Plastic Replacement, Recyclability, and Paper-Based Packaging Driving Strong Growth

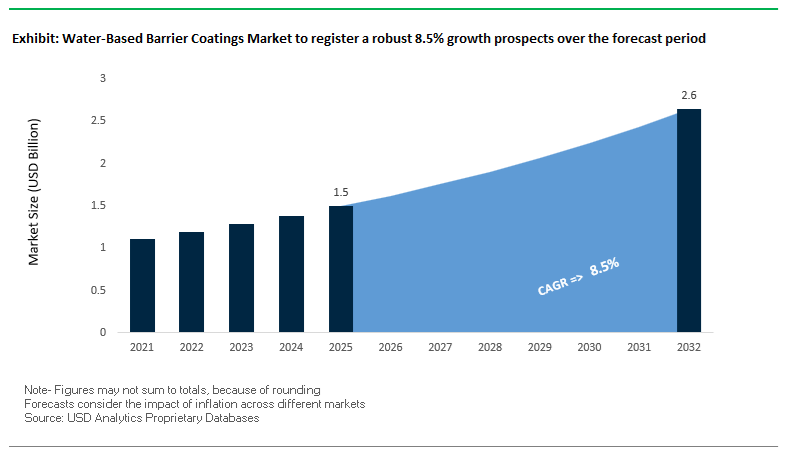

The global Water-Based Barrier Coatings Market is expanding rapidly, driven by the accelerating shift toward sustainable, fiber-based packaging and plastic reduction initiatives. The market was valued at $1.5 billion in 2025 and is projected to reach $2.7 billion by 2032, growing at a CAGR of 8.5% during 2025–2032. This growth is primarily fueled by regulatory pressure and brand commitments to eliminate single-use plastics, particularly in food, beverage, and e-commerce packaging.

A key structural driver is the transition from multi-layer plastic laminates to mono-material paper-based packaging, enabled by advanced water-based barrier coatings. These coatings provide essential functional properties such as grease resistance, moisture protection, oxygen barrier, and heat-sealability, making them viable replacements for polyethylene (PE), polypropylene (PP), and other plastic layers.

Another major trend is the development of high-performance barrier chemistries, including polyurethane dispersions (PUD), acrylic dispersions, and bio-based polymers, which deliver improved durability and recyclability. These coatings are increasingly being engineered to pass global recyclability standards, ensuring compatibility with existing paper recycling streams without contaminating fiber recovery processes.

Sustainability is the dominant market driver. Water-based barrier coatings are low-VOC, PFAS-free, and compatible with circular economy models, addressing both regulatory requirements and consumer expectations. Additionally, the demand for food-safe, low-migration coatings is driving innovation in packaging applications such as cups, wraps, sachets, and flexible paper packaging.

The market is also benefiting from the rapid growth of e-commerce and packaged food consumption, where demand for durable, lightweight, and sustainable packaging solutions is increasing globally.

Market Analysis: PFAS-Free Innovation, Paper-Based Packaging Systems, and Cold-Seal Technologies Reshaping Competitive Landscape

The water-based barrier coatings market is undergoing rapid transformation, driven by plastic replacement strategies, PFAS-free innovation, and high-performance coating technologies. Henkel’s April 2026 launch of a global paper coatings portfolio marks a significant step toward replacing plastic layers in packaging. These coatings provide grease, water, and moisture barriers on paper substrates, enabling the production of recyclable packaging for dry food and hygiene products.

Process innovation is also advancing packaging efficiency. Henkel’s February 2026 cold-seal solution allows barrier-coated paper to be sealed without heat, maintaining coating integrity while enabling high-speed packaging operations, particularly in confectionery and secondary packaging.

Major packaging players are accelerating adoption. Mondi’s February 2026 upgrade to recyclable spice packaging demonstrates the shift toward mono-material paper solutions, utilizing water-based barrier coatings to replace traditional plastic laminates while maintaining aroma and moisture protection.

