Waterborne Epoxy Resins Market Growth Accelerated by Low-VOC Mandates and High-Performance Industrial Applications

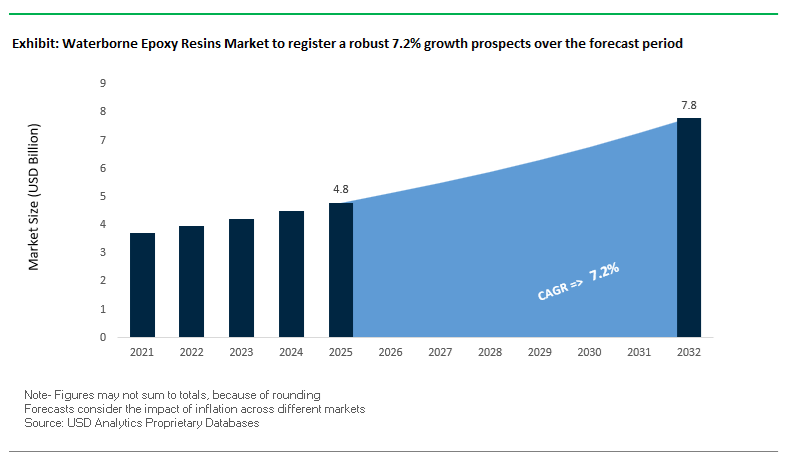

The global Waterborne Epoxy Resins Market reached $4.8 billion in 2025 and is projected to grow at a CAGR of 7.2% through 2032, attaining $7.8 billion by 2032. This above-average growth rate—relative to broader coatings segments—reflects the increasing shift toward low-VOC, high-performance resin systems across industrial coatings, infrastructure, automotive OEM, wind energy, and protective applications. Waterborne epoxy resins are gaining strong adoption due to their superior adhesion, corrosion resistance, chemical durability, and environmental compliance, positioning them as a critical alternative to solvent-based epoxies.

A primary market driver is the tightening of global VOC emission regulations, particularly in North America and Europe, which is compelling manufacturers to transition toward waterborne epoxy dispersions and hybrid systems. These formulations enable compliance without compromising on performance, especially in demanding applications such as marine coatings, bridge infrastructure, oil & gas assets, and heavy industrial flooring. Additionally, the rise of renewable energy infrastructure—particularly wind power—and electric vehicle manufacturing is driving demand for epoxy systems that offer rapid curing, mechanical strength, and long-term durability under extreme environmental conditions.

Technological advancements are further enhancing the competitiveness of waterborne epoxy resins. Innovations in amine-based curing agents, hybrid latex-epoxy systems, and bio-based resin formulations are improving flexibility, impact resistance, and application efficiency. The integration of natural rubber-modified epoxy systems and cashew-derived curing agents demonstrates a broader industry shift toward bio-based chemistry and circular material innovation. Furthermore, manufacturers are focusing on high-molecular-weight dispersions and BPA-free formulations, particularly in food packaging and coil coating applications, to meet evolving regulatory and safety standards.

Market Analysis: Shift Toward Specialty Epoxy Systems, Capacity Expansion, and Regulatory Pressure Reshaping Market Dynamics

The Waterborne Epoxy Resins Market is experiencing a structural shift driven by capacity rationalization, specialty product innovation, and regulatory acceleration, redefining competitive dynamics across the value chain. A notable development is Olin Corporation’s strategic pivot (February 2026) following its credit rating downgrade to ‘BB’. In response to global overcapacity in commodity epoxy resins, the company is prioritizing high-margin, specialized waterborne epoxy systems, signaling a broader industry move away from commoditized products toward value-added formulations.

Strategic consolidation and R&D integration are also reshaping innovation pipelines. The ongoing AkzoNobel–Axalta merger (March 2026) has initiated the consolidation of resin research, with a focus on developing unified waterborne epoxy basecoat platforms that combine automotive mobility coatings with industrial wood and flooring technologies. This integration is expected to accelerate the commercialization of cross-functional epoxy systems tailored to multiple end-use sectors.

