Water Testing Equipment Market Outlook: Size, CAGR, and Strategic Insights for Industry Leaders

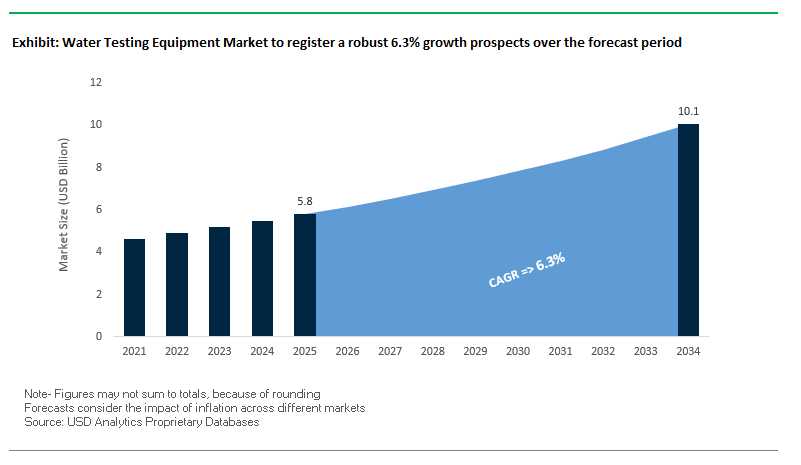

The global water testing equipment market is projected to expand from USD 5.8 billion in 2025 to USD 10.1 billion by 2034, achieving a CAGR of 6.3% over the forecast period. Growth is driven by tightening regulatory mandates, increasing concern over emerging contaminants, and technological advancements in digital monitoring and decentralized testing. For seasoned industry professionals, the market is at an inflection point where precision, compliance, and operational efficiency converge as core investment priorities.

Stricter potable water quality specs and effluent limits within industrial effluents are driving expanded use of sophisticated analytical tools within cities, industries, and utilities. High-end analytical tools such as immunoassay-based analyzers continue to earn entry into measurement of micropollutants such as drug residues and endocrine disruptors, while IoT-based sensors integrated into cloud-based data handling systems continue to redefine monitoring from reactive to predictive.

Portably accessible and decentralised kits that can conduct water testing is another innovation where compliance can be performed remotely or in rural locations without central lab reliance. Decentralisation not only enhances detection but reduces operational costs both on a governmental and operator-industrial level.

Key Insights for Professionals:

- CAGR of 6.3% driven by regulatory enforcement, IoT adoption, and emerging contaminant monitoring.

- Immunoassay-based analyzers are becoming central to advanced contaminant detection workflows.

- IoT-enabled and cloud-integrated water testing systems are reshaping real-time compliance monitoring.

- Decentralized and portable water testing equipment is expanding market access in rural and remote areas.

Market Analysis: Regulatory Pressure, Technology Advancements, and Strategic Developments

The market is in a phase of rapid technological transformation, catalyzed by both environmental mandates and operational efficiency goals. The demand for PFAS testing equipment has surged following stricter regulations, with Veolia’s USD 35 million PFAS treatment facility in the U.S. (June 2025) standing as a benchmark project. The facility underscores the growing need for specialized analytical instruments capable of accurately detecting and validating the removal of persistent contaminants.

Instrument innovation is a characteristic trend. Xylem's release of the NH6000sc ammonia analyzer (August 2025) featuring Gas Sensing Electrode (GSE) technology and minimized reagent usage shows the market shift toward high-accuracy, low-maintenance instruments appropriate for long-term use. Likewise, Thermo Fisher Scientific's Heratherm Environment al Chamber (August 2025) meets a paramount laboratory need: controlling exact and reproducible environmental conditions to guarantee the integrity of analysis of water samples.

Strategic collaboration defines roadmaps for R&D. Collaboration between SUEZ and CNRS (April 2025) targets state-of-the-art micropollutant treatment technology, such as PFAS removal. Innovative WTW analyzers by Xylem Analytics (May 2025) to identify high-concentration ammonium and a Hach SL250 portable instrument (September 2024) reflect interest in mobility, automation, and wide-end-user accessibility.

