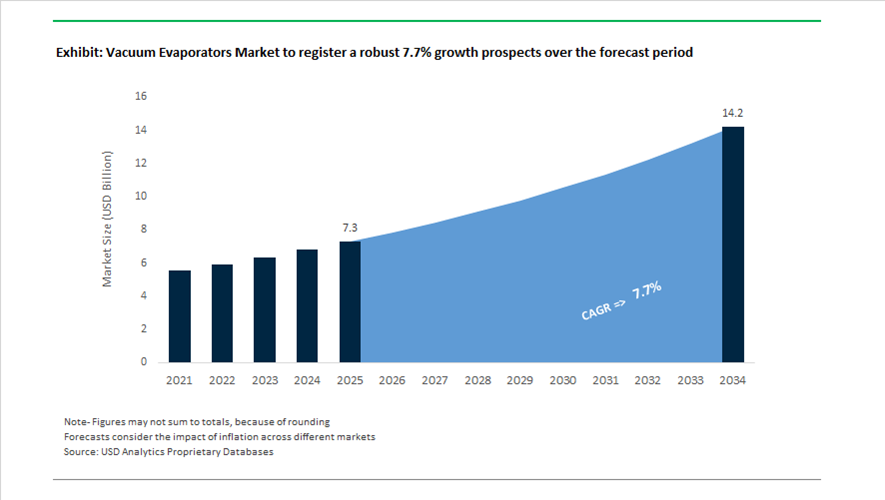

Vacuum Evaporators Market Overview 2025–2034: $7.3 Billion to $14.2 Billion at 7.7% CAGR Powered by Industrial Wastewater Recovery, High-Purity Semiconductor Processing, and Lab Automation

The global Vacuum Evaporators market is valued at $7.3 billion in 2025 and is projected to reach $14.2 billion by 2034, expanding at a robust CAGR of 7.7%. Growth is being driven by rising demand for industrial wastewater evaporation systems, zero liquid discharge (ZLD) technologies, rotary evaporators for pharmaceutical labs, solvent recovery units, sludge concentration systems, and high-purity evaporation equipment for semiconductor and OLED manufacturing. Increasing environmental regulations, microelectronics water reuse mandates, and pharmaceutical R&D intensity are reinforcing the adoption of vacuum-based evaporation systems due to their energy efficiency, lower boiling point operation, and ability to preserve thermally sensitive compounds. Industrial decarbonization strategies and circular water management initiatives are accelerating deployment across energy, chemicals, municipal wastewater, and electronics fabrication sectors.

Strategic consolidation and infrastructure investments intensified between 2024 and 2026. In May 2025, Veolia signed an agreement to acquire CDPQ’s 30% stake in Veolia Water Technologies and Solutions for over $800 million, securing full ownership and enabling streamlined integration of its industrial evaporator portfolio within global wastewater treatment projects. In May 2025, Veolia also secured $750 million in flagship contracts across energy and semiconductor markets, deploying advanced evaporation systems designed for ultra-high-purity microelectronics processing. In January 2026, Suez was awarded a major sludge dewatering and evaporation contract for Asia’s largest sewage treatment facility in Hong Kong, establishing a benchmark for integrated liquid waste management. In October 2026, Suez and PYREG launched an integrated sludge dewatering and pyrocarbonisation platform engineered to operate alongside vacuum evaporation units, transforming sewage sludge into biochar and reinforcing circular economy water treatment models. In September 2025, TCL CSOT announced a $4.15 billion investment in its 8.6-generation OLED line in Guangzhou and issued a Letter of Intent for advanced OLED vacuum evaporation equipment, with delivery scheduled for 2026. These developments highlight expanding capital expenditure in high-precision evaporation technologies for both environmental infrastructure and advanced electronics manufacturing.

Laboratory-scale innovation and sustainability certifications are reshaping the research equipment segment. In April 2024, BÜCHI introduced the compact Rotavapor® R-80, targeting cost-sensitive laboratories requiring precision solvent evaporation. In October 2024, Organomation launched the S-EVAP+, a high-throughput vacuum evaporator designed for solvent recovery and environmental sample preparation. In February 2025, BÜCHI earned My Green Lab ACT® certification for its Lyovapor™ L-250 and Rotavapor® R-80 systems, validating energy and water efficiency credentials. In May 2025, BÜCHI acquired the NeoSpectra platform to integrate near-infrared spectroscopy into its evaporator ecosystem, enabling real-time material analysis during evaporation. In September 2025, BÜCHI expanded its portfolio with the Rotavapor® R-180 featuring automatic safety lifts and dedicated sample drying modes. In June 2025, Artisan Industries introduced the ROTOTHERM® MINI, a lab-scale continuous vacuum evaporator/dryer optimized for pharmaceutical and polymer pilot plants.

