Transparent Barrier Packaging Films in Consumer Goods Market Size, Overview, and Growth Outlook (2025–2034)

Transparent Barrier Packaging Films in Consumer Goods Market Projected to Surge to $14.4 Billion by 2034 as Sustainability and Product Protection Drive Growth

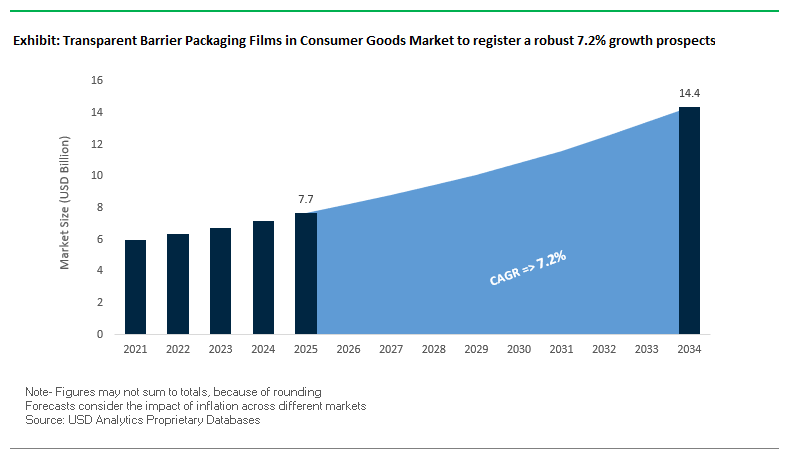

The global transparent barrier packaging films in Consumer Goods market in consumer goods is expected to grow from $7.7 billion in 2025 to $14.4 billion by 2034, at a CAGR of 7.2%. These films combine visual appeal with high-performance protection, safeguarding perishable goods from oxygen, moisture, and UV exposure while maintaining product visibility. The market’s growth is fueled by consumer demand for extended shelf life, innovative packaging solutions, and eco-friendly alternatives.

Key Insights for industry professionals and buyers:

- Shelf-life extension is a primary driver, with materials like EVOH and advanced coatings reducing gas and moisture transmission.

- Mono-material films are redefining recyclability, using PE or PP to enable circular economy alignment.

- Bio-based and compostable options derived from sugarcane bagasse and plant polymers are gaining attention due to regulatory and consumer pressures.

- Nanotechnology and smart packaging are emerging trends, integrating antimicrobial agents and freshness indicators to enhance product safety and differentiation.

- Cross-industry applications include food, beverages, personal care, and pharmaceuticals, emphasizing versatility and market opportunity.

These trends highlight significant opportunities for packaging innovators, material scientists, and sustainability-focused companies seeking to differentiate products while reducing environmental impact.

Market Analysis: Advanced Materials and Sustainability Initiatives Are Transforming Transparent Barrier Packaging Films

The transparent barrier packaging films in Consumer Goods market is witnessing rapid evolution driven by technological innovation and sustainability commitments. In August 2025, a review article highlighted the growing use of advanced additives to improve mechanical and antimicrobial performance in packaging films, demonstrating the industry’s focus on functional and sustainable solutions. Concurrently, Amcor upgraded its UK recycling facility to enhance the use of post-consumer recycled content, reflecting global investment trends in circular packaging solutions.

July 2025 saw Melodea Ltd. introduce MelOx Ngen, a bio-based, water-based coating that enables recyclability of plastic food packaging, marking a pivotal shift toward plant-sourced barrier solutions. Research also demonstrated the efficacy of carrageenan-polyoxometalate composite films, offering strong bactericidal activity and rapid biodegradability, meeting both food safety and sustainability goals.

Innovations in production and packaging efficiency continue to shape the market. In April 2025, ExxonMobil Chemical launched a fully recyclable PE-based thermoformed food barrier package, while TOPPAN Holdings and its Indian subsidiary in March 2024 initiated GL-SP production, a BOPP-based transparent barrier film designed for mono-material packaging and improved recyclability.