Capacity expansion remains critical to meeting rising global demand. Huntsman’s commissioning of its amine-based curing facility (January 2026)—powered by green energy—targets the growing need for rapid-cure epoxy systems in infrastructure and renewable energy projects. Similarly, Allnex’s 2025 expansion in China strengthens its ability to supply low-emission waterborne epoxy resins to the rapidly growing Asian automotive and industrial markets. These investments highlight the importance of localized production and supply chain resilience.

Product innovation is increasingly focused on durability and sustainability. Olin’s launch of durability-enhanced curing agents (February 2025) improves chemical resistance and lifecycle performance in harsh environments such as maritime and oil & gas infrastructure. Meanwhile, Cardolite’s NX-8402 zero-VOC curing agent, derived from cashew nutshell liquid, demonstrates the viability of bio-based alternatives that deliver high-performance corrosion resistance. In parallel, Kukdo Chemical’s expansion of BPA-free waterborne epoxy dispersions addresses tightening European regulations on food-contact materials, particularly in packaging and coil coatings.

Regulatory pressure continues to act as a major catalyst. The U.S. EPA’s finalization of VOC emission amendments (January 2025) has accelerated the industry-wide transition toward waterborne epoxy technologies, forcing manufacturers to reformulate product portfolios. Additionally, Nan Ya Plastics’ low-carbon transformation strategy emphasizes the integration of recyclable and water-soluble epoxy precursors, particularly for high-growth sectors such as AI infrastructure and wind energy.

Emerging research is also influencing commercial innovation. A 2025 study published in Scientific Reports on natural rubber-latex epoxy hybrids is being adopted by industry players to enhance flexibility and impact resistance in flooring applications, signaling the growing role of material science convergence in next-generation epoxy systems.

Market Trend: EU Regulation (EU) 2024/3190 Accelerating BPA-Free Waterborne Epoxy Resin Adoption

The enforcement of EU Regulation (EU) 2024/3190 is significantly reshaping the waterborne epoxy resins market, particularly within food-contact coatings and packaging applications. The prohibition of Bisphenol A and other hazardous bisphenols has established a new regulatory baseline for epoxy-based varnishes and coatings across Europe.

Although the regulation came into force on January 20, 2025, the transition period allowing legacy compliant products extends until July 20, 2026, creating a critical window for manufacturers to reformulate. This regulatory shift is accelerating the adoption of BPA-free epoxy resins and non-bisphenol precursors in waterborne coating systems, especially in food and beverage packaging sectors.

The 2026 compliance environment is defined by extremely stringent safety thresholds, with the European Food Safety Authority setting a tolerable daily intake of just 0.2 nanograms per kilogram of body weight. This effectively mandates non-detectable migration levels, pushing manufacturers toward ultra-pure raw materials and advanced polymer chemistries that eliminate residual monomers. This trend is driving innovation in food-safe coatings and sustainable epoxy resin technologies aligned with global health and safety standards.

Market Trend: China GB 9685-2016 Amendment Driving Low-Migration and Low-VOC Epoxy Coatings

The amendment to China’s GB 9685-2016 standard, introduced in 2025 and enforced through 2026, is raising the bar for waterborne epoxy coatings used in food-contact applications. The updated regulation focuses on stricter migration limits and enhanced purity requirements, targeting residual monomers and secondary aromatic amines that can impact food safety.

Manufacturers are required to meet more stringent specific migration limits, accelerating the development of low-migration epoxy coatings and high-purity resin systems. This is particularly relevant in the food processing and beverage packaging industries, where regulatory compliance is critical for market access.

In parallel, China is aligning its VOC emission standards with the European Industrial Emissions Directive, mandating VOC levels below 30 g/L for waterborne epoxy coatings used in new facilities. This is reinforcing the global shift toward low-VOC coatings and environmentally sustainable industrial coatings, strengthening the demand for advanced waterborne epoxy resin formulations in Asia-Pacific markets.

