Tube Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Tube Packaging Market Set to Reach $27.4 Billion by 2034 as Sustainability and Premiumization Drive Growth

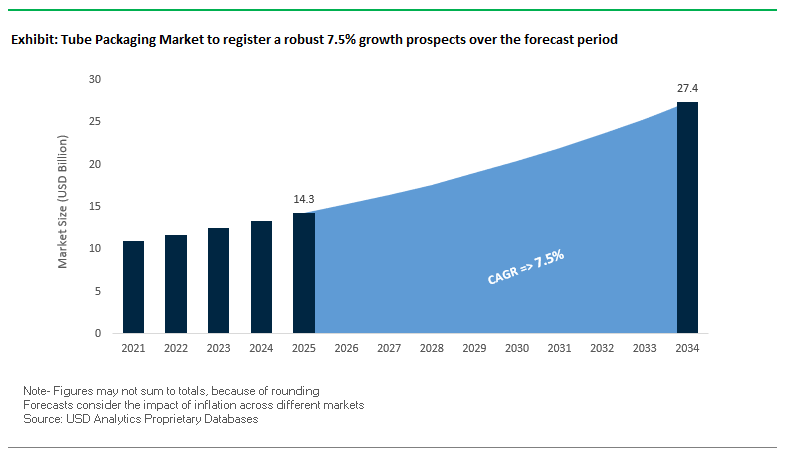

The global tube packaging market is projected to grow from $14.3 billion in 2025 to $27.4 billion by 2034, at a CAGR of 7.5%. This market is at the forefront of packaging innovation, driven by the need for product preservation, consumer convenience, and sustainable solutions. Tubes—including plastic, aluminum, and laminate variants—provide an effective balance of functionality, protection, and brand visibility, serving personal care, food, and pharmaceutical industries.

Key Insights for industry professionals and buyers:

- Sustainability is a primary driver, with mono-material solutions and recyclable tubes reducing environmental impact.

- Refillable and reusable systems are gaining traction, lowering material usage while promoting brand loyalty.

- Advanced printing and finishing techniques, including digital printing and tactile textures, create premium product experiences.

- E-commerce optimization is critical; tubes’ lightweight and durable nature makes them ideal for direct-to-consumer channels.

- Integration of security features, such as QR codes and tamper-evident seals, enhances logistics, inventory management, and product protection.

Market Analysis: Strategic Acquisitions and Technological Innovations Propel Tube Packaging Market Forward

The tube packaging industry is witnessing rapid innovation, driven by sustainability, consolidation, and technological advancements. In August 2025, Albéa acquired Amfora Packaging, expanding its footprint in Latin America. The same month, academic research highlighted the use of advanced additives to improve mechanical and antimicrobial properties of sustainable packaging films. Additionally, a new composite antimicrobial film demonstrated strong bactericidal activity and biodegradability, emphasizing the focus on health and environmental safety.

In June 2025, Indorama Ventures acquired a minority stake in EPL Limited, enhancing its tube packaging capabilities. In March 2025, TOPPAN Holdings launched GL-SP, a biaxially oriented polypropylene (BOPP) transparent barrier film, enabling mono-material and recyclable packaging. Earlier, in May 2024, L’Oréal and Albéa unveiled a paper-based tube, reinforcing the market trend toward eco-friendly packaging, while April 2024 saw Hoffmann Neopac divest its metal tin business to focus on core tube packaging solutions.

March 2024 marked EPL Limited’s acquisition of Creative Stylo Packs, expanding its product portfolio for high-performance and sustainable tubes.

Trends and Opportunities in the Tube Packaging Market

Strategic Shift Towards High-Performance Mono-Material Polyethylene Tubes

The tube packaging market is undergoing a major transformation with the adoption of mono-material polyethylene (PE) tubes, engineered for recyclability without compromising performance. Traditionally, tube packaging relied on multi-material structures—such as laminated bodies paired with non-PE caps—which created recycling bottlenecks. Recent innovations are overcoming these barriers. For example, Hoffmann Neopac has launched the market’s first fully recyclable polyethylene tubes with a high-density polyethylene (HDPE) flip-top cap, ensuring that both the body and closure can be processed in existing HDPE recycling streams.

