage and Power

- Healthcare and Pharmaceuticals

- Industrial Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Spray Pyrolysis Industry

- Sono-Tek Corporation

- Bühler AG

- Wacker Chemie AG

- Shin-Etsu Chemical Co., Ltd.

- Holmarc Opto-Mechatronics Ltd.

- Siansonic Technology Co., Ltd.

- MTI Corporation

- Hielscher Ultrasonics GmbH

- Navson Technologies Pvt. Ltd.

- Cheersonic Ultrasonic Equipment Co., Ltd.

- Nordson Corporation

- Zhengzhou CY Scientific Instrument Co., Ltd.

- Acmefil Engineering Systems Pvt. Ltd.

- Frontier Laboratories Ltd.

- Sonaer Inc.

*- List not Exhaustive