Market Opportunity: High-Solids Waterborne Epoxy Resins Driving Industrial Flooring Innovation

The transition toward high-solids waterborne epoxy systems is creating significant opportunities in the industrial flooring coatings market. These advanced formulations combine the durability of solvent-based high-build coatings with the environmental benefits of waterborne systems, addressing both performance and regulatory requirements.

Modern waterborne epoxy resins with solids content of 50% or higher are capable of achieving dry film thickness levels of 10 to 20 mils in a single application. This high-build capability reduces the number of coating passes required and shortens overall drying time by approximately 30%, improving application efficiency in large-scale industrial projects.

These coatings are engineered to deliver compressive strength of 60 MPa or higher, ensuring durability under heavy mechanical stress from forklifts and industrial machinery. This makes them highly suitable for warehouses, manufacturing plants, and logistics centers where load-bearing performance is critical.

In addition, high-solids waterborne epoxy coatings demonstrate strong adhesion to damp or green concrete, achieving pull-off adhesion values of at least 3.0 MPa on substrates cured for only 7 to 10 days. This significantly reduces construction timelines and enhances project flexibility, positioning these coatings as a preferred solution in fast-track industrial developments.

Market Opportunity: Low-Temperature Cure Waterborne Epoxy Systems Enabling Infrastructure Coatings Expansion

Advancements in low-temperature curing technologies are unlocking new opportunities for waterborne epoxy resins in infrastructure coatings, particularly in bridge protection and cold-weather applications. Traditional epoxy systems have been limited by high minimum curing temperatures, but 2026 innovations are overcoming this barrier.

Next-generation waterborne epoxy dispersions, combined with advanced amine-functional curing agents, are capable of achieving full cure at temperatures as low as 5°C within 24 hours. This represents a significant improvement over legacy systems that required temperatures of 15°C or higher, enabling year-round application in colder climates.

These coatings also demonstrate excellent corrosion resistance, achieving over 1,000 hours of salt spray resistance under ASTM B117 testing without blistering or delamination. This level of performance ensures long-term protection for steel structures in harsh environmental conditions, making them ideal for bridges, offshore infrastructure, and industrial facilities.

Thermal stability is another critical advantage, with low-temperature curing systems achieving glass transition temperatures above 50°C within seven days of application at 10°C. This ensures that coatings maintain their structural integrity during temperature fluctuations, particularly during seasonal transitions. These advancements are positioning waterborne epoxy coatings as a key solution in sustainable infrastructure development and protective coatings markets.

Waterborne Epoxy Resins Market Share and Segmentation Insights

Two-Component (2K) Systems Lead with 54.8% Share Due to High-Performance Protection

The two-component (2K) segment dominates the waterborne epoxy resins market with a leading 54.8% market share in 2025, driven by its superior chemical resistance, adhesion strength, and corrosion protection capabilities. In the waterborne epoxy coatings and industrial protective coatings market, 2K systems are widely used for industrial flooring, concrete sealers, metal primers, and heavy-duty coatings, offering performance levels comparable to traditional solvent-borne epoxies. A key technological advantage is the extended pot life of 4–12 hours, allowing applicators sufficient working time while maintaining efficient curing cycles for large-scale projects. These systems are particularly valued in infrastructure, manufacturing plants, and marine applications, where durability and resistance to harsh chemicals and environmental conditions are critical. As industries shift toward low-VOC, environmentally compliant coating systems, 2K waterborne epoxies continue to lead innovation and adoption in the global waterborne epoxy resins market.

Direct Sales Channel Dominates with 51.9% Share Through Technical Support and Custom Solutions

The direct sales segment leads the waterborne epoxy resins market by sales channel with a 51.9% market share in 2025, supported by the need for technical expertise, formulation precision, and application support. Within the industrial coatings and specialty chemicals market, waterborne epoxy systems require accurate mixing ratios, controlled application conditions, and performance optimization, making direct manufacturer involvement essential. Suppliers work closely with industrial users, contractors, and OEMs to ensure proper system performance in applications such as protective coatings, flooring systems, and corrosion-resistant finishes. Additionally, large-scale customers demand customized epoxy formulations tailored to specific substrates, cure speeds, and environmental conditions, which can only be achieved through direct collaboration. This model enables consistent quality, technical guidance, and long-term supply agreements, reinforcing the dominance of direct sales in the global waterborne epoxy resins market supply chain.

