Ultra-High Molecular Weight Polyethylene Fibers Market Overview: Strength-to-Weight Leadership in Ballistics and Marine Ropes

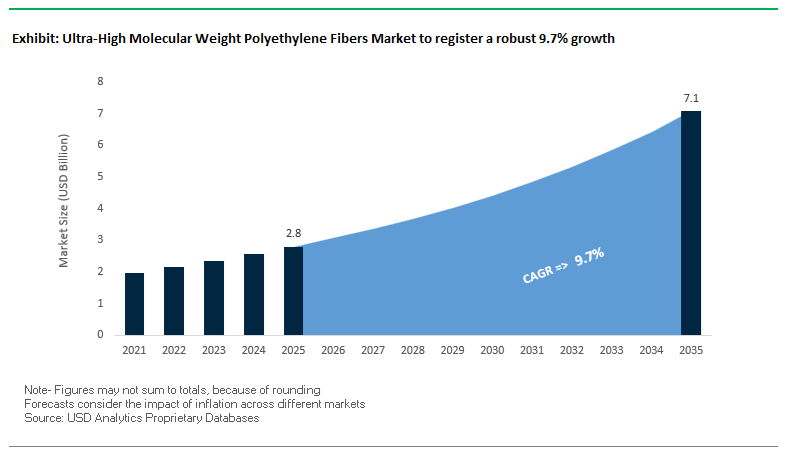

The Ultra-high Molecular Weight Polyethylene (UHMWPE) Fibers Market is projected to grow from USD 2.8 billion in 2025 to around USD 7.1 billion by 2035, registering a robust CAGR of 9.7% (2025–2035). This growth is underpinned by the fiber’s unmatched strength-to-weight ratio, exceptional chemical resistance, and buoyancy advantages that make it a preferred material for ballistic protection, marine mooring lines, offshore rigging, aquaculture netting, industrial lifting slings, and high-performance ropes. For manufacturers and vendors, UHMWPE (also referred to as High Modulus Polyethylene, HMPE) remains the strategic material platform for next-generation defense armor systems, deepwater offshore solutions, and ultra-light industrial textiles.

On a weight-for-weight basis, UHMWPE fibers are up to 15 times stronger than high-grade steel and approximately 40% stronger than aramid fibers, which cements their role in lightweight ballistic vests, helmets, vehicle armor and high-performance tethers. Their specific gravity of around 0.97–0.98 g/cm³ ensures neutral or positive buoyancy, enabling floating ropes and lines that are safer and easier to handle in marine environments. In dynamic applications, gel-spun UHMWPE fibers exhibit superior flex fatigue and bending life compared with aramids, making them the material of choice for winch lines, crane ropes and cyclically loaded offshore mooring systems. At the same time, unidirectional UHMWPE ballistic composites deliver up to 20% higher V50 values (projectile resistance) versus equivalent aramid composites at the same areal density, giving armor OEMs more performance headroom or weight reduction leverage.

From a durability standpoint, UHMWPE’s chemical inertness and UV resistance support long life in harsh industrial and marine environments, including exposure to seawater, hydraulic fluids and even 50% sulfuric acid with near 100% strength retention over prolonged service. For vendors, this combination of mechanical performance, durability and low density is driving steady substitution of conventional steel wire and aramid solutions in defense, offshore energy, aquaculture, industrial PPE, and high-performance sports gear.

Key technical and commercial insights for UHMWPE fiber stakeholders include:

- Specific tensile strength benchmark: UHMWPE fibers (HMPE) deliver the highest strength-to-weight ratio of any commercial fiber, up to 15× stronger than high-grade steel and about 40% stronger than aramid fibers, making them the reference material for lightweight ballistic protection and high-load ropes.

- Density and buoyancy advantage: With a specific gravity of 0.97–0.98 g/cm³, UHMWPE fibers float in water, which is critical for offshore mooring lines, marine towing ropes, aquaculture netting and rescue lines where flotation and low weight improve safety and handling.

- Flex fatigue and bending life: Gel-spun UHMWPE fibers maintain structural integrity and working load after extensive bending over sheaves and pulleys, outperforming aramids in flex fatigue and internal abrasion resistance and extending service intervals for dynamic lifting and hoisting systems.

- Ballistic energy absorption: Unidirectional UHMWPE composites typically achieve V50 values up to 20% higher than comparable aramid-based armor at the same areal density, enabling lighter vests, helmets and vehicle armor without compromising protection.