Aside from innovation, company strategies are oriented toward mobility and rapid deployment. Veolia's expansion of mobile water services in Malaysia (March 2024) exemplifies the new trend toward prefabricated and in-site solutions, supported by correspondingly agile testing units. Procurement choices are increasingly informed by sustainability credentials, like Hach's winning an EcoVadis Gold Medal (August 2024).

Trends and Opportunities in Water Testing Equipment Market

Trend 1: Rapid Adoption of AI-Powered Real-Time Monitoring Systems

Water testing technology market is shifting increasingly toward AI-based, real-time monitoring systems that integrate IoT sensor networks and sophisticated analytics to facilitate predictive water quality management. By predictive, we can mean that systems powered by AI will be capable of anticipating contamination events at an average level of about 94% such that cities, manufacturing centers, and environmental commissions can respond immediately and mitigate the effects of polluters. Research has indicated that coupling AI with IoT and satellite remote sensing can decrease field sample costs by a range of 60% while boosting monitoring effectiveness by about 40%. More than mere efficiency, however, these systems can examine sophisticated chemical interactions and biological impacts and provide a broader perspective about aquatic ecosystems such as how a study in China's Chaobai River uncovered cumulative toxic effects that conventional monitoring can miss. It is a trend that suggests a shift toward data-driven automated monitoring of waters that optimizes operational effectiveness, regulatory conformance, and environmental protection.

Trend 2: Portable Testing Kits for Emerging Contaminants

As awareness about contaminants such as PFAS and microplastics increases among consumers, portable testing kits for water become popular in residential, municipal, and industrial applications. Portable testing kits conduct on-location testing for emerging contaminants and provide quick, accurate, and actionable results. For example, companies such as Cyclopure and Culligan provide consumers with mail-to-lab PFAS kits capable of identifying up to 55 PFAS analytes to part-per-trillion (ppt) levels and making compliance testing with EPA levels a snap. Likewise, emerging microplastics testing kits utilize optical and Nile red-staining-based polarized light microscopy to identify particles in the range of down to 1 micron. Advanced water quality testing is made available in a mobile format that has clear results with health-based risk interpretation and recommendations on treatments. Increasing numbers and sophistication of portable testing kits indicate a market trend fueled by convenience, awareness, and compliance requirements driven by regulation.

Opportunity 1: Military and Disaster Response Applications

The defense and aid fields are leading demand drivers for portable, rugged water testing instruments. For use in field missions, forward operating bases, and disaster response applications, fieldable water testing kits are essential in securing potable drinking water where conventional supplies are not available. Equipment such as the U.S. military's Water Assessment and Purification (WAsP) toolkit equip military personnel with transportable systems to measure pH levels, turbidity levels, and other measurements while enabling stand-alone water evaluation and purification solutions. Bacterial detection kits such as E. coli detection kits find application in tactical missions and disaster response applications while enabling safe supply waters on military ships and disaster relief locations. The opportunity emphasizes the importance of convenient, compact testing instruments that can be easily utilized in stringent, resource-scarce situations.

Opportunity 2: Agricultural Runoff Monitoring

Agricultural runoff, a principal cause of water pollution, is fueling demand growth for special purpose water testing instruments in agricultural areas. Initiatives like the USDA's National Water Quality Initiative (NWQI) invests in and technical assistance for watershed-wide monitoring of nutrient and pesticide runoff in target watersheds, generating demand for precise in-stream testing instruments that yield accurate results. Data-driven mapping and forecasting tools, such as those modeled after the British Geological Survey's work, enable exact tracking of pollutant origin and effects assessment. Nutrient pollution remaining the number-one cause of degraded river and stream quality, testing instruments for water help track nitrogen, phosphorus, and other pollutants, inform mitigation practices, and enhance agricultural sustainability. A new opportunity highlights expansion in environmental monitoring and regulatory compliance in the market.

