Trimethyl Pentanediol Monoisobutyrate Market Overview 2025–2034: $910.5 Million to $1,790 Million at 7.8% CAGR Powered by Waterborne Coatings, Circular Additives, and Green Certification Momentum

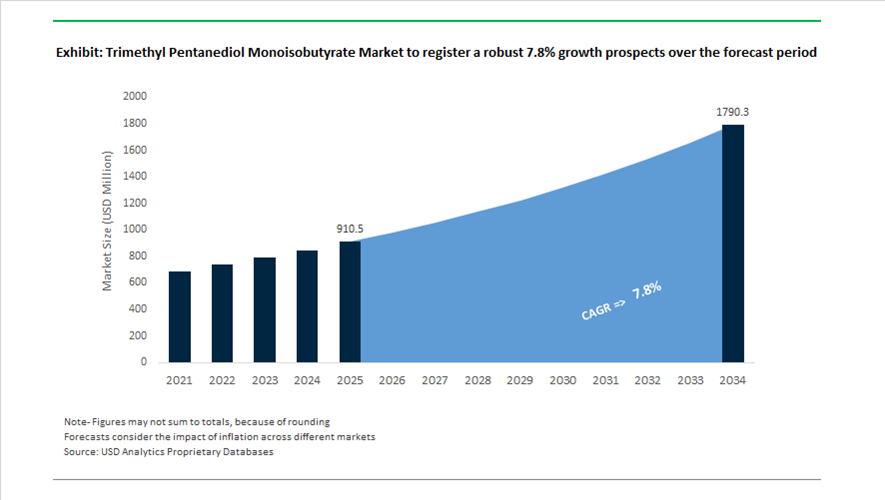

The global Trimethyl Pentanediol Monoisobutyrate (TMPD-MIB) market is valued at $910.5 million in 2025 and is projected to reach $1,790 million by 2034, registering a robust CAGR of 7.8%. TMPD-MIB, widely marketed under trade names such as Texanol, functions primarily as a high-performance coalescing agent in waterborne architectural coatings, latex paints, acrylic dispersions, adhesives, and specialty polymer systems. Demand is being driven by tightening VOC regulations, expansion of water-based coating technologies, and increasing adoption of eco-certified building materials. The market is shifting toward high-purity grades (>99.5%), low-odor variants, and circular feedstock integration as manufacturers align with green building standards and decarbonization targets.

Strategic supply agreements and portfolio optimization initiatives reshaped the competitive landscape beginning in 2024. In January 2024, BASF introduced Paladin RHE 5100, a next-generation coalescing agent designed to enhance film formation in waterborne coatings, intensifying competition in the Texanol-equivalent segment. In March 2024, Dow and DuPont executed further portfolio streamlining initiatives to sharpen focus on additives and intermediates supporting industrial and consumer latex formulations. In May 2024, Ashland Specialty Ingredients signed a strategic supply agreement with PPG Industries, positioning itself as a primary supplier of specialized coalescing agents for next-generation waterborne architectural coatings aimed at reducing environmental impact. Distribution networks expanded in 2025 as Wego Chemical Group in the United States and Stobec in Europe broadened logistics coverage for high-purity TMPD-MIB grades serving electronics coatings and pharmaceutical film applications. In early 2025, Chinese manufacturers such as Runtai Chemical achieved Green Label Type II certification for their TMPD-MIB lines, enabling adoption in zero-VOC architectural projects across Asia-Pacific markets.

Feedstock economics, circular chemistry, and price adjustments defined 2025–2026 market dynamics. In late 2025, Sinopec integrated green hydrogen from its Xinjiang project into specialty chemical production, creating a lower-carbon pathway for intermediates used in Chinese-manufactured Texanol-equivalent products. During the same period, Eastman Chemical Company reported that its Kingsport molecular recycling facility reached production milestones exceeding 2.5 times its 2024 output, strengthening circular supply capabilities for specialty additives. Effective January 2026, Eastman implemented a $0.04 per pound price increase across its Oxo-derivative alcohol portfolio, followed by a second increase in March 2026 citing elevated raw material and operating costs. Celanese announced additional region-wide price hikes in January 2026 effective February 2026, reflecting persistent feedstock volatility. In February 2026, BASF expanded acrylic dispersions production at its Mangalore site to support faster drying, humidity-resistant coatings optimized for tropical conditions where TMPD-MIB plays a critical film-formation role. In the same month, Eastman launched Naia Lyte performance fiber, signaling broader investment in pentanediol-derived and circular specialty chemistries that reinforce long-term structural demand for TMPD-MIB intermediates through 2034.