- Chemical and UV resistance: UHMWPE fibers remain highly chemically inert, retaining nearly 100% of their strength after prolonged exposure to seawater, hydraulic fluids and 50% sulfuric acid, making them ideal for cut-resistant gloves, chemical plant ropes and offshore rigging in highly aggressive environments.

Ultra-High Molecular Weight Polyethylene Fibers Market Analysis: Bio-Based Innovation, Defense Contracts and Maritime Expansion

Recent developments in the UHMWPE fibers industry highlight an increasingly technology- and sustainability-driven growth trajectory across defense, marine, industrial and medical applications. In March 2025, Avient Corporation (Dyneema) launched its bio-based Dyneema® fiber portfolio, using renewable feedstocks while retaining identical mechanical performance. This move, certified under ISCC sustainability standards, positions UHMWPE as a key material for low-carbon ballistic armor, lightweight ropes and performance textiles, and gives OEMs and brands a powerful lever to meet ESG and Scope 3 emission targets. Earlier, in January 2025, a major Asian UHMWPE producer completed a new gel-spinning facility in China with a capacity of 500 tonnes per year aimed at high-tenacity UHMWPE yarns for cut-resistant textiles and fishing lines, reinforcing Asia-Pacific’s role as a high-volume manufacturing hub for protective apparel and marine applications.

The innovation pipeline is also targeting traditional limitations of UHMWPE, particularly its thermal performance ceiling. In November 2024, academic studies reported a coating technology that raises the usable thermal limit of UHMWPE fibers from around 130°C to approximately 160°C, opening new opportunities in moderate-temperature industrial and automotive environments where prior heat limitations restricted adoption. On the defense and security front, demand visibility was strengthened in June 2025, when Honeywell International secured a multi-year defense contract exceeding USD 75 million to supply Spectra Shield® ballistic composites to a NATO ally for personnel armor upgrades and vehicle spall liners. This underscores the continued preference for UHMWPE-based ballistic systems in national defense modernization programs and cements UHMWPE’s status as a strategic material in the global body armor and vehicle protection market.

Medtech and deepwater offshore segments are further broadening the demand base for ultra-high molecular weight polyethylene fibers. In February 2024, DSM-Firmenich Biomedical introduced Ulteeva Purity™ fiber (formerly Dyneema Purity®) in an ultra-fine 10 dtex filament count, enabling its use in minimally invasive surgical applications such as sutures and catheter reinforcement, where ultra-low profile, biocompatibility and high tensile strength are mandatory. In Q3 2024, a leading offshore energy company partnered with a specialist UHMWPE rope manufacturer to develop next-generation deepwater mooring lines capable of operating at depths greater than 3,000 meters with a 25% reduction in diameter compared with equivalent steel wire, directly leveraging UHMWPE’s buoyancy, strength and fatigue performance. Regulatory and policy tailwinds are also emerging: in December 2025, the International Maritime Organization (IMO) advanced its rope safety guidelines for towing and mooring, which indirectly favor UHMWPE ropes due to their lower recoil energy on break, enhancing safety in ports and offshore operations. Complementing this, in April 2025, a private equity firm invested USD 20 million into an emerging Korean UHMWPE producer focused on UV-stabilized yarns for aquaculture and industrial netting, highlighting investor confidence in APAC capacity expansion and blue-economy demand growth.

Acceleration of Offshore Mooring Adoption, Hybrid Ballistic Fabrics, Surface-Modified UHMWPE for Composites, and Biomedical-Grade Lightweight Implants

Market Trend 1: Offshore Sector Expansion Driving Large-Scale UHMWPE Fiber Adoption in Deep-Water Mooring and Dynamic Cabling Systems

A defining trend in the UHMWPE fibers market is the rapid expansion of offshore infrastructure—deep-water oil & gas platforms, floating wind turbines, and subsea dynamic cables—requiring ultra-lightweight, ultra-high-strength synthetic ropes. UHMWPE’s extraordinary specific strength, which is 7–15 times higher than steel wire on a weight basis, makes it the benchmark material for next-generation deep-water mooring systems. Equally critical is its relative density of ~0.97 g/cm³, enabling UHMWPE ropes to float—reducing load on mooring systems by as much as 700% versus steel chains.