Water Testing Equipment Market Share

by Product Type: Test Kits & Reagents Leading the Consumables Segment

Test kits and reagents account for the largest market share at around 35% of the global water testing equipment market, making them the backbone of recurring revenue. Their dominance is rooted in the constant need for consumables, as each test requires disposable reagents or strips, unlike capital equipment which is purchased less frequently. The segment encompasses colorimetric kits, reagent refills, and test strips, which are widely used across municipal facilities, industrial operators, and residential consumers. The scalability of these consumables, coupled with growing consumer awareness of water safety, ensures their sustained growth. Additionally, The category represents the aftermarket core of the industry, making it strategically vital for suppliers to maintain recurring sales and customer loyalty.

by Product Type: Portable Testing Equipment: The Field & Rapid Response Driver

Portable testing equipment holds a 26.1% market share, driven by its indispensable role in providing rapid, on-site water analysis. These handheld and field-deployable instruments are favored by environmental consultants, industrial operators, and compliance officers who require immediate data in remote or time-sensitive scenarios. Their growing adoption reflects the increasing emphasis on decentralized testing, where decisions need to be made on the spot rather than waiting for centralized laboratory reports. Moreover, portable equipment has become critical for emergency response, spill detection, and infrastructure monitoring, cementing its role as the fieldwork champion of the water testing industry.

.png)

Market Share by Testing Parameter: Microbiological Testing as the Public Health Pillar

Microbiological testing dominates with 30.6% of the market, reflecting its irreplaceable role in safeguarding public health. Pathogen detection including particularly for E. coli, coliforms, and viruses is mandated across drinking water and wastewater applications worldwide. The consistency of demand stems from strict regulations and the non-negotiable nature of ensuring pathogen-free water supplies. Municipal water authorities, food and beverage industries, and healthcare facilities rely heavily on microbiological testing, making it the most stable revenue stream for the market. As waterborne diseases remain a pressing public health concern, the segment continues to anchor the global water testing landscape.

By Testing Parameter: Chemical Testing: Expanding with Emerging Contaminants

Chemical testing represents 28% of the market and is rapidly evolving as new contaminants such as PFAS, pharmaceuticals, pesticides, and microplastics enter the regulatory spotlight. While traditional chemical testing for ions, metals, and organic compounds remains essential, the segment’s growth is fueled by the global push for advanced analytical capabilities. Governments and industries are under increasing pressure to address non-traditional pollutants that pose long-term ecological and health risks. The expanding scope positions chemical testing as not only a compliance necessity but also a growth engine in the water testing equipment market.

Market Share by End-User Industry: Municipal Water & Wastewater at the Forefront

Municipal water and wastewater utilities command the largest market share at 34.9%, owing to their heavy regulatory obligations and extensive testing needs across the entire water cycle. From source water quality assessments to treated drinking water validation and effluent discharge compliance, municipalities are responsible for maintaining the highest testing frequency of any sector. Their investments extend to both consumables and high-precision laboratory instruments, making The segment a cornerstone of demand. Increasing global urbanization and the aging of water infrastructure further reinforce the dominance of the category, as utilities must continuously upgrade testing practices to ensure safe and reliable supply.

by End-User Industrial Sector: Diverse Needs Driving High-Value Demand

The industrial sector represents 30% of the global market, with a broad spectrum of applications ranging from monitoring process water to ensuring wastewater compliance. Industries such as power generation, pharmaceuticals, food and beverage, and chemicals each have distinct testing requirements, making the one of the most diverse end-user categories. The high financial stakes of compliance failures ranging from fines to reputational damage push industries to invest heavily in reliable testing systems. The diversity, combined with the growing adoption of continuous monitoring solutions for operational efficiency, cements the industrial sector as a high-value driver of the water testing equipment market.

