Waterborne Wood Coatings Market Growth Driven by Sustainable Furniture Manufacturing and Bio-Based Innovations

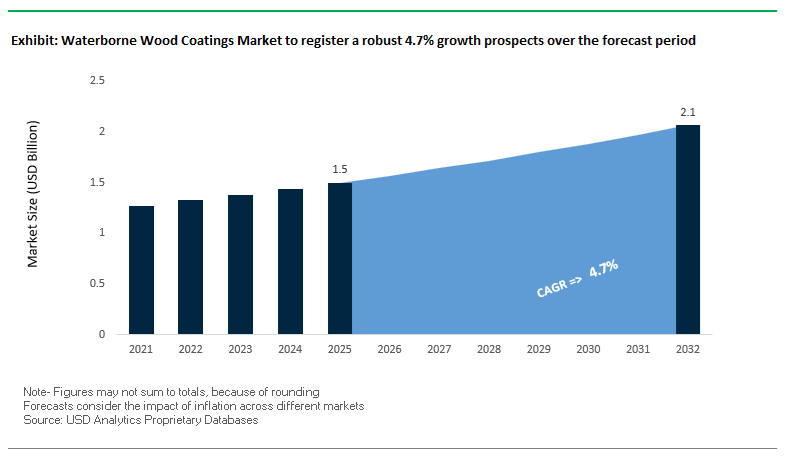

The global Waterborne Wood Coatings Market was valued at $1.5 billion in 2025 and is projected to grow at a CAGR of 4.7% from 2025 to 2032, reaching $2.1 billion by 2032. This steady growth reflects the increasing transition toward low-VOC, environmentally compliant coatings across furniture manufacturing, cabinetry, flooring, and interior architectural wood applications. Waterborne wood coatings are gaining traction due to their low odor, fast drying properties, improved worker safety, and compliance with stringent indoor air quality regulations, particularly in Europe and North America.

A key market driver is the rising demand for sustainable and aesthetically refined wood finishes, particularly in premium residential and commercial interiors. Advances in acrylic-hybrid polymers, polyurethane dispersions, and UV-curable waterborne systems are enabling coatings that deliver enhanced grain clarity, scratch resistance, chemical durability, and long-term color retention, rivaling traditional solvent-based systems. Additionally, the growing adoption of ready-to-assemble (RTA) furniture, modular interiors, and customized cabinetry solutions is increasing demand for coatings that support high-speed production, immediate stacking, and process efficiency.

Sustainability remains central to market evolution. Manufacturers are focusing on bio-based resins, circular raw materials, and renewable feedstocks, aligning with global decarbonization targets and regulatory mandates such as CLP compliance. The emergence of plant-derived coatings using materials like rapeseed oil, pine resin, and natural waxes is redefining product development strategies. Furthermore, the integration of functional properties such as UV protection, anti-yellowing performance, and adaptability to varying humidity conditions is enhancing the applicability of waterborne coatings across diverse climatic environments.

Market Analysis: Bio-Based Coating Breakthroughs, Design-Led Innovation, and Capacity Expansion Reshaping Market Dynamics

The Waterborne Wood Coatings Market is undergoing a transformation driven by bio-based innovation, design-centric product development, and capacity expansion, reflecting evolving consumer preferences and regulatory pressures. A notable development is AkzoNobel’s 2026 launch of the “Rhythm of Blues” industrial wood finishes collection, which introduces specialized waterborne topcoats designed to achieve deep, high-definition color tones—a capability historically limited in waterborne systems. This launch underscores the market’s shift toward premium aesthetics combined with sustainable chemistry.

Product innovation is increasingly aligned with high-end interior and renovation trends. Hempel’s expansion of Farrow & Ball’s Dead Flat® Eggshell finish (April 2026) targets luxury residential markets with a super-tough, ultra-low sheen coating suitable for wood, metal, and concrete surfaces. Similarly, Sherwin-Williams’ 2026 Colormix® forecast introduced advanced waterborne stains and sealants using acrylic-hybrid polymers, enabling faster sanding and enhanced grain definition for furniture manufacturers.

Sustainability-driven product development continues to accelerate. AkzoNobel’s RUBBOL WF 3350 bio-based coating (February 2025)—featuring 20% renewable content verified via ASTM standards—represents a milestone in combining exterior durability with plant-based chemistry. Complementing this, Teknos’ participation in the Nordic Circular Design Programme highlights the increasing adoption of secondary raw materials and circular design principles in wood coatings to meet evolving regulatory requirements.

Operational efficiency and environmental adaptability are also key focus areas. Sherwin-Williams’ SHER-WOOD® EA Hydroplus™ technology enables consistent performance across varying humidity and temperature conditions, addressing one of the primary challenges of waterborne coatings in industrial settings. Meanwhile, PPG’s expansion of waterborne wood coatings capacity—targeting the RTA furniture segment—emphasizes high-speed application, ultra-low VOC emissions, and localized manufacturing strategies in emerging markets.

Innovation is extending into mobility applications as well. Axalta’s development of waterborne UV-curable coatings for automotive interior wood trims combines luxury aesthetics with rapid curing capabilities, aligning with the needs of premium EV manufacturers. Additionally, AkzoNobel’s scaling of bio-based coatings derived from rapeseed and pine resin reflects the growing integration of plant-based materials in automotive interiors, reinforcing the convergence of sustainability and design.