The marine environment imposes extreme cyclic loading: UHMWPE excels with relaxation fatigue strength up to 1,000× better than steel cable, and rope designs capable of 100,000 cycles at 40–50% load with no loss in breaking strength. These properties are essential for floating production systems and high-motion offshore wind platforms. Large-diameter UHMWPE mooring ropes are now engineered to achieve Minimum Breaking Loads (MBL) ≥10,000 kN, enabling longer lifespans, easier installation, and significantly lower maintenance compared to steel alternatives. This trend is accelerating as deep-water exploration moves further from shore and floating wind deployments scale globally.

Market Trend 2: Rapid Innovation in Hybrid UHMWPE Ballistic Fabrics for Lightweight Armor and Smart Protective Systems

Another major trend influencing the UHMWPE fibers market is the shift toward lightweight hybrid ballistic solutions in defense, law enforcement, and personal protection. UHMWPE laminates offer up to 50% weight reduction compared to steel plates while maintaining comparable ballistic resistance—an enormous advantage for soldier mobility, stab-proof vests, and high-performance helmets.

Hybrid armor systems combining UHMWPE with next-generation aramid fabrics exhibit significant ballistic performance improvements, with Ballistic Limit Velocity (V50/Vbl) increased by 25.6%–40.4% compared to pure UHMWPE laminates. These improvements are especially critical under high-temperature impact scenarios and against pointed or non-blunt projectiles. UHMWPE’s intrinsic high energy absorption and low back-face deformation further contribute to advanced protection requirements.

A new frontier is emerging with conductive and functionalized hybrid fabrics. For example, aramid textiles coated with graphene oxide (GO) have shown up to 50% higher resistive force, enabling integrated sensing networks, situational awareness systems, and connected smart armor. This trend is aligned with military modernization programs that require both ballistic protection and electronic integration in a single textile architecture.

Market Opportunity 1: High-Adhesion, Surface-Modified UHMWPE Fibers Unlocking Advanced Composite Performance

One of the most transformative opportunities for the UHMWPE fibers market lies in overcoming the material’s natural chemical inertness through surface modification, enabling its integration into high-value structural composites. Traditional UHMWPE suffers from poor matrix adhesion, but plasma-modified and chemically functionalized UHMWPE fibers have demonstrated extraordinary improvements.

Plasma treatments (e.g., Ar–O₂ plasma) can raise Interfacial Shear Strength (IFSS) by 143%–181%, while MWCNT–GMA grafting techniques achieve increases up to 336%. Such enhancements shift the failure mode from interfacial debonding to fiber defibrillation or cohesive matrix failure, allowing the composite to harness the fiber’s full tensile capability.

Surface treatments introduce polar functional groups that improve wettability and hydrophilicity, allowing UHMWPE to bond effectively with epoxy, polyurethane, and other polymer matrices. This unlocks new markets in lightweight automotive structures, aerospace panels, sports equipment, and industrial load-bearing components—areas where high toughness, low weight, and corrosion resistance are mission-critical.

Market Opportunity 2: UHMWPE Fiber Integration in Lightweight, High-Strength Medical Implants and Surgical Devices

The biomedical sector presents another high-growth opportunity for UHMWPE fibers, driven by the need for lightweight, high-strength, biocompatible implant materials. UHMWPE is already the gold standard for orthopedic bearings, and highly cross-linked UHMWPE reduces wear rates by up to 90% in hip and knee joints—demonstrating exceptional long-term biological performance.

When engineered into fiber-reinforced composite implants, UHMWPE offers a high specific strength that significantly reduces implant weight, improving patient comfort and mobility. Its mechanical tuneability allows implants to be manufactured with a Young’s Modulus aligned with natural bone (7–20 GPa), preventing stress shielding and facilitating better bone regeneration. This is a major advantage over titanium, which has a stiffness of ~110 GPa and often causes long-term compatibility issues.

Applications include spinal cages, cranial plates, trauma fixation devices, sutures, and high-strength surgical textiles. As orthopedic and trauma care shifts toward minimally invasive, load-sharing, and patient-centric implant designs, UHMWPE fiber composites represent a next-generation solution for durable, lightweight medical devices.

