Trimethylamine Market Overview 2025–2034: $625.3 Million to $937.3 Million at 4.6% CAGR Anchored in Bio-Methanol Feedstocks, Renewable Amines, and Capacity Expansion

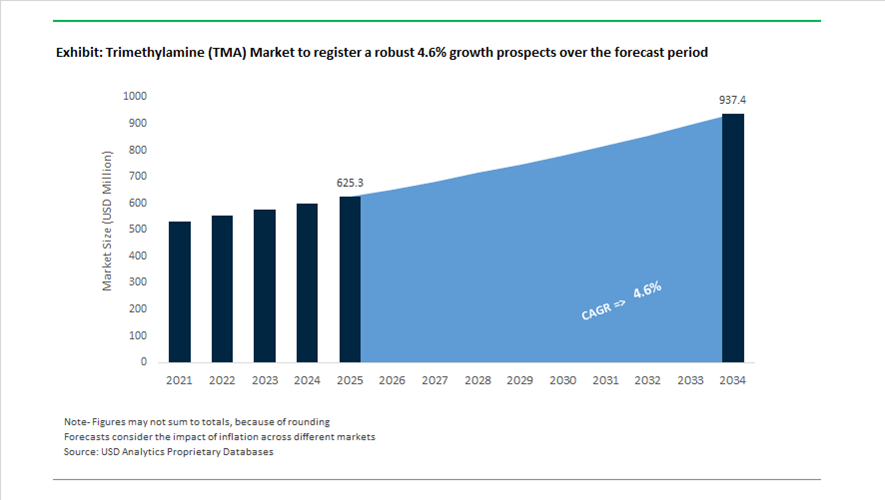

The global Trimethylamine (TMA) market is valued at $625.3 million in 2025 and is projected to reach $937.3 million by 2034, expanding at a CAGR of 4.6%. Trimethylamine, a critical intermediate in the methylamine value chain, serves as a building block for choline chloride, surfactants, polyurethane catalysts, water treatment chemicals, agrochemicals, pharmaceutical intermediates, and electronic-grade amines. Market growth is being shaped by capacity additions in Asia and North America, rising demand for tertiary amines in hygiene and polyurethane applications, and accelerating decarbonization initiatives across methanol-to-amine production pathways. Structural shifts toward biomass-balanced feedstocks and renewable electricity integration are redefining competitive positioning in the global amines industry.

Feedstock transformation and ESG alignment became central themes beginning in 2024. In June 2024, Mitsubishi Gas Chemical became the first Japanese producer of bio-methanol derived from digester gas, securing a renewable carbon pathway for trimethylamine synthesis, as methanol remains the primary feedstock for TMA production. In July 2024, BASF introduced its biomass-balanced trimethylamine BMBcert line, replacing fossil-based feedstocks with certified renewable inputs while maintaining drop-in compatibility for downstream customers. In October 2024, Evonik implemented AI-driven optimization tools across its amine manufacturing network to improve synthesis efficiency and demand forecasting for TMA derivatives used in pharmaceutical and agricultural formulations. Capacity expansion also accelerated in late 2024. In November 2024, Balaji Amines commissioned a new methylamine facility at its Unit IV plant in India, doubling methylamine capacity from 48,000 TPA to 88,000 TPA and strengthening regional supply of TMA and related amines. During late 2023 and early 2024, BASF completed expansion projects at its Geismar, Louisiana site to increase output of specialty amine catalysts used in polyurethane systems that depend on TMA intermediates.

Operational scale and renewable integration intensified during 2025 and 2026. In July 2025, BASF transitioned its Nanjing amines production hub to 100% renewable electricity, positioning one of the world’s largest amines sites to meet global ESG reporting requirements and reduce Scope 2 emissions. In August 2025, Kao Corporation operationalized its world-scale tertiary amine facility in Pasadena, Texas, producing intermediates for surfactants and sterilization agents that rely on trimethylamine chemistry. Eastman Chemical reported in January 2026 that its Kingsport methanolysis facility achieved more than 2.5 times higher recycled-content output in 2025 compared to 2024, supporting circular intermediates within its amine derivative portfolio. In February 2026, Mitsubishi Chemical Group announced its exit from the coke and carbon materials business, reallocating capital toward high-value functional chemicals including electronic-grade amines.