Product innovation is focused on performance and recyclability. Michelman’s Michem® Coat 9250 (November 2025) introduces a high-performance coating for paper cups that withstands hot liquids while meeting global recyclability standards, outperforming conventional PE and PLA liners in fiber recovery.

PFAS-free solutions are becoming a central competitive factor. Siegwerk’s 2025–2026 roadmap and Allinova acquisition significantly expand its portfolio of PFAS-free water-based dispersions, providing grease resistance for food packaging without relying on fluorinated chemicals.

Material innovation is also advancing through polyurethane technologies. Sun Chemical’s BLUEPUR and HYDRAN lines (March 2025) introduce amine-free water-based PUD coatings, delivering high barrier performance with reduced VOC emissions and improved process safety for converters.

Sustainability is extending beyond packaging into other sectors. AkzoNobel’s bio-based barrier coatings (2024–2025 scaling) utilize plant-derived resins such as rapeseed and pine, while its solar-absorbing barrier technology integrates moisture protection with thermal efficiency, demonstrating cross-industry applications of water-based barrier systems.

Additionally, BASF’s bio-attributed resin developments (October 2025) highlight the integration of low-carbon materials into barrier coatings, supporting broader sustainability goals across packaging and industrial applications.

Market Trend: EU PPWR 2025/40 Regulation Driving Recyclable and PFAS-Free Barrier Coatings Adoption

The implementation of the European Packaging and Packaging Waste Regulation (EU) 2025/40 is significantly reshaping the water-based barrier coatings market across Europe, with full legal enforcement beginning August 12, 2026. This regulation mandates a systemic shift toward sustainable packaging materials, positioning waterborne barrier coatings as a critical technology in enabling recyclable and environmentally compliant packaging solutions.

Under Article 6, the Design for Recyclability requirement compels all packaging formats to be compatible with existing recycling infrastructure. Water-based barrier coatings are emerging as the preferred alternative to polyethylene-laminated substrates, as they allow paper-based packaging to be efficiently processed in standard hydropulpers without clogging or fiber contamination. This is accelerating the adoption of paper-based flexible packaging and fiber-based food packaging across the fast-moving consumer goods sector.

The regulation also enforces stringent chemical restrictions, particularly targeting PFAS compounds in food-contact materials. PFAS-free waterborne coatings are witnessing rapid adoption, achieving near-complete replacement rates in applications such as fast-food wrappers and microwaveable packaging within the Eurozone. This trend is strengthening demand for non-toxic barrier coatings and sustainable food packaging technologies aligned with circular economy principles.

Market Trend: U.S. FDA Low-Migration Standards Driving Functional Barrier Coatings and Traceability Integration

The evolving regulatory framework under the U.S. FDA Human Foods Program 2026 Deliverables is driving a major shift toward low-migration water-based barrier coatings in the North American packaging market. The “Closer to Zero” initiative is intensifying scrutiny on chemical contaminants in food-contact packaging, pushing manufacturers toward safer, compliant coating technologies.

Waterborne barrier coatings utilizing Food Contact Notification authorized polymeric binders are becoming the industry standard for food-safe packaging applications. A key requirement is the reduction of mineral oil migration, particularly MOSH and MOAH compounds originating from recycled paperboard. As of 2026, functional barrier coatings must demonstrate at least a 90% reduction in hydrocarbon migration to maintain GRAS compliance for dry food packaging, driving innovation in advanced barrier coating formulations.

Additionally, the FSMA Food Traceability Final Rule mandates the implementation of digital chemical passports for packaging materials. This requirement ensures full traceability of waterborne resin systems down to their monomeric origin, enhancing supply chain transparency and risk management. The integration of traceability systems is becoming a competitive differentiator for packaging converters and coating manufacturers operating in regulated food packaging markets.

Market Opportunity: High-Barrier Waterborne Coatings Enabling Mono-Material Flexible Packaging Solutions

The transition toward mono-material flexible packaging is creating substantial growth opportunities in the high-barrier water-based coatings segment. Advanced waterborne dispersions, including ethylene-modified polyvinyl alcohol (PVOH) and nano-clay reinforced systems, are achieving oxygen transmission rates below 1.0 cm³/m²/day at 50% relative humidity. This level of performance enables the replacement of traditional EVOH layers in snack packaging and pet food pouches, supporting recyclable packaging formats.