Trends and Opportunities in the Vacuum Evaporators Market

Regulatory Rescaling of ZLD Compliance and Operating Permits

Zero Liquid Discharge has transitioned from a voluntary environmental upgrade to a binding regulatory prerequisite across water-intensive industries, fundamentally reshaping demand for vacuum evaporators. In pharmaceuticals, specialty chemicals, textiles, and food processing, environmental authorities are now linking operating permits and capacity expansions directly to demonstrated ZLD capability. As a result, Mechanical Vapor Recompression vacuum evaporators are increasingly specified as core infrastructure rather than auxiliary wastewater equipment.

Technical assessments published in December 2025 indicate that advanced vacuum evaporation systems are enabling facilities to recover up to 97% of clean process water, materially reducing freshwater intake and eliminating discharge liabilities. This recovery rate is particularly critical in jurisdictions where non-compliance penalties now include production curtailment or permit revocation, effectively making ZLD a license to operate rather than a sustainability differentiator.

Energy efficiency has become the decisive selection criterion. Case studies released in 2025 by Condorchem and Myande Group demonstrate that modern vacuum evaporators can reduce liquid waste volume by 95 to 99% while consuming 30 to 60% less energy than atmospheric or multi-effect thermal evaporation. This performance directly supports Scope 2 emissions reduction strategies, allowing manufacturers to align regulatory compliance with corporate decarbonization targets without sacrificing throughput.

Coupling Crystallization for Critical Mineral and Lithium Recovery

The strategic importance of lithium and critical minerals is driving a new class of vacuum evaporator deployments focused on resource recovery rather than waste minimization alone. As battery supply chains diversify away from conventional hard-rock mining, unconventional sources such as geothermal brines and oilfield produced water are becoming central to new supply growth. By late 2025, industry projections indicate that more than 30% of incremental lithium supply will originate from these non-traditional streams.

Vacuum evaporators are being integrated with advanced crystallization and Direct Lithium Extraction processes to enable rapid concentration and selective precipitation of lithium salts. Startups and technology developers report that compact, modular vacuum systems operating under reduced pressure can achieve lithium recovery rates exceeding 95%, a step change compared to the 20 to 50% recovery typical of legacy solar evaporation ponds. This accelerated concentration not only improves yield but also compresses project timelines from years to months, a decisive advantage in fast-moving battery markets.

Purity control is another critical driver. Reduced-pressure operation at temperatures as low as 35 to 40 degrees Celsius prevents thermal degradation of heat-sensitive complexes, ensuring downstream lithium carbonate and hydroxide products consistently meet the 99.5% purity thresholds required for next-generation electric vehicle batteries. As refining standards tighten globally, vacuum evaporation is increasingly viewed as an enabling technology for battery-grade mineral compliance rather than a peripheral processing step.

Addressing the PFAS Forever Chemical Remediation Mandate

PFAS regulation has emerged as one of the most immediate growth catalysts for vacuum evaporators, particularly in municipal and industrial water treatment. The U.S. Environmental Protection Agency’s National Primary Drinking Water Regulation, enforced throughout 2025, established legally binding Maximum Contaminant Levels of just 4 parts per trillion for PFOA and PFOS. These ultra-low thresholds have forced utilities and industrial operators to deploy advanced separation technologies at unprecedented scale.

Vacuum evaporators are being positioned downstream of Reverse Osmosis and Ion Exchange systems to concentrate PFAS-laden brines into minimal volumes suitable for final destruction via high-temperature incineration or electrochemical oxidation. By concentrating contaminants rather than attempting complete removal in a single step, operators can reduce hazardous waste transport volumes dramatically. Engineering evaluations conducted in 2025 show that vacuum evaporation can cut the volume of PFAS waste requiring final treatment by up to 80%, materially lowering lifecycle remediation costs.