Ultra-high Molecular Weight Polyethylene Fibers Market Share Analysis

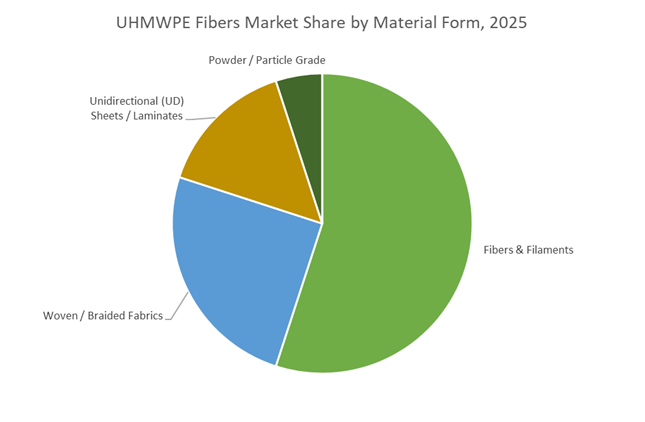

Market Share by Material Form: Fibers & Filaments Dominate Due to Critical Role in High-Strength, High-Value Applications

Fibers & Filaments account for the largest share of the global UHMWPE fibers market—approximately 55%—because this material form fully leverages the polymer’s hallmark characteristics: exceptional tensile strength, ultra-low density, and outstanding energy absorption. UHMWPE fibers, produced through advanced gel-spinning technology, achieve extreme molecular chain alignment, enabling tensile strengths more than 15× higher than steel by weight. This performance profile makes fibers and filaments the essential base form for virtually all high-value UHMWPE applications, including ballistic composites, cut-resistant textiles, offshore mooring ropes, and deep-water lifting lines. These fibers serve as the direct feedstock for unidirectional (UD) laminates used in body armor and vehicle protection systems, as well as high-strength braided ropes that replace steel cables in marine, aerospace, and industrial lifting operations. Moreover, the fiber segment commands premium pricing due to stringent purity, alignment, and quality requirements demanded by defense, marine, and medical industries, reinforcing its position as the revenue-leading material form. As global demand intensifies for high-performance lightweight materials in protective gear, military systems, and renewable offshore energy infrastructure, the Fibers & Filaments category continues to consolidate its share as the technological and commercial backbone of the UHMWPE market.

Market Share By End-Use Industry: Defense & Security Leads Driven by Ballistic Protection and Global Military Modernization

The Defense & Security sector represents the largest end-use share of the UHMWPE fibers market—approximately 45%—as the material has become indispensable for next-generation ballistic protection systems. Its unmatched strength-to-weight ratio and exceptional impact resistance make UHMWPE the preferred material for lightweight body armor, tactical helmets, ballistic shields, and composite vehicle armor panels. Defense agencies worldwide increasingly rely on UHMWPE-based unidirectional laminates for NIJ-certified body armor capable of multi-hit protection while significantly reducing soldier load, thereby enhancing mobility, endurance, and mission effectiveness. Military modernization programs in the U.S., Europe, India, and Asia-Pacific continue to prioritize advanced soldier protection systems, fueling sustained procurement of UHMWPE-based armor solutions. Beyond personal protective equipment, UHMWPE fibers are critical in naval and aerospace defense platforms for lightweight tow lines, parachute systems, and impact-resistant structural components. Reports consistently show that 29%–42% of all UHMWPE fiber consumption is tied directly to ballistic and protective applications, underlining that defense procurement cycles, rising geopolitical tensions, and increasing investment in soldier survivability are structurally reinforcing the Defense & Security segment’s market leadership.

Country Analysis: Global UHMWPE Fiber Hotspots and Strategic Material Advancements

United States: Defense Modernization and Aerospace-Grade UHMWPE Composites Accelerating High-Value Adoption

The United States remains one of the most strategically important markets for Ultra-high Molecular Weight Polyethylene (UHMWPE) fibers, led by substantial defense procurement cycles and the integration of advanced lightweight composites across personal protection and aerospace platforms. In 2025, U.S. military and law enforcement agencies accelerated adoption of Dyneema® HB330/HB332 hard armor grades and SB301 soft armor substrates, enabling Level III rifle plates to drop below 2.0 pounds while reducing body armor panel weight by 10–20% without requiring retooling. This material transition underscores how UHMWPE’s exceptional tensile strength, low density, and superior energy absorption characteristics are transforming next-generation soldier protection systems.

In parallel, Honeywell’s Spectra® fiber and Spectra® Shield composites continue to play a critical role in strategic defense applications due to their up to 40% higher specific strength than aramid fibers, combined with outstanding chemical and environmental resistance. U.S. aerospace companies—including Boeing and Lockheed Martin—are increasingly integrating UHMWPE fiber-reinforced composites into structural reinforcement components to improve fuel efficiency, weight reduction, and impact resistance. This dual-domain penetration (armor and aerospace) positions the U.S. as a hotbed for advanced composite innovation, with UHMWPE serving as a core material enabling modern lightweighting, ballistic protection, and high-performance engineering.

