Waterborne Industrial Coatings Market Expansion Driven by EV Manufacturing, Infrastructure Demand, and Low-VOC Compliance

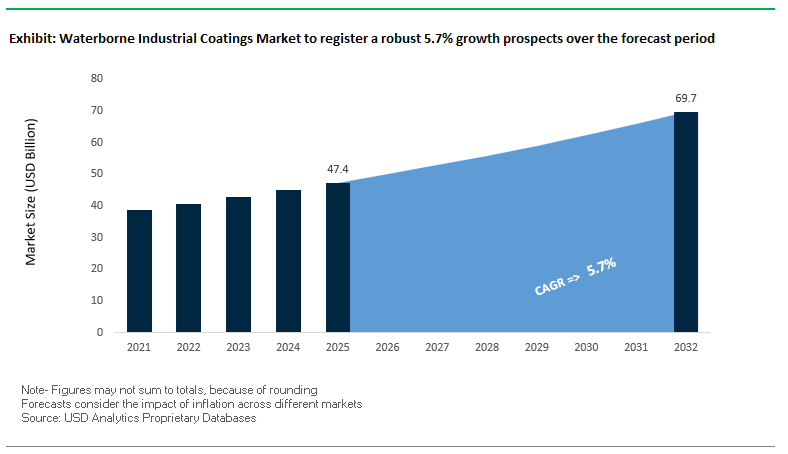

The global Waterborne Industrial Coatings Market was valued at $47.4 billion in 2025 and is projected to grow at a CAGR of 5.7% from 2025 to 2032, reaching $69.9 billion by 2032. This growth is underpinned by the accelerating transition toward low-VOC, environmentally compliant industrial coatings, particularly across automotive OEM, heavy infrastructure, machinery, and energy sectors. Waterborne industrial coatings are increasingly replacing solvent-based systems due to their reduced emissions, improved worker safety, regulatory compliance, and competitive lifecycle performance.

A key growth driver is the rapid expansion of electric vehicle (EV) manufacturing ecosystems, which require advanced coating systems for battery enclosures, thermal management, corrosion protection, and lightweight substrates. Waterborne coatings are being engineered to deliver high adhesion, chemical resistance, and durability, even under extreme thermal and environmental stress. Additionally, large-scale investments in water infrastructure, renewable energy projects, and industrial modernization are significantly boosting demand for protective coatings capable of withstanding harsh operational conditions.

Technological advancements in polymer dispersions, hybrid coatings (waterborne-powder systems), and fast-curing formulations are enhancing the performance capabilities of waterborne industrial coatings. These innovations are enabling improved film formation, corrosion resistance, and substrate compatibility, making them viable for heavy-duty industrial applications such as marine, oil & gas, and municipal infrastructure. Furthermore, the increasing integration of smart coatings with thermal regulation, anti-corrosion, and energy-efficiency features is expanding the functional scope of waterborne systems.

Sustainability remains a central market force. Manufacturers are focusing on bio-based raw materials, carbon footprint reduction, and circular production processes, aligning with global decarbonization goals and tightening environmental regulations.

Market Analysis: Strategic Divestments, EV-Focused Innovation, and Digital Logistics Reshaping Industrial Coatings Landscape

The Waterborne Industrial Coatings Market is undergoing a structural transformation driven by corporate restructuring, EV-centric product innovation, and supply chain optimization, redefining competitive dynamics across global markets. A major development is the March 2026 leadership transition at BASF Coatings, as it prepares to operate as a standalone entity under new CEO Jens Luehring. This shift is expected to accelerate entrepreneurial decision-making and innovation in sustainable industrial coatings, particularly in automotive OEM and advanced surface treatment applications.

Strategic portfolio optimization is also shaping market positioning. In February 2026, AkzoNobel completed the divestment of its Indian business, generating €922 million and enabling a sharper focus on high-growth waterborne industrial segments in Europe and China. This move aligns with broader industry trends toward capital reallocation and margin optimization in core markets.

Operational efficiency and digitalization are becoming key differentiators. Nippon Paint’s expansion of its Direct-to-Factory (D2F) logistics model—with 70% of industrial orders in Shanghai now processed through this system—demonstrates the increasing importance of streamlined supply chains and direct customer engagement, particularly in high-end manufacturing environments such as clean rooms and precision industries.