Structural Realignment, Regulatory Compression, and High-Value Diversification in the Trimethylamine (TMA) Market

Vertical Integration and Trade Protection Reshape the TMA–Choline Chloride Value Chain

The Trimethylamine market remains structurally anchored to choline chloride production, which continues to absorb the majority of global TMA volumes due to sustained growth in poultry and swine nutrition. Global adoption of choline chloride as a non-negotiable feed additive has increased by an estimated 18 to 22%, driven by intensified protein demand and tighter feed efficiency targets. However, the operating dynamics of this value chain shifted decisively in 2025 as trade policy replaced price arbitrage as the primary market driver.

The European Commission’s decision in December 2024 to impose definitive anti-dumping duties of 90.0 to 115.9% on Chinese choline chloride imports fundamentally altered regional sourcing strategies. These measures, effective for five years, eliminated low-cost imports from the European feed additives market and forced downstream formulators to secure domestic supply. In response, European and North American producers accelerated backward integration into TMA production to stabilize feedstock availability and protect margins.

Producers such as Balchem and Eastman have responded by expanding in-house TMA-to-choline conversion capacity, upgrading automation, and shifting toward high-purity aqueous choline solutions that meet “gold standard” feed certifications. Balchem’s 50% expansion of its primary choline facility, including more than 2,200 square meters of new processing and packaging infrastructure, reflects a broader industry pivot toward regionally insulated supply chains. As a result, TMA demand is becoming increasingly regionalized, with producers prioritizing proximity to feed markets and regulatory alignment over export-led volume growth.

Pharmaceutical-Grade TMA Faces Tightened GMP and Nitrosamine Controls

Beyond animal nutrition, the TMA market is undergoing a pronounced quality-driven bifurcation due to escalating regulatory scrutiny in pharmaceutical manufacturing. As a strong nucleophile and methylating agent, TMA plays a critical role in synthesizing a range of Active Pharmaceutical Ingredients, including intermediates requiring precise quenching and methylation steps. In 2025, this application is shifting decisively toward ultra-high-purity grades as regulators intensify oversight of nitrosamine contamination risks.

The U.S. FDA’s September 2024 Revision 2 guidance on controlling nitrosamine impurities has had immediate downstream effects on tertiary amines such as TMA. Even trace levels of secondary amine impurities can react with nitrites during API synthesis, forming potentially carcinogenic nitrosamines. As a result, pharmaceutical manufacturers are now mandating Certificates of Analysis demonstrating TMA purity exceeding 99.9%, alongside detailed impurity profiling and batch traceability.

Parallel developments in Europe are reinforcing this trend. The EMA’s January 2025 draft updates to its Chemistry of Active Substances guideline require full disclosure of reagents used during work-up and quenching steps, including precise molar equivalents. This has elevated GMP-compliant TMA from a cost input to a regulatory risk variable. Suppliers capable of offering pharmaceutical-grade TMA with validated impurity controls are capturing pricing premiums, while commodity-grade producers face structural exclusion from regulated drug manufacturing supply chains.

Opportunity: Amine-Based Carbon Capture and Biogas Upgrading Systems

A structurally significant growth opportunity for TMA is emerging in carbon capture and renewable gas upgrading, where amine chemistry is central to decarbonization economics. Conventional Monoethanolamine systems suffer from high regeneration energy requirements, limiting large-scale deployment. TMA and its derivatives are increasingly being evaluated as alternative amine components that offer higher CO₂ loading capacity and lower thermal penalties.