Trends and Opportunities in the Transparent Barrier Packaging Films Market

Shift Towards High-Performance Mono-Material Polyolefin Structures

One of the most transformative developments in the transparent barrier packaging films in Consumer Goods market is the rapid adoption of mono-material polyolefin structures. Historically, the industry faced a trade-off between recyclability and barrier performance, but innovations are now closing this gap. TOPPAN’s GL BARRIER™ films, available in both PE- and PP-based grades, demonstrate oxygen transmission rates (OTR) and water vapor transmission rates (WVTR) comparable to complex multi-material laminates, making them a viable recyclable alternative for sensitive applications.

Regulatory pressure is accelerating this transition. The EU Packaging and Packaging Waste Regulation (PPWR) mandates that all packaging must be recyclable by 2030, driving brands to adopt structures compatible with established recycling streams. Companies such as Berry Global are scaling commercialization with solutions like BPP80, a mono-material PP film that has already enabled the production of over 25 million recyclable snack pouches annually. Beyond compliance, mono-materials also deliver manufacturing efficiency, as simplified structures reduce lamination complexity, lower energy consumption, and cut the carbon footprint per unit produced. This trend demonstrates how sustainability, compliance, and cost-effectiveness are converging to reshape the packaging films sector.

Adoption of Vapor-Coated and Atomic Layer Deposited (ALD) Barriers

Another major trend is the integration of vapor-coated and ALD-based transparent barriers that provide ultra-high protection with nanoscale precision. Research on Atomic Layer Deposition (ALD) highlights the use of conformal coatings of aluminum oxide (Al₂O₃) and silicon oxide (SiO₂) on plastic substrates, achieving OTR levels below 0.1 cm³/m²/day. These films match the performance of aluminum foil while remaining transparent, lightweight, and flexible, making them highly suitable for electronics, pharmaceuticals, and premium consumer goods.

Film manufacturers are commercializing vapor-deposited solutions that maintain durability under bending, folding, and creasing—critical for supply chain resilience. Unlike traditional foil laminates, these transparent high-barrier films reduce bulk and weight, improving shipping efficiency and creating more consumer-friendly formats. By combining aesthetic transparency with high functional protection, this trend is setting new performance benchmarks in flexible packaging innovation.

Enabling the Fresh and Prepared Food E-commerce Supply Chain

The rise of e-commerce grocery and meal kit delivery has created a strong opportunity for transparent barrier packaging films that can balance visual appeal with product protection. Online grocery logistics expose perishable items like produce, dairy, and ready-to-eat meals to temperature fluctuations and extended transit times. High-barrier transparent films address this challenge by maintaining freshness, blocking oxygen and moisture, and reducing spoilage during last-mile delivery.

For consumers, transparency is equally critical. It allows visual inspection of food quality before opening, enhancing trust in online purchases and reducing returns. This is especially valuable for short shelf-life items such as salads, berries, and bakery goods, where freshness and appearance directly influence buying decisions. As demand for fresh and convenient online food solutions grows, high-barrier transparent packaging emerges as a strategic enabler of consumer confidence and brand loyalty in the e-commerce supply chain.

Development of Bio-Based and Home-Compostable Barrier Films

The second major opportunity lies in addressing end-of-life challenges by scaling bio-based and compostable barrier films. Flexible packaging, particularly multi-layer laminates, remains difficult to recycle, creating demand for sustainable alternatives that can biodegrade in home or industrial composting environments. Innovators such as TIPA are developing transparent bio-based films that provide barrier properties comparable to conventional plastics for dry and frozen foods while offering a clear pathway to circularity.

Material science is advancing with renewable feedstocks. FKuR’s Bio-Flex® resins, derived from corn and sugarcane, serve as “drop-in” solutions that run on existing film extrusion lines, enabling manufacturers to transition without heavy capital investment. These materials meet consumer demand for eco-friendly packaging while supporting regulatory targets for compostable and bio-based alternatives. For brands, integrating compostable transparent barriers provides both an environmental marketing advantage and a practical solution to reducing landfill waste from single-use flexible packaging.

Competitive Landscape: Leading Players in Transparent Barrier Packaging Films Are Driving Innovation and Sustainability

The transparent barrier packaging films industry is shaped by major players who leverage material science, manufacturing expertise, and sustainability initiatives to deliver innovative and compliant solutions across consumer goods sectors.