Capacity expansion and regional manufacturing strategies continue to support market growth. PPG’s Thailand-based waterborne coatings plant (March 2025), with a 2,000-ton annual capacity, strengthens its position as a regional hub for automotive coatings, particularly for Chinese EV manufacturers expanding across Southeast Asia. Meanwhile, Axalta’s record 22% adjusted EBITDA margin in 2025 highlights the profitability potential of high-margin waterborne refinish systems and localized production strategies.

Innovation is increasingly centered on EV and infrastructure applications. Jotun’s launch of EV battery coating solutions (June 2025) integrates waterborne hybrid technologies to address thermal management and corrosion protection challenges, particularly mitigating risks such as thermal runaway in high-voltage systems. Similarly, Sherwin-Williams’ involvement in the Sioux Falls water infrastructure project underscores the growing adoption of waterborne protective coatings in municipal and heavy industrial environments, where durability and environmental compliance are critical.

Further reinforcing market evolution, Hempel’s launch of Hempaguard NB silicone hull coating complements its waterborne industrial portfolio, while Farrow & Ball’s Flat Eggshell finish demonstrates the convergence of aesthetic performance and industrial-grade durability, expanding the applicability of waterborne coatings across diverse substrates including metal and concrete.

Market Trend: EPA NESHAP 2025–2026 Enforcement Accelerating Waterborne Industrial Coatings Adoption

The enforcement of EPA National Emission Standards for Hazardous Air Pollutants under 40 CFR Part 63 is significantly transforming the waterborne industrial coatings market, particularly across metal parts manufacturing and coating production facilities. The 2025–2026 compliance milestones under Subpart MMMM and Subpart HHHHH are driving a decisive shift toward low-HAP and low-VOC waterborne coatings as industrial operators seek cost-effective compliance strategies.

Facilities are now required to meet stringent metal hazardous air pollutant limits, including thresholds such as 0.014 gr/dscf for existing emission sources. This is forcing a move away from solvent-borne coatings that rely on high-load HAP-containing materials, accelerating demand for environmentally compliant waterborne industrial coatings.

A critical economic driver behind this transition is the high capital expenditure associated with solvent abatement technologies. The installation of regenerative thermal oxidizers, often exceeding $1 million in cost, is becoming increasingly unviable for many operators. As a result, waterborne coating systems are emerging as a preferred solution to bypass complex emission control infrastructure while maintaining regulatory compliance. This trend is strengthening the adoption of sustainable industrial coatings across manufacturing sectors.

Market Trend: China GB 30981.2-2025 Standard Driving Low-VOC and Low-Toxicity Industrial Coatings

The introduction of China’s GB 30981.2-2025 standard is establishing a new regulatory framework for the waterborne industrial coatings market, with full enforcement scheduled for June 1, 2026. This regulation replaces the earlier GB 30981-2020 standard and serves as a comprehensive mandate to limit harmful substances and VOC emissions in industrial coatings.

The 2026 standard enforces VOC concentration limits of 300 g/L or lower for heavy-duty corrosion protection coatings, with green-certified formulations targeting VOC levels below 100 g/L. This is accelerating the adoption of waterborne industrial primers and protective coatings that meet both environmental and performance requirements.

In addition to VOC restrictions, the regulation imposes cumulative limits on hazardous substances such as formaldehyde, benzene, and polycyclic aromatic hydrocarbons. These requirements are driving the use of high-purity waterborne resin dispersions and advanced formulation technologies that ensure safety without compromising durability. This regulatory shift is promoting the development of high-performance, low-toxicity coatings across China’s industrial and infrastructure sectors.

Market Opportunity: Waterborne Epoxy-PUD Hybrid Coatings Driving Offshore Wind Infrastructure Protection

The rapid expansion of offshore wind energy installations is creating significant growth opportunities for waterborne epoxy-polyurethane hybrid coatings. With global offshore wind capacity projected to reach 140 GW annually in 2026, the demand for durable and corrosion-resistant coatings is increasing across marine infrastructure applications.