Competitive Landscape Analysis of the Waterborne Epoxy Resins Market

Olin Leads Integrated Waterborne Epoxy Resin Supply for EV Battery Safety

Olin Corporation remains the world’s largest integrated epoxy resin manufacturer, with its 2026 strategy centered on higher-margin waterborne epoxy dispersions and value-added specialties. The company commercialized the D.E.R.™ 900 Series in early 2026 for EV battery enclosures, offering strong dielectric performance and fire retardancy. Olin has shifted 40% of Blue Cube epoxy capacity toward waterborne and low-carbon solvent-free variants to meet LEED and REACH mandates. Its vertically integrated chlor-alkali platform secures epichlorohydrin supply, helping protect its waterborne epoxy portfolio from raw material volatility.

Hexion Advances Bio-Circular Waterborne Epoxy Systems for Industrial Floors and Wind Energy

Hexion Inc., now integrated into Westlake Epoxy, is strengthening the waterborne epoxy resins market through its EpoVIVE™ bio-circular epoxy portfolio, designed to reduce the carbon footprint of industrial floor coatings by 30%. Its AQUAREOUS™ epoxy systems combine resins and waterborne amine hardeners into a single-source solution, simplifying formulation for Tier-1 coating manufacturers. Hexion also dominates the wind energy coatings segment, supplying waterborne epoxy primers for turbine blades with UV resistance and edge retention. Its R&D focus on Bisphenol-A alternatives positions the company ahead of expected EU and North American regulatory shifts.

Huntsman Scales ARALDITE Waterborne Epoxies for Aerospace and Marine Coatings

Huntsman Corporation is expanding its waterborne epoxy resins market presence through regulatory-driven innovation in aerospace and protective coatings. At SAMPE 2026, the company emphasized compliance-led development while scaling ARALDITE® waterborne epoxy systems for aerospace OEMs managing record production backlogs. Its URALANE® 5774-1 water-based FST-compliant adhesive/coating improves bonding to high-performance thermoplastics by 20% for aircraft interiors. Huntsman’s Advanced Materials division reported USD 6 billion in 2025 revenue, with waterborne composite and coating systems growing at 7.2% CAGR. A new German reactor supports demand for sustainable marine and protective coatings in the North Sea region.

allnex Innovates Decorative and Non-Isocyanate Waterborne Epoxy Technologies

allnex, a PTG company, is differentiating in the waterborne epoxy resins market with specialty hardeners, non-isocyanate chemistry, and sustainable resin platforms. At ACS 2026, it showcased BECKOPOX™ EH 2162w, enabling liquid-metal and acid-stain concrete aesthetics without hazardous acid processes. Its ACURE® AQ system introduces a waterborne non-isocyanate technology with rapid-cure 2K epoxy-urethane hybrid performance. The ECOWISE™ CHOICE portfolio now includes rPET-based waterborne resins for improved adhesion to challenging plastic substrates in consumer electronics. allnex also offers ADDITOL® XW 6602, a defoamer engineered to prevent micro-foam during high-shear waterborne epoxy application.

Kukdo Expands Asia-Pacific Waterborne Epoxy Scale With Green PCB Coatings

Kukdo Chemical Co., Ltd. dominates Asia-Pacific waterborne epoxy resin production, benefiting from the region’s 47.05% share of the global waterborne market. The company generates 94% of its revenue, 1.51T KRW, from epoxy products and operates some of the world’s largest continuous epoxy resin production lines. In February 2026, Kukdo expanded its Green Epoxy line for PCB manufacturers, offering halogen-free, high-Tg waterborne insulating coatings. Its scale enables competitive pricing for bisphenol-A and bisphenol-F waterborne dispersions. By expanding logistics hubs in the Americas and Europe, Kukdo aims to raise waterborne resin exports by 20% by 2027.