In addition to oxygen barrier performance, water vapor transmission rates are also being optimized through acrylic-wax hybrid coatings, achieving WVTR levels below 2.0 g/m²/day. These coatings provide effective moisture protection for hygroscopic food products such as powders and dehydrated goods without relying on polyethylene film lamination. This dual barrier capability is positioning waterborne coatings as a key enabler of sustainable flexible packaging innovation.

Production scalability is further enhancing market adoption, as modern water-based barrier coatings are engineered for high-speed gravure and flexographic printing processes. With stable rheological properties at line speeds of 300 to 400 meters per minute, these coatings eliminate previous throughput limitations, allowing packaging manufacturers to maintain operational efficiency while transitioning to eco-friendly barrier technologies.

Market Opportunity: Compostable Waterborne Coatings Advancing Sustainable Paperboard Food Packaging

The increasing demand for compostable food packaging solutions is driving innovation in water-based barrier coatings for paperboard trays and molded fiber products. These coatings are replacing conventional wax and plastic linings, supporting the shift toward biodegradable and recyclable food service packaging in line with global sustainability mandates.

Advanced compostable waterborne coatings are achieving high grease resistance, with Kit Test ratings exceeding Kit 12, making them suitable for high-fat food applications such as fried foods and sauces. This performance level ensures functional equivalence to traditional barrier materials while maintaining environmental compliance.

To meet international compostability standards such as EN 13432 and ASTM D6400, these coatings demonstrate over 90% disintegration within 12 weeks under industrial composting conditions, with no ecotoxic impact on soil quality. This certification is critical for gaining regulatory approval and market acceptance in environmentally regulated regions.

Thermal performance is also a key area of advancement, with next-generation waterborne barrier resins engineered to withstand temperatures up to 220°C for 30 minutes. This enables the development of dual-ovenable paperboard trays suitable for both microwave and conventional oven use, expanding their application in ready-meal packaging while maintaining full recyclability and compostability.

Water-Based Barrier Coatings Market Share and Segmentation Insights

Binders Lead with 54.2% Share as Core Driver of Barrier Properties in Sustainable Packaging

The binders segment dominates the water-based barrier coatings market with a 54.2% market share in 2025, reflecting its critical role in delivering oxygen, moisture, and grease resistance across packaging applications. In the sustainable packaging coatings and functional barrier materials market, binders such as acrylics, polyurethanes, EVOH (ethylene vinyl alcohol), and PVDC latexes are essential for ensuring product protection, shelf-life extension, and regulatory compliance in food packaging. These materials are widely used in paperboard, flexible films, and coated paper packaging, particularly for applications requiring oil resistance (e.g., pizza boxes) and moisture barriers (e.g., frozen food cartons). Additionally, binders represent 40–60% of total coating formulation solids, making them the largest contributor by volume and a key cost driver. As demand rises for eco-friendly, water-based coatings replacing plastic laminates, binders remain central to innovation and performance in the global water-based barrier coatings market.

Converters and Specialized Coating Houses Lead with 49.3% Share Through Application Expertise and Customization

The converters and specialized coating houses segment leads the water-based barrier coatings market with a 49.3% market share in 2025, driven by their technical expertise in coating application and substrate processing. Within the food packaging and industrial coating services market, converters apply barrier coatings to paper, film, and foil substrates using advanced techniques such as gravure, flexographic, and rod coating processes, ensuring consistent performance and quality. These players source binders, additives, and formulation components directly from specialty chemical suppliers, enabling precise control over coating characteristics. A key growth driver is the need for customized barrier solutions tailored to specific packaging requirements, such as grease-resistant coatings for quick-service food packaging and moisture barriers for frozen and perishable goods. Their ability to deliver application-specific performance, scalability, and innovation makes converters indispensable in the global water-based barrier coatings value chain, reinforcing their dominant market position.