This demand is being amplified by public funding. Under the U.S. Bipartisan Infrastructure Law, significant federal and state resources are being allocated to PFAS remediation, accelerating public-private partnerships where vacuum evaporators serve as critical volume minimizers. In this context, evaporation technology is no longer competing on capital cost alone but on its ability to unlock access to regulatory funding and ensure long-term compliance certainty.

On-Site Solvent Recovery to De-Risk Industrial Supply Chains

Beyond wastewater, vacuum evaporators are gaining strategic importance in solvent recovery as manufacturers confront volatile raw material prices, tightening VOC regulations, and supply chain disruptions. Industries such as coatings, electronics, and pharmaceuticals are increasingly deploying on-site vacuum solvent recovery systems to reclaim high-value solvents including NMP, ethanol, and specialty alcohols.

Industrial benchmarking studies released in December 2025 indicate that on-site recovery systems can deliver payback periods of 12 to 24 months, driven by reductions of up to 50% in solvent procurement and hazardous waste disposal costs. These economics are particularly compelling in battery manufacturing and pharmaceutical synthesis, where solvent purity requirements are high and disposal costs are escalating rapidly under environmental regulations.

Strategic decarbonization further reinforces this opportunity. Pharmaceutical leaders such as Sanofi have publicly committed to circular economy roadmaps targeting 90% waste reuse or recovery by the end of 2025. In these net-zero-oriented facilities, vacuum evaporators enable the safe recovery of heat-sensitive solvents while significantly reducing emissions associated with off-site waste transport and incineration. As ESG metrics become embedded in investor and regulatory scrutiny, solvent recovery via vacuum evaporation is evolving from a cost-saving measure into a core pillar of industrial sustainability strategy.

Vacuum Evaporators Market Share and Segmentation Insights

Technology Market Share: Mechanical Vapor Recompression Leads with High Energy Efficiency and Cost Savings

Mechanical vapor recompression (MVR) holds a 38.60% share in the vacuum evaporators market in 2025, supported by its ability to significantly reduce energy consumption by reusing latent heat through vapor compression. This technology delivers substantial operating cost savings compared to conventional evaporation systems, making it highly attractive for large-scale industrial applications. Multiple effect evaporation, thermal vapor recompression, heat pump evaporation, low temperature evaporators, and vacuum crystallizers serve diverse process requirements. A key market driver is rising energy cost sensitivity, where advancements in compressor technology and digital process control enable efficient operation even in corrosive and high-fouling industrial environments.

End-Use Industry Market Share: Chemical and Petrochemical Sector Leads with ZLD and Process Optimization Demand

Chemical and petrochemical industries account for 28.40% of the vacuum evaporators market in 2025, driven by the need for concentration, solvent recovery, and wastewater treatment across complex processing operations. Food and beverage, pharmaceutical and biotechnology, mining and metallurgy, electronics, automotive, and textile sectors contribute additional demand. A key trend is the adoption of zero liquid discharge (ZLD) systems, where vacuum evaporators and crystallizers are integrated to recover water and eliminate wastewater discharge. This trend is gaining traction due to stringent environmental regulations and water scarcity concerns, positioning evaporator technologies as critical components in sustainable industrial processing systems.

Vacuum Evaporators Market Competitive Landscape

The Vacuum Evaporators market in 2026 is defined by resource recovery engineering, modular plug-and-play systems, and energy-efficient MVR technologies that enable recovery of APIs, solvents, and metals while reducing capital expenditure for Zero Liquid Discharge (ZLD) across pharmaceuticals, chemicals, and electronics manufacturing.

Veolia Water Technologies Leads MVR-Based Vacuum Evaporation with Integrated Circular Solutions

Veolia Water Technologies, through its Evaled® platform, is dominating the Vacuum Evaporators market with high-efficiency MVR systems designed for maximum water recovery and energy optimization. Its 2026 system launch targets chemical and pharmaceutical industries, delivering reduced energy consumption per cubic meter of distillate. Full acquisition of Water Technologies and Solutions for €900 million strengthens integration across evaporation and membrane systems, unlocking €90 million in synergies. Veolia secured over $750 million in flagship contracts across semiconductor and energy sectors, reflecting strong demand for ultra-low discharge solutions. The Evaled® RV and AC series enable in-line wastewater reuse within production cycles. This modular and integrated approach positions Veolia as a leader in circular water management.

