Market Overview: Advanced Non-Wetting Surface Engineering Driving High-Growth Adoption Across Marine, Aerospace & Electronics

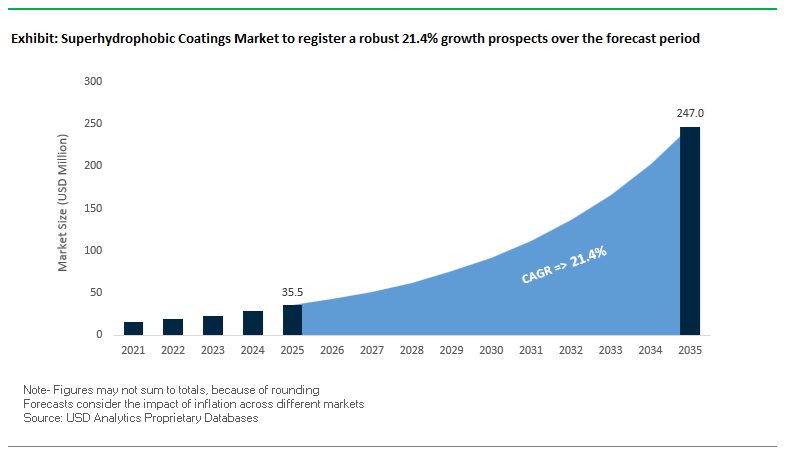

The Superhydrophobic Coatings Market is set to expand from USD 35.5 million in 2025 to USD 246.8 million by 2035, advancing at a powerful CAGR of 21.4% (2025–2035). The accelerated shift toward ultra-durable, low-surface-energy coatings in marine equipment, automotive components, aerospace transparencies, and electronic protection systems is providing strong momentum to manufacturers and vendors. Market growth is fueled by rapid advancements in contact angle optimization, nanoparticle morphology control, abrasion-resistant film design, and fluorine-free hydrophobic chemistries. Commercial players are now engineering surfaces that maintain contact angles above 150° and sliding angles below 5°, ensuring superior self-cleaning and anti-wetting functionality even after mechanical stress cycles.

Manufacturers are increasingly optimizing nanoparticle loading ratios—such as 1.5 g functionalized silica per 10 g solvent—to achieve surface roughness near 360 nm and deliver coating behaviors with contact angles exceeding 160°. Mechanical durability remains a core performance benchmark, with premium coatings now engineered to maintain >150° contact angles even after 240-grit sand abrasion at 7.75 kPa. Additionally, sectors such as aerospace require hydrophobic performance compliant with ASTM F791 and ASTM F484, maintaining >90° contact angles on sensitive polycarbonate transparencies used in cockpit visibility systems.

Key Insights for Manufacturers & Vendors

- Classification Threshold: Superhydrophobicity requires CA ≥150° and sliding angle <5° for commercial acceptance.

- Nanoparticle Optimization: Silica-based systems reach CA >160° with surface roughness ≈360 nm at optimized nanoparticle loadings.

- Durability Benchmark: Coatings must retain >150° CA after sandpaper abrasion (7.75 kPa) for automotive and marine certification.

- Aerospace Requirement: Hydrophobic finishes must comply with ASTM F791/F484, delivering >90° CA under harsh operating conditions.

- Shift to Fluorine-Free Systems: Regulations such as REACH and Prop 65 accelerate adoption of fluorine-free DWR and eco-safe nano-coatings.

Market Analysis: Capacity Expansions, Advanced Nanomaterials, and Cross-Sector Adoption Fuel High-Velocity Growth

The global Superhydrophobic Coatings Industry is undergoing accelerated innovation, driven by capacity expansion, breakthroughs in nanomaterial engineering, and increasing adoption in automotive, marine, aerospace, and wearable electronics. In Q4 2025, AkzoNobel completed a major capacity upgrade at its Suzhou facility in China, doubling its Marine and Protective Coatings output. This expansion is strategically aligned with the rising demand for anti-fouling, drag-reducing, and corrosion-resistant hydrophobic surfaces across commercial shipping fleets. In August 2025, researchers developed a graphene-based superhydrophobic coating achieving contact angles >165° with superior corrosion resistance, demonstrating the commercial viability of next-generation carbon-based nano-coatings over traditional silica-PDMS systems.

Product innovation continues to shift the competitive landscape. In March 2024, 3M introduced a fluorosilane-based polymer coating under its Novec™ electronic-grade line that delivers anti-wetting and anti-stiction properties at thicknesses below 10 nm, making it crucial for mobile electronics miniaturization. By September 2025, automakers in Europe began adopting superhydrophobic nano-coatings for LED lighting assemblies, addressing condensation issues and performance degradation in optical systems. These developments reflect the rapid convergence of hydrophobicity with automotive lighting, sensor integration, and component longevity.

The industry is also witnessing strong sustainability and defense-sector drivers. In February 2024, NeverWet entered a strategic agreement to supply fluorine-free DWR coatings to a major outdoor apparel brand, aligning with tightening global chemical regulations. In July 2025, academic testing demonstrated that superhydrophobic surfaces applied to UAV wings can reduce aerodynamic drag by up to 5% in heavy rain—gaining attention from defense agencies focused on all-weather drone reliability. Investment interest continues to rise, with Q1 2025 seeing private equity firms increasing funding for companies developing anti-icing coatings to reduce ice adhesion on wind turbine blades and transmission infrastructure. By December 2024, PPG Industries confirmed broad adoption of its HYDROSKIP® hydrophobic finish in aviation fleets, improving pilot visibility and reducing rain-induced distractions in civilian and military aircraft.

Breakthroughs in Abrasion Durability, Antimicrobial Surface Engineering, Low-Temperature Textile Coatings, and Condensation Heat Transfer Optimization

Market Trend 1: Transition Toward Abrasion-Resistant Superhydrophobic Coatings Capable of Maintaining Extreme Wetting States Under High Erosion Loads

A defining transformation across the Superhydrophobic Coatings Market is the move from laboratory-scale hydrophobic films to highly durable, erosion-resistant coatings engineered for extreme industrial conditions. Superhydrophobicity is technically defined by a Water Contact Angle (WCA) greater than 150° and a Water Sliding Angle (WSA) below 10°, metrics that must remain intact despite abrasion, particle impact, or hydrodynamic stress. This performance requirement is particularly acute in wind turbine blade protection, where blade tip velocities frequently exceed 80 m/s, exposing surfaces to intense rain droplet and airborne particulate erosion that can reduce aerodynamic efficiency by up to 20% if unprotected.

The market is therefore shifting toward advanced nanocomposite, fluoropolymer, and hierarchical microstructure coatings engineered to survive standardized durability tests such as ASTM D1044 abrasion cycles. Next-generation superhydrophobic formulations now target the ability to maintain WCA >150° even after 200 abrasion cycles, preserving the Cassie–Baxter air-retaining wetting regime required for self-cleaning and drag-reduction applications. This durability renaissance is directly influencing adoption across aerospace, maritime, automotive, and renewable energy sectors where resistance to long-term mechanical wear is now a prerequisite for qualification.

Market Trend 2: Integration of Antiviral and Antimicrobial Agents to Create Self-Sanitizing Superhydrophobic Surfaces for Healthcare, Consumer Goods, and Public Infrastructure

The second major trend shaping the Superhydrophobic Coatings Market is the fusion of superhydrophobic surface architecture with antiviral and antimicrobial functionalities, driven by post-pandemic priorities in healthcare, transportation, and shared public environments. Coatings incorporating Silver (Ag) or Copper Oxide (CuO) nanoparticles have demonstrated outstanding bactericidal performance, with CuO-based systems achieving an R value greater than 6, corresponding to >99.9999% bacterial reduction for pathogens like E. coli and S. aureus. When benchmarked against standard disinfectants, the superiority becomes evident—Ag nanoparticles at 100 mg/L reduce Streptococcus mutans survival to 2%, compared to 60% with chlorhexidine.

Equally important is stability under photocatalytic conditions. Many multifunctional coatings incorporate TiO₂ nanoparticles to enable self-cleaning and photocatalytic antimicrobial action, yet uncontrolled photocatalysis can degrade the polymer binder and collapse superhydrophobicity. Advanced formulations now maintain long-term WCA stability by preventing the rapid decomposition of low-surface-energy components—preserving wetting properties even under prolonged UV exposure. This convergence of antimicrobial efficacy with long-term hydrophobic stability is setting new qualification standards for hospital equipment, HVAC systems, food-contact surfaces, and consumer touchpoints.

Market Opportunity 1: Scalable Low-Temperature Curing Superhydrophobic Coatings for Technical Textiles and Performance Apparel

A high-growth commercial opportunity lies in extending superhydrophobic functionality to textiles, where low-temperature curing, wash durability, and flexibility drive market viability. Industrial textile processing requires coatings that cure below 85–100°C to avoid thermal damage to heat-sensitive fibers such as nylon and polyester. PDMS-based nanocomposite systems now meet this requirement, enabling integration into standard textile finishing lines.

Durability remains a dominant performance metric. Advanced textile coatings have demonstrated stable superhydrophobicity—retaining WCA >168° after 50 household laundry cycles—highlighting their potential for reusable medical garments, military uniforms, outdoor sportswear, and protective workwear. Temperature resilience is equally critical, with next-generation formulations showing <4.1% WCA loss across −10°C to 180°C, ensuring hydrophobic performance across varied climates and industrial washing conditions. Scalable low-temperature curing chemistry positions textile-focused superhydrophobic coatings as the next major industrial expansion segment.

Market Opportunity 2: High-Efficiency Dropwise Condensation (DWC) Engineering to Transform Heat Exchanger Performance and Energy Systems

The application of superhydrophobic coatings to condensation surfaces represents one of the most technologically significant opportunities in thermal engineering. These coatings induce Dropwise Condensation (DWC) instead of Filmwise Condensation (FWC), enabling a dramatic 10× increase in overall Heat Transfer Coefficient (HTC)—a leap that directly improves power plant efficiency, desalination throughput, industrial cooling performance, and heat exchanger compactness.

The performance hinges on controlling droplet behavior. DWC systems optimize for a droplet departure size of ~1 mm, facilitating rapid shedding and continuous surface renewal. Maintaining a near-perfect non-wetted state—WCA approaching 180°—sustains DWC by preventing film formation, which otherwise suppresses heat transfer. Superhydrophobic coatings tailored for condensation environments must simultaneously maintain low surface energy, mechanical robustness, and resistance to fouling or scaling. This aligns closely with market demand for next-generation energy-efficient condensers, industrial boilers, ORC systems, and atmospheric water capture technologies.

Superhydrophobic Coatings Market Share Analysis

Market Share by Material Base: Fluoropolymer Coatings Dominate Due to Ultra-Low Surface Energy and Proven Durability

Fluoropolymer coatings maintain the largest share of the global superhydrophobic coatings market—approximately 45% in 2025—because they deliver the fundamental chemical properties required to achieve extreme water repellency while offering unmatched environmental durability. Their intrinsically ultra-low surface energy, derived from strong carbon–fluorine (C–F) bonds, enables water contact angles exceeding 150°, making them the benchmark material for long-standing superhydrophobic performance. This chemistry not only drives superior hydrophobicity but also provides exceptional chemical inertness, UV resistance, and thermal stability, making fluoropolymers indispensable for high-performance applications exposed to harsh outdoor conditions. Industries such as automotive, aerospace, and marine rely heavily on these coatings for anti-corrosion protection, chemical shielding, and surface longevity—requirements that silica- and polymer-based alternatives often cannot match in demanding environments. Although regulatory scrutiny surrounding PFAS is accelerating the growth of alternative material classes, the entrenched use of fluoropolymer chemistries in critical infrastructure, high-value industrial surfaces, and premium protective systems ensures they continue to command the leading revenue share within the superhydrophobic coatings market. Their broad compatibility with metals, glass, composites, and plastics further strengthens their leadership by enabling cross-sector adoption and scalable deployment in both OEM and aftermarket applications.

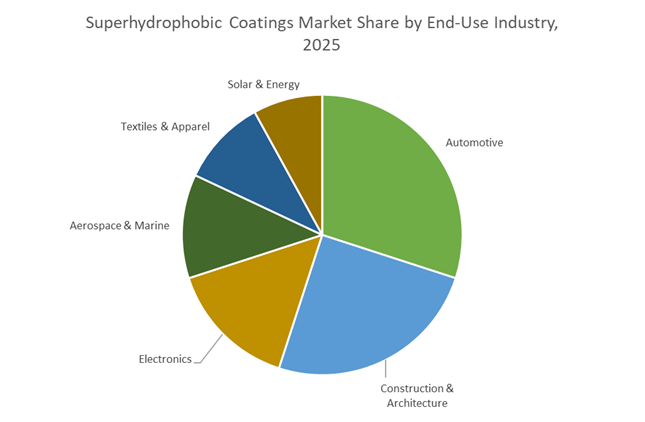

Market Share by End-Use Industry: Automotive Sector Leads Through High-Volume Adoption and Safety-Critical Applications

The automotive industry, accounting for roughly 30% of global demand, remains the largest end-user of superhydrophobic coatings due to the sector’s strong emphasis on safety, aesthetics, and lifetime component durability. Superhydrophobic coatings provide significant functional advantages across exterior and sensor-exposed vehicle surfaces by enabling instant water repellency on windshields, mirrors, lidar housings, and camera lenses, ensuring uninterrupted visibility and improving the performance of ADAS (Advanced Driver-Assistance Systems). As vehicles become increasingly sensor-driven—particularly with semi-autonomous and electric vehicle (EV) platforms—the need for anti-fogging, anti-contamination, and moisture-resistant coatings is expanding rapidly. In addition to safety, automakers leverage these coatings to enhance long-term aesthetic durability, reducing paint fading, corrosion, and micro-abrasion caused by UV radiation, road salts, and particulate matter, which directly helps lower warranty-related costs. Within EVs, the adoption curve is even steeper: superhydrophobic coatings are applied to battery systems, power electronics, and thermal management components to shield them from moisture ingress and environmental degradation, improving reliability and extending component life. High global vehicle production volumes, combined with the premium aftermarket segment’s rapid growth, reinforce the automotive industry's position as the top revenue-generating application segment in the superhydrophobic coatings market.

Country Analysis: Global Superhydrophobic Coatings Hotspots and Regional Technology Leadership

United States: Aerospace-Grade Superhydrophobic Coatings, Anti-Icing Nanotechnology, and Defense-Driven Innovation

The United States continues to dominate high-performance superhydrophobic coatings innovation, particularly for aerospace, defense, and industrial energy applications. In 2024, major U.S. aerospace and defense contractors accelerated testing of graphene-based superhydrophobic anti-icing coatings for aircraft wings and rotorcraft, a critical advancement given the material’s extremely low surface energy and resilience under high wind shear. These coatings are designed to prevent ice nucleation in flight, potentially reducing energy-intensive de-icing cycles and improving mission readiness for military aircraft. At the commercial level, NEI Corporation’s NANOMYTE® SuperCN launch demonstrated the increasing market shift toward abrasion-resistant, industrial-grade hydrophobic coatings, offering a water contact angle above 105° and surviving 500+ ASTM D1044 abrasion cycles, a benchmark for long-term durability on metals and plastics.

Leading players like 3M are intensifying R&D around fluoropolymer and PDMS-based systems to create anti-soiling, anti-oil, and chemical-resistant superhydrophobic films for electronics, industrial assets, and protective equipment. Meanwhile, the U.S. Department of Energy (DOE) is driving strong demand through initiatives that support coatings improving solar panel efficiency by reducing dust accumulation and reflection losses—pushing manufacturers to adopt nanostructured hydrophobic layers capable of maintaining maximum photovoltaic output. These developments collectively reinforce the U.S. as a powerhouse in aerospace-grade nanocoatings, military-grade anti-fouling surfaces, and next-generation clean energy materials.

Germany/European Union: Low-VOC Superhydrophobic Coatings and Automotive Nanocoating Innovation Under EU Green Deal Pressure

Germany and the broader European Union stand at the forefront of sustainable, low-VOC superhydrophobic coating technologies, driven by stringent REACH compliance and the environmental priorities of the EU Green Deal. European material science companies increasingly prioritize bio-based hydrophobic coatings with ultra-low fluorine content, addressing regulatory pressure and OEM requirements for greener surface protection systems. At Automechanika Frankfurt 2024, several German suppliers showcased next-generation automotive nano coatings engineered with self-healing capabilities, hydrophobic top layers, and aerodynamic efficiency enhancements—features critical for EVs, where surface cleanliness reduces drag and improves energy consumption.

In April 2025, BASF SE confirmed a major strategic shift toward advanced specialty surface solutions, including anti-graffiti coatings, self-cleaning façade materials, and long-life hydrophobic surface treatments for mobility and construction sectors. These innovations are complemented by rapidly expanding R&D in smart architectural coatings, where European firms experiment with nanoparticle-enhanced hydrophobic films for building exteriors and EV charging infrastructure. Altogether, the EU’s material ecosystem is becoming a global benchmark for environmentally compliant, automotive-grade, and construction-ready superhydrophobic coatings.

China: Industrial-Scale Superhydrophobic Coating Production for Anti-Corrosion and Infrastructure Durability

China’s rapid industrialization continues to drive explosive growth in superhydrophobic coating production, particularly for large-scale anti-corrosion applications across infrastructure, marine, and heavy manufacturing environments. Chinese companies are expanding their production capacity to meet surging domestic demand for corrosion-resistant coatings applied to bridges, steel beams, industrial machinery, and chemical processing equipment operating in high-humidity and chemically aggressive environments.

Academic research in China is also advancing at a remarkable pace. In December 2025, scientists announced a breakthrough superhydrophobic zirconia (ZrO₂) coating for metallic glass substrates, which integrates corrosion protection, mechanical durability, and surface repellency into a single material. Innovations like these support China’s push to commercialize superhydrophobic coatings for complex industrial components where long-term material degradation is a critical engineering challenge. China’s scale, combined with aggressive investment in materials science, is cementing its role as a central global hub for industrial-grade, cost-optimized superhydrophobic coating systems.

Japan: Photocatalytic TiO₂-Based Smart Coatings and Advanced Sol-Gel Hydrophobic Technologies

Japan holds a unique leadership position in photocatalytic and sol-gel-based superhydrophobic coatings, particularly for the construction, consumer electronics, and industrial components sectors. Japanese firms excel in integrating Titanium Dioxide (TiO₂) into glass, concrete, and façade materials, leveraging photocatalysis to decompose organic contaminants. Rainwater or light motion easily removes the degraded residue, creating a self-cleaning effect that improves the longevity and clarity of architectural glass and high-rise building exteriors. While the mechanism is partially superhydrophilic, Japanese researchers have perfected hybrid TiO₂ systems that exhibit both photocatalytic cleaning and hydrophobic water-shedding effects depending on environmental exposure.

Japan’s material manufacturers also continue to advance sol-gel processing for hydrophobic coatings on high-temperature ceramics and precision-engineered components used in automotive and industrial machinery. These coatings must withstand extreme thermal cycling and mechanical wear, making Japan’s sol-gel innovations essential for global supply chains requiring premium-grade, long-life superhydrophobic materials.

Malaysia/Southeast Asia: Expanding Regional Manufacturing Hub for Anti-Stick and Hydrophobic Coating Systems

Southeast Asia—driven by Malaysia’s rapidly expanding coatings industry—is becoming an influential regional hub for superhydrophobic coating manufacturing. PPG Industries’ major Malaysia plant expansion (August 2024) specifically boosted production capacity for anti-stick, low-friction coatings used in transportation, industrial machinery, and infrastructure sectors. This expansion is expected to spill over into advanced hydrophobic and easy-clean paints widely used across Southeast Asia’s fast-growing construction markets.

Strong regional investment in public transport systems, airports, marine infrastructure, and high-rise urban development is fueling adoption of hydrophobic architectural coatings with moisture resistance, reduced maintenance requirements, and pollution-repellent properties. The region’s low-cost manufacturing environment, combined with expanding logistics and export capabilities, positions Southeast Asia as a rising global participant in durable, industrial-use superhydrophobic coatings.

India: Rising Adoption of Anti-Fouling and Anti-Corrosion Hydrophobic Coatings for Infrastructure and Steel Protection

India is rapidly increasing its focus on superhydrophobic coatings as part of its national strategy to reinforce infrastructure durability, reduce corrosion-related losses, and enhance the longevity of steel structures. Government-backed infrastructure megaprojects—bridges, railway systems, coastal ports, and public transportation hubs—are driving demand for anti-fouling and corrosion-resistant coatings, particularly in humid, saline, and industrial pollution-heavy regions.

Indian manufacturers and public-sector agencies are increasingly evaluating polymer-based hydrophobic coatings, hybrid sol-gel systems, and nanoengineered surface treatments to extend maintenance cycles and reduce operational downtime across critical infrastructure. This trend is amplified by India’s broader push to localize material production and incorporate nanotechnology-driven protective layers for structural steel, pipelines, and energy installations. As India continues to expand its industrial and transportation footprint, superhydrophobic coatings are emerging as a strategic necessity for long-term asset protection and national infrastructure resilience.

Competitive Landscape: Leadership in Marine, Aerospace, Electronics & Nano-Coatings Defines Market Strength

The Superhydrophobic Coatings Market features a diversified competitive environment with leading players specializing in marine anti-fouling systems, aerospace optical coatings, ultrathin electronics coatings, textile water repellents, and nano-scale hydrophobic treatments. Competitiveness is shaped by material durability, functional nanostructure design, regulatory compliance, substrate compatibility, and integration with high-performance industrial processes. Many companies are strategically shifting toward fluorine-free and abrasion-resistant hydrophobic systems, improving sustainability while maintaining high performance.

AkzoNobel N.V.: Marine & Protective Coatings Leadership

AkzoNobel leads globally in marine and protective coatings, including anti-fouling and fouling-release solutions engineered for extreme saltwater environments. The company is integrating superhydrophobic principles to enhance drag reduction, fuel efficiency, and corrosion resistance on vessels and offshore structures. Its ongoing investment of €18+ million in global powder coatings expansion strengthens its capability to deliver large-volume, functionalized coatings for infrastructure, shipbuilding, and industrial assets. AkzoNobel’s scale and technical expertise position it as a primary driver of hydrophobic innovation in the shipping and heavy industrial sectors.

PPG Industries: Aerospace-Grade Hydrophobic Coating Specialist

PPG Industries dominates the aerospace hydrophobic coatings segment with its HYDROSKIP® finish, designed for aircraft transparencies and cockpit windows. Its coatings exhibit outstanding optical clarity, weatherability, and compatibility with polycarbonate substrates. PPG’s emphasis on corrosion-resistant protective coatings aligns with its strategy to reduce moisture exposure across oil & gas, infrastructure, and transportation markets. Its deep portfolio of industrial coatings demonstrates strong capability to integrate hydrophobic technologies into multi-functional protective systems.

3M Company: Ultra-Thin Hydrophobic Films for Precision Electronics

3M’s strength lies in precision-engineered electronic-grade hydrophobic coatings, particularly the Novec™ series, which delivers anti-wetting protection at thicknesses below 10 nm. These ultra-thin films provide anti-smudge, anti-stiction, and moisture resistance critical for smartphones, cameras, wearable devices, and semiconductor components. 3M also supplies high-durability elastomeric coatings for aerospace, capable of resisting hydraulic oils, fuel exposure, and abrasion, making the company a key innovator in protective and electronic surface technologies.

NeverWet (RPM International): Consumer & Industrial Fluorine-Free Superhydrophobic Coatings

NeverWet is a pioneer in consumer-grade and industrial superhydrophobic products, offering two-part coatings that create highly water-repellent surfaces for wood, metal, concrete, and textiles. The company’s strategic pivot toward fluorine-free DWR formulations addresses strict global regulations, enabling apparel and textile manufacturers to achieve high-performance water repellency without PFAS chemicals. Its agility in customizing solutions for OEMs accelerates deployment across retail, automotive, and outdoor products markets.

Aculon, Inc.: Nano-Scale Hydrophobic Coatings for Electronics

Aculon specializes in self-assembled monolayer (SAM) hydrophobic coatings under 4 nm thick, offering exceptional repellency for PCBs, semiconductors, sensors, and wearables. Its NanoProof™ series is widely adopted in high-volume electronics to prevent moisture ingress and enhance device longevity. Aculon’s focus on dip and spray process integration allows manufacturers to seamlessly incorporate hydrophobic protection into existing electronics production workflows, making it a preferred partner in next-gen device engineering.

Superhydrophobic Coatings Market Report Scope

Superhydrophobic Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$35.5 Million

|

|

Market Size (2035)

|

$246.8 Million

|

|

Market Growth Rate

|

21.4%

|

|

Segments

|

By Material Base (Fluoropolymer Coatings, Silica/SiO₂ Coatings, Graphene/CNT-Based Coatings, Polymer-Based Coatings), By Preparation Method (Two-Step, One-Step, Aerosol Spray, Sol-Gel/Dip/Spin Coating), By End-Use Industry (Automotive, Construction & Architecture, Aerospace & Marine, Electronics, Textiles & Apparel, Solar & Energy)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M, PPG, BASF, AkzoNobel, Sherwin-Williams, Nippon Paint, NEI Corporation, Axalta, Kansai Paint, Aculon, DryWired, Nanex, NTT Advanced Technology, RPM International, Hempel

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Superhydrophobic Coatings Market Segmentation

By Material Base

- Fluoropolymer Coatings

- Silica / SiO₂ Coatings

- Graphene / CNT-Based Coatings

- Polymer-Based Coatings

By Preparation Method

- Two-Step

- One-Step

- Aerosol Spray

- Sol-Gel / Dip / Spin Coating

By End-Use Industry

- Automotive

- Construction & Architecture

- Aerospace & Marine

- Electronics

- Textiles & Apparel

- Solar & Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Superhydrophobic Coatings Market

- 3M

- PPG

- BASF

- AkzoNobel

- Sherwin-Williams

- Nippon Paint

- NEI Corporation

- Axalta

- Kansai Paint

- Aculon

- DryWired

- Nanex

- NTT Advanced Technology

- RPM International

- Hempel.

*- List not Exhaustive