Breakthrough research published by MIT chemical engineers in December 2025 demonstrated that amine-buffered capture systems can release CO₂ at temperatures as low as 60 degrees Celsius, compared with the 120 degrees Celsius required in conventional solvent regeneration. This reduction has the potential to cut energy penalties for post-combustion carbon capture by nearly 50%, materially improving project economics for cement, steel, and power generation facilities.

In parallel, the biogas sector represents a fast-growing application corridor. Raw biogas typically contains up to 40% CO₂, requiring upgrading before grid injection or vehicle fuel use. Research from the University of Twente in late 2025 highlighted the effectiveness of amine-functionalized materials, including TMA-derived systems, in selectively removing CO₂ to produce pipeline-quality biomethane. This positions TMA as a strategic enabler for farm-scale digesters and wastewater treatment plants seeking compliance with renewable gas standards.

Opportunity: High-Purity TMA Salts for Electronics, Energy Storage, and Hydrogen Carriers

A second high-value opportunity is emerging at the intersection of advanced electronics and the hydrogen economy, where TMA serves as a precursor for specialty salts and functional materials. In semiconductor manufacturing, demand for Tetramethylammonium Hydroxide continues to grow as feature sizes shrink and defect tolerance narrows. This is driving upstream demand for electronic-grade TMA with ultra-low metal and halide contamination.

Beyond electronics, TMA is gaining relevance in energy applications. Industrial producers such as Chemanol are increasingly positioning TMA as a precursor for aviation-grade antiknock additives, water-gel explosives, and other performance-critical formulations that outperform traditional commodity outlets. These applications are demonstrating stronger margins and more resilient demand cycles than bulk feed uses.

In hydrogen storage and transport, publicly funded research programs in the United States and Europe are investigating methylated amines as safer liquid organic hydrogen carriers. TMA-based salts are also being qualified for Alkaline Exchange Membrane electrolyzers, which aim to reduce green hydrogen costs by enabling non-precious metal catalysts. These developments, supported by federal funding initiatives launched in late 2024, indicate that TMA’s role is expanding from a classical industrial amine to a functional building block in next-generation energy systems.

Trimethylamine Market Share and Segmentation Insights

Grade Market Share: Industrial Grade Leads with Bulk Chemical and Feed Additive Production

Industrial grade trimethylamine holds a 52.80% market share in 2025, reflecting its dominant role in large-scale applications such as choline chloride production, quaternary ammonium compounds, and agrochemicals. Its cost-effectiveness and consistent quality make it suitable for high-volume industrial processes. Technical grade, food and pharmaceutical grade, and electronic grade serve more specialized applications requiring higher purity levels. A key market driver is its strong linkage to animal feed production, where trimethylamine is a primary input for choline chloride, supporting nutritional requirements in poultry, swine, and aquaculture industries and sustaining steady global demand.

Application Market Share: Choline Chloride Production Leads with Livestock Nutrition Demand

Choline chloride production accounts for 38.60% of the trimethylamine market in 2025, driven by its essential role as a feed additive that supports animal growth, liver function, and feed efficiency. Other applications such as quaternary ammonium salts, agrochemicals, ion exchange resins, pharmaceutical intermediates, petroleum additives, and electronic chemicals contribute to diversified demand. A key trend is the evolution toward precision animal nutrition, where customized choline chloride formulations including liquid and dry variants, optimized carriers, and blended additives are increasingly adopted to enhance bioavailability and handling, supporting sustained trimethylamine consumption across global livestock production systems.

Trimethylamine Market Competitive Landscape

The Trimethylamine market in 2026 is shaped by vertical feedstock security, CCS-enabled low-carbon TMA production, and rapid scaling of high-purity electronic-grade intermediates for semiconductors, water treatment, and specialty resins, with sustainability-as-a-service and regional integration defining competitive positioning.