Netherlands / European Union: Bio-Based UHMWPE Transition and Biomedical-Grade Fiber Leadership

The Netherlands and broader European Union remain global leaders in sustainable UHMWPE fiber development, owing largely to the region's regulatory emphasis on environmental performance and the technological leadership of dsm-firmenich, the producer of Dyneema. In 2024, the company introduced a bio-based version of its Ulteeva Purity™ (formerly Dyneema Purity®) medical-grade UHMWPE fiber, derived from ISCC-certified renewable feedstocks. This marks a pivotal industry milestone, aligning UHMWPE with the EU’s circular materials agenda while simultaneously expanding its role in orthopedic and cardiovascular devices, where superior wear resistance, biocompatibility, and fatigue strength are critical.

European biomedical firms continue pioneering enhancements through irradiation and crosslinking techniques, allowing UHMWPE to achieve exceptional tribological performance in knee and hip implants. Meanwhile, regulatory bodies across the EU are driving development of hybrid ballistic solutions blending UHMWPE with aramid fibers to meet stringent fire, heat, and occupational safety standards. This positions Europe not only as the hub for sustainable UHMWPE production but also as a key market for high-end protective equipment and precision biomedical applications.

China: National-Scale Capacity Expansion and Strategic UHMWPE Industrialization

China is rapidly scaling its domestic UHMWPE fiber industry, driven by national priorities for self-sufficiency in advanced materials supporting defense, maritime, and industrial sectors. Government policy continues to channel investment into leading manufacturers such as Shanghai Lianle and Zhongke Xinxing, enabling expansion of second-generation and industrial UHMWPE fiber capacity. This scaling initiative ensures China can supply significant portions of its own demand for ballistic protection, aerospace components, and high-strength industrial textiles.

China’s maritime and fishing industries remain major consumers of UHMWPE ropes and nets, capitalizing on the fiber’s low water absorption, buoyancy, UV stability, and abrasion resistance, which outperform traditional nylon and polyester systems. With continuous industrial expansion and high-volume application demand, China is rapidly emerging not just as a manufacturing giant but as a long-term strategic competitor in the global UHMWPE fiber supply chain.

Japan: Precision Gel-Spinning and Biomedical-Grade UHMWPE for High-Performance Applications

Japan continues to reinforce its leadership in polymer precision manufacturing, driving advanced UHMWPE fiber development for high-value sectors such as medical components, heavy-duty industrial systems, and extreme-environment ropes and nets. Companies like Asahi Kasei Advance Corporation maintain strong market presence with premium UHMWPE forms—including rods, sheets, and tubes—engineered for applications requiring exceptional wear resistance, dimensional stability, and chemical inertness.

Japan’s academic and industrial polymer science ecosystem is also advancing innovation in gel-spinning techniques, achieving higher crystallinity and molecular alignment to produce UHMWPE fibers with tensile properties surpassing current commercial benchmarks. These breakthroughs position Japan at the frontier of next-generation UHMWPE technology, enabling its application in severe-environment offshore ropes, precision industrial parts, and biomedical-grade materials used in long-service-life implants.

India: Defense Infrastructure Modernization Driving Demand for Ballistic-Grade UHMWPE Fibers

India’s UHMWPE fiber demand is rising sharply as national defense spending continues to expand, particularly across ballistic helmets, tactical vests, and lightweight armor plates. Domestic manufacturers such as MKU and SMPP are increasingly integrating imported and locally processed UHMWPE fibers into NIJ-compliant ballistic protection systems to support India’s modernization and indigenization objectives under the “Make in India” program.

In parallel, India’s industrial and transportation sectors are adopting UHMWPE composites for lightweight reinforcement, high-strength ropes, and protective textiles, reflecting the country’s broader shift toward advanced materials in defense manufacturing, aerospace, and high-performance infrastructure development. As domestic fiber processing capacity grows, India is poised to become a significant regional consumer and potential future manufacturer of ballistic-grade UHMWPE composites.