Country Analysis of the Water Testing Equipment Market

United States: Expanding PFAS and Lead Testing Infrastructure

U.S. water testing instrumentation sales are greatly facilitated by the Bipartisan Infrastructure Law dedicating more than $50 billion to improving drinking water and sewer systems. Dedicated funding to treat emerging contaminants like PFAS is motivating demand for customized PFAS testing applications and high-accuracy lab analyzers. To address lead contamination in schools and childcare centers, new grant programs have been launched at the United States Environmental Protection Agency (EPA) involving lead testing in schools and childcare centers, immediately stimulating demand for portable field-deployable lead testing instrumentation. Furthermore, Water Quality Association (WQA)-backed Healthy Drinking Water Affordability Act initiatives will further extend residential water testing programs, while corporate strategies like Xylem Inc.'s purchasing of Evoqua will solidify portfolios within sustainable waters management and analytical applications. Large settlements like 3M's $12.5 billion PFAS remediation settlement further motivate investment in across-the-nation testing, while initiatives like EPA's Public Water System Supervision (PWSS) Grant help provide ongoing demand across advanced instruments utilized in monitoring waters quality.

China: Government-Led Standards and Smart Monitoring Solutions

China’s water testing equipment market is rapidly advancing under the 14th Five-Year Plan, which enforces nationwide standards for municipal and industrial wastewater quality. Government initiatives to improve rural water safety are promoting decentralized and on-site testing solutions, particularly in remote regions. Key industrial sectors, including pharmaceuticals and electronics, are fueling demand for high-precision, laboratory-grade water testing equipment. The adoption of cloud-based platforms enables real-time monitoring and reporting, enhancing transparency and compliance. Emerging technologies, such as immunoassay-based analyzers for endocrine disruptors and pharmaceutical residues, are driving the market toward smart water testing devices and automated kits suitable for decentralized facilities.

India: IoT-Enabled Water Quality Monitoring under Jal Jeevan Mission

Water testing instrumentation in India is being driven by the Jal Jeevan Mission to supply safe drinking water to all rural families. Emphasis is primarily placed on monitoring water quality through stationary and mobile labs that are fortified with smart IoT-based systems capable of generating real-time alerts for remedial action. National programs make public testing available in govt labs, ensuring a large boost in demand for analytical instruments for testing waters. Organizations such as the National Institute of Hydrology, Roorkee, have state-of-the-art labs capable of testing numerous water parameters. Furthermore, research, development, and demonstration (RD&D) for sustainable solutions in waters is fostered through the Water Technology Initiative (WTI) that further creates demand within municipal and industrial applications for sophisticated monitoring and testing of water quality technology.

Germany: Green Technology and Microplastic Detection Driving Innovation

Germany's water testing instrumentation market is pushed by sustainability and climate resilience programs. German Association for Gas and Water (DVGW) has initiated the ""Innovation programme water"" to bridge gaps between climate change and water supply and drive innovation in monitoring water quality. Water-i.d. GmbH provides such instruments as the PrimeLab 2.0 Photometer capable of monitoring more than 150 parameters and having connectivity through WiFi, Bluetooth, and USB. Wasser 3.0 is creating rapid, standardized microplastic analysis instruments for monitoring water quality. Germany's focus on green technology and circular economy concepts is driving a market for energy-efficient water testing instrumentation supporting resource recovery, while the National Water Strategy focuses on resilient monitoring systems capable of meeting climate-related challenges.

Japan: Advanced IoT and AI-Driven Water Quality Analytics

Japan leads in technology-driven water testing equipment, integrating advanced sensors, IoT, and machine learning for predictive water quality management. Niterra Co., Ltd. has developed seawater monitoring systems that visualize real-time quality using sensor technologies adapted from automotive applications. Land-based aquaculture systems are leveraging AI and IoT to transform invisible water quality data into actionable insights, ensuring stable operations. Research at Science Tokyo has introduced solar-powered methods to purify water and recover metals from seawater brine, requiring sophisticated monitoring equipment to ensure efficiency. Kurita Water Industries’ Innovation Hub supports R&D in advanced water treatment technologies, emphasizing water quality testing as a central component of sustainable and high-performance water management solutions.

Saudi Arabia: National Water Strategy Spurs Testing Equipment Demand

Saudi Arabia’s water testing equipment market is driven by government regulations under the newly formed Saudi Water Authority (SWA) and Vision 2030 initiatives, which prioritize water security and quality monitoring. The SWA’s ""Saudi Water Quality Index"" provides a scientific tool for continuous assessment, requiring high-performance analytical instruments. Policies supporting the use of treated wastewater for industrial purposes further increase the need for compliant water testing solutions. Licensing, standard-setting, and regulatory supervision by the SWA ensure ongoing demand for advanced water quality testing equipment, while innovation and research in water resources management are promoting the development of next-generation analytical and monitoring systems.