BASF SE Advances Biomass-Balanced Trimethylamine and Verbund Integration Strategy

BASF SE is strengthening its leadership in the Trimethylamine market through its “Winning Ways” strategy centered on specialty amines and integrated Verbund production. The launch of trimethylamine pure BMBcert™ enables 100% renewable feedstock substitution, supporting low-carbon TMA demand across pharmaceuticals and water treatment applications while reducing Scope 3 emissions. The Zhanjiang Verbund site enhances regional supply chain security and localized methylamines production for Asia’s agrochemical and nutrition sectors. BASF’s EBITDA guidance of €6.2–€7.0 billion for 2026 is supported by €2.3 billion in cost optimization initiatives, reinforcing margin stability. The company’s focus on structural value unlocking optimizes amination asset utilization while accelerating renewable electricity adoption. Its decarbonization roadmap targets CO2 emissions reduction to 17.2–18.2 million metric tons, aligning with global green chemical manufacturing trends.

Eastman Chemical Company Strengthens Specialty Amine Margins Through Pricing Discipline

Eastman Chemical Company is consolidating its position in the Trimethylamine market by leveraging its Taminco platform and specialty amine portfolio. The company generated nearly $1 billion in operating cash flow in 2025, demonstrating resilience amid global economic volatility. Strategic price increases across oxo-derivatives and amines in 2026 reflect proactive margin protection against raw material inflation and reinforce premium positioning. Eastman achieved $100 million in cost savings in 2025 and targets an additional $100 million in 2026 through operational efficiency programs. Its lean manufacturing model enhances competitiveness in methylamines and downstream TMA derivatives. The company is expanding applications in consumables and building materials, where TMA-based surfactants and resins are critical for waterborne coatings and high-durability construction systems.

Balaji Amines Limited Accelerates Import Substitution with Capacity Expansion

Balaji Amines Limited is emerging as a dominant regional player in the Trimethylamine market through aggressive import substitution and capacity scaling strategies. The commissioning of its Unit IV methylamines plant increased capacity from 48,000 TPA to 88,000 TPA, delivering cost advantages and strengthening domestic supply resilience. Approximately 80% captive consumption of methylamines into derivatives such as choline chloride and DMAc reduces exposure to TMA price volatility and enhances value chain integration. Government-backed incentives totaling ₹258 crore under “Mega Project” status improve long-term profitability through tax benefits and subsidies. The company’s zero-debt balance sheet supports its ₹750 crore investment in specialty chemicals expansion via internal accruals. This vertically integrated model positions Balaji Amines as a key supplier in South Asia’s agrochemical and feed additive markets.

Mitsubishi Gas Chemical Drives Green TMA Production with Bio-Methanol Feedstocks

Mitsubishi Gas Chemical (MGC) is advancing the Trimethylamine market through its “Grow UP 2026” strategy focused on high-functionality chemicals and green transformation. The company is prioritizing electronic materials and life sciences, where high-purity TMA derivatives are essential for semiconductor processing and pharmaceutical synthesis. Its transition to bio-methanol feedstocks enables the production of green TMA, aligning with decarbonization mandates across Japan and Southeast Asia. MGC is investing in R&D for specialty amine catalysts used in polyurethane foams, targeting automotive and furniture sectors requiring low-emission and low-odor solutions. The company is strengthening its electronic chemicals segment to offset cyclicality in commodity chemicals. This strategic pivot enhances resilience and positions MGC at the forefront of sustainable methylamine innovation.

AkzoNobel/Nouryon Expands TMA Demand Through Coatings Innovation and Strategic Merger

AkzoNobel and Nouryon are reinforcing their influence in the Trimethylamine market through downstream demand creation in performance coatings and specialty additives. A 27% increase in operating profit to €1.16 billion in 2025 reflects a price-over-volume strategy and €980 million in cost reductions, highlighting operational discipline. The planned merger with Axalta will create a $17 billion coatings leader, significantly increasing internal demand for TMA-derived curing agents and resins. The Industrial Excellence Program streamlined operations by reducing 3,100 roles, optimizing manufacturing toward high-margin marine and protective coatings. Divestment of its India business for €922 million enables reinvestment into advanced R&D in Europe and North America. The company is prioritizing waterborne coatings technologies to comply with stringent VOC regulations, increasing reliance on amine-based crosslinking systems.

