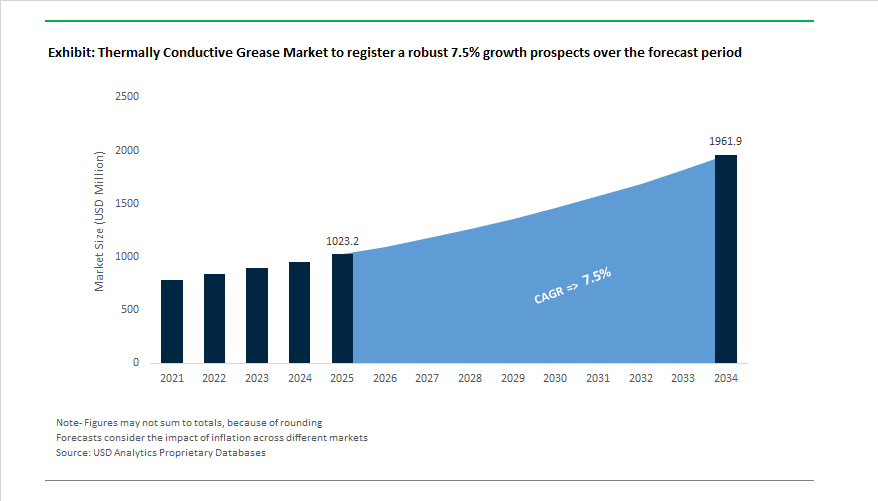

The Global Thermally Conductive Grease Market is expected to expand from USD 1,023.2 million in 2025 to USD 1,961.7 million by 2034, advancing at a CAGR of 7.5%, as thermal management shifts from a component-level consideration to a system-level design limiter across electronics, electrified mobility, and digital infrastructure. The market’s momentum is not driven by volume growth alone, but by the escalating thermal loads created by higher chip power densities, tighter component spacing, and longer duty cycles in next-generation devices.

Thermally conductive greases are increasingly specified as performance-critical thermal interface materials (TIMs) rather than commodity fillers. Semiconductor manufacturers, power electronics OEMs, and EV platform designers are pushing interface materials to deliver stable thermal conductivity in the 3–10 W/m·K range, low thermal resistance under thin bond lines, and long-term pump-out resistance under vibration and thermal cycling. This is particularly evident in IGBT modules, SiC/GaN power devices, onboard chargers, and high-performance CPUs/GPUs, where even marginal increases in junction temperature directly translate into reduced efficiency, derating, or shortened service life.

From a materials standpoint, manufacturers are refining silicone-based and hybrid grease systems with engineered ceramic fillers such as aluminum oxide, aluminum nitride, and boron nitride to balance conductivity, electrical insulation, and rheological stability. Leading suppliers have also focused on controlled viscosity profiles and low-bleed formulations, addressing long-standing reliability challenges such as oil separation, migration, and dry-out in vertical or high-vibration assemblies. In EV and rail traction applications, where components are exposed to repeated −40°C to +150°C thermal cycling, grease stability over multi-year lifetimes has become a decisive qualification criterion.

At the manufacturing and operations level, thermally conductive greases are favored for their reworkability, low contact pressure requirements, and compatibility with automated dispensing, particularly in high-mix electronics and battery module assembly. As data centers and hyperscale operators push higher rack power densities, and EV platforms consolidate power electronics into fewer, hotter modules, the role of thermal greases is expanding from traditional CPU cooling into powertrain, inverter, and energy storage architectures.

The thermally conductive grease industry is witnessing major transitions driven by innovation, regulation, and corporate restructuring. A consistent theme across developments was the migration from traditional silicone-based systems to non-silicone and hybrid nanomaterial formulations, alongside the rise of structural thermal adhesives for e-mobility and semiconductor applications.

In October 2025, Wacker Chemie AG presented its next-generation thermally conductive adhesives (TCA) for EV architectures at The Battery Show, marking a significant industry pivot from conventional greases to structural, easy-handling TIM solutions optimized for cell-to-pack (CTP) and cell-to-chassis (CTC) battery designs. Similarly, in September 2025, Master Bond launched EP53TC, a new two-component epoxy with enhanced heat dissipation and low viscosity, meeting the needs of structural bonding applications in electronics and aerospace.