Amcor plc: Advancing Recyclable and PVC-Free Barrier Films for Consumer Goods

Amcor offers AmLite and AmPrima™ series, providing metal-free, high-barrier laminates and recycle-ready flexible pouches. In August 2025, the company upgraded its UK recycling facility and is developing AmSky™ thermoform blister systems, a PVC-free and aluminum-free solution. Amcor’s vertically integrated operations enable scalable, sustainable packaging solutions across regions and industries.

Berry Global Group, Inc.: Driving Circular Economy with High-Performance Transparent Films

Berry Global specializes in rigid and flexible films with a focus on lightweighting and recycled material utilization. In March 2025, the company reported 93% of FMCG packaging is recyclable or has validated alternatives, alongside a 130% increase in bioplastics purchases. Its Impact 2025 roadmap emphasizes scaling circular, net-zero economy solutions using proprietary technologies like CleanStream®.

Mondi Group: Providing EcoSolutions for Recyclable Transparent Packaging Films

Mondi offers recycle-ready flexible packaging and barrier films, emphasizing sustainability through its EcoSolutions approach. In June 2025, the company launched recyclable mono-material bags for dry pet food and developed Hug&Hold, a paper-based alternative to shrink wrap. Mondi’s strategy aligns with its 2030 sustainability targets of fully recyclable, reusable, or compostable packaging.

Sealed Air Corporation: Enhancing Product Protection with Sustainable High-Performance Films

Sealed Air provides films, bags, and protective packaging materials across food, healthcare, and industrial sectors. Its Plastic Reduction strategic plan focuses on reducing environmental footprint while expanding manufacturing capacity to meet global e-commerce and retail food demand. Sealed Air’s solutions combine high-performance protection with sustainability across multiple applications.

TOPPAN Holdings Inc.: Pioneering Transparent Barrier Films for Mono-Material Packaging

TOPPAN produces the GL BARRIER series, including GL-SP, a BOPP-based transparent barrier film designed for mono-material packaging and improved recyclability. In March 2024, the company expanded production in India and Europe, targeting food, medical, and industrial markets. TOPPAN’s vertically integrated model ensures innovative, high-quality, and compliant packaging solutions globally.

Transparent Barrier Packaging Films in Consumer Goods Market Share Insights, 2025-2034

Food & Beverages Drive Majority Share by Application in Transparent Barrier Packaging Films Industry

Food and beverages dominate the transparent barrier packaging films in Consumer Goods market with a commanding 65% share, underscoring the sector’s reliance on advanced packaging technologies to ensure extended shelf life, safety, and visual appeal. High-barrier films incorporating EVOH, metallization, or transparent oxide coatings are used extensively in applications such as coffee, snacks, cheese, fresh produce, and ready-to-eat meals, where oxygen and moisture protection directly correlate to product quality and shelf stability. The combination of consumer demand for preservative-free foods, rising global trade in perishable items, and regulatory pressure for safer packaging continues to fuel innovation in this segment. Transparent barrier films allow brand owners to balance sustainability with performance, enabling recyclability through mono-material structures while maintaining the product visibility consumers expect. This makes food and beverages the undisputed growth driver for the industry.

Stand-up Pouches Command Market Share by Packaging Format in Transparent Barrier Packaging Films Industry

Stand-up pouches account for the largest share at 40% of the transparent barrier films market, emerging as the preferred packaging format across both food and non-food sectors. Their popularity is driven by material efficiency, superior shelf presence, and consumer convenience features such as resealability and portability. Stand-up pouches combine high-barrier laminates with advanced sealing technologies to preserve freshness while reducing packaging weight compared to rigid alternatives, directly supporting sustainability goals. They are widely adopted in snacks, beverages, pet food, and even detergents, benefiting from the ongoing trend toward flexible packaging. The ability of this format to integrate mono-material structures for recyclability while still maintaining high oxygen and moisture barriers further reinforces its leadership, positioning stand-up pouches as the future-ready standard in transparent barrier packaging films.