India Trimethylamine Market Strengthened by Scale Expansion and Export Stability

India has emerged as one of the most structurally resilient Trimethylamine markets globally, anchored by aggressive capacity expansion and integrated energy planning. In November 2024, Balaji Amines commissioned its Methyl Amine Unit IV, effectively doubling installed TMA capacity to 88,000 TPA by FY2025. This expansion is not an isolated move but part of a broader roadmap that targets total amine capacity of 416,000 MT by 2026, supported by ₹200–₹250 crore of internally funded capital expenditure. This scale-up has materially reduced India’s dependence on imported TMA and derivatives, particularly for pharmaceutical and agrochemical applications.

Energy integration has become a competitive lever. To mitigate rising carbon-related costs on export-grade amines, Balaji Amines commissioned the first 8 MW phase of a 20 MW captive solar project in April 2025, directly powering energy-intensive TMA distillation columns. On the demand side, regulatory reforms announced by the Ministry of Health and Family Welfare in September 2025 halved drug development test-license timelines, accelerating domestic pharmaceutical R&D where TMA serves as a critical intermediate. Export momentum remains strong, with TMA-derived herbicides recording peak shipments to South America in early 2025. Importantly, domestic pricing remained stable around $811 per metric ton in Q3 2025, reflecting feedstock security and insulation from global freight volatility.

China Trimethylamine Market Anchored in Cost Leadership and Low-Carbon Transition

China continues to define the global price benchmark for Trimethylamine, underpinned by massive scale and vertically integrated methanol-to-amine infrastructure. In late 2024, BASF completed the transition of its Nanjing amines portfolio to 100% renewable electricity, delivering an estimated 4% reduction in product carbon footprint versus 2020 baselines. This move aligns with China’s broader industrial decarbonization agenda while preserving cost competitiveness.

Capacity optimization remains central. In July 2025, BASF nearly doubled production of DMAPA, a key TMA derivative, at its Nanjing site to serve surging Asia-Pacific surfactant demand. At the technology frontier, BASF and ExxonMobil formalized a methane pyrolysis collaboration in November 2025, targeting low-emission hydrogen supply for future amine synthesis. Despite these sustainability investments, China maintained its position as the global price floor for TMA, with Q3 2025 prices averaging $688 per metric ton. This pricing power continues to pressure international producers while reinforcing China’s dominance in bulk-grade exports.

European Union Trimethylamine Market Defined by Trade Defense and Biocatalytic R&D

The European Union TMA market, with Germany at its core, has shifted decisively toward trade protection and technological differentiation. In December 2025, the EU imposed anti-dumping duties ranging from 90.0% to 115.9% on Chinese choline chloride imports, a major TMA derivative, securing domestic feed additive value chains for an initial five-year period. This was reinforced by stricter customs origin rules finalized by DG TRADE to prevent circumvention via third-country processing.

Parallel to these trade measures, German research clusters have intensified work on advanced biocatalysis. Late-2025 initiatives focused on glycyl radical enzyme engineering to improve microbial conversion efficiency of choline to TMA, targeting specialty and pharmaceutical-grade applications rather than bulk volumes. This dual strategy of regulatory insulation and biochemical innovation positions the EU market toward higher-value, lower-volume TMA derivatives with strong compliance credentials.

United States Trimethylamine Market Sustained by Specialty Demand and Pricing Power

The United States represents the highest-priced major TMA market, reflecting its orientation toward specialty end uses. Prices reached approximately $925 per metric ton in September 2025, supported by consistent demand from oilfield chemicals and regulated pharmaceutical manufacturing. Domestic producers have deliberately avoided volume-driven competition, instead focusing on purity and compliance.

