Transparent Barrier Packaging Films Market Size, Overview, and Growth Outlook (2025–2034)

Transparent Barrier Packaging Films Market Expected to Double by 2034 as Innovation and Sustainability Drive Consumer Goods Growth

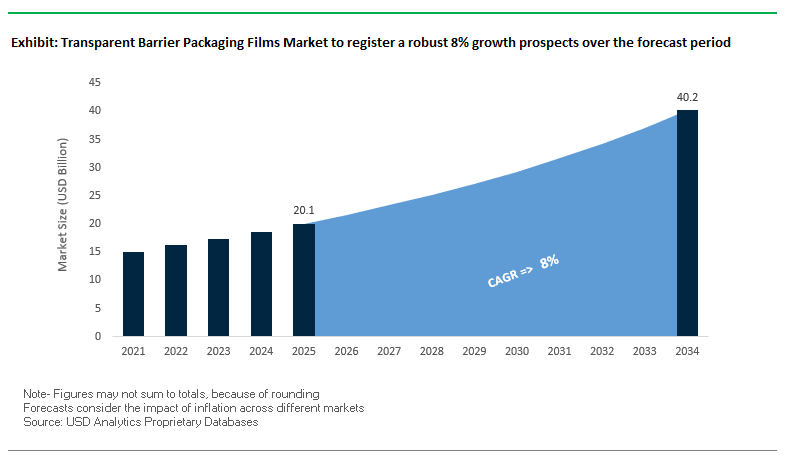

The global transparent barrier packaging films market is projected to grow from $20.1 billion in 2025 to $40.2 billion by 2034, at a CAGR of 8%. These films serve a dual role of protection and product visibility, shielding perishable items from oxygen, moisture, and UV exposure while maintaining consumer appeal. Growth is fueled by the need to extend shelf life, enhance product aesthetics, and meet sustainability objectives across the food, beverage, and personal care industries.

Key Insights for industry professionals and buyers:

- Shelf-life enhancement is critical, with advanced materials such as EVOH reducing gas and moisture transmission for fresh produce, snacks, and ready-to-eat meals.

- Mono-material films enable recyclability, with high-performance PE and PP films supporting circular economy principles.

- Bio-based and compostable materials are emerging to meet consumer and regulatory demands for sustainable packaging solutions.

- Nanotechnology and smart packaging provide antimicrobial properties, freshness indicators, and enhanced barrier performance.

- Cross-industry applications demonstrate versatility, including food, beverages, personal care, and pharmaceutical packaging.

These trends indicate significant opportunities for innovation, sustainability-driven differentiation, and regulatory compliance.

Market Analysis: Technological Innovation and Sustainability Initiatives Are Shaping Transparent Barrier Packaging Films

The transparent barrier packaging films industry is rapidly evolving with advancements in materials, coatings, and recycling solutions. In August 2025, a review article highlighted the increasing use of advanced additives to improve mechanical and antimicrobial properties of sustainable films. Simultaneously, Amcor upgraded its UK recycling facility to enhance the use of post-consumer recycled content, underscoring the growing industry focus on circular economy and sustainable packaging.

In July 2025, Melodea Ltd. launched MelOx Ngen, a plant-based, water-based coating designed to enable recyclability of plastic food packaging, while a study highlighted the use of carrageenan-polyoxometalate composite films offering strong bactericidal activity and rapid biodegradability. These innovations reinforce the dual focus on food safety and environmental sustainability.

Additional strategic moves highlight production efficiency and material innovation. In June 2025, ALPLA Group began series production of thin-walled rPET yogurt cups, advancing circular economy practices for dairy packaging. ExxonMobil Chemical announced a 95% PE-based recyclable thermoformed food package in April 2025, while TOPPAN Holdings and Jindal Films launched BOPP and monomaterial films in March 2024, aligning with recyclability standards in Europe.

Trends and Opportunities in the Transparent Barrier Packaging Films Market

Accelerated Adoption of Recyclable Mono-Material Polymer Structures

The transparent barrier packaging films market is undergoing a rapid transformation as mono-material structures emerge as a scalable alternative to complex multi-layer laminates. Historically, the industry faced a performance-versus-recyclability trade-off, but new innovations are overcoming this challenge. TOPPAN’s GL BARRIER™ PE and PP mono-material grades now deliver exceptional drop strength and retort sterilization compatibility, making them viable for demanding liquid packaging applications.