The year also marked pivotal corporate changes: DuPont announced in July 2025 its plan to spin off its Electronics business by November 2025, sharpening its focus on semiconductor and interconnect technologies—areas where thermal greases and TIMs are indispensable. In May 2025, Dow launched an automotive-optimized grade of DOWSIL™ TC-5351, a non-curing compound (3.3 W/m·K) tailored for Electronic Control Units (ECUs), emphasizing vertical gap-fill capability and processability for automation lines.

Meanwhile, Laird Performance Materials (part of DuPont/Rogers) introduced a new grease line in February 2025 offering anti-pump-out stability for datacom and server environments, tackling one of the industry’s toughest reliability challenges. Shin-Etsu Chemical, in November 2024, unveiled a plan to expand production capacity for high-function silicone products, citing surging APAC electronics demand. Henkel, in October 2024, launched non-curing thermal greases with 0.02 K·cm²/W resistance, designed for AI accelerators and data center processors, while the EU regulatory framework (September 2024) tightened restrictions on low-molecular-weight siloxanes (D4–D6), accelerating the market shift to low-volatile and silicone-free greases.

Market Trend 1: Shift Towards High-Performance, Low-Bleed Formulations for Automotive Power Electronics

As electric vehicles (EVs) and hybrid systems evolve toward higher power density and faster charging, the demand for thermally conductive greases with exceptional thermal stability, low oil separation, and high conductivity retention has become critical. Traditional silicone-based greases are increasingly being replaced by synthetic formulations capable of maintaining viscosity, performance, and adhesion under prolonged high-temperature conditions.

A recent NREL (National Renewable Energy Laboratory) study on automotive power electronics thermal management reported that thermal resistance within the TIM layer can cause a temperature jump of up to 23°C in Insulated Gate Bipolar Transistor (IGBT) modules. However, advanced high-performance greases capable of reducing TIM thermal resistance by fivefold can bring the temperature rise down to roughly 7°C, directly enhancing power cycling endurance and component lifespan.

The need is amplified in fast-charging EV platforms, where research indicates that rapid charging accelerates thermal degradation—leading to 1.5–2× faster capacity loss in batteries compared to slow-charging cycles. In such systems, ultra-reliable, low-bleed thermal greases prevent performance drift and mechanical breakdown in inverters and onboard chargers exposed to sustained thermal stress.

A major performance enabler in the trend is the use of synthetic base oils such as Polyalphaolefin (PAO) and synthetic esters, which outperform mineral oils in oxidative and thermal stability. These synthetics maintain structural integrity up to 280–320°C, making them indispensable for high-heat flux automotive environments. As a result, automotive OEMs and Tier-1 suppliers are increasingly specifying synthetic-based thermal greases for long-life, maintenance-free EV electronics applications.

Market Trend 2: Proliferation of Non-Silicone, Ceramic-Filled Greases for Sensitive Electronics and Optical Devices

The global electronics sector is witnessing a steady shift toward non-silicone, ceramic-filled thermal greases to eliminate the risk of contamination and ensure long-term performance in high-precision, sensitive environments such as sensors, optics, RF modules, and LED assemblies. Silicone migration—commonly known as “oil blooming”—has been a major reliability concern, as siloxane molecules can migrate and degrade optical clarity, insulation resistance, and solder adhesion.

To address the, manufacturers are developing non-silicone greases based on hydrocarbon and polyalphaolefin matrices, loaded with high-thermal-conductivity ceramic fillers such as aluminum oxide, boron nitride, and aluminum nitride. These formulations achieve thermal conductivities between 1.3 and 6.0 W/m·K, with zero outgassing and minimal material bleed.

Modern ceramic-filled non-silicone TIMs are engineered for extreme stability—resisting hardening, melting, or oil separation even at continuous exposure to 250°C. Such reliability ensures consistent performance across multiple thermal cycles, making these greases ideal for CPUs, GPUs, laser diodes, LEDs, and optical modules.

The transition reflects a broader movement in thermal management toward contamination-free, long-life greases that combine mechanical resilience, electrical insulation, and chemical inertness, particularly for semiconductor packaging and high-frequency communication systems.

Market Opportunity 1: Development of Phase-Change Thermal Greases for Power-Dense, Cyclic Applications

The rise of AI accelerators, 5G infrastructure, and data center processors has redefined the operational profile of modern electronics. These systems operate in high-thermal-flux, cyclic environments, where traditional greases often suffer from “pump-out”—the tendency to migrate under temperature fluctuations, leaving air gaps that degrade heat transfer.