Independent verification of recyclability is critical to industry adoption. Neopac’s Polyfoil® MMB tube has earned RecyClass approval, confirming its compatibility with Europe’s rigid HDPE recycling streams. This certification demonstrates that plastic recovered from these tubes can re-enter high-value applications, such as HDPE blow-molded bottles with 25% recycled content, thus supporting a closed-loop circular economy.

The momentum is driven by brand-level sustainability commitments. For instance, Albéa has pledged to make 100% of its packaging recyclable, reusable, or compostable by 2025, and has developed all-PE tubes for the oral care segment that can be recycled in a single waste stream. These innovations signal a structural shift, where recyclable mono-material tubes are set to become the industry standard.

Adoption of Integrated Digital Printing for Mass Customization and Anti-Counterfeiting

Digital printing is redefining the aesthetics and security landscape of tube packaging. Unlike traditional offset printing, which requires expensive plates and long production runs, digital technology enables cost-efficient customization and variable data printing, making it possible to run limited batches, personalized designs, and targeted campaigns. Brands can deliver consumer engagement at scale, using packaging as a direct marketing channel.

The benefits extend to brand protection and anti-counterfeiting. Digital techniques allow for the integration of micro-text, serialized QR codes, and invisible inks that consumers can verify with smartphones. A serialized code enables real-time authentication; if a number is duplicated, the system flags it as counterfeit. Furthermore, covert security features—such as specialized varnishes or UV-reactive micro-text—add deeper layers of protection, making replication by counterfeiters extremely difficult.

This dual function—enhanced consumer engagement and product authentication—is fueling the widespread adoption of digital printing in tube packaging, particularly in high-value categories like pharmaceuticals, nutraceuticals, and premium cosmetics, where counterfeiting poses significant risks.

Development of Refillable and Reusable Tube Systems

One of the most promising opportunities in the tube packaging industry lies in refillable and reusable systems, particularly for cosmetics and personal care. Companies like Meliora Packaging are pioneering outer shells made from durable materials such as aluminum or premium PCR plastics, which house replaceable inner pouches. This design reduces single-use plastic waste while cultivating consumer loyalty through refill-based consumption habits.

Early trials indicate strong consumer acceptance. Unilever’s in-store refill pilots have reported that weekly purchases from refill stations outpaced sales of single-use packs by over one-third, proving the commercial viability of refill systems. Beyond sustainability, these solutions support premiumization by offering luxury tactile and visual appeal—outer shells in brushed aluminum or high-quality plastics enhance the consumer experience while lowering environmental impact.

The opportunity aligns with broader ESG commitments and the consumer shift toward eco-friendly packaging alternatives, positioning refillable tubes as a high-growth segment.

Expansion into High-Growth Pharmaceutical and Nutraceutical Applications

Another major growth driver for tube packaging is its adoption in pharmaceuticals and nutraceuticals, where precision dosing and barrier integrity are critical. Tubes provide controlled single-dose dispensing, making them ideal for ointments, gels, and topical formulations, ensuring patient compliance and reducing waste.

Packaging providers such as Montebello Packaging offer aluminum and laminated tubes registered with USFDA and EU DMF (Drug Master File) standards, ensuring compliance for regulated applications. These tubes are engineered to protect sensitive formulations from oxygen, moisture, and UV light, extending product shelf life and maintaining efficacy.

The pharmaceutical sector also demands chemically inert materials capable of withstanding aggressive formulations. Innovations in specialized aluminum laminates and high-barrier polymer coatings are expanding the role of tubes in this segment. Meanwhile, the nutraceutical sector is embracing tube-based packaging for gels, supplements, and wellness products, capitalizing on their portability, dosing accuracy, and consumer convenience.

Competitive Landscape: Leading Tube Packaging Companies Drive Sustainability, Innovation, and Operational Excellence Globally

The tube packaging market is shaped by major players leveraging materials science, design innovation, and manufacturing expertise to deliver high-performance, eco-friendly, and durable packaging solutions.

EPL Limited (formerly Essel Propack): Setting Standards in Sustainable Laminated Tube Solutions

EPL Limited manufactures laminated plastic tubes, including Platina and Green V-pack lines, designed to be recyclable and lightweight. The company’s EPL Way strategy emphasizes circular economy initiatives and environmental footprint reduction. EPL recently won the IMC Ramkrishna Bajaj National Quality Award 2024, reflecting its commitment to quality and innovation.