Competitive Landscape – Technology Leadership and Strategic Expansion in the Water Testing Equipment Industry

The competitive environment is defined by diversified portfolios, strong R&D capabilities, and a shift toward smart, interconnected solutions. Global players are not only competing on precision and reliability but also on integration with digital platforms, sustainability performance, and the ability to deliver turnkey solutions spanning testing, monitoring, and treatment.

Danaher Corporation (Veralto) – Leveraging Operational Excellence for End-to-End Water Quality Solutions

Operating its water quality business under the brand Veralto, Danaher provides a complete portfolio of analytical instrumentation and water treatment services under brands such as Hach, Trojan, and ChemTreat. Through a 2023 spin-off of its Environmental & Applied Solutions segment, the company has honed in on high-impact investments in the water business. Recognized for its operating discipline under the Danaher Business System (DBS), the company thrives in satisfying laboratory-to-field solutions that fit easily within municipal and industrial applications.

Thermo Fisher Scientific – Precision-Driven Laboratory and Field Water Testing Technologies

Thermo Fisher's product range includes ion chromatography, mass spectrometry, and specialty sensors to identify contaminants such as harmful algae blooms to regulated haloacetic acids. Its August 2025 launch of Heratherm™ Environmental Chamber further cemented its position in providing instruments essential to precise, reproducible analysis in regulated applications. Its fort√ implies supporting customers across the whole workflow from sample collection right through to validated reporting and meeting research and compliance obligations.

Xylem Inc. – Smart and Connected Water Analysis for Real-Time Decision Making

Through Xylem Analytics and associated brands such as YSI and WTW, Xylem has a wide product portfolio of multiparameter sondes, portable meters, and online analyzers. Products such as the NH6000sc ammonia analyzer and new WTW ammonium analyzers suggest dedication to automation, low maintenance requirements, and long use life. Its HydroSphere digital platform takes these instruments' value a step further still by facilitating visualization and control of data supporting networks that provide real-time monitoring.

SUEZ S.A. – AI-Enhanced and Robotic Water Quality Monitoring Systems

SUEZ aims to combine AI, robots, and IoT-enabled sensors to improve water network testing and diagnostics at reduced costs and higher efficiency. Its "Hypervision" monitoring system and ON'connect™ distant-reading meters are behind the move. Its research collaboration agreement with CNRS running until April 2025 will yield new micropollutant detectability innovations and cement a SUEZ reputation for pairing traditional water knowhow with state-of-the-art digital technology.

Water Testing Equipment Market Report Scope

Water Testing Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.8 Billion

|

|

Market Size (2034)

|

$10.1 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Product Type (Portable Testing Equipment, Benchtop/Lab Equipment, Online/Continuous Monitoring Systems, Test Kits & Reagents), By Testing Parameter (Physical (pH, TDS, turbidity), Chemical (heavy metals, pesticides), Microbiological (bacteria, viruses), Radiological (uranium, radon)), By End-User Industry (Residential, Municipal Water & Wastewater, Industrial Sector, Environmental & Government Agencies, Commercial & Residential)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Thermo Fisher Scientific Inc.,Danaher Corporation,Xylem Inc.,SGS SA,Veolia Environnement SA,Emerson Electric Co.,Honeywell International Inc.,Agilent Technologies Inc.,LaMotte Company,YSI Incorporated,Tintometer GmbH (Lovibond®), Mettler-Toledo International Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Testing Equipment Market Segmentation

By Product Type

- Portable Testing Equipment

- pH Meters

- Dissolved Oxygen Meters

- Turbidity Meters

- Conductivity/TDS Meters

- Multi-Parameter Testers

- Benchtop/Lab Equipment

- Spectrophotometers

- Chromatography Systems

- Microbiological Testing Systems

- Online/Continuous Monitoring Systems

- IoT-Enabled Sensors

- Automated Analyzers

- Test Kits & Reagents

By Testing Parameter

- Physical (pH, TDS, turbidity)