GEA Group Advances Decarbonized Evaporation with eZero Systems and Digital Process Control

GEA Group AG is strengthening its position in the Vacuum Evaporators market through decarbonized evaporation technologies and integrated process solutions. The launch of the eZero Dairy Evaporator combines heat pump systems with multi-effect evaporation to significantly reduce carbon emissions in food processing. Its new U.S. Technology Center supports R&D in lithium-ion battery recycling, expanding applications into energy storage value chains. GEA’s digital process control systems leverage IoT sensors for predictive maintenance, reducing downtime by up to 15%. The company integrates evaporation with spray drying and crystallization to deliver complete resource recovery solutions. This system-level integration enhances efficiency across pharmaceutical and chemical manufacturing processes.

SUEZ Expands Smart Maintenance and Industrial Wastewater Recovery in Asia

SUEZ is advancing in the Vacuum Evaporators market through smart maintenance technologies and large-scale wastewater infrastructure projects. Its Smart Glasses platform enables remote technical support, addressing skilled labor shortages in complex evaporation system maintenance. The Hong Kong Sha Tin Caverns project demonstrates SUEZ’s capability in delivering compact, high-capacity evaporation systems for urban wastewater treatment. Investment in a solvent recycling facility in Chongqing supports processing of 30,000 tonnes of hazardous waste annually using vacuum distillation. The company’s partnership with INRAE focuses on resource recovery innovations such as vacuum-assisted pyrolysis for sludge valorization. This combination of digital service models and infrastructure expansion strengthens SUEZ’s regional leadership.

H2O GmbH Delivers High-Efficiency Modular VACUDEST Systems for Industrial ZLD

H2O GmbH is a pioneer in the Vacuum Evaporators market with its VACUDEST technology focused on achieving Zero Liquid Discharge in industrial processes. Its systems reduce wastewater volumes by up to 99%, significantly lowering disposal costs for surface treatment and coating industries. The patented Clearcat condensation stage ensures up to 99% COD reduction, delivering high-purity distillate even from complex wastewater streams. The updated Destcontrol pH system enhances operational stability across variable chemical compositions. Strong demand in 2025 drove record order volumes, supported by Activepowerclean technology that minimizes fouling and maintenance downtime. Its modular product range allows scalable deployment from small to large industrial operations.

ENCON Evaporators Strengthens Compact ZLD Solutions with Pilot Testing and Low-Maintenance Design

ENCON Evaporators is expanding its footprint in the Vacuum Evaporators market through compact, high-capacity systems tailored for mid-market industrial users. Its vacuum heat pump and MVR evaporators now support capacities up to 550 GPH and 4,000 GPH respectively, addressing larger industrial requirements. The company’s pilot testing service allows customers to validate ZLD performance and ROI before full-scale deployment, reducing investment risk. A notable ZLD installation in a seawater aquarium highlights its capability in non-traditional applications. ENCON’s focus on low-maintenance engineering, including wide-gap heat exchangers, ensures reliability in handling high-solid and oil-laden wastewater. This emphasis on operational durability and flexibility strengthens its competitive positioning.

India Vacuum Evaporators Market Accelerated by Water Recycling Mandates and Indigenous Manufacturing Push

India’s vacuum evaporators market is entering a structurally accelerated adoption phase, driven primarily by federal water reuse mandates and state-level Zero Liquid Discharge enforcement. In 2025, the Central Pollution Control Board introduced binding regulations requiring bulk industrial water users to recycle a minimum of 20% to 30% of their total water consumption. This policy shift has directly increased procurement of high-capacity vacuum distillation and multiple-effect evaporator systems, particularly across chemicals, pharmaceuticals, textiles, and bulk drug manufacturing clusters where high-salinity effluents cannot be treated through membrane filtration alone.

State-level implementation is amplifying demand. Maharashtra’s Safe Reuse Policy 2025 mandates treated industrial wastewater as a priority input for thermal power plants and industrial estates, while enforcing Zero Liquid Discharge in high-load chemical and pharmaceutical zones. This has positioned vacuum evaporators and crystallizers as core compliance infrastructure rather than optional treatment add-ons. Capital formation is being reinforced by central incentives. Production Linked Incentive schemes for Specialty Chemicals and Bulk Drugs have encouraged domestic fabrication of Multiple-Effect Evaporators, reducing reliance on imported European systems. Infrastructure programs are also material. Under the Namami Gange Mission, more than ₹20,000 crore is being deployed toward sewage and industrial effluent treatment, with evaporative technologies prioritized for eliminating toxic discharge into the Ganga basin.