Albéa S.A.: Expanding Global Footprint with Recyclable and Eco-Friendly Tube Solutions

Albéa specializes in beauty and personal care tubes, offering Greenleaf and RecyClass-certified products. The August 2025 acquisition of Amfora Packaging strengthened its Latin American presence, while the Albéa Way strategic plan focuses on sustainable materials, circularity, and eco-conscious innovation.

Amcor plc: Integrating Recycled Content and High-Barrier Laminates for Premium Packaging

Amcor provides flexible and rigid packaging, including AmLite high-barrier laminates and AmPrima™ recycle-ready pouches. In August 2025, it upgraded its UK recycling facility to boost post-consumer recycled content. Its strategy emphasizes circular economy adoption while maintaining product protection and brand differentiation.

Hoffmann Neopac AG: Concentrating on Tube Packaging Excellence through Sustainable Materials

Hoffmann Neopac focuses on EcoDesign and recycled plastic tubes, divesting its metal tin business in April 2024 to prioritize core tube solutions. Its Neopac Way strategy drives material innovation, environmental sustainability, and global operational efficiency, ensuring high-quality tube packaging delivery.

Huhtamaki Oyj: Pioneering Fiber-Based and Recyclable Tube Packaging for Food and Consumer Products

Huhtamaki provides paper and fiber-based containers and tubes, developing plant-fiber alternatives for sustainability. In July 2025, it earned an EcoVadis gold medal for the fifth consecutive year and continues to innovate with Push Tab® mono-material PET tubes that are ready for recycling.

Tube Packaging Market Share Insights, 2025-2034

Squeeze Tubes Dominate Market Share by Product Type in the Tube Packaging Industry

Squeeze tubes command the largest share of the tube packaging market at around 40%, underscoring their unmatched versatility and cost-effectiveness across diverse applications. Manufactured primarily from polyethylene (PE) or laminated plastic structures, squeeze tubes are the standard packaging for mid-to-low viscosity products such as toothpaste, lotions, creams, adhesives, and food pastes. Their dominance is reinforced by the balance of performance and affordability: they provide lightweight protection, strong barrier properties, and excellent printability, which enhances brand visibility in highly competitive consumer markets. Additionally, the surge in demand for sustainable packaging has driven innovation in recyclable and PCR (post-consumer recycled) squeeze tubes, aligning with both regulatory mandates and corporate ESG goals. This adaptability across sectors, combined with the ability to scale for mass production at low cost, ensures squeeze tubes remain the backbone of the tube packaging industry.

Cosmetics & Personal Care Drive Majority Share by Application in the Tube Packaging Industry

Cosmetics and personal care products account for the majority share of the tube packaging industry at an estimated 60%, making this sector the innovation and volume leader. Packaging in this category must not only protect formulations from contamination, oxidation, and moisture loss but also serve as a key brand differentiator in an image-driven market. Airless tubes, premium finishes (such as matte, metallic, or soft-touch), and tubes with high PCR content are gaining traction as consumers increasingly demand sustainable and luxury-oriented packaging formats. From mass-market toothpaste and shampoos to high-end skincare serums, tube packaging enables precise dispensing, portability, and strong shelf appeal. This segment’s dominance reflects the global expansion of beauty and personal care consumption, particularly in emerging markets where rising disposable incomes are fueling premiumization, further solidifying tube packaging’s role as the preferred format in this industry.

European Union: PPWR Regulations and Sustainable Tube Packaging Innovation

The European tube packaging market is undergoing major transformation under the Packaging and Packaging Waste Regulation (PPWR), effective from February 2025. The regulation requires manufacturers to use recycled content and recyclable mono-material tubes, accelerating investment in new machinery that can process these materials. Complementing this is the Ecodesign for Sustainable Products Regulation (ESPR), which drives innovations in refillable systems and compostable tube solutions. Programs like Horizon Europe are channeling significant R&D funding toward bio-based and compostable alternatives, including starch blends and cellulose films, further expanding the material base for sustainable tube packaging.