- Chemical (heavy metals, pesticides)

- Microbiological (bacteria, viruses)

- Radiological (uranium, radon)

By End-User Industry

- Residential

- Municipal Water & Wastewater

- Treatment plant monitoring

- Regulatory compliance testing

- Industrial Sector

- Food & Beverage

- Pharmaceuticals

- Oil & Gas

- Chemical & Petrochemical

- Power Generation

- Environmental & Government Agencies

- Pollution monitoring

- Research institutions

- Commercial & Residential

- Pool & spa maintenance

- Home water quality testing

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water Testing Equipment Market

- Thermo Fisher Scientific Inc.

- Danaher Corporation

- Xylem Inc.

- SGS SA

- Veolia Environnement SA

- Emerson Electric Co.

- Honeywell International Inc.

- Agilent Technologies Inc.

- LaMotte Company

- YSI Incorporated

- Tintometer GmbH (Lovibond®)

- Mettler-Toledo International Inc.

Research Coverage

This report investigates the Global Water Testing Equipment Market, providing analysis reviews of regulatory drivers, technology innovations, and competitive strategies shaping industry growth. Published by USDAnalytics, it highlights how tightening potable water and industrial discharge regulations, demand for PFAS and microplastics testing, and breakthroughs in IoT-enabled monitoring are redefining compliance and operational efficiency. The study examines product innovations ranging from immunoassay-based analyzers to AI-driven predictive platforms, while also tracking corporate strategies such as partnerships, acquisitions, and mobile service expansions. By covering regulatory frameworks, regional investments, and disruptive trends like decentralized testing, this report highlights growth opportunities, competitive positioning, and future pathways. This report is an essential resource for manufacturers, utilities, industrial operators, policymakers, and investors seeking actionable insights into the evolving water testing equipment industry.

Scope Includes:

- Segmentation: By Product Type (Test Kits & Reagents, Portable Equipment, Laboratory Instruments, Online/Continuous Monitoring Systems), By Testing Parameter (Microbiological, Chemical, Physical, Emerging Contaminants), and By End-User (Municipal, Industrial, Commercial, Residential).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Profiles and competitive analysis of 15+ leading companies operating in the global water testing equipment market.

Methodology

The research methodology adopted by USDAnalytics combines primary interviews and secondary data sources to ensure accuracy and depth. Industry experts, regulatory authorities, technology suppliers, and end-users were consulted through surveys and structured interviews to validate trends, demand patterns, and adoption rates. Secondary data was gathered from government publications, corporate reports, peer-reviewed journals, and trade databases. Market sizing applied both top-down and bottom-up approaches, cross-verified using data triangulation and scenario modeling. This methodology ensures a comprehensive, reliable, and forward-looking assessment that supports strategic planning and decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Testing Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Professionals

1.3. Global Market Snapshot

2. Water Testing Equipment Market Overview, Size, and Growth Drivers (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $5.8 Billion