Competitive Landscape Analysis of the Water-Based Barrier Coatings Market

AkzoNobel Expands Water-Borne Barrier Coatings Through Dubai Aerospace Hub

AkzoNobel N.V. is strengthening its water-based barrier coatings market position with the Q2 2026 launch of its Dubai Aerospace Coatings Hub, which also integrates water-borne barrier technologies for regional industrial packaging and reduces Middle Eastern lead times by an estimated 30%. The company has scaled integrated barrier systems for liquid packaging, achieving a 95% repulpability rate in standard paper recycling streams. AkzoNobel’s adjusted EBITDA margin reached 14.5% in early 2026, supported by high-margin specialty barrier coatings in EMEA. Its Interpon® and Resicoat® lines are being adapted for functional packaging, offering anti-corrosive water-based barriers for industrial drum and container linings.

BASF Advances Joncryl Water-Based Dispersions for Circular Packaging and EV Safety

BASF SE leads the water-based barrier coatings market through its Joncryl® resin and functional additives portfolio, expanded in 2026 with mass-balance certified water-based dispersions that help converters claim a 50% reduction in fossil-fuel usage. BASF introduced eco-friendly oxygen-scavenging resin systems for ready-to-eat meal packaging, extending shelf life by 15–20% without aluminum foil. Holding a 16% share of the global functional additives market, BASF uses Ultrasim® simulation technology to optimize barrier thickness for CPG brands. The company is also targeting eMobility and battery safety with water-based dielectric barrier coatings that provide fire retardancy and moisture insulation for high-density EV battery packs.

Mondi Leads Paper-Based Barrier Packaging With Award-Winning Recyclable Solutions

Mondi Group is a major force in water-based barrier coatings, reinforced by nine WorldStar Packaging Awards in 2026, including recognition for re/cycle HiProtex Paper, a high-barrier solution replacing aluminum and PVDC composites with over 80% paper content. As a fully integrated player, Mondi controls the value chain from sustainable forestry to water-based functional coating application, supporting closed-loop packaging for FreshFood BOX and protective mailers. Its 2026 upgrade to paper-based padded mailer production aims to replace 1.2 billion plastic bubble mailers annually. Mondi’s Ad/Vantage Smooth Brown kraft paper delivers strong coating compatibility and MVTR control for heavy-duty industrial bags.

Michelman Strengthens PFAS-Free Food Contact Barrier Coatings

Michelman is expanding its role in the water-based barrier coatings market through sustainable chemistry and food-contact innovation. In 2026, the company released VaporCoat® 2200R, a repulpable kraft liner coating designed to replace plastic bags and poly-laminated boards in poultry and produce packaging. Its collaboration with HP Indigo optimized DigiPrime® Vision 9200, a water-resistant primer for high-speed digital printing on compostable barrier films. Michelman leads in PFAS-free food contact coatings, with HydraBan® and Michem® Flex technologies used by global fast-food chains seeking grease-resistant wraps without forever chemicals. Its Singapore manufacturing hub supports ASEAN-China markets with water-resistant coatings for fruit and vegetable export boxes.

Stora Enso Accelerates Bio-Based Dispersion Barrier Coatings for Fiber Packaging

Stora Enso is advancing the water-based barrier coatings market through its biomaterials transition and fiber-based packaging strategy. Following its January 2026 restructure, the company consolidated Consumer Packaging and Integrated Packaging to prioritize high-growth barrier solutions. Its Consumer Packaging division reported EUR 354 million in Q1 2026 revenue, driven by adoption of water-based Dispersion Barrier technology for hot and cold beverage cups. Stora Enso is piloting lignin-based barrier resins with strong oxygen barrier performance and industrial compostability. Through its Biomaterials division, the company is developing “tree-to-tray” packaging using micro-fibrillated cellulose to improve strength and barrier performance in molded fiber packaging.

Germany Leading Circular Packaging Innovation and PPWR Compliance

Germany is at the forefront of the water-based barrier coatings market, driven by strict regulatory alignment with the upcoming EU Packaging and Packaging Waste Regulation (PPWR). The requirement for >95% repulpability in paper-based packaging is accelerating the shift toward fully recyclable aqueous barrier systems.