Technology and financing mechanisms are further improving adoption economics. Pilot projects in Gujarat and Rajasthan have integrated solar-thermal systems with vacuum crystallizers, lowering electrical operating costs by an estimated 15% to 20%. In parallel, the Department of Science and Technology extended its Waste Management Technologies grant program through August 2025, offering capital subsidies that enable MSMEs to deploy modular vacuum evaporators. Collectively, these factors position India as one of the most regulation-driven growth markets for vacuum evaporation systems globally.

United States Vacuum Evaporators Market Shaped by Effluent Regulation, Localization, and Digital Optimization

The United States vacuum evaporators market is being reshaped by tightening effluent standards, domestic manufacturing localization, and advanced digital control systems. In 2025, the Environmental Protection Agency updated its Effluent Limitation Guidelines to impose stricter contaminant thresholds on wastewater from power generation and mining operations. These guidelines increasingly favor vacuum evaporation over conventional filtration for high-total-dissolved-solids streams, particularly where brine concentration and solvent recovery are required.

Trade policy has reinforced domestic capacity. New 2025 tariffs on imported chemical processing equipment have prompted companies such as De Dietrich and SPX Flow to localize fabrication of stainless steel and nickel-alloy evaporator components within the United States. Federal infrastructure funding is also acting as a catalyst. Grants under the Bipartisan Infrastructure Law have accelerated installation of large-scale Mechanical Vapor Recompression systems in drought-stressed states including California and Arizona, where industrial water recycling is becoming a permitting requirement.

Operational efficiency is emerging as a differentiator. U.S. technology providers introduced Digital Twin software platforms in late 2024 that allow operators to model fouling, scaling, and heat-transfer degradation scenarios. Facilities adopting these tools reported a 25% reduction in unplanned downtime during 2025. A distinct demand driver is the regulated cannabis extraction sector, where solvent recovery and concentration are mission-critical. This niche but rapidly professionalizing industry is creating substantial demand for high-performance vacuum evaporators designed for flammable solvent handling and precise thermal control.

Germany Vacuum Evaporators Market Defined by Energy Optimization and REACH-Driven Process Upgrades

Germany’s vacuum evaporators market is anchored in energy efficiency leadership and regulatory foresight. A 2025 pilot project in Cuxhaven demonstrated that AI-enabled SCADA integration across vacuum evaporation systems can reduce combined aeration and heating energy consumption by approximately 30%, translating into annual savings exceeding one million kilowatt-hours at a single facility. These results are accelerating adoption of intelligent control architectures across municipal and industrial treatment plants.

Regulatory preparedness is a parallel driver. Ahead of 2026 REACH compliance milestones, German chemical manufacturers are replacing legacy wastewater treatment assets with low-temperature vacuum evaporators that prevent thermal degradation of heat-sensitive by-products. This shift is particularly relevant for fine chemicals, specialty intermediates, and pharmaceutical residues where product recovery and by-product valorization are economically material. Technology innovation is reinforcing this transition. H2O GmbH expanded its VACUDEST platform in 2025, integrating advanced heat pump technology that delivers energy savings of up to 95% compared to atmospheric evaporation. Germany thus functions as a reference market for ultra-low-energy vacuum evaporation design.

China Vacuum Evaporators Market Driven by Industrial Park Standardization and Battery Recycling

China represents the largest policy-coordinated deployment environment for vacuum evaporators, underpinned by industrial park standardization and strategic recycling priorities. Under the 14th Five-Year Plan, the Ministry of Industry and Information Technology mandated that 70% of industrial parks achieve standardized water recycling benchmarks. This requirement is triggering large-scale installations of Mechanical Vapor Recompression and Multiple-Effect Evaporator systems across chemical, metallurgy, and materials processing zones.

Industrial consolidation is reshaping system architecture. New chemical capacity approvals in 2025 are largely restricted to designated Resource Recycling Bases, where centralized vacuum evaporation hubs treat combined effluent streams from multiple small and mid-sized enterprises. This shared-infrastructure model is driving demand for very large-capacity, corrosion-resistant evaporators with high operational uptime. Capacity expansion is also being driven by the lithium-ion battery recycling sector. Domestic equipment manufacturers have scaled up production of titanium-clad evaporators to support recovery of battery-grade salts, where precise vacuum evaporation is critical for purity control and yield optimization.