Balchem Corporation and Eastman Chemical are leading the transition toward ultra-high-purity choline chloride for human nutrition, eliminating residual chlorinated impurities that are increasingly scrutinized by regulators. On the sustainability front, Eastman reaffirmed its 2050 carbon neutrality target in late 2025, initiating energy audits across TMA production assets to evaluate low-carbon methanol sourcing. These steps collectively reinforce the U.S. market’s premium positioning.

Japan Trimethylamine Market Oriented Toward Electronic-Grade Specialization

Japan’s TMA market is structurally distinct, prioritizing ultra-high-purity and electronics-grade applications over volume growth. In November 2025, Mitsubishi Gas Chemical secured a long-term agreement for one million tons per year of ultra-low-carbon methanol from the Pacifico Mexinol Project. This feedstock underpins Japan’s strategy to commercialize “green” TMA by the end of the decade.

Japanese producers have simultaneously pivoted toward electronic-grade TMA used in semiconductor cleaning and fabrication processes, a shift that drove regional prices to approximately $1,210 per metric ton in Q3 2025. This premium reflects both stringent purity requirements and Japan’s entrenched role in the global semiconductor supply chain, making TMA a strategic specialty chemical rather than a commodity.

Comparative Snapshot: Trimethylamine Market by Country

Trimethylamine (TMA) Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Structural Advantage

|

Market Character

|

|

India

|

Capacity doubling, export stability

|

Local feedstock, renewable energy

|

Scale-driven and resilient

|

|

China

|

Cost leadership, decarbonized bulk

|

Integrated methanol supply

|

Volume-dominant, low-cost

|

|

European Union

|

Trade protection, biocatalysis

|

Regulatory insulation

|

High-value, compliance-led

|

|

United States

|

Specialty purity, nutrition and pharma

|

Pricing power

|

Premium-oriented

|

|

Japan

|

Electronic-grade and green TMA

|

Ultra-low-carbon feedstock

|

Niche, high-margin

|

Trimethylamine (TMA) Market Report Scope

Trimethylamine (TMA) Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$625.3 Million

|

|

Market Size (2034)

|

$937.3 Million

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Grade (Technical Grade, Industrial Grade, Food and Pharmaceutical Grade, Electronic Grade), By Form (Anhydrous Trimethylamine, Aqueous Trimethylamine), By Application (Choline Chloride Production, Quaternary Ammonium Salts, Ion Exchange Resins, Agrochemicals, Pharmaceutical Intermediates, Petroleum Additives, Electronic Chemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Eastman Chemical Company, Balaji Amines Limited, Mitsubishi Gas Chemical Company Inc., Luxi Chemical Group Co. Ltd., Akzo Nobel N.V., Balchem Corporation, Alkyl Amines Chemicals Limited, Sintez OKA, Zhejiang Jianye Chemical Co. Ltd., Celanese Corporation, Shandong Hualu Hengsheng Chemical Co. Ltd., Evonik Industries AG, Triveni Interchem Pvt. Ltd., Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Trimethylamine Market Segmentation

By Grade

- Technical Grade

- Industrial Grade

- Food and Pharmaceutical Grade

- Electronic Grade

By Form

- Anhydrous Trimethylamine

- Aqueous Trimethylamine

By Application

- Choline Chloride Production

- Quaternary Ammonium Salts

- Ion Exchange Resins

- Agrochemicals

- Pharmaceutical Intermediates

- Petroleum Additives

- Electronic Chemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Trimethylamine Market

- BASF SE

- Eastman Chemical Company

- Balaji Amines Limited

- Mitsubishi Gas Chemical Company Inc.

- Luxi Chemical Group Co. Ltd.

- Akzo Nobel N.V.

- Balchem Corporation

- Alkyl Amines Chemicals Limited

- Sintez OKA

- Zhejiang Jianye Chemical Co. Ltd.

- Celanese Corporation

- Shandong Hualu Hengsheng Chemical Co. Ltd.

- Evonik Industries AG

- Triveni Interchem Pvt. Ltd.

- Huntsman Corporation

*- List not Exhaustive