Technological advancements include the development of high-performance water-based barrier resins that match the oxygen and moisture resistance of traditional polyethylene laminations while remaining compatible with paper recycling streams. Product innovation such as de-laminating aqueous adhesives is enabling efficient separation of multi-layer packaging, supporting circular economy goals.

Strategic investments in circular packaging centers are enhancing capabilities in low-migration, food-safe barrier coatings, particularly for the fast-growing grab-and-go food sector. Infrastructure upgrades, including automated coating quality monitoring systems, are ensuring high precision in barrier application. These developments position Germany as a global leader in sustainable and recyclable packaging barrier technologies.

United States Driving PFAS-Free Barrier Coatings and Compostable Packaging Solutions

The United States is undergoing a major transition in the water-based barrier coatings industry, driven by regulatory bans on PFAS and increasing demand for compostable packaging. Multiple state-level bans on PFAS in food packaging are accelerating adoption of aqueous grease-resistant coatings, significantly expanding the market.

Product innovations include PFAS-free moisture barrier coatings designed for high-speed production lines in the packaging industry. Government initiatives such as the USDA BioPreferred Program are promoting the use of bio-based barrier coating materials, encouraging sustainable procurement practices.

Technological advancements in nano-cellulose reinforced coatings are enabling high-performance oxygen barriers, replacing aluminum-based laminates. Industrial expansion is supporting large-scale production of compostable barrier solutions for quick-service restaurants and e-commerce packaging. Key applications include cold-chain insulation coatings, replacing traditional polystyrene materials. These trends position the U.S. as a leader in sustainable and high-performance barrier coating technologies.

China Scaling Water-Based Barrier Coatings Through Green Packaging Mandates

China is rapidly expanding its footprint in the water-based barrier coatings market, driven by state-led sustainability initiatives and large-scale industrialization. Government policies offering incentives for replacing plastic-coated paper are accelerating adoption of water-based functional coatings across multiple industries.

Technological advancements include the integration of graphene-oxide additives into aqueous barrier systems, enhancing both moisture resistance and EMI shielding capabilities. Infrastructure developments such as dedicated industrial zones for barrier coating production are supporting high-volume manufacturing for global exports.

Strategic expansions in polyurethane dispersion (PUD) capacity are strengthening supply chains for food packaging and logistics applications. Key applications include moisture-proof coatings for 5G infrastructure components, ensuring durability during transportation. Regulatory updates enforcing strict safety standards are further driving innovation, positioning China as a leader in scalable and high-performance aqueous barrier coatings.

India’s Rapid Growth Driven by Plastic Ban and Cold-Chain Logistics Expansion

India is emerging as a high-growth market in the water-based barrier coatings sector, fueled by regulatory action and infrastructure modernization. The expansion of the single-use plastic ban is driving a significant shift toward recyclable, water-based coated packaging solutions.

Technological advancements include the development of tropical-grade barrier coatings, designed to maintain performance in high-humidity environments. Strategic investments in bio-barrier board production are strengthening domestic capabilities, while infrastructure developments such as sustainable packaging hubs are supporting innovation and adoption.

Key applications include antimicrobial barrier coatings for pharmaceutical packaging, improving shelf life and safety for exported products. Product innovation using agricultural waste-derived resins is reducing dependence on imported materials, enhancing cost efficiency. These developments position India as a growing hub for eco-friendly and cost-effective water-based barrier coatings.

Japan Leading Nano-Precision Barrier Coatings for Electronics and Medical Applications

Japan continues to lead in nano-engineered water-based barrier coatings, focusing on high-precision applications in electronics, packaging, and healthcare. Innovations such as ultra-thin EVOH-based barrier layers are achieving high oxygen barrier performance while maintaining recyclability.

Technological advancements are enabling the use of UV-curable aqueous barrier coatings in high-speed applications such as railway catering packaging, supporting lightweight and sustainable solutions. Investments in advanced barrier adhesives are expanding applications in extreme environments, including cryogenic conditions for LNG transport.