Regulatory frameworks such as the European Union’s 2030 recyclability mandate are accelerating this transition, with companies like Borealis showcasing closed-loop “pouch-to-pouch” recycling systems for PE laminates. These systems prove that mechanically recycled content can be reprocessed into new high-performance films without compromising sealing or mechanical properties. Brand adoption is also scaling rapidly. At Drupa 2024, Jindal Films demonstrated its PP and PE mono-material films with major global printing press manufacturers, underlining the industry’s commitment to commercializing recyclable packaging across multiple print and pack formats.

Integration of Ultra-Thin Vapor-Deposited Ceramic and Glass Barriers

Another critical trend is the integration of vapor-deposited ceramic and glass-like barrier coatings that rival the protection of aluminum foil while maintaining transparency. Using materials such as silicon oxide (SiOₓ) and aluminum oxide (AlOₓ), manufacturers achieve oxygen and moisture barrier levels comparable to foil, but in lightweight, flexible, and scannable formats.

Durability is a standout feature—these films retain barrier integrity under repeated bending and after retort processing, which is essential for logistics resilience. TOPPAN’s GL BARRIER™ portfolio and DNP’s transparent barrier films exemplify how advanced coatings enable retortable, microwaveable, and metal detector–scannable solutions. These properties expand transparent film use into food, medical, and pharmaceutical applications, sectors that were previously limited to opaque aluminum foil-based structures.

Development of Bio-Based and Marine-Degradable Barrier Coatings

The industry has a significant opportunity to address the end-of-life challenges of plastic films by developing bio-based and marine-degradable coatings. Research is focusing on leveraging abundant natural resources such as seaweed, chitosan, and fish collagen to engineer biodegradable films with improved transparency and mechanical strength. A recent 2025 study demonstrated that seaweed–chitosan–collagen blends outperform seaweed-only films in both functionality and clarity, making them suitable for consumer applications.

These biopolymers also offer natural biodegradability in marine environments, addressing a critical gap for flexible packaging that escapes recycling systems. Chitosan, derived from shellfish waste, is particularly promising due to its film-forming and edible properties, making it an ideal candidate for safe, sustainable coatings. The integration of these materials presents a pathway toward functional barriers that degrade safely in oceans and soils, creating a circular and regenerative model for transparent barrier films.

Enabling Active and Intelligent Packaging for Pharmaceutical and Fresh Food Logistics

Beyond traditional protection, transparent barrier films are evolving into active and intelligent packaging platforms. For fresh food logistics, incorporating oxygen scavengers directly into film layers can lower oxygen concentrations to below 0.01%, dramatically extending the shelf life of sensitive items such as meats and baked goods. This represents a step change from passive to active packaging, offering a dynamic preservation mechanism.

In pharmaceuticals, the opportunity lies in real-time quality monitoring through intelligent film integration. Early-stage R&D has demonstrated the use of pH-sensitive dyes in chitosan-based films, which change color in response to spoilage or chemical instability. Such systems would allow stakeholders to track quality throughout the supply chain and ensure regulatory compliance for biologics and other high-value drugs. By embedding these smart functionalities, transparent barrier packaging films can differentiate as enablers of safety, trust, and traceability in high-stakes markets.

Competitive Landscape: Leading Transparent Barrier Packaging Films Companies Drive Innovation and Sustainability Across Consumer Goods

The transparent barrier packaging films market is dominated by companies leveraging material science, manufacturing expertise, and sustainability initiatives to deliver high-performance and eco-friendly solutions for various end-use applications.

Amcor plc: Expanding PVC-Free and Recyclable Barrier Films for Consumer Goods

Amcor provides AmLite and AmPrima™ series, offering metal-free, high-barrier laminates and recycle-ready flexible pouches. In August 2025, the company upgraded its UK recycling facility and developed the AmSky™ thermoform blister system, a PVC- and aluminum-free solution. Amcor’s vertically integrated operations enable scalable sustainable packaging solutions worldwide.