China’s High-End Transformation and Strategic Consolidation in Waterborne Epoxy Resins

China remains the dominant force in the waterborne epoxy resins market, transitioning from large-scale commodity production to high-value specialty systems. This strategic shift is supported by significant capacity expansions, such as Hongchang Electronics’ Zhuhai Phase II project, which has introduced advanced closed-loop waterborne processing to enhance efficiency and reduce production costs. The country is also focusing on localizing high-end materials, with major restructuring initiatives aimed at strengthening domestic supply chains for semiconductor and new energy applications.

Technological advancement is a key priority, particularly in the development of ultra-low chlorine waterborne epoxy resins for electronic applications such as epoxy molding compounds (EMC) used in 5G and AI chips. Environmental regulations are further accelerating the transition, with government mandates pushing manufacturers toward water-based dispersions that comply with strict VOC standards. Infrastructure projects, including bridges and maritime developments, are increasingly specifying waterborne epoxy zinc-rich primers, boosting demand for surfactant-stabilized systems. Additionally, favorable trade developments have reopened export opportunities for high-performance waterborne epoxy resins, reinforcing China’s global market position.

United States: Infrastructure Investments and PFAS-Free Innovation Driving Demand

The United States waterborne epoxy resins market is undergoing a transformation driven by federal infrastructure spending and stringent chemical safety regulations. The Infrastructure Investment and Jobs Act (IIJA) is a major catalyst, with large-scale bridge rehabilitation projects specifying waterborne epoxy concrete sealers for enhanced durability and environmental compliance. This trend underscores the growing preference for water-based epoxy systems in heavy-duty infrastructure applications.

Regulatory pressures are also reshaping the market landscape. The elimination of PFAS-based additives is accelerating the development of safer, environmentally compliant formulations. Tightening VOC limits, particularly in California, are further driving the shift toward ultra-low VOC waterborne epoxy technologies. Innovation is expanding into renewable energy applications, with advanced epoxy systems being used in offshore wind turbine manufacturing. Additionally, the expansion of EV charging infrastructure is increasing demand for waterborne epoxy encapsulants, while the commercial flooring segment is witnessing strong growth in bio-based epoxy dispersions aligned with green building standards.

Germany: Circular Economy Leadership and High-Performance Epoxy Innovations

Germany continues to lead the European waterborne epoxy resins market, driven by stringent environmental standards and advanced R&D capabilities. The focus on indoor air quality and sustainability is evident in the development of low-emission epoxy dispersions designed for commercial flooring applications. Compliance with regulations such as REACH ensures the continued use of safe and environmentally friendly epoxy systems across sensitive sectors, including food packaging.

The country is also advancing innovation in renewable energy and emerging technologies. Waterborne epoxy coatings are being developed for hydrogen storage infrastructure, requiring zero-porosity performance to prevent material degradation. Public procurement policies are reinforcing demand, with government tenders mandating the use of environmentally certified waterborne epoxy systems in schools and hospitals. Research into self-crosslinking epoxy-acrylic hybrids is enabling high-performance coatings with reduced application complexity and waste. Additionally, trade protections such as anti-dumping duties are supporting domestic manufacturers, allowing them to scale production and strengthen their competitive position in the global market.

India: Expanding Domestic Capacity and Renewable Energy Integration

India is emerging as a high-growth market for waterborne epoxy resins, driven by industrial expansion and increasing investments in renewable energy infrastructure. Major capacity expansions, including large-scale projects in Gujarat, are significantly boosting domestic production of epoxy resins with a strong focus on waterborne technologies. These developments are aligned with the government’s “Make in India” initiative, which aims to strengthen local manufacturing capabilities.

Renewable energy projects are a major demand driver, with increasing installations of wind energy infrastructure requiring high-performance epoxy coatings for turbine protection. The growth of the electric vehicle ecosystem is also contributing to demand, particularly for fire-retardant coatings used in battery insulation. Urban infrastructure initiatives such as the Smart Cities Mission are further driving the adoption of waterborne epoxy anti-carbonation coatings in public transport and construction projects. Additionally, collaborations in recyclable materials for wind farms highlight India’s commitment to sustainable innovation in epoxy resin technologies.