Leading companies such as Albéa are spearheading the shift with Greenleaf and Greenleaf 2 tube technologies, both recognized by the Association of Plastic Recyclers (APR) as recycling-ready within the HDPE rigid stream. Regulatory oversight by the European Chemicals Agency (ECHA) ensures that materials meet stringent health and safety standards, supporting safe adoption in cosmetics, pharmaceuticals, and food sectors. The planned Digital Product Passport will further reshape packaging by mandating traceability and transparency, embedding QR codes and digital identifiers into tube designs. Innovations such as Mondi’s sustainable pouch (March 2024) demonstrate how viscous-liquid packaging technologies can be adapted for tube-like applications, reinforcing Europe’s leadership in sustainable tube packaging.

United States: FDA Regulations, Sustainable Materials, and E-commerce Growth

In the United States, the tube packaging market is shaped by a mix of FDA regulations for food safety and medical devices, and the U.S. Environmental Protection Agency (EPA)’s push toward ambitious recycling targets. These policies are driving investments in recyclable mono-material solutions, post-consumer recycled (PCR) resins, and compostable tube designs. With the rapid growth of e-commerce and direct-to-consumer channels, demand is rising for lightweight, space-efficient, and tamper-resistant tube packaging that can withstand shipping challenges while ensuring sustainability.

Industry leaders are responding with innovation. In July 2023, Albéa Group introduced its Timeless PCR PBL tubes, which are APR-approved and recycling-ready in the HDPE rigid stream. Organizations like the Sustainable Packaging Coalition (SPC) are influencing packaging strategies by promoting closed-loop systems and recyclable material adoption. Simultaneously, manufacturers are investing in automation and digital printing technologies to produce tubes that meet clean-label consumer expectations while offering high-quality graphics and branding. With strong momentum from both regulatory enforcement and market trends, the U.S. is emerging as a global leader in sustainable, smart, and e-commerce-ready tube packaging solutions.

India: Extended Producer Responsibility and Eco-Friendly Tube Packaging Innovation

The India tube packaging market is experiencing rapid regulatory-driven transformation following the Plastic Waste Management (Amendment) Rules, 2024, effective April 1, 2025, which emphasize Extended Producer Responsibility (EPR). From July 2025, all plastic packaging must be traceable via barcodes or QR codes, reinforcing accountability across the supply chain. The Food Safety and Standards Authority of India (FSSAI) has also initiated consultations on sustainable packaging, particularly the integration of recycled PET (rPET), aligning domestic practices with global safety standards.

Leading companies are at the forefront of innovation. EPL Limited (formerly Essel Propack) and UFlex are investing in eco-friendly tube solutions, such as food-grade USFDA-approved rPET tubes and KRAFTIKA eco-tubes (launched November 2024), which reduce tube body weight by up to 45% using virgin kraft paper. These innovations highlight India’s strong focus on reducing material intensity while ensuring functionality. Coupled with rapid growth in e-commerce and personal care consumption, India is emerging as a significant hub for eco-conscious and technologically advanced tube packaging solutions.

China: Green Policy Enforcement and High-End Tube Packaging Demand

China’s tube packaging market is strongly influenced by the government’s “14th Five-Year” plan, which mandates eco-friendly and reusable packaging solutions across sectors, with enforcement starting in June 2025 for express delivery companies. This regulatory framework is driving adoption of sustainable tube materials for both consumer goods and e-commerce packaging. Tax incentives for companies investing in green technology and remanufacturing are further accelerating adoption of recyclable and compostable tube solutions.

A key trend in China is the rising demand for premium, high-barrier tube packaging that addresses both food safety and counterfeiting concerns. The State Administration for Market Regulation (SAMR) introduced GB 4806.1 standards that incorporate the concept of a “complete barrier”, ensuring robust protection for food and pharmaceutical applications. This, combined with consumer demand for premium cosmetic and personal care packaging, is pushing manufacturers to adopt advanced multilayer barrier tubes with enhanced security features. China is rapidly becoming a leader in producing high-performance tube packaging for both domestic and export markets.

Japan: Plastic Resource Circulation Policies Driving Tube Packaging Transition

The Japan tube packaging market is shaped by stringent sustainability frameworks, notably the Plastic Resource Circulation Strategy (2025) and the Plastic Resource Circulation Promotion Law (2025), which mandate a shift from single-use plastics to reusable and compostable alternatives. These laws directly impact the tube packaging industry, compelling companies to adopt paper-based, recyclable, and bio-based tube materials.