South Korea: UHMWPE Composite Integration for Automotive Lightweighting and Advanced Industrial Engineering

South Korea is rapidly expanding its footprint in UHMWPE fiber applications, particularly within the automotive industry, where lightweighting is a top priority for electric vehicle (EV) efficiency. Korean automakers are exploring UHMWPE composites to replace heavier metal components in interior structures, energy-absorbing panels, and protective reinforcements, leveraging the fiber’s high strength-to-weight ratio and impact tolerance.

In addition to automotive innovations, South Korean industrial R&D programs are deploying UHMWPE fibers in thermal management systems, industrial ropes, robotics components, and anti-corrosion reinforcements, reflecting the country’s commitment to advanced materials engineering. This diversification places South Korea among the emerging high-technology adopters of UHMWPE across both mobility and industrial sectors.

Ultra-High Molecular Weight Polyethylene Fibers Competitive Landscape: Dyneema, Spectra and Global HMPE Leaders

The competitive landscape of the UHMWPE fibers market is highly consolidated at the top end, with a handful of global technology leaders controlling proprietary gel-spinning processes, resin platforms and ballistic composite technologies. Avient (Dyneema) and Honeywell (Spectra) dominate the premium ballistic and maritime segments, while Mitsui Chemicals, Toyobo and Celanese anchor the upstream and regional supply of resins, sheet, and high-strength fibers for industrial, medical and marine use. Strategically, leading players are differentiating through bio-based product lines, ballistic systems integration, medical-grade purity, and region-specific rope and netting solutions, alongside capacity expansions in Asia-Pacific and increased focus on sustainability and regulatory compliance (e.g., IMO safety guidelines). For market entrants and buyers, understanding the interplay between branded fiber platforms (Dyneema®, Spectra®, Izanas®, GUR®) and their target applications is essential to assess supply security, performance guarantees and long-term cost of ownership.

Avient Corporation scales Dyneema UHMWPE fibers for sustainable high-performance protection

Avient Corporation, steward of the Dyneema® brand, remains the global reference player in UHMWPE fibers, with a portfolio that includes Dyneema SK78, SK99, DM20 grades, Dyneema® Composite Fabrics (DCF) and medical-grade Ulteeva Purity™ fibers. The company’s core strength lies in its proprietary gel-spinning technology, which enables extremely high molecular orientation and, therefore, world-leading strength-to-weight performance in ropes, soft armor, helmets and performance gear. Strategically, Avient is positioning Dyneema as both a performance and sustainability benchmark, highlighted by the March 2025 launch of bio-based Dyneema fibers, which maintain identical mechanical properties while leveraging renewable feedstocks under ISCC certification. This move allows OEMs to reduce the carbon footprint of ballistic protection, offshore mooring lines and high-performance sports equipment without sacrificing safety or durability. The brand’s extensive penetration into maritime, defense, sports, and medical applications gives Avient a powerful advantage when negotiating long-term supply contracts and co-development programs with top-tier customers.

Honeywell International advances Spectra UHMWPE fibers for global defense and ballistic systems

Honeywell International is a leading player in UHMWPE fibers and ballistic systems through its Spectra® fibers (grades 900, 1000, 2000) and Spectra Shield® / Gold Shield® composite technologies. Its competitive edge comes from an integrated defense-focused strategy, where Honeywell not only supplies the fiber, but also engineers fully qualified ballistic panels for body armor, helmets and vehicle protection systems used by military and law enforcement agencies worldwide. In June 2025, the company secured a multi-year USD 75+ million defense contract to supply Spectra Shield® composites for a NATO ally’s personnel armor upgrades and spall liners, reinforcing its status as a trusted domestic supplier for Western defense programs. Honeywell’s UHMWPE technology is engineered for high energy absorption, superior flex fatigue performance, and low weight, which enable lighter, more comfortable protective gear with improved multi-hit capability. Its close alignment with defense procurement cycles and standards provides strong demand visibility and positions the company as a cornerstone supplier in the global ballistic armor value chain.

Mitsui Chemicals leverages Tekmilon UHMWPE for industrial and medical performance

Mitsui Chemicals, Inc. participates in the UHMWPE fibers and materials market through its Tekmilon® UHMWPE sheet and fiber products, as well as high-purity UHMWPE powders for medical and industrial applications. The company capitalizes on its broad polymer chemistry expertise to engineer resins with precisely controlled molecular weight distributions, tailored for applications ranging from industrial wear parts to orthopedic implants. In the medical space, Mitsui’s UHMWPE materials are used as standard-bearing bearing surfaces in artificial joints, where high purity, low wear and long-term biocompatibility are critical. Industrially, Tekmilon® products support high-strength ropes, nets and technical fabrics that exploit UHMWPE’s chemical resistance and low friction. The firm’s integration across petrochemicals, high-performance polymers and healthcare materials allows it to offer application-specific grades and to collaborate closely with OEMs on regulatory compliance and product validation, strengthening its competitive position in both Asia and global niche markets.