Japan: High-Purity Resins and Infrastructure Longevity

Japan’s waterborne epoxy resins market is defined by its focus on high-purity materials and long-lasting performance in critical applications. Government-backed initiatives are supporting the development of advanced epoxy systems for the semiconductor industry, ensuring a stable supply of high-performance materials for electronic packaging and next-generation technologies.

Infrastructure maintenance is another key focus area, with waterborne epoxy-zinc systems being widely adopted for bridge protection to achieve long maintenance cycles. Regulatory developments in food safety are also driving the adoption of BPA-NI waterborne epoxy liners in packaging applications. Innovation extends to advanced composite materials, with epoxy-nano-silica hybrids offering enhanced thermal and electrical performance. Urban sustainability initiatives, such as cool roof programs, are further boosting demand for waterborne epoxy coatings. Additionally, the integration of robotic application technologies is improving efficiency in prefabricated housing and industrial coating processes.

Brazil: Regulatory Evolution and Maritime Sector Driving Market Growth

Brazil plays a crucial role in the Latin American waterborne epoxy resins market, supported by evolving regulations and strong demand from maritime and industrial sectors. Government policies aimed at reducing solvent emissions are accelerating the shift toward waterborne epoxy systems, particularly in applications such as food packaging and construction adhesives.

Maritime environmental regulations are a significant growth driver, with increasing adoption of waterborne antifouling coatings in major ports. The country is also benefiting from investments in renewable energy infrastructure, particularly offshore wind projects, which require advanced epoxy coatings for corrosion protection. Regulatory frameworks such as the National Inventory of Chemical Substances are encouraging the use of safer, water-based epoxy formulations. Additionally, the expansion of the aerospace sector is driving demand for high-performance epoxy coatings, supporting the development of a domestic supply chain that aligns with global environmental standards.

Waterborne Epoxy Resins Market Report Scope

Waterborne Epoxy Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2032)

|

$7.8 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Molecular Weight (High Molecular Weight, Low Molecular Weight), By Product Form (Liquid Epoxy, Solid Epoxy, Semi-Solid), By Component (Single Component, Two Component, Aqueous Dispersions, Water-Reducible Resins), By End-User Industry (Construction and Infrastructure, Automotive and Transportation, Electrical and Electronics, Packaging, Aerospace and Marine, Wind Energy), By Sales Channel (Direct Sales, Specialty Chemical Distributors, Wholesalers and Trade Suppliers)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hexion Inc., Olin Corporation, Huntsman Corporation, Aditya Birla Chemicals, Allnex GmbH, Kukdo Chemical Co., Ltd., Evonik Industries AG, Nan Ya Plastics Corporation, DIC Corporation, Cardolite Corporation, Adeka Corporation, Reichhold LLC, Mitsubishi Chemical Group, Arclin, Inc., Gabriel Performance Products

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Waterborne Epoxy Resins Market Segmentation

By Molecular Weight

- High Molecular Weight

- Low Molecular Weight

By Product Form

- Liquid Epoxy

- Solid Epoxy

- Semi-Solid

By Component

- Single Component

- Two Component

- Aqueous Dispersions

- Water-Reducible Resins

By End-User Industry

- Construction and Infrastructure

- Automotive and Transportation

- Electrical and Electronics

- Packaging

- Aerospace and Marine

- Wind Energy

By Sales Channel

- Direct Sales

- Specialty Chemical Distributors

- Wholesalers and Trade Suppliers

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Waterborne Epoxy Resins Industry

- Hexion Inc.

- Olin Corporation

- Huntsman Corporation

- Aditya Birla Chemicals

- Allnex GmbH

- Kukdo Chemical Co., Ltd.

- Evonik Industries AG

- Nan Ya Plastics Corporation

- DIC Corporation

- Cardolite Corporation

- Adeka Corporation

- Reichhold LLC

- Mitsubishi Chemical Group

- Arclin, Inc.

- Gabriel Performance Products

*- List not Exhaustive