2.2.2. Forecasted Market Size (2034): $10.1 Billion at 6.3% CAGR

2.3. Market Drivers and Key Insights

2.3.1. Tightening Regulatory Mandates and Emerging Contaminants

2.3.2. Technological Advancements in Digital Monitoring

2.3.3. Decentralized and Portable Testing

3. Market Analysis: Regulatory Pressure, Technology Advancements, and Strategic Developments

3.1. Overview of Market Transformation

3.2. Regulatory Catalysts

3.2.1. PFAS Testing Surge (e.g., Veolia's U.S. Facility)

3.3. Instrument Innovation

3.3.1. Xylem's NH6000sc Ammonia Analyzer

3.3.2. Thermo Fisher Scientific's Heratherm™ Environmental Chamber

3.4. Strategic Collaboration and Company Roadmaps

3.4.1. SUEZ and CNRS Partnership

3.4.2. Hach's EcoVadis Gold Medal

4. Trends and Opportunities in Water Testing Equipment Market

4.1. Trend 1: Rapid Adoption of AI-Powered Real-Time Monitoring Systems

4.1.1. Predictive Water Quality Management

4.1.2. Decreasing Field Sample Costs

4.2. Trend 2: Portable Testing Kits for Emerging Contaminants

4.2.1. On-Location Testing for PFAS and Microplastics

4.2.2. Convenience and Regulatory Compliance

4.3. Opportunity 1: Military and Disaster Response Applications

4.3.1. Demand for Rugged and Portable Instruments

4.3.2. Ensuring Water Safety in Resource-Scarce Situations

4.4. Opportunity 2: Agricultural Runoff Monitoring

4.4.1. Testing for Nutrient and Pesticide Runoff

4.4.2. Informing Mitigation Practices and Sustainability

5. Water Testing Equipment Market Share Insights

5.1. By Product Type

5.1.1. Test Kits & Reagents

5.1.2. Portable Testing Equipment

5.1.3. Benchtop/Lab Equipment

5.1.4. Online/Continuous Monitoring Systems

5.2. By Testing Parameter

5.2.1. Microbiological Testing

5.2.2. Chemical Testing

5.2.3. Physical and Radiological Testing

5.3. By End-User Industry

5.3.1. Municipal Water & Wastewater

5.3.2. Industrial Sector

5.3.3. Environmental & Government Agencies

5.3.4. Commercial & Residential

6. Country Analysis of the Water Testing Equipment Market

6.1. United States: PFAS and Lead Testing Infrastructure

6.2. China: Government-Led Standards and Smart Monitoring

6.3. India: IoT-Enabled Water Quality Monitoring

6.4. Germany: Green Technology and Microplastic Detection

6.5. Japan: Advanced IoT and AI-Driven Analytics

6.6. Saudi Arabia: National Water Strategy Spurs Demand

6.7. Other Country Analysis

7. Water Testing Equipment Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Product Type, Parameter, and End-User

7.2. Europe Market Size Outlook to 2034

7.2.1. By Product Type, Parameter, and End-User

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Product Type, Parameter, and End-User

7.4. South America Market Size Outlook to 2034

7.4.1. By Product Type, Parameter, and End-User

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Product Type, Parameter, and End-User

8. Company Profiles: Top Companies in Water Testing Equipment Market

8.1. Danaher Corporation (Veralto)

8.2. Thermo Fisher Scientific Inc.

8.3. Xylem Inc.

8.4. SUEZ S.A.

8.5. SGS SA

8.6. Veolia Environnement SA

8.7. Emerson Electric Co.

8.8. Honeywell International Inc.

8.9. Agilent Technologies Inc.

8.10. LaMotte Company

8.11. YSI Incorporated

8.12. Tintometer GmbH (Lovibond®)

8.13. Mettler-Toledo International Inc.

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations

Water Testing Equipment Market Segmentation

By Product Type

· Portable Testing Equipment

• pH Meters

• Dissolved Oxygen Meters

• Turbidity Meters

• Conductivity/TDS Meters

• Multi-Parameter Testers

· Benchtop/Lab Equipment

• Spectrophotometers

• Chromatography Systems

• Microbiological Testing Systems

· Online/Continuous Monitoring Systems

• IoT-Enabled Sensors

• Automated Analyzers

· Test Kits & Reagents

By Testing Parameter

· Physical (pH, TDS, turbidity)

· Chemical (heavy metals, pesticides)

· Microbiological (bacteria, viruses)

· Radiological (uranium, radon)

By End-User Industry

· Residential

· Municipal Water & Wastewater

• Treatment plant monitoring

• Regulatory compliance testing

· Industrial Sector

• Food & Beverage

• Pharmaceuticals

• Oil & Gas

• Chemical & Petrochemical

• Power Generation

· Environmental & Government Agencies

• Pollution monitoring

• Research institutions

· Commercial & Residential

• Pool & spa maintenance

• Home water quality testing

Countries Analyzed

· North America (US, Canada, Mexico)

· Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

· Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

· South America (Brazil, Argentina, Rest of South America)

· Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)