Netherlands Vacuum Evaporators Market Focused on Circular Food Processing and Exportable Water Technologies

The Netherlands vacuum evaporators market is characterized by circular processing leadership and export-oriented water technology development. In a benchmark 2025 deployment, a major Dutch dairy processor implemented an energy-efficient vacuum evaporation system capable of recovering approximately 80% of process water, aligning operations with the latest European environmental directives. This project has become a reference case for food and beverage manufacturers seeking to decouple production growth from freshwater intake.

At the policy level, the Dutch government is actively subsidizing the export of plug-and-play modular vacuum evaporators to emerging markets. These systems emphasize compact footprints, rapid installation, and low operator intervention, making them suitable for urban-industrial zones with constrained space and water stress. As a result, the Netherlands is positioning itself less as a volume deployment market and more as a global exporter of advanced vacuum evaporation solutions.

Summary of Country-Level Vacuum Evaporators Market Dynamics

Vacuum Evaporators Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Core Application Focus

|

Strategic Positioning

|

|

India

|

Water recycling mandates and ZLD enforcement

|

Chemicals, pharmaceuticals, MSMEs

|

Regulation-led rapid adoption

|

|

United States

|

ELG tightening and infrastructure funding

|

Power, mining, cannabis processing

|

Localized manufacturing and digital optimization

|

|

Germany

|

Energy efficiency and REACH readiness

|

Specialty chemicals, municipal treatment

|

Ultra-low-energy technology benchmark

|

|

China

|

Industrial park standardization

|

Chemicals, battery recycling

|

Policy-driven scale and centralized hubs

|

|

Netherlands

|

Circular processing and exports

|

Dairy, modular water systems

|

Innovation-led exporter of compact solutions

|

Vacuum Evaporators Market Report Scope

Vacuum Evaporators Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.3 Billion

|

|

Market Size (2034)

|

$14.2 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Technology (Mechanical Vapor Recompression, Thermal Vapor Recompression, Multiple Effect Evaporation, Heat Pump Vacuum Evaporation, Vacuum Crystallizers, Low Temperature Evaporators), By Operation Mode (Batch Operation, Continuous Operation), By Capacity (Small Capacity, Medium Capacity, Large Capacity, Ultra-Large Capacity), By Application (Wastewater Treatment, Product Concentration and Purification, Solvent Recovery, Resource Recovery), By End-Use Industry (Pharmaceutical and Biotechnology, Chemical and Petrochemical, Food and Beverage, Electronics and Semiconductor, Automotive and Surface Treatment, Mining and Metallurgy, Textile and Tannery)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia Water Technologies, GEA Group Aktiengesellschaft, SPX Flow Inc., Alfa Laval AB, SUEZ Water Technologies and Solutions, H2O GmbH, Condorchem Enviro Solutions, Eco-Techno Srl, Bucher Unipektin AG, Sasakura Engineering Co. Ltd., Saltworks Technologies Inc., De Dietrich Process Systems, 3V Tech S.p.A., Samsco

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Vacuum Evaporators Market Segmentation

By Technology

- Mechanical Vapor Recompression

- Thermal Vapor Recompression

- Multiple Effect Evaporation

- Heat Pump Vacuum Evaporation

- Vacuum Crystallizers

- Low Temperature Evaporators

By Operation Mode

- Batch Operation

- Continuous Operation

By Capacity

- Small Capacity

- Medium Capacity

- Large Capacity

- Ultra-Large Capacity

By Application

- Wastewater Treatment

- Product Concentration and Purification

- Solvent Recovery

- Resource Recovery

By End-Use Industry

- Pharmaceutical and Biotechnology

- Chemical and Petrochemical

- Food and Beverage

- Electronics and Semiconductor

- Automotive and Surface Treatment

- Mining and Metallurgy

- Textile and Tannery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Vacuum Evaporators Market

- Veolia Water Technologies

- GEA Group Aktiengesellschaft

- SPX Flow Inc.

- Alfa Laval AB

- SUEZ Water Technologies and Solutions

- H2O GmbH

- Condorchem Enviro Solutions

- Eco-Techno Srl

- Bucher Unipektin AG

- Sasakura Engineering Co. Ltd.

- Saltworks Technologies Inc.

- De Dietrich Process Systems

- 3V Tech S.p.A.

- Samsco

*- List not Exhaustive