Berry Global Group, Inc.: Leading Circular Economy Adoption with High-Performance Films

Berry Global produces rigid and flexible films focused on lightweighting and recycled materials. In March 2025, the company reported 93% of FMCG packaging as recyclable or having validated alternatives, alongside a 130% increase in bioplastics purchases. Its Impact 2025 roadmap prioritizes circular, net-zero solutions using proprietary CleanStream® technology.

Mondi Group: Delivering Recyclable and Eco-Friendly Barrier Packaging Solutions

Mondi specializes in recycle-ready flexible packaging and barrier films, emphasizing sustainability through its EcoSolutions approach. In June 2025, the company launched recyclable mono-material bags for dry pet food and Hug&Hold, a paper-based shrink wrap alternative. Mondi targets a 2030 goal of fully recyclable, reusable, or compostable packaging.

Sealed Air Corporation: Protecting Products Globally While Advancing Sustainability Goals

Sealed Air offers films, bags, and protective packaging materials for food, healthcare, and industrial sectors. Its Plastic Reduction strategic plan focuses on reducing environmental footprint while expanding manufacturing to meet global e-commerce and retail food demand. Sealed Air combines high-performance protection with sustainability across diverse applications.

TOPPAN Holdings Inc.: Pioneering Mono-Material Transparent Barrier Films for Global Markets

TOPPAN produces the GL BARRIER series, including GL-SP, a BOPP-based mono-material transparent barrier film. In March 2024, the company expanded production in India and Europe, targeting food, pharmaceutical, and industrial markets. TOPPAN’s vertically integrated operations ensure innovative, high-quality, and compliant solutions for a global customer base.

Transparent Barrier Packaging Films Market Share Insights, 2025-2034

Food & Beverages Lead Transparent Barrier Packaging Films Market by Application

Food and beverages command the largest share of the transparent barrier packaging films industry at 68%, making them the primary driver of innovation and production scale. This dominance is rooted in the sector’s critical need to balance extended shelf life with consumer demand for product visibility and clean-label credentials. High-barrier films such as EVOH, PVDC, metallized PET, and transparent oxide-coated laminates (SiOx, AlOx) are extensively adopted in this segment to reduce oxygen ingress, prevent aroma loss, and protect against moisture while allowing full product visibility on retail shelves. With the global food industry facing mounting pressure to reduce preservatives, improve freshness, and maintain product safety, the packaging’s barrier integrity has become indispensable. Rising e-commerce grocery demand, premiumization of packaged food, and regulatory scrutiny on material safety further reinforce why food and beverages remain the largest and most innovation-intensive user of transparent barrier packaging films.

Stand-up Pouches Dominate Transparent Barrier Packaging Films Market by Format

Stand-up pouches hold the largest share at 42% of the packaging format segment, cementing their role as the preferred choice across food, beverage, and non-food applications. Their ability to merge superior barrier properties with shelf-ready aesthetics and consumer convenience has made them the most widely adopted flexible format. Transparent barrier films enable pouches to protect oxygen- and moisture-sensitive products like coffee, snacks, pet food, and ready-to-drink beverages, while their rigid base ensures strong shelf presence and marketing impact. The growing demand for resealability, portion control, and lightweight logistics advantages further drives this format’s adoption. Additionally, industry innovation is increasingly focused on mono-material pouch structures that are fully recyclable, helping brand owners align with global sustainability goals. This combination of functionality, efficiency, and recyclability secures stand-up pouches as the leading format for transparent barrier packaging films worldwide.

European Union: Regulatory Transformation and New Production Facilities Driving Growth

The European transparent barrier packaging films market is undergoing rapid transformation driven by the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. This regulation mandates that by 2030 all plastic packaging, including barrier films, must meet strict recycled content targets, pushing companies to adopt monomaterial and recyclable alternatives. Alongside this, the Ecodesign for Sustainable Products Regulation (ESPR) is promoting the shift toward durable, refillable, and reusable consumer goods packaging, accelerating innovation in barrier film design.