Additionally, the Ministry of Health, Labor and Welfare (MHLW) has implemented a positive list system for synthetic food packaging materials (June 2025), setting clear safety standards for food-contact applications. Japanese manufacturers are leveraging their expertise in precision manufacturing to produce tubes that balance sustainability with performance, including high-barrier, recyclable formats. This regulatory push, coupled with the country’s strong demand for cosmetic, pharmaceutical, and food packaging, is establishing Japan as a global leader in eco-friendly tube packaging innovation.

Brazil: Reverse Logistics and Waste Management Shaping Tube Packaging Market

The Brazil tube packaging market is evolving under the country’s National Solid Waste Policy (PNRS), which mandates sustainable waste disposal and recycling practices. The introduction of Law No. 15,088 (January 2025), which bans the import of solid waste, has heightened the focus on domestic recycling and sustainable material development. These policies are creating strong demand for eco-friendly tube packaging solutions, especially in the personal care and food sectors.

Brazil is also investing heavily in reverse logistics systems, making producers accountable for the collection and recycling of post-consumer packaging. With a growing emphasis on sustainable, recyclable, and compostable tubes, international and local players are expanding their presence to meet demand. The country’s abundant raw materials, coupled with policy-driven sustainability initiatives, are positioning Brazil as a key market for green innovation in tube packaging.

Tube Packaging Market Report Scope

Tube Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.3 Billion

|

|

Market Size (2034)

|

$27.4 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Material (Laminated Tubes, Plastic Tubes, Aluminum Tubes, Paper-based Tubes), By Product Type (Squeeze Tubes, Twist-up Tubes, Collapsible Tubes, Cartridge Tubes, Stick Tubes, Airless Tubes), By Application (Cosmetics & Personal Care, Pharmaceuticals & Healthcare, Food & Beverages, Household & Industrial, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Albéa, Amcor plc, EPL Limited (formerly Essel Propack Ltd.), Huhtamaki Oyj, CCL Industries Inc., Hoffmann Neopac AG, Mondi Group, Sonoco Products Company, Montebello Packaging, ALLTUB Group, LINHARDT GmbH & Co KG, Unette Corporation, Berry Global, Inc., CTLpack, Kuraray Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tube Packaging Market Segmentation

By Material

- Laminated Tubes

- Plastic Tubes

- Aluminum Tubes

- Paper-based Tubes

By Product Type

- Squeeze Tubes

- Twist-up Tubes

- Collapsible Tubes

- Cartridge Tubes

- Stick Tubes

- Airless Tubes

By Application

- Cosmetics & Personal Care

- Pharmaceuticals & Healthcare

- Food & Beverages

- Household & Industrial

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Tube Packaging Market

- Albéa

- Amcor plc

- EPL Limited (formerly Essel Propack Ltd.)

- Huhtamaki Oyj

- CCL Industries Inc.

- Hoffmann Neopac AG

- Mondi Group

- Sonoco Products Company

- Montebello Packaging

- ALLTUB Group

- LINHARDT GmbH & Co KG

- Unette Corporation

- Berry Global, Inc.

- CTLpack

- Kuraray Co., Ltd.

* List Not Exhaustive

Methodology

USDAnalytics applies a comprehensive, multi-layered research methodology to analyze the global tube packaging market, combining primary interviews with manufacturers, brand owners, co-packers, and regulatory authorities, alongside secondary research from company reports, academic studies, and industry publications. Our approach evaluates market dynamics such as sustainability-driven innovations, mono-material and refillable tubes, advanced digital printing, anti-counterfeiting features, premiumization, and e-commerce optimization. USDAnalytics incorporates detailed market sizing, CAGR projections, and segmentation by material, product type, application, and end-use industries, with regional analysis spanning North America, Europe, Asia-Pacific, India, China, Japan, and Brazil. The methodology also factors in regulatory influences, environmental compliance, and technological adoption—including antimicrobial films, high-barrier laminates, and precision dosing solutions—providing actionable insights for industry professionals, investors, and packaging solution providers seeking growth opportunities in high-performance, sustainable, and innovative tube packaging systems.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.