Waterborne epoxy-PUD hybrid systems are engineered to deliver enhanced erosion resistance, reducing maintenance frequency by approximately 30% compared to traditional coating systems. This is particularly valuable in offshore environments where maintenance operations are complex and costly, often exceeding $100,000 per service intervention.

These coatings are capable of achieving over 2,000 hours of salt spray resistance under ASTM B117 testing, meeting the stringent C5-M marine corrosion classification required for long-term structural protection. This performance ensures a service life of up to 25 years for offshore wind towers and related infrastructure.

Additionally, UV stability is significantly improved through the integration of polyurethane dispersion technology, with coatings maintaining color stability characterized by a ΔE value below 0.5 after 4,000 hours of xenon-arc exposure. This ensures long-term aesthetic and functional performance in high-exposure maritime conditions, positioning waterborne hybrid coatings as a critical solution in renewable energy infrastructure.

Market Opportunity: Waterborne Railcar Coatings Enabling Fleet Modernization and Asset Preservation

The global railcar coatings market is undergoing a transformation toward asset preservation strategies, creating strong opportunities for waterborne industrial coatings in both exterior and interior applications. With railcar coating volumes projected to reach 218.6 kilotons in 2026, waterborne systems are gaining traction due to their safety, durability, and regulatory compliance advantages.

Modern waterborne rail enamels are achieving drying performance comparable to solvent-borne coatings, with dry-to-handle times below 60 minutes at standard conditions of 25°C. This allows manufacturers to maintain production throughput while reducing fire and explosion risks in enclosed railcar painting facilities.

For chemical freight applications, waterborne epoxy liner systems are engineered to provide resistance across a wide pH range from 2 to 12, enabling safe transport of diverse industrial chemicals. This versatility enhances the operational efficiency of rail logistics networks.

Performance durability is further reinforced by strong adhesion and impact resistance properties. Waterborne coatings achieve 5B cross-hatch adhesion and impact resistance exceeding 160 inch-pounds, ensuring resistance to mechanical stress during transportation. This prevents micro-cracking and under-film corrosion, extending the service life of rail assets and reducing maintenance costs across the rail transportation sector.

Waterborne Industrial Coatings Market Share and Segmentation Insights

Waterborne Dispersions Lead with 57.5% Share Due to Versatility and Regulatory Compliance

The waterborne dispersions segment dominates the waterborne industrial coatings market with a 57.5% market share in 2025, driven by its broad substrate compatibility, low-VOC formulation, and high-performance durability. In the industrial coatings and environmentally friendly surface finishing market, waterborne dispersions—including acrylic, polyurethane, and epoxy hybrid systems—are extensively used across metal, plastic, and wood substrates, making them highly versatile for diverse industrial applications. These coatings deliver excellent adhesion, corrosion resistance, and weatherability, meeting the performance demands of automotive, machinery, appliance, and general industrial sectors. A major growth driver is the increasing adoption of waterborne basecoats and topcoats in OEM and refinish applications, as manufacturers comply with stringent environmental regulations such as EPA, CARB, and the EU Industrial Emissions Directive. As industries prioritize sustainable, high-performance coatings, waterborne dispersions continue to lead the global waterborne industrial coatings market.

Direct Sales Channel Dominates with 53.2% Share Through OEM Partnerships and Custom Solutions

The direct sales segment leads the waterborne industrial coatings market by sales channel with a 53.2% market share in 2025, supported by strong demand from large-scale OEM manufacturers and industrial users. Within the industrial coatings supply chain and advanced manufacturing market, sectors such as automotive, heavy equipment, and appliances rely on direct procurement to integrate coatings into high-speed, automated production lines. This approach ensures consistent coating quality, optimized curing performance, and seamless compatibility with manufacturing processes. Additionally, direct supplier relationships enable the development of custom formulations tailored to specific industrial requirements, including precise color matching, gloss levels, corrosion protection, and substrate adhesion. OEMs benefit from technical support, formulation expertise, and long-term supply agreements, enhancing operational efficiency and product quality. This combination of customization, scale, and integration reinforces the dominance of direct sales in the global waterborne industrial coatings market.