The EU’s Horizon Europe funding program is providing significant R&D capital for bio-based and compostable film solutions, particularly those using starch blends and cellulose films. The European Food Safety Authority (EFSA) plays a key role by ensuring that transparent barrier films meet stringent food safety standards, making regulatory compliance a core growth factor. On the corporate front, Jindal Films’ launch of PP and PE monomaterial films in March 2024 highlights the industry’s compliance with new recycling rules, while Toppan Holdings’ new Czech Republic production plant marks its first European facility, reducing lead times and strengthening supply chain resilience across the region.

United States: Recycling Initiatives and High-Barrier Film Investments

The U.S. transparent barrier packaging films market is shaped by sustainability goals outlined by the Environmental Protection Agency (EPA), which has spurred significant investments in recycling infrastructure. A defining trend is the use of in-mold labeling (IML), enabling graphics to be embedded during molding, thus creating fully recyclable packaging without adhesives that compromise recycling streams. This approach is particularly gaining traction in snack packaging and food-contact films, where recyclability and performance must go hand in hand.

The rise of e-commerce continues to drive demand for durable, lightweight, and space-efficient barrier films capable of protecting goods through rigorous shipping channels. U.S. companies are also at the forefront of integrating biometric security features, using barrier films to ensure authenticity and prevent counterfeiting in high-value consumer goods. A major development came in January 2023, when Amcor announced a new production facility for recyclable high-barrier films, targeting fast-growing consumer markets in Asia and Latin America, further reinforcing the U.S.’s global leadership in sustainable film innovation.

China: Regulatory Reforms and High-End Packaging Innovation

The Chinese transparent barrier films market is strongly driven by the government’s “14th Five-Year” plan, which includes strict measures against plastic pollution. New rules effective June 1, 2025 require express delivery companies to adopt eco-friendly and reusable packaging—directly boosting demand for recyclable and reusable barrier films in the country’s booming e-commerce sector. Simultaneously, the State Administration for Market Regulation (SAMR) introduced GB 4806.1 food-contact standards, which emphasize “complete barrier” protection to ensure food safety.

China is also witnessing rapid demand for premium, high-barrier packaging with enhanced security features to combat counterfeiting, especially in pharmaceuticals, cosmetics, and high-value foods. The Ellen MacArthur Foundation’s 2024 joint report with Tsinghua University emphasized the urgent need to improve China’s plastic recycling infrastructure, which aligns with government-led incentives promoting remanufacturing and green technologies. These combined efforts are positioning China as a dominant market for advanced and sustainable transparent barrier films.

India: Extended Producer Responsibility and Domestic Film Innovations

The India transparent barrier packaging films market is evolving rapidly under the Plastic Waste Management (Amendment) Rules, 2024, effective from April 1, 2025, which place strong emphasis on Extended Producer Responsibility (EPR). From July 1, 2025, all plastic packaging must be traceable through barcodes or QR codes, pushing companies to adopt smart traceability in their barrier film designs. The Food Safety and Standards Authority of India (FSSAI) has been actively consulting on the use of recycled PET (rPET) for packaging, aiming to align Indian practices with global food-safety standards.

Leading packaging companies are innovating quickly. UFlex Limited has been at the forefront of recycling mixed flexible waste and developing food-grade rPET films approved by the USFDA and aligned with FSSAI guidelines. Furthermore, TOPPAN Speciality Films Private Limited (TSF), in collaboration with TOPPAN Inc., launched GL-SP, a high-performance barrier film made with biaxially oriented polypropylene (BOPP), manufactured locally in India. These initiatives highlight India’s commitment to both sustainability and technological advancement in the transparent barrier films sector, supported by rising demand from e-commerce, retail, and food processing.

Japan: Precision Manufacturing and Global Leadership in Barrier Films

The Japan transparent barrier packaging films market is supported by the country’s Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. Complementing this, the Plastic Resource Circulation Promotion Law (2025) mandates reductions in 12 categories of single-use plastic products, reinforcing demand for compostable and recyclable alternatives. The Ministry of Health, Labor, and Welfare (MHLW) also introduced a new positive list system effective June 2025, specifying approved materials for food contact applications, adding another layer of safety regulation.