Structural Substitution, Performance Requalification, and High-Compliance Growth Pathways in the Trimethyl Pentanediol Monoisobutyrate (TXIB) Market

Regulatory Substitution of Phthalates Accelerates TXIB Adoption Across PVC and Polymer Emulsions

The Trimethyl Pentanediol Monoisobutyrate (TXIB) market is experiencing structurally driven demand growth as regulators close remaining loopholes for legacy phthalates in flexible polymers and coatings. The enforcement of China’s GB 4806.15-2024 standard in February 2025 and the tightening of EU REACH annex restrictions have made non-phthalate plasticization a compliance requirement rather than a sustainability preference. Within this regulatory context, TXIB is being qualified as a secondary and performance-enhancing plasticizer that preserves flexibility while enabling ultra-low VOC formulations.

From a processing standpoint, TXIB’s role in plastisol optimization is becoming increasingly strategic. Performance data released in 2025 confirms TXIB’s exceptionally low intrinsic viscosity of approximately 9 cps, positioning it as the lowest-viscosity additive currently available for flexible PVC systems. When used as a partial substitute for primary plasticizers, TXIB can reduce overall plastisol viscosity by up to 40%. This viscosity reduction enables manufacturers to incorporate higher filler loadings, such as calcium carbonate, to control formulation costs without compromising flow, leveling, or coating uniformity.

Beyond PVC, TXIB’s low vapor pressure and high boiling point of approximately 280°C are driving its adoption in water-based polymer emulsions. As the EU’s Ecodesign for Sustainable Products Regulation becomes a baseline compliance framework in 2025, formulators are integrating TXIB as a coalescing agent to lower minimum film-forming temperatures while maintaining VOC emissions well below the 250 g/L threshold required for green building and architectural coating certifications.

Performance-Driven Penetration into Automotive and Cold-Climate Construction Sealants

In parallel with regulatory substitution, TXIB is gaining traction through performance requalification in demanding end-use environments, particularly automotive and construction sealants. Hybrid sealants and one-component polyurethane systems increasingly rely on TXIB to resolve surface tackiness and cold-temperature brittleness associated with legacy benzoate and phthalate plasticizers.

Automotive coating suppliers reported a measurable increase in TXIB usage in underbody coatings and anti-chip primers during the second half of 2025. Unlike traditional plasticizers such as DOP, TXIB delivers a dry-touch surface finish that limits dust pickup and improves interlayer adhesion. This characteristic is particularly critical in electric vehicle manufacturing, where thinner coatings are applied to lightweight substrates and any surface contamination can compromise corrosion protection and paint-line efficiency.

Cold-climate performance is further strengthening TXIB’s value proposition in construction sealants. Research published in late 2024 demonstrated that TXIB-modified sealants retain up to 20% higher elongation-at-break at temperatures as low as minus 20 degrees Celsius compared to standard benzoate systems. This performance advantage has translated into specification-driven adoption for expansion joints, façade sealants, and infrastructure projects in Northern Europe and Canada, where freeze-thaw durability directly influences lifecycle maintenance costs.

Opportunity: Low-Migration Plasticization for Medical and Food-Contact Applications

TXIB’s low migration behavior is opening high-margin opportunities in regulated applications where additive leaching presents both performance and health risks. The formal EU ban on Bisphenol A and certain phthalates in food-contact materials in January 2025 has accelerated qualification cycles for alternative plasticizers in medical devices and packaging components. TXIB, often formulated in blends with DOTP, is increasingly being specified for medical-grade PVC tubing, bags, and connectors due to its reduced extractability under physiological conditions.