Key applications include moisture-resistant coatings for medical devices, capable of withstanding repeated sterilization cycles. Regulatory standards are ensuring high performance and durability, reinforcing Japan’s leadership in precision-driven and high-value barrier coating technologies.

Brazil Advancing Bio-Based Barrier Coatings Through Pulp Industry Integration

Brazil is leveraging its strong pulp and forestry sector to become a key player in the bio-based water-based barrier coatings market. Vertical integration of coating systems within pulp production lines is enabling efficient manufacturing of renewable barrier-coated packaging materials.

Product innovations include lignin-based barrier coatings, utilizing forestry by-products to provide natural grease and UV resistance. Technological advancements such as smart-color barrier coatings are improving product safety by visually indicating barrier integrity.

Strategic investments in bio-polyethylene dispersions are bridging the gap between traditional plastics and aqueous coatings. Regulatory initiatives promoting bio-based content are further supporting market growth. Key applications include moisture-resistant coatings for agricultural packaging, ensuring durability and biodegradability. These developments position Brazil as a leader in sustainable and renewable barrier coating technologies.

Water-Based Barrier Coatings Market Report Scope

Water-Based Barrier Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2032)

|

$2.7 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Resin (Acrylic-based Coatings, Polyurethane, Epoxy-based Coatings, Ethylene Vinyl Acetate, Polyvinylidene Chloride, Biopolymer-based, Wax-based Emulsions), By Barrier Functionality (Moisture and Water Vapor Barrier, Oil and Grease Barrier, Gas and Oxygen Barrier, Aroma and Flavor Barrier, Chemical and Corrosion Resistance, Heat Sealability), By Component (Binders, Additives, Fillers and Pigments), By Substrate (Paper and Paperboard, Plastic Films, Metal, Glass, Biodegradable), By End-User Industry (Food and Beverage Packaging, Pharmaceutical and Healthcare, Consumer Goods and Personal Care, E-commerce and Logistics, Industrial and Manufacturing, Agricultural), By Sales Channel (Direct Sales, Converters and Specialized Coating Houses, Industrial Chemical Distributors, Online B2B Procurement Platforms)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, ALTANA AG, Michelman, Inc., Solenis, Henkel Adhesive Technologies, Dow Inc., H.B. Fuller Company, Kuraray Co., Ltd., Siegwerk Druckfarben AG and Co. KGaA, Stora Enso Oyj, Mondi Group, Imerys, Sonoco Products Company, Archroma, Paramelt B.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Based Barrier Coatings Market Segmentation

By Resin

- Acrylic-based Coatings

- Polyurethane

- Epoxy-based Coatings

- Ethylene Vinyl Acetate

- Polyvinylidene Chloride

- Biopolymer-based

- Wax-based Emulsions

By Barrier Functionality

- Moisture and Water Vapor Barrier

- Oil and Grease Barrier

- Gas and Oxygen Barrier

- Aroma and Flavor Barrier

- Chemical and Corrosion Resistance

- Heat Sealability

By Component

- Binders

- Additives

- Fillers and Pigments

By Substrate

- Paper and Paperboard

- Plastic Films

- Metal

- Glass

- Biodegradable

By End-User Industry

- Food and Beverage Packaging

- Pharmaceutical and Healthcare

- Consumer Goods and Personal Care

- E-commerce and Logistics

- Industrial and Manufacturing

- Agricultural

By Sales Channel

- Direct Sales

- Converters and Specialized Coating Houses

- Industrial Chemical Distributors

- Online B2B Procurement Platforms

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Water Based Barrier Coatings Industry

- BASF SE

- ALTANA AG

- Michelman, Inc.

- Solenis

- Henkel Adhesive Technologies

- Dow Inc.

- H.B. Fuller Company

- Kuraray Co., Ltd.

- Siegwerk Druckfarben AG & Co. KGaA

- Stora Enso Oyj

- Mondi Group

- Imerys

- Sonoco Products Company

- Archroma

- Paramelt B.V.

*- List not Exhaustive