Competitive Landscape Analysis of the Waterborne Industrial Coatings Market

AkzoNobel Strengthens Waterborne Industrial Coatings Leadership Through Axalta Merger

AkzoNobel N.V. is reinforcing its position in the waterborne industrial coatings market through its April 2026 all-stock merger agreement with Axalta, creating a pure-play coatings leader with stronger R&D in water-reducible industrial systems. The company reported an 80 bps profitability improvement in Q1 2026, supported by pricing and cost discipline. Its Rhythm of Blues 2026 Color of the Year uses specialized waterborne resins to improve opacity and edge-hide across architectural and industrial coatings. AkzoNobel’s Dubai Aerospace Coatings Hub, opening in Q2 2026, will cut regional lead times by 30%, while its AI-powered drone inspection tool reduces aircraft and industrial maintenance turnby 15–20%.

PPG Expands Waterborne Industrial Coatings Through Ozark Materials and UV/EB Innovation

PPG Industries, Inc. dominates the general industrial waterborne coatings segment, which represents 17% of the global waterborne market. In early 2026, its sustainably advantaged products, including water-based systems, accounted for 43% of total revenue. The April 2026 acquisition of Ozark Materials expanded PPG’s presence in waterborne pavement markings and infrastructure safety coatings, supported by a 64% global adoption rate of low-VOC mandates. PPG is also advancing radiation-curable waterborne coatings at its Marly, France testing facility to deliver instant-dry performance for appliance and electronics manufacturing. Its DELTRON® NXT waterborne system uses machine learning to reduce automotive paint-shop waste by 12%.

Sherwin-Williams Leads Professional Waterborne Industrial Alkyd Adoption

The Sherwin-Williams Company maintains a 63% share of the U.S. professional channel, strengthening its leadership in the waterborne industrial coatings market. Its Performance Coatings Group reported a 6.8% net sales increase in early 2026, driven by demand for water-reducible industrial alkyds. The Ultra 9K™ Waterborne System is a benchmark for conversion simplicity, using 62 pigment-rich toners with little to no equipment modification for shops moving away from solvent-based coatings. Sherwin-Williams also offers Collision Core™ Inventory, a real-time analytics platform that reduces waterborne primer and clearcoat inventory costs by 18%. Its BASF Decorative Paints acquisition supports European expansion in industrial wood and metal coatings.

BASF Expands Waterborne Dispersions and C5 Corrosion Protection in APAC

BASF SE is strengthening its waterborne industrial coatings market footprint through a major February 2026 expansion at its Mangalore, India facility, adding production for Acronal® and Basonal® waterborne dispersions. The company’s new India Global Hub supports bio-attributed resin supply chains with up to 50% lower carbon footprint than fossil-based alternatives. BASF leads in water-based packaging finishes, offering moisture- and grease-resistant barrier coatings for sustainable food packaging. Its specialized 2K waterborne polyurethane systems achieve C5-high corrosion protection, helping heavy-machinery OEMs meet 2027 EPA mandates without sacrificing durability.

Nippon Paint Advances PFAS-Free and Functional Waterborne Coatings in Asia-Pacific

Nippon Paint Holdings is Asia-Pacific’s largest player in the waterborne industrial coatings market, capturing strong demand from the region’s 39.77% global waterborne volume share. The company expanded its India workforce to 2,399 employees by March 2026 to support industrial growth. In 2026, Nippon Paint partnered with Humble Bee to develop bee-inspired biomaterials for waterborne resin synthesis, targeting a full phase-out of PFAS-based additives by 2028. Its anti-corrosion Quartz Technology uses microfibers to reinforce waterborne paint films against humidity and UV exposure in tropical climates. The company also leads in Silver Ion and AirGuard functional coatings for healthcare facilities.

China’s “Oil-to-Water” Transition Accelerating Industrial Coatings Adoption

China remains the most influential market in the waterborne industrial coatings landscape, driven by aggressive environmental policies and rapid industrial transformation. The strict enforcement of the GB 30981-2020 standard has made low-VOC waterborne coatings mandatory across industrial applications, effectively accelerating the shift away from solvent-based systems. Additional regulatory measures such as VOC taxation in multiple provinces have further discouraged the use of traditional coatings, making waterborne alternatives economically and environmentally viable.