Toxicological assessments conducted by regulatory bodies, including validation by U.S. consumer safety authorities, have confirmed TXIB’s suitability for sensitive applications such as children’s products and healthcare devices. Compared with monomeric phthalates, TXIB exhibits significantly lower migration rates, reducing risks of polymer embrittlement, odor generation, and patient exposure during prolonged use.

In food packaging, the implementation of Japan’s Final Positive List for food-contact synthetic resins in May 2025 has created immediate demand for compliant additives in adhesives, gaskets, and sealing layers. TXIB’s resistance to extraction by fatty food simulants enables compliance with FDA 21 CFR and EU 10/2011 migration limits, making it particularly attractive for high-speed packaging lines handling oils, dairy, and processed foods.

Opportunity: High-Flash Point, Non-HAP Solvent Systems for Precision Industrial Cleaning

A less traditional but rapidly expanding growth avenue for TXIB lies in industrial degreasing and precision cleaning, as manufacturers move away from chlorinated solvents and fluorinated systems with high regulatory and environmental risk. Increasing restrictions on substances such as n-propyl bromide and trichloroethylene are forcing cleaning formulators to adopt non-HAP, high-flash-point alternatives capable of dissolving heavy oils and resins.

In late 2025, industrial cleaning suppliers introduced PFAS-free solvent blends positioned as direct replacements for legacy degreasers. TXIB is being incorporated into these systems due to its high flash point, strong solvency, and low global warming potential relative to fluorinated solvents. These attributes allow operators to meet occupational safety and emissions requirements without sacrificing cleaning efficiency.

Precision cleaning applications are emerging as a particularly attractive niche. Aerospace maintenance and electronics manufacturing increasingly require solvents with low outgassing characteristics to prevent fogging and residue formation on optical and electronic components. TXIB’s thermal stability and low volatility profile are driving its qualification in aerospace MRO operations and electronics assembly lines, aligning it with the fastest-growing segments of the industrial cleaning market in 2025.

Trimethyl Pentanediol Monoisobutyrate Market Share and Segmentation Insights

Purity Grade Market Share: Industrial Grade Leads with Waterborne Coatings Expansion

Industrial grade trimethyl pentanediol monoisobutyrate dominates with a 72.80% market share in 2025, supported by its extensive use in paints and coatings, construction materials, and industrial cleaning formulations. Its cost efficiency and proven performance make it the preferred choice for high-volume applications, particularly as a coalescing agent in waterborne coatings. High-purity grade serves niche applications requiring tighter specifications. A key growth driver is the increasing adoption of waterborne coatings, where trimethyl pentanediol monoisobutyrate enables effective film formation at ambient temperatures while complying with stringent VOC regulations, supporting large-scale demand across architectural and industrial coating segments.

End-Use Industry Market Share: Building and Construction Dominates with Architectural Coatings Demand

Building and construction accounts for 48.60% of the trimethyl pentanediol monoisobutyrate market in 2025, driven by its widespread use in architectural paints for residential and commercial infrastructure. The compound is a critical coalescent in waterborne latex paints, ensuring film integrity, durability, and application performance. Automotive and transportation, printing and packaging, personal care and pharmaceuticals, and agriculture and agrochemicals contribute additional demand across specialized applications. A major trend is the shift toward low-VOC paint formulations, where regulatory standards and green building certifications are accelerating the adoption of high-performance coalescing agents that balance environmental compliance with coating performance requirements.

Trimethyl Pentanediol Monoisobutyrate Market Competitive Landscape

The TMPD-MIB market in 2026 is defined by performance-led sustainability, with rising demand for high-purity (>99.5%) coalescents and bio-based synthesis routes. Vertical integration into oxo-alcohol feedstocks and circular production technologies is enabling supply stability for architectural coatings and industrial paint OEMs.