Toyobo scales Izanas UHMWPE fibers for Asian defense, fishing and industrial ropes

Toyobo Co., Ltd. is an important Asian competitor in UHMWPE fibers with its Izanas® high-strength polyethylene fiber platform, targeting fishing, security and industrial rope applications. The company’s strategy centers on scaling its proprietary Izanas® technology to capture rising regional demand in defense, commercial fishing, offshore energy and industrial lifting, particularly in Asia-Pacific markets. Toyobo’s fibers combine high tensile strength, low density and excellent fatigue resistance, enabling manufacturers to produce thinner, lighter lines and nets that maintain or exceed the performance of traditional steel wire or aramid-based systems. The company has reinforced its market position through a joint venture launched in 2022 to boost development, manufacturing and sales of functional materials, including high-performance fibers. This JV structure enhances Toyobo’s ability to co-develop application-specific UHMWPE solutions with regional partners, accelerate time-to-market, and tailor products to local regulatory and performance requirements.

Celanese Corporation underpins UHMWPE fiber production with GUR resin leadership

Celanese Corporation plays a critical upstream role in the UHMWPE fibers ecosystem through its GUR® UHMWPE resin portfolio (e.g., GUR 4150, GHR 8020 grades), which serves as the base polymer feedstock for many gel-spun UHMWPE fiber and sintered product manufacturers. The company’s competitive strength lies in its ability to deliver extremely high-purity, consistent UHMWPE powders, a prerequisite for achieving reliable mechanical performance and processability in spinning and molding operations. Celanese operates a world-class GUR® production facility in Nanjing, China, providing a strategically located supply base for the growing Asia-Pacific UHMWPE processing industry, including rope, fiber, filtration and medical implant manufacturers. By focusing on tight molecular weight control, low contaminant levels and robust quality systems, Celanese reduces variability for downstream fiber producers, helping them optimize drawing conditions, tensile strength, and long-term performance. Its role as a trusted raw material supplier anchors many of the global UHMWPE value chains, giving it strong leverage and long-term partnerships with leading fiber brands and processors.

Ultra-High Molecular Weight Polyethylene Fibers Market Report Scope

Ultra-High Molecular Weight Polyethylene Fibers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2035)

|

$7.1 Billion

|

|

Market Growth Rate

|

9.7%

|

|

Segments

|

By Material Form (Fibers & Filaments, Unidirectional Sheets/Laminates, Woven/Braided Fabrics, Powder/Particle Grade), By End-Use Application (Defense & Security, Medical & Orthopedics, Marine & Offshore, Industrial, Sports & Consumer Goods), By Polymer Type (Gel-Spun UHMWPE, Sintered/Ram-Extruded UHMWPE)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

dsm-firmenich (Dyneema), Honeywell (Spectra), Celanese (GUR), Asahi Kasei, Mitsui Chemicals, Braskem, LyondellBasell, Shanghai Lianle, KPIC, Zhongke Xinxing, Sinopec Yanshan, Teijin, DSM Biomedical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ultra-High Molecular Weight Polyethylene (UHMWPE) Fibers Market Segmentation

By Material Form

- Fibers & Filaments

- Unidirectional (UD) Sheets / Laminates

- Woven / Braided Fabrics

- Powder / Particle Grade

By End-Use Industry

- Defense & Security

- Medical & Orthopedics

- Marine & Offshore

- Industrial

- Sports & Consumer Goods

By Polymer Type

- Gel-Spun UHMWPE

- Sintered / Ram-Extruded UHMWPE

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Ultra-High Molecular Weight Polyethylene (UHMWPE) Fibers Market

- dsm-firmenich (Dyneema)

- Honeywell (Spectra)

- Celanese (GUR)

- Asahi Kasei

- Mitsui Chemicals

- Braskem

- LyondellBasell

- Shanghai Lianle

- KPIC

- Zhongke Xinxing

- Sinopec Yanshan

- Teijin

- DSM Biomedical

*- List not Exhaustive