Japan’s corporate landscape is marked by high-value innovation. Toppan’s GL BARRIER film has achieved global success across food, beverage, health, and beauty applications, demonstrating Japan’s dominance in high-barrier packaging solutions. Similarly, Kuraray’s EVAL™ EVOH technology allows the production of ultra-thin, lightweight multilayer structures with excellent oxygen-barrier properties, reducing material use while maintaining performance. Japan is emerging as a global hub for transparent barrier film innovation, with an emphasis on precision engineering, sustainability, and advanced functionality.

Brazil: Solid Waste Policy and Reverse Logistics Advancing Film Market

The Brazil transparent barrier packaging films market is shaped by the National Solid Waste Policy (PNRS), which promotes waste reduction, recycling, and responsible disposal. A major legislative update, Law No. 15,088 (January 2025), banned the import of solid waste, including plastics, effectively boosting the domestic market for sustainable packaging materials. This has encouraged local manufacturers to develop recyclable and compostable barrier films tailored to both food and consumer goods packaging.

Brazil is also investing in reverse logistics systems that make producers responsible for post-consumer waste management, reinforcing circular economy practices. The country’s abundant agricultural resources and growing demand for sustainable consumer packaging are driving interest in bio-based transparent barrier films, particularly for food exports and retail packaging. These developments place Brazil as a key growth market in Latin America for sustainable barrier film innovation and adoption.

Transparent Barrier Packaging Films Market Report Scope

Transparent Barrier Packaging Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$20.1 Billion

|

|

Market Size (2034)

|

$40.2 Billion

|

|

Market Growth Rate

|

8%

|

|

Segments

|

By Material (PET, PP, PE, EVOH, PVDC, PA, Coatings, Bio-based Polymers), By Application (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Electronics & Consumer Durables, Industrial), By Packaging Format (Stand-up Pouches, Films & Wraps, Bags, Blister Packs, Lidding Films), By End-Use Industry (Food & Beverage, Consumer Goods, Pharmaceutical & Healthcare, Industrial & Chemical)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Huhtamaki Oyj, Mondi Group, Toppan Inc., Constantia Flexibles Group GmbH, Kuraray Co., Ltd., Sealed Air Corporation, Sonoco Products Company, Uflex Limited, Toray Industries, Inc., Innovia Films, Jindal Poly Films Ltd., Cosmo Films Ltd., Mitsubishi Chemical Group Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Transparent Barrier Packaging Films Market Segmentation

By Material

- PET

- PP

- PE

- EVOH

- PVDC

- PA

- Coatings

- Bio-based Polymers

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Electronics & Consumer Durables

- Industrial

By Packaging Format

- Stand-up Pouches

- Films & Wraps

- Bags

- Blister Packs

- Lidding Films

By End-Use Industry

- Food & Beverage

- Consumer Goods

- Pharmaceutical & Healthcare

- Industrial & Chemical

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Transparent Barrier Packaging Films Market

- Amcor plc

- Berry Global, Inc.

- Huhtamaki Oyj

- Mondi Group

- Toppan Inc.

- Constantia Flexibles Group GmbH

- Kuraray Co., Ltd.

- Sealed Air Corporation

- Sonoco Products Company

- Uflex Limited

- Toray Industries, Inc.

- Innovia Films

- Jindal Poly Films Ltd.

- Cosmo Films Ltd.

- Mitsubishi Chemical Group Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, industry-focused methodology to analyze the transparent barrier packaging films market, integrating both qualitative and quantitative research. Our approach combines primary research with interviews of key stakeholders including packaging manufacturers, material scientists, brand owners, and regulatory experts, alongside secondary research from corporate reports, scientific studies, and government publications. USDAnalytics evaluates market drivers such as mono-material adoption, bio-based films, vapor-deposited barriers, and smart packaging technologies, while assessing innovation trends in antimicrobial coatings, ALD barriers, and active/intelligent packaging. Regional analysis encompasses North America, Europe, Asia-Pacific, and Latin America, focusing on regulatory compliance, sustainability mandates, e-commerce logistics, and consumer demand for product visibility and freshness. Market sizing, growth projections, and segmentation by material, application, packaging format, and end-use industry are derived from historical data, technological adoption rates, and regulatory forecasts, offering actionable insights for packaging designers, consumer goods manufacturers, sustainability-focused companies, and investors seeking growth opportunities in functional and eco-friendly transparent barrier films.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.