Infrastructure development continues to act as a major growth engine, with large-scale projects including 5G base stations, ultra-high-voltage grids, and high-speed rail networks requiring advanced waterborne anti-corrosive coatings. Technological innovation is also playing a key role, particularly in the development of waterborne epoxy-acrylic hybrids tailored for the high-volume 3C electronics manufacturing sector. Domestic players are investing heavily in automated waterborne production lines, replacing legacy solvent-based facilities and improving efficiency. The widespread adoption of waterborne primers in heavy-duty rail infrastructure highlights China’s leadership in large-scale industrial coating applications.

United States: Sustainability-Driven Innovation and Industrial Performance Advancements

The United States waterborne industrial coatings market is evolving rapidly, supported by regulatory pressure and innovation in sustainable materials. Stricter VOC limits and the phased introduction of PFAS restrictions are forcing manufacturers to reformulate coatings, accelerating the adoption of water-based technologies across industrial sectors. These regulatory changes are positioning waterborne coatings as the preferred solution for compliance and environmental performance.

Innovation is a key differentiator in the U.S. market, with the commercialization of bio-based waterborne polyurethanes derived from renewable feedstocks such as castor oil and soybean. Federal investments under the Infrastructure Investment and Jobs Act (IIJA) are further driving demand for durable, eco-friendly coatings used in bridge and tunnel rehabilitation. Technological advancements, including UV-curable waterborne coatings, are improving production efficiency by reducing curing times and energy consumption. The automotive sector is also undergoing a major transition, with a significant share of paint booths shifting to waterborne basecoats. Collaborative R&D initiatives are fostering the development of smart coatings, including self-healing films that enhance durability and lifecycle performance.

Germany: High-Tech Polyurethane Dispersions and Sustainable Coating Innovation

Germany stands at the forefront of the European waterborne industrial coatings market, driven by advanced R&D and a strong focus on sustainability. The country is leading innovation in polyurethane dispersions (PUDs), including the development of amine-free waterborne systems that reduce emissions and improve environmental performance. Alignment with the EU Chemicals Strategy for Sustainability is pushing manufacturers to eliminate hazardous substances and develop safer coating solutions.

Product innovation is expanding into high-performance hybrid resins, including polysiloxane-acrylic systems that provide superior weather resistance without relying on PFAS chemicals. Infrastructure and construction sectors are increasingly adopting zero-VOC waterborne coatings to meet green building certification requirements. German engineering firms are also advancing electrostatic spray technologies, improving application efficiency and reducing material waste. Significant investments by major chemical companies are strengthening production capabilities for water-based resin precursors, reinforcing Germany’s position as a leader in sustainable industrial coatings.

India: Manufacturing Expansion and Infrastructure-Led Demand Growth

India is emerging as a key growth market for waterborne industrial coatings, supported by rapid urbanization and government-led manufacturing initiatives. Programs such as “Make in India” 2.0 are incentivizing domestic production of waterborne resins, reducing dependence on imports and strengthening the local supply chain. Large-scale infrastructure projects under the Gati Shakti National Master Plan are driving demand for waterborne protective coatings across transportation and logistics sectors.

The industrial sector is undergoing a significant transition, with increased adoption of waterborne 2K polyurethane systems in agricultural and construction equipment manufacturing to meet global export standards. Leading paint companies are investing in dedicated waterborne production facilities to cater to growing demand in automotive and industrial applications. Regulatory pressure from environmental authorities is also encouraging small and medium enterprises to adopt cleaner water-based technologies. Additionally, the domestic appliance industry is transitioning to waterborne stoving enamels, highlighting the expanding application scope of these coatings in India.

Japan: Nanotechnology Integration and Advanced Industrial Coatings

Japan’s waterborne industrial coatings market is characterized by high precision, technological innovation, and a focus on durability. The integration of nanotechnology into waterborne coatings is enabling the development of advanced materials with self-cleaning and enhanced protective properties for industrial and public infrastructure applications. These innovations are particularly relevant in high-performance sectors such as electronics and advanced manufacturing.

The maritime sector is a key area of growth, with Japan leading the development of waterborne antifouling coatings that comply with stringent international environmental standards. The adoption of AI-driven formulation technologies is improving coating performance, particularly for automotive and industrial applications requiring high precision. Urban sustainability initiatives are driving the use of cool-roof waterborne coatings to mitigate heat island effects. Additionally, Japan’s emphasis on lifecycle assessment and reduced carbon footprints is reinforcing the adoption of environmentally friendly waterborne coatings across industrial sectors.