Eastman Strengthens Texanol Leadership with Circular Methanolysis and Pricing Discipline

Eastman Chemical Company remains the global benchmark in TMPD-MIB through its Texanol™ ester alcohol, the industry-standard coalescent for latex paints and architectural coatings. The company generated nearly $1 billion in operating cash flow in 2025, reinforcing financial resilience amid raw material volatility. Strategic price increases of $0.04/lb across North America and Europe protect margins in its oxo-derivatives portfolio. Eastman’s Kingsport methanolysis facility exceeded targets, producing 2.5x recycled content, supporting sustainable coalescent production. For 2026, the company is targeting $125–$150 million in structural cost reductions through higher utilization rates. Its focus on circular economy integration and high-performance additives strengthens leadership in low-VOC coating formulations.

OQ Chemicals Expands Dual-Atlantic Supply of High-Purity OXFILM Coalescents

OQ Chemicals leverages its oxo-intermediate dominance to supply high-purity TMPD-MIB via its OXFILM® 351 platform, optimized for high-PVC architectural coatings. The product’s low-odor profile and 255°C boiling point enhance film formation and scrub resistance in premium latex paints. Its dual production hubs in Germany and the U.S. ensure supply chain resilience across Atlantic markets. OQ is advancing low-toxicity additive systems to help formulators achieve Ecolabel certification with simplified chemistries. The company is expanding aggressively in Asia-Pacific, targeting high-growth applications such as retail floor polishes in India and Southeast Asia. Integrated feedstock control strengthens its position in volatile raw material environments.

Wanhua Accelerates Petrochemical Integration to Scale Specialty Coalescent Production

Wanhua Chemical is rapidly scaling its presence in the TMPD-MIB market through deep petrochemical integration and high-volume capacity expansion. The company surpassed RMB 200 billion in revenue in 2025, supported by a 16% increase in product volumes. Its RMB 7.67 billion investment program is enhancing ethylene and oxo-derivative capabilities critical for isobutyrate ester production. Wanhua’s strategy integrates polyurethane leadership with fine chemicals, enabling bundled solutions for coatings manufacturers. Despite temporary supply disruptions in early 2026, the company continues expanding its global footprint through European distribution partnerships. Its scale-driven cost competitiveness positions it strongly in global coalescent supply chains.

Runtai Advances Ultra-Pure Low-Odor TMPD-MIB for Automotive and Cold-Climate Coatings

Runtai Chemical is emerging as a specialist in environmentally friendly TMPD-MIB, focusing on ultra-pure (>99.7%) grades for high-end coatings. Its products offer exceptional low-temperature performance (-50°C), making them ideal for exterior coatings in cold climates. The company has expanded exports to North America, maintaining compliance with ASTM VOC standards while offering cost advantages. Investments in chromatographic purification enable entry into automotive OEM and electronics coating markets. Runtai’s low-odor synthesis technology reduces residual acids, supporting zero-VOC interior paint applications. Its innovation-driven positioning enhances competitiveness in premium coalescent segments.

Celanese Enhances Feedstock Integration and R&D for Next-Generation Coalescent Systems

Celanese Corporation is strengthening its role in the TMPD-MIB value chain through feedstock integration and advanced materials R&D. The company reported $9.5 billion in 2025 sales and generated $773 million in free cash flow despite volume pressures. Its expanded Michigan Technology Center enables co-development of next-generation coating additives and resin systems. Strategic price increases implemented in March 2026 address supply chain disruptions and protect innovation investments. Celanese continues to supply critical intermediates such as isobutyraldehyde, ensuring upstream stability for TMPD-MIB producers. Integration with engineered materials portfolios enhances its relevance in high-performance coatings.

Chaitanya Chemicals Targets Value-Grade TMPD-MIB with Export Expansion and Custom Supply Solutions

Chaitanya Chemicals operates as a key regional supplier in the value-grade TMPD-MIB segment, focusing on 99% industrial-grade coalescents for water-based paints. Its products are widely used in latex coatings, oil-drilling fluids, and wood preservatives due to their stability and low water solubility. The company expanded exports in late 2025 to capitalize on construction growth in the Middle East and Africa. Its flexible packaging and customized supply capabilities allow it to serve mid-tier coating manufacturers effectively. Chaitanya is also targeting ore flotation applications, diversifying end-use markets. Its cost-effective manufacturing and regional supply strength position it competitively in emerging economies.