Further supporting this trend, Sikkens’ CETOL® WF 771 expansion introduces high-transparency finishes aligned with biophilic design trends, offering natural aesthetics with enhanced UV protection. Collectively, these developments indicate a market transitioning toward bio-based, design-driven, and performance-optimized wood coating solutions, supported by innovation in materials science, sustainability frameworks, and evolving end-user demands.

Market Trend: CARB 2025–2026 VOC Enforcement Driving Ultra-Low VOC Wood Coatings Innovation

The enforcement of the California Air Resources Board 2025–2026 Suggested Control Measure is significantly reshaping the waterborne wood coatings market, establishing a uniform 50 g/L VOC cap across California and multiple Ozone Transport Commission states. This regulatory shift is accelerating the transition toward ultra-low VOC wood coatings, particularly in architectural wood finishes, furniture coatings, and joinery applications.

To comply with these stringent VOC limits, manufacturers are increasingly adopting bio-based coalescents that provide high boiling points while contributing zero VOC content under EPA Method 24. This innovation enables waterborne wood coatings to maintain extended open time and workability, which is critical for large-surface applications such as flooring and cabinetry.

Despite the reduction in solvent content, 2026-generation formulations are delivering high-performance durability, achieving Class 1 scrub resistance as per ISO 11998 with less than 5 microns of film loss. This demonstrates that environmentally compliant waterborne wood coatings can match or exceed the durability of traditional solvent-based systems, reinforcing their adoption in residential and commercial wood finishing markets.

Market Trend: China GB/T 41662-2025 Standard Driving Hygrothermal Stability and Aesthetic Durability

China’s GB/T 41662-2025 standard is elevating performance benchmarks in the waterborne wood coatings market by focusing on hygrothermal stability and long-term finish durability. Fully enforced across the country by early 2026, this regulation addresses coating failures in high-humidity environments, particularly in Southern Monsoon regions.

The standard mandates a minimum wet-state bond strength of 0.4 MPa after 168 hours of continuous water immersion, effectively eliminating low-performance emulsions from the commercial wood coatings segment. This is driving demand for polymer-modified and high-performance waterborne coatings capable of withstanding prolonged moisture exposure.

In addition to moisture resistance, the regulation introduces strict anti-yellowing requirements, mandating a Delta b value below 1.5 after 500 hours of UV exposure for first-grade coatings. This is encouraging the adoption of high-purity acrylic-urethane hybrid systems, which offer superior color stability and aesthetic performance compared to traditional waterborne alkyd coatings. These advancements are strengthening the demand for UV-resistant wood coatings and premium furniture finishes in the Asia-Pacific market.

Market Opportunity: High-Hardness Waterborne Wood Coatings Expanding into Commercial Interior Applications

The growing demand for durable and sustainable finishes in commercial interiors is creating strong opportunities for high-hardness waterborne wood coatings. These advanced formulations are increasingly penetrating segments such as commercial flooring, office furniture, and retail fixtures, traditionally dominated by solvent-borne polyurethane coatings.

Next-generation two-component waterborne coatings based on self-crosslinking acrylic-polyurethane dispersions are achieving pencil hardness levels of 2H or higher within 48 hours of application. This level of hardness provides enhanced scratch resistance and durability required for high-traffic environments.

In abrasion testing under ASTM D4060 conditions, these coatings demonstrate mass loss below 20 milligrams per 1,000 cycles, ensuring long-term resistance to wear and tear in demanding applications such as hospitality flooring and commercial spaces.

Chemical resistance is another key advantage, with modern waterborne coatings showing no effect after 24-hour exposure to aggressive substances including household cleaners, alcohol, and alkaline solutions. This makes them highly suitable for office furniture, countertops, and institutional environments where surface durability and maintenance resistance are critical performance parameters.

Market Opportunity: UV-Curable Waterborne Wood Coatings Driving High-Speed Furniture Manufacturing Efficiency

The adoption of UV-curable waterborne coatings is creating significant opportunities in the wood coatings market, particularly for high-speed furniture manufacturing and industrial wood finishing lines. These coatings combine the environmental benefits of waterborne systems with the rapid curing capabilities of UV technology, enabling substantial improvements in production efficiency.

Modern waterborne UV coatings are capable of supporting production line speeds exceeding 15 to 20 meters per minute in roller coating and digital finishing applications. This represents a major advancement over conventional air-dry waterborne coatings, allowing manufacturers to significantly increase throughput.

Energy efficiency is also a critical benefit, as UV-curable systems reduce oven energy consumption by 50% to 60% through the use of flash evaporation and UV-LED curing instead of prolonged thermal drying cycles. This contributes to lower operational costs and reduced carbon emissions in furniture manufacturing processes.

The compact curing process enables a reduction of approximately 30% in factory floor space requirements, as shorter drying tunnels and the elimination of cooling zones streamline production layouts. Additionally, these coatings deliver up to three times lower VOC emissions compared to standard waterborne systems while maintaining high-gloss finishes and the visual warmth associated with traditional solvent-based coatings. This combination of performance, efficiency, and sustainability is positioning UV-curable waterborne coatings as a key innovation in the global wood coatings industry.

Waterborne Wood Coatings Market Share and Segmentation Insights

Varnishes and Lacquers Lead with 36.9% Share Due to Clear Finish Performance and Fast Drying

The varnishes and lacquers segment dominates the waterborne wood coatings market with a 36.9% market share in 2025, driven by its superior clear finish performance, non-yellowing properties, and rapid drying characteristics. In the wood coatings and furniture finishing market, waterborne varnishes and lacquers are widely used for furniture