European Union: Circular Economy Targets Driving Barrier Film Innovation

The European Union transparent barrier packaging films in Consumer Goods market is shaped by stringent sustainability regulations such as the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. This legislation mandates that all plastic packaging, including barrier films, must incorporate minimum levels of post-consumer recycled content by 2030. Alongside PPWR, the Ecodesign for Sustainable Products Regulation (ESPR) is accelerating the push for durable and refillable consumer goods packaging, prompting innovation in refill systems and reusable components.

Funding initiatives like Horizon Europe are further strengthening research into bio-based alternatives such as starch blends and cellulose films. The European Food Safety Authority (EFSA) plays a critical role by evaluating additives and ensuring that transparent barrier films meet the highest standards for food safety and contact compliance. Leading companies such as Mondi are at the forefront, offering flexible laminates and paper-based alternatives tailored to meet both sustainability goals and performance needs in consumer goods packaging.

United States: Recycling, Mono-Material Films, and High-Tech Applications

The United States transparent barrier packaging films in Consumer Goods market is being reshaped by the U.S. Environmental Protection Agency (EPA)’s recycling goals, which are encouraging investments in infrastructure and the adoption of recycle-ready materials. The U.S. Food and Drug Administration (FDA) also plays a pivotal role, particularly for food-contact films, by driving adoption of decontaminated recycled PET (rPET) that complies with strict safety regulations.

A major trend is the shift toward mono-material films, especially for snacks and packaged foods, making them easier to recycle while maintaining high oxygen and moisture barriers. Companies are also integrating in-mold labeling (IML) into transparent barrier packaging, reducing contamination from adhesives. Beyond sustainability, innovation is evident in biometric-enabled barrier films that enhance authentication and traceability for high-value consumer goods. The e-commerce boom is further amplifying demand for lightweight, durable, and space-efficient packaging solutions that protect products in transit.

China: Regulatory Standards and Demand for Advanced Packaging Security

The China transparent barrier packaging films in Consumer Goods market is strongly influenced by the “14th Five-Year Plan”, which emphasizes plastic pollution control and the development of a modern cold-chain logistics system. From June 1, 2025, new regulations require express delivery companies to use eco-friendly and reusable packaging, significantly boosting the adoption of sustainable barrier films in e-commerce and logistics.

The State Administration for Market Regulation (SAMR) has introduced new food safety standards such as GB 4806.1, which enforces “complete barrier” compliance for food-contact materials. In parallel, demand is rising for sophisticated, high-end packaging that integrates anti-counterfeiting and enhanced barrier properties, particularly in food, beverages, and pharmaceuticals. Reports from the Ellen MacArthur Foundation and Tsinghua University highlight the urgent need for high-quality plastic recycling systems, which will further shape the country’s barrier film market in the coming years.

India: Extended Producer Responsibility and Food-Grade rPET Adoption

The India transparent barrier packaging films in Consumer Goods market is being reshaped by the Plastic Waste Management (Amendment) Rules, 2024, which came into force in April 2025. These rules enforce Extended Producer Responsibility (EPR) for packaging, requiring brands to track and recycle their materials. By July 1, 2025, all plastic packaging in India must be traceable via barcodes or QR codes, ensuring accountability and transparency.

The Food Safety and Standards Authority of India (FSSAI) is actively aligning Indian packaging regulations with global practices, particularly around the safe use of recycled PET (rPET) in food packaging. Companies like UFlex Limited are leading the transition, investing in recycling mixed flexible waste and developing food-grade rPET approved by the USFDA. Rising e-commerce adoption is also fueling demand for traceable, secure, and sustainable barrier films in the consumer goods segment.

Japan: Pioneering Barrier Film Technologies with Global Impact

The Japan transparent barrier packaging films in Consumer Goods market is undergoing rapid change due to the Plastic Resource Circulation Strategy mandating that all packaging be reusable or recyclable by 2025. This aligns with the Plastic Resource Circulation Promotion Law, also effective in 2025, which targets the reduction and redesign of single-use plastics.