United States TMPD-MIB Market Anchored in VOC Policy and Infrastructure-Led Paint Demand

The United States represents the most regulation-driven TMPD-MIB market globally, with demand tightly linked to evolving air-quality standards and public construction activity. The January 2025 amendments finalized by the U.S. Environmental Protection Agency introduced a reactivity-based framework for aerosol coatings, explicitly favoring low-reactivity coalescents such as TMPD-MIB to curb ground-level ozone formation. This regulatory pivot has accelerated reformulation across architectural and industrial latex paints, positioning TMPD-MIB as a compliance-critical ingredient rather than a discretionary additive.

Supply-side strength further reinforces U.S. leadership. Eastman’s Longview, Texas complex continues to function as the world’s largest integrated Texanol production site, with ongoing AI-enabled optimization programs improving batch consistency and achieving purity levels approaching 99.5% for premium coatings. On the demand side, public construction spending exceeding $500 billion annually in 2025 has created sustained pull for weather-resistant exterior paints and protective coatings, where TMPD-MIB is essential for film coalescence, durability, and low-temperature application. Adoption has been further amplified by LEED v5 standards introduced in late 2025, which mandate substantial indoor VOC reductions and have driven TMPD-MIB uptake in “Clean Air” certified building materials ahead of the 2026 compliance cycle.

China TMPD-MIB Market Driven by Green Certification and Digital Manufacturing Scale

China’s TMPD-MIB market is shaped less by price competition and more by policy-backed green labeling and manufacturing digitization. Government-aligned sustainability programs have elevated TMPD-MIB’s role in eco-certified construction, with Green Label Type II approvals increasingly enabling its use in large-scale “Eco-City” and public infrastructure projects. This certification-driven demand has effectively embedded TMPD-MIB into government procurement pathways through 2026.

From a production standpoint, the Eastman–Zibo joint venture has emerged as a strategic Asia-Pacific supply hub. In 2025, the site completed a Digital Twin upgrade that improved energy efficiency and yield control in the self-condensation of isobutyraldehyde, lowering variable costs while tightening quality specifications. Looking ahead, preparatory guidance under China’s upcoming industrial planning cycle, led by the Ministry of Industry and Information Technology, prioritizes high-solids and waterborne coatings for export markets. This positions TMPD-MIB as a structurally embedded coalescent for Chinese architectural coatings supplied to Europe and Southeast Asia. Concurrently, regional logistics clusters in Jiangsu and Shandong have reduced last-mile delivery costs, strengthening just-in-time supply to major domestic paint producers.

India TMPD-MIB Market Accelerated by Low-VOC Policy and Infrastructure Expansion

India is transitioning into a structurally high-growth TMPD-MIB market, driven by regulatory tightening and unprecedented infrastructure investment. A draft low-VOC policy released in May 2025 proposes mandatory compliance with IS 15489 standards for public and commercial buildings by January 2026. This has triggered early-stage reformulation among Indian paint manufacturers, with TMPD-MIB increasingly specified as a compliant coalescent for waterborne architectural coatings.

Industrial localization is progressing in parallel. Under the Production Linked Incentive framework, domestic chemical firms are being encouraged to establish integrated isobutyraldehyde-to-TMPD-MIB value chains, targeting the elimination of 15–20% import dependence in specialty coatings. Demand visibility is further reinforced by the National Infrastructure Pipeline, which has earmarked more than $1.4 trillion for roads, transit hubs, and urban development. These projects require sun-resistant, long-life exterior paints, where TMPD-MIB plays a critical role in maintaining film integrity under high thermal stress. The commissioning of new coating plants in Chennai during 2025 underscores the shift toward localized, climate-adapted formulations incorporating TMPD-MIB.

Japan TMPD-MIB Market Focused on Performance Stability and Smart-City Applications

Japan’s TMPD-MIB market is distinguished by performance specificity rather than volume expansion. Domestic formulators prioritize coalescents that ensure consistent film formation under high humidity and seasonal temperature variability. Proprietary TMPD-MIB grades marketed by JNC Corporation have gained traction for their ability to suppress whitening effects and lower minimum film-forming temperatures, making them indispensable in premium interior and exterior paints.

Innovation partnerships further reinforce this position. Collaborative developments between Japanese resin producers and global chemical suppliers have produced next-generation acrylic emulsions optimized for pairing with TMPD-MIB, enhancing adhesion on mixed substrates such as weathered wood, plastics, and composite panels. Demand visibility was reinforced in 2025 through smart-city redevelopment projects in Tokyo’s waterfront districts, where ultra-low-odor, fast-reoccupancy paints formulated with high-purity TMPD-MIB were specified for large-scale indoor renovations. These applications highlight Japan’s role as a technology benchmark market rather than a volume-driven one.

Comparative Snapshot: TMPD-MIB Market Dynamics by Country

Trimethyl Pentanediol Monoisobutyrate Market County Level Snapshot

|

Country

|

Primary Demand Catalyst

|

Regulatory Influence

|

Market Character

|

|

United States

|

VOC reformulation, public construction

|

Reactivity-based VOC limits, LEED v5

|

Regulation-led, infrastructure-driven

|

|

China

|

Green certification, export coatings

|

Industrial planning and eco-labels

|

Scale with digital efficiency

|

|

India

|

Low-VOC mandates, infrastructure boom

|

Draft national standards, PLI

|

Rapid growth and localization

|

|

Japan

|

Humidity performance, smart cities

|

Quality and performance norms

|

Technology- and premium-focused

|

Trimethyl Pentanediol Monoisobutyrate Market Report Scope

Trimethyl Pentanediol Monoisobutyrate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$910.5 Million

|

|

Market Size (2034)

|

$1790 Million

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Purity Grade (Industrial Grade, High-Purity Grade), By Application (Latex Paint Coalescing Agent, Chemical Intermediates, Solvents and Humectants, Specialty Additives, Industrial Coatings, Oil Drilling Muds), By End-Use Industry (Building and Construction, Automotive and Transportation, Personal Care and Pharmaceuticals, Agriculture and Agrochemicals, Printing and Packaging)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Eastman Chemical Company, JNC Corporation, Celanese Corporation, BASF SE, Nanjing Leopard Chemical Co. Ltd., Jiangsu Tianyin Chemical Co. Ltd., Wuhan Hezhong Biochemical Manufacturing Co. Ltd., Zhejiang Jiande Jianye Organic Chemical Co. Ltd., Dorf Ketal Chemicals, Alfa Chemistry, Suzhou Senfeida Chemical Co. Ltd., Jiangsu Dena Chemical Co. Ltd., Weifang City Riding Out Chemical Co. Ltd., Beijing Eastern Acrylic Chemical Co. Ltd., Hebei Zhenjia New Material Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Trimethyl Pentanediol Monoisobutyrate Market Segmentation

By Purity Grade

- Industrial Grade

- High-Purity Grade

By Application

- Latex Paint Coalescing Agent

- Chemical Intermediates

- Solvents and Humectants

- Specialty Additives

- Industrial Coatings

- Oil Drilling Muds

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- Personal Care and Pharmaceuticals

- Agriculture and Agrochemicals

- Printing and Packaging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Trimethyl Pentanediol Monoisobutyrate Market

- Eastman Chemical Company

- JNC Corporation

- Celanese Corporation

- BASF SE

- Nanjing Leopard Chemical Co. Ltd.

- Jiangsu Tianyin Chemical Co. Ltd.

- Wuhan Hezhong Biochemical Manufacturing Co. Ltd.

- Zhejiang Jiande Jianye Organic Chemical Co. Ltd.

- Dorf Ketal Chemicals

- Alfa Chemistry

- Suzhou Senfeida Chemical Co. Ltd.

- Jiangsu Dena Chemical Co. Ltd.

- Weifang City Riding Out Chemical Co. Ltd.

- Beijing Eastern Acrylic Chemical Co. Ltd.

- Hebei Zhenjia New Material Co. Ltd.

*- List not Exhaustive