South Korea: Marine Innovation and Heavy-Duty Waterborne Coating Leadership

South Korea is positioning itself as a global hub for heavy-duty waterborne coatings, particularly in the maritime and offshore energy sectors. Government initiatives such as the “K-Shipbuilding Strategy” are accelerating the development of eco-friendly hull coatings designed to improve fuel efficiency and reduce environmental impact. These advancements are driving the transition from solvent-based to waterborne systems in shipbuilding and marine applications.

Technological expertise in waterborne epoxy primers is enabling performance levels comparable to traditional coatings, even in harsh saline environments. Significant investments in R&D are supporting the development of advanced protective coatings for offshore wind structures, aligning with global renewable energy trends. Regulatory frameworks are tightening VOC limits across large-scale painting facilities, further boosting demand for water-based technologies. Additionally, the construction of automated coating lines tailored for waterborne applications is enhancing production efficiency and supporting large-scale industrial adoption.

Brazil: Automotive Expansion and Bio-Polymer Innovation in Waterborne Coatings

Brazil is emerging as a regional leader in the waterborne industrial coatings market, leveraging its strong automotive sector and access to renewable raw materials. Significant investments by major automotive OEMs are modernizing paint shops, driving the adoption of waterborne technologies in vehicle manufacturing and refinishing processes. This transition is enhancing environmental compliance while improving coating performance.

Innovation in bio-based materials is a key growth driver, with the development of sucrose-derived polyols for waterborne polyurethane dispersions. Regulatory initiatives aimed at reducing solvent emissions are further accelerating the shift toward eco-friendly coatings. Infrastructure development, including large-scale housing projects, is creating additional demand for waterborne coatings in metal components and construction applications. Regional manufacturers are expanding their presence in sectors such as mining and agricultural machinery, while advancements in fast-drying waterborne alkyds are addressing the challenges of high-humidity tropical climates.

Waterborne Industrial Coatings Market Report Scope

Waterborne Industrial Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$47.4 Billion

|

|

Market Size (2032)

|

$69.9 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Resin Type (Acrylic, Polyurethane, Epoxy, Alkyd, Polyester, Fluoropolymer, Others), By Technology (Water-soluble, Waterborne Dispersions, Colloidal Dispersions, Electrodeposition), By End-User Industry (Automotive and Transportation, General Manufacturing, Building and Construction, Energy and Power, Consumer Goods and Appliances, Packaging, Marine), By Curing Mechanism (Air Drying, Baking, Radiation Cured, Multi-component), By Sales Channel (Direct Sales, Specialized Industrial Distributors, Technical Service Providers, Online B2B Platforms), By Sustainability (Low-VOC Formulations, Ultra-Low, PFAS-Free Industrial Coatings, Bio-based)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Axalta Coating Systems Ltd., BASF SE, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun A/S, Hempel A/S, RPM International Inc., Berger Paints India Limited, Asian Paints Limited, Tikkurila Oyj, KCC Corporation, Teknos Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Waterborne Industrial Coatings Market Segmentation

By Resin Type

- Acrylic

- Polyurethane

- Epoxy

- Alkyd

- Polyester

- Fluoropolymer

- Others

By Technology

- Water-soluble

- Waterborne Dispersions

- Colloidal Dispersions

- Electrodeposition

By End-User Industry

- Automotive and Transportation

- General Manufacturing

- Building and Construction

- Energy and Power

- Consumer Goods and Appliances

- Packaging

- Marine

By Curing Mechanism

- Air Drying

- Baking

- Radiation Cured

- Multi-component

By Sales Channel

- Direct Sales

- Specialized Industrial Distributors

- Technical Service Providers

- Online B2B Platforms

By Sustainability

- Low-VOC Formulations

- Ultra-Low

- PFAS-Free Industrial Coatings

- Bio-based

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Waterborne Industrial Coatings Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Axalta Coating Systems Ltd.

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun A/S

- Hempel A/S

- RPM International Inc.

- Berger Paints India Limited

- Asian Paints Limited

- Tikkurila Oyj

- KCC Corporation

- Teknos Group

*- List not Exhaustive