Leading companies like Toppan are expanding their global reach with the GL BARRIER film, which is widely used across food, beverages, health, and beauty industries. Similarly, Kuraray is innovating with EVAL™ EVOH barrier materials, enabling ultra-thin, resource-saving multilayer structures that deliver both performance and sustainability. The Ministry of Health, Labor and Welfare (MHLW) has introduced a positive list system for food-contact materials (effective June 2025), ensuring high safety standards. Japan’s leadership in sustainable high-performance films positions it as a key driver of global innovation in transparent barrier packaging.

Brazil: Waste Management Regulations Supporting Sustainable Packaging Growth

The Brazil transparent barrier packaging films in Consumer Goods market is guided by the National Solid Waste Policy (PNRS), which enforces principles of recycling, reuse, and reduction across industries. In January 2025, Law No. 15,088 came into effect, banning the import of plastic waste, compelling companies to rely on domestic recycling ecosystems and adopt sustainable packaging practices.

Brazil is also investing in reverse logistics systems, making producers accountable for the post-consumer recycling and disposal of packaging materials. These initiatives are expected to significantly influence the adoption of transparent barrier packaging films, especially in consumer goods where demand for eco-friendly and recyclable solutions continues to rise.

Transparent Barrier Packaging Films in Consumer Goods Market Report Scope

Transparent Barrier Packaging Films in Consumer Goods Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.7 Billion

|

|

Market Size (2034)

|

$14.4 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Material (PET, PP, PE, EVOH, PVDC, PA, Coatings, Bio-based Polymers), By Application (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Electronics & Consumer Durables, Industrial), By Packaging Format (Stand-up Pouches, Films & Wraps, Bags, Blister Packs, Lidding Films), By End-Use Industry (Food & Beverage, Consumer Goods, Pharmaceutical & Healthcare, Industrial & Chemical)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Huhtamaki Oyj, Mondi Group, Toppan Inc., Constantia Flexibles Group GmbH, Kuraray Co., Ltd., Sealed Air Corporation, Sonoco Products Company, Uflex Limited, Toray Industries, Inc., Innovia Films, Jindal Poly Films Ltd., Cosmo Films Ltd., Mitsubishi Chemical Group Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Transparent Barrier Packaging Films in Consumer Goods Market Segmentation

By Material

- PET

- PP

- PE

- EVOH

- PVDC

- PA

- Coatings

- Bio-based Polymers

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Electronics & Consumer Durables

- Industrial

By Packaging Format

- Stand-up Pouches

- Films & Wraps

- Bags

- Blister Packs

- Lidding Films

By End-Use Industry

- Food & Beverage

- Consumer Goods

- Pharmaceutical & Healthcare

- Industrial & Chemical

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Transparent Barrier Packaging Films in Consumer Goods Market

- Amcor plc

- Berry Global, Inc.

- Huhtamaki Oyj

- Mondi Group

- Toppan Inc.

- Constantia Flexibles Group GmbH

- Kuraray Co., Ltd.

- Sealed Air Corporation

- Sonoco Products Company

- Uflex Limited

- Toray Industries, Inc.

- Innovia Films

- Jindal Poly Films Ltd.

- Cosmo Films Ltd.

- Mitsubishi Chemical Group Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, industry-focused methodology to analyze the transparent barrier packaging films in Consumer Goods market in consumer goods, combining qualitative and quantitative insights. Our approach integrates primary research through interviews with packaging manufacturers, material scientists, brand owners, and regulatory experts, alongside secondary research from corporate reports, scientific publications, and regulatory documents. USDAnalytics evaluates market drivers including sustainability mandates, mono-material adoption, high-barrier technologies, and bio-based alternatives, while assessing innovation in antimicrobial coatings, ALD and vapor-coated barriers, and smart packaging solutions. Regional analyses cover key markets such as the United States, European Union, China, India, Japan, and Brazil, focusing on regulatory compliance, circular economy adoption, e-commerce supply chain needs, and consumer preference for visibility and freshness. Market sizing, CAGR projections, and segmentation by material, application, and packaging format are derived using historical trends, technological adoption rates, and regulatory forecasts, offering actionable insights for packaging designers, consumer goods manufacturers, sustainability-focused companies, and investors seeking growth opportunities in functional and eco-friendly transparent barrier films.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.