The challenge has paved the way for phase-change thermal greases (PCTGs)—engineered formulations that shift from solid to paste-like consistency within a defined temperature range (typically 45–80°C). At operational temperatures, the grease softens and flows to fill microscopic voids, achieving minimal bond line thickness (BLT) and exceptional interfacial contact. When cooled, it resolidifies to prevent further migration, providing long-term mechanical and thermal stability.

In March 2024, a leading global materials supplier introduced a reworkable phase-change material optimized for telecom base stations and data center server blades, designed to eliminate pump-out and withstand repetitive power cycling. Such greases address the increasing heat flux density of compact, high-wattage devices, marking a major advancement in thermally conductive interface design.

As high-performance computing moves toward heterogeneous integration (chiplets and 3D packages), the demand for phase-change thermal materials with reworkable and low-volatile properties will accelerate, bridging the gap between traditional greases and solid gap fillers.

Market Opportunity 2: Engineering of Electrically Insulative yet Thermally Conductive Greases for Wide-Bandgap Semiconductors

The transition to Wide-Bandgap (WBG) semiconductors such as Silicon Carbide (SiC) and Gallium Nitride (GaN) is revolutionizing power electronics, but also presenting new thermal management challenges. These materials operate at higher junction temperatures (>175°C) and higher critical electric fields (up to 3×10⁶ V/cm) compared to conventional silicon, necessitating dielectric-strength-optimized thermal greases that offer both high conductivity and electrical insulation.

In SiC and GaN devices, self-heating effects (SHE) significantly impact performance and longevity. For instance, GaN-based HEMTs can experience severe temperature rises due to localized heat buildup, leading to carrier mobility degradation and early device failure. To mitigate the, thermally conductive greases incorporating electrically insulating ceramics (e.g., aluminum nitride or boron nitride) are being developed to achieve thermal conductivities up to 5 W/m·K while maintaining dielectric breakdown strengths suitable for high-voltage environments.

Such greases are increasingly critical in EV powertrains, renewable energy converters, and high-frequency telecom modules, where both thermal dissipation and electrical isolation are mission-critical. As SiC/GaN device adoption expands in 5G base stations, solar inverters, and EV traction systems, these dual-function thermal greases represent a high-value segment with strong long-term growth potential.

Thermally Conductive Grease Market Share Insights, 2025-2034

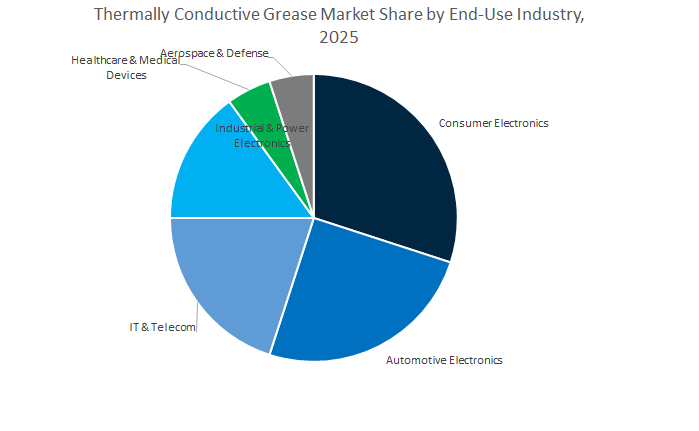

Market Share by End-Use Industry

The consumer electronics segment holds the largest share of the global thermally conductive grease market, commanding approximately 31.4% of total demand in 2025. This dominance is primarily driven by the exponential production of smartphones, laptops, tablets, gaming consoles, and wearables, all of which demand compact, high-performance thermal interface materials (TIMs) to dissipate heat from microprocessors and chipsets. As electronic components continue to miniaturize and power densities rise, thermally conductive greases have become indispensable for efficient heat transfer and maintaining device reliability. The automotive electronics sector represents the fastest-growing segment, fueled by the electrification of vehicles, rapid deployment of ADAS (Advanced Driver Assistance Systems), and the increasing complexity of onboard electronic control units. The transition to electric vehicles (EVs) amplifies the need for advanced thermal management in batteries, inverters, and power control modules, where silicone and metal oxide-based greases ensure consistent thermal conductivity and long-term stability. Meanwhile, the IT & telecom industry maintains a strong share, driven by the expansion of data centers, cloud infrastructure, and 5G networks that demand efficient thermal control in servers, transceivers, and base stations. Industrial and power electronics utilize these materials in automation systems, motor drives, and power modules, emphasizing durability under continuous operation. Niche but critical segments such as healthcare and aerospace depend on thermally conductive greases for medical imaging equipment, satellite electronics, and defense-grade systems, where reliability under extreme conditions is non-negotiable.

Market Share by Form/Packaging

In terms of form and packaging, syringe and cartridge-dispensed thermally conductive greases dominate the global market, accounting for 63.6% of total share in 2025. This format remains the industry standard due to its ease of handling, precision dispensing, and adaptability across consumer, automotive, and industrial manufacturing environments. Syringe-based systems allow for accurate dosing, reduced material wastage, and simplified application in both manual assembly lines and maintenance operations, making them highly preferred for electronics repair centers and prototyping environments. Furthermore, cartridge systems enable semi-automated processes in mid-scale assembly operations, supporting consistent performance without the need for advanced dispensing infrastructure. However, automated dispense systems are rapidly gaining traction, driven by the increasing adoption of high-throughput manufacturing and robotics in electronics and automotive sectors. These systems deliver unmatched precision, uniform layer thickness, and repeatability, essential for mass production of semiconductors, printed circuit boards (PCBs), and electric vehicle battery packs. Manufacturers are transitioning toward closed-loop automated dispensing platforms to reduce contamination risk and improve thermal contact efficiency, particularly in high-reliability industries such as data centers, EV manufacturing, and medical equipment.

The competitive ecosystem of the Thermally Conductive Grease Market is characterized by chemistry-driven innovation, application-specific engineering, and regional manufacturing expansion. Major players such as DuPont, Dow, Henkel, Wacker, Shin-Etsu, and Laird Performance Materials are driving market leadership by balancing thermal efficiency, reliability, and environmental compliance. Each company’s strategic roadmap reveals a unique approach to addressing the thermal management needs of next-generation electronics, EVs, and energy systems.

Laird Performance Materials, integrated into DuPont/Rogers, leads in high-reliability thermal interface solutions with its Tgrease™ series, including both silicone-based and silicone-free greases like Tgrease™ 2500 (3.8 W/m·K). The company’s formulations are optimized for optical and sensor systems where silicone migration cannot be tolerated. Laird’s expertise in pump-out resistance, dispensing compatibility, and screen-printable TIMs positions it as a trusted supplier for datacom, telecom, and consumer electronics manufacturers seeking process-stable materials.

Dow continues to dominate with its DOWSIL™ line, offering non-curing thermal compounds with exceptional dielectric strength (≥8 kV/mm) and thermal stability. Its TC-5351 and TC-5860 grades serve high-reliability markets such as EV power modules, inverters, and renewable energy systems, ensuring consistent heat management under high loads. Dow’s commitment to formulation optimization, combined with its deep silicone chemistry expertise, solidifies its role as a leading supplier for next-generation automotive and energy electronics.

DuPont, through its Bergquist brand, offers one of the most comprehensive TIM portfolios globally, including Gap Pad® TGP and thermal grease lines known for ease of automation and repeatable thermal performance. The upcoming spin-off of its Electronics division (targeted for November 2025) underscores DuPont’s strategy to focus on semiconductor and high-performance computing segments, where demand for high-efficiency thermal greases is surging. The company’s integration of Bergquist TIM technology within its Electronics & Industrial division strengthens its vertical presence across critical growth sectors.

Shin-Etsu Chemical is a global powerhouse in silicone-based thermal greases, including the G-Series and CLG-Series, renowned for thermal oxidation stability and long-term performance in automotive power modules and LEDs. With its tripartite model—spanning sales, development, and production—it ensures flexibility and high customization. The 2024 capacity expansion announcement aims to support the rising electronics manufacturing base in Asia-Pacific, reinforcing its status as a dependable supplier for high-volume, high-precision thermal materials.

Wacker Chemie AG offers SEMICOSIL® Paste 40 TC (4.0 W/m·K) and ELASTOSIL®-based adhesives, combining non-curing thermal grease performance with structural bonding capabilities. Its showcase at The Battery Show (October 2025) emphasized hybrid silicone formulations (STP-E technology) that deliver high thermal conductivity with mechanical integrity—essential for cell-to-pack battery architectures. Wacker’s expanding E-Mobility portfolio highlights its push to become a leading supplier in electric vehicle thermal management.

Henkel continues to lead with its LOCTITE® and BERGQUIST® brands, offering stencil-printable, high-throughput thermal greases that achieve ultra-low bond line thickness (BLT) and thermal resistance reductions. The company’s October 2024 product series introduced 0.02 K·cm²/W resistance formulations for AI accelerators and data center CPUs, setting a benchmark in the server cooling segment. Henkel’s strategy emphasizes automated dispensing compatibility, ESG-driven formulations, and innovation leadership across power electronics and data processing sectors.

Country Analysis: Global Thermally Conductive Grease Industry

China – Global Hub for EV and 5G Thermal Interface Material Production

China continues to dominate the global thermally conductive grease market, driven by its vast electric vehicle (EV) ecosystem, 5G infrastructure development, and massive electronics manufacturing base. With major global and domestic thermal management companies expanding capacity in China, the country has become a central node in the Asia-Pacific supply chain for thermally conductive materials. The expansion aligns with China’s New Energy Vehicle (NEV) mandate, which compels OEMs to integrate high-conductivity greases into EV battery packs, electric motors, and inverters to ensure safety, efficient heat dissipation, and improved battery longevity.

The surge in 5G base station installations and data transmission infrastructure is accelerating demand for non-silicone thermal greases and phase change materials (PCMs) that can handle high power densities. Domestic R&D centers are pioneering next-generation graphene and carbon nanotube (CNT) composite thermal greases with conductivities exceeding 10 W/mK, advancing their competitiveness in semiconductor and high-frequency device applications. Meanwhile, China’s 14th Five-Year Plan continues to strengthen local supply chain independence through the domestic production of boron nitride and aluminum oxide fillers, reducing reliance on imported materials. The strategic integration of R&D, policy support, and industrial scaling cements China’s leadership in high-performance, sustainable thermal interface materials (TIMs).

United States – Advancing Aerospace, AI Hardware, and EV Thermal Innovations

The United States thermally conductive grease industry is evolving rapidly under the twin forces of technological innovation and clean manufacturing policy. Leading U.S. material science companies are launching next-generation thermally conductive greases designed for data centers, AI servers, and GPU/CPU cooling where low thermal impedance and long-term stability are critical. Recent innovations in liquid metal and hybrid nanomaterial-based TIMs developed in U.S. university laboratories are revolutionizing thermal management for high-performance computing (HPC) systems and supercomputers.

Government incentives under the Inflation Reduction Act (IRA) and the Bipartisan Infrastructure Law are catalyzing domestic production of EV battery and charging infrastructure, creating an immediate surge in demand for thermal greases in battery pack assemblies and inverter systems. Aerospace and defense sectors continue to require mil-spec, vibration-resistant thermal greases that deliver reliable performance across wide temperature ranges. Regulatory oversight by the EPA on VOC emissions has prompted leading manufacturers to introduce ultra-low-bleed, solvent-free formulations that meet sustainability standards without compromising performance. As corporate investment in North American production facilities intensifies, the U.S. is consolidating its role as a global leader in high-reliability, environmentally compliant thermal interface materials.

Germany – Driving Automotive Electrification and Industrial Power Electronics Efficiency

Germany’s thermally conductive grease market is strongly influenced by the country’s automotive electrification initiatives and its industrial power electronics ecosystem. Major German automotive OEMs—including Volkswagen, BMW, and Mercedes-Benz—are setting strict thermal performance standards for EV battery modules and powertrain systems, requiring greases with superior dielectric strength, fire resistance, and long-term stability. Local adhesive and sealant producers are investing in bio-based thermal grease formulations under the EU’s Horizon sustainability programs, emphasizing reduced environmental impact while maintaining high conductivity.

Furthermore, Germany’s industrial automation and renewable energy sectors are key application drivers. Specialized thermal greases are increasingly used in IGBT modules, wind turbine generators, and solar inverter units, where consistent performance is required under cyclic thermal stress. The expansion of dedicated European production lines for electrically insulating yet highly conductive greases further supports domestic manufacturing independence. The trends align with the National Electromobility Program, ensuring continuous demand for advanced automotive and power electronics TIM solutions across Europe’s most technologically mature market.

Japan – Precision Engineering in Miniaturized and High-Reliability Electronics

Japan remains a global leader in precision thermal management materials, leveraging its strengths in miniaturized electronics, semiconductor packaging, and robotics. Japanese chemical companies have perfected ultra-thin bond line (BLT) thermally conductive greases with low viscosity and high flowability, ideal for smartphones, wearables, and advanced semiconductor chips. Collaborations between semiconductor foundries and material suppliers are enabling co-development of custom thermal compounds designed to complement next-generation chip architectures and package designs.

In addition, hexagonal boron nitride (h-BN) and structured filler systems are being optimized to enhance thermal conductivity in silicone-based greases without compromising application smoothness. Japan’s industrial automation and robotics sectors depend heavily on high-reliability thermal pastes that endure continuous motion and high thermal cycling. With strict Japanese Industrial Standards (JIS) ensuring product safety and performance certification, the market consistently demands premium, zero-defect materials. The culture of precision and reliability keeps Japan at the forefront of high-performance thermally conductive grease innovation.

Thermally Conductive Grease Market Report Scope

Thermally Conductive Grease Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1023.2 Million

|

|

Market Size (2034)

|

$1961.7 Million

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Base Material (Silicone-Based, Non-Silicone-Based), By Filler Material (Ceramic-Based, Carbon-Based, Metal-Based, Hybrid/Composite), By End-User (Automotive Electronics, Consumer Electronics, IT & Telecom, Industrial & Power Electronics, Healthcare & Medical Devices, Aerospace & Defense), By Form (Syringe/Cartridge, Automated Dispense

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Dow Inc., DuPont de Nemours, Inc., Parker-Hannifin Corporation, Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, 3M Company, Honeywell International Inc., Momentive Performance Materials Inc., AOS Thermal Compounds LLC, Indium Corporation, Fujipoly America Corporation, Electrolube, KULR Technology Group, Inc., H.B. Fuller Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Base Material

- Silicone-Based

- Non-Silicone-Based

By Filler Material

- Ceramic-Based

- Carbon-Based

- Metal-Based

- Hybrid/Composite

By End-Use Industry

- Automotive Electronics

- Consumer Electronics

- IT & Telecom

- Industrial & Power Electronics

- Healthcare & Medical Devices

- Aerospace & Defense

By Form/Packaging

- Syringe/Cartridge

- Automated Dispense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Thermally Conductive Grease Market-

- Henkel AG & Co. KGaA

- Dow Inc.

- DuPont de Nemours, Inc.

- Parker-Hannifin Corporation

- Shin-Etsu Chemical Co., Ltd.

- Wacker Chemie AG

- 3M Company

- Honeywell International Inc.

- Momentive Performance Materials Inc.

- AOS Thermal Compounds LLC

- Indium Corporation

- Fujipoly America Corporation

- Electrolube

- KULR Technology Group, Inc.

- H.B. Fuller Company

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how next-generation thermally conductive grease (TCG) platforms are enabling reliable heat dissipation across EV power electronics, data centers, and high-power semiconductor devices; it synthesizes breakthroughs in high-k multiphase oils, BN/ceramic hybrid fillers, silicone-free stability, anti-pump-out rheology, and phase-change behaviors into decision-grade insights for engineering and sourcing teams. Our analysis reviews performance envelopes (thermal conductivity, thermal impedance, BLT control, bleed/outgassing), qualification pathways for SiC/GaN modules, and manufacturing impacts such as automation compatibility and reworkability, and highlights the implications of evolving VOC/siloxane rules and supply security for TIM value chains. Built for R&D leaders, reliability engineers, and procurement professionals, this report is an essential resource for benchmarking TCG options versus pads and gap-fillers, optimizing stack-ups for power density, and aligning supplier selection with durability, cost, and ESG objectives, etc……

Scope Highlights

Segmentation:

- By Base Material: Silicone-Based; Non-Silicone-Based

- By Filler Material: Ceramic-Based; Carbon-Based; Metal-Based; Hybrid/Composite

- By End-Use Industry: Automotive Electronics; Consumer Electronics; IT & Telecom; Industrial & Power Electronics; Healthcare & Medical Devices; Aerospace & Defense

- By Form/Packaging: Syringe/Cartridge; Automated Dispense

- By Region: North America; Europe; Asia Pacific; South & Central America; Middle East & Africa

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies — Henkel AG & Co. KGaA; Dow Inc.; DuPont de Nemours, Inc.; Parker-Hannifin Corporation; Shin-Etsu Chemical Co., Ltd.; Wacker Chemie AG; 3M Company; Honeywell International Inc.; Momentive Performance Materials Inc.; AOS Thermal Compounds LLC; Indium Corporation; Fujipoly America Corporation; Electrolube; KULR Technology Group, Inc.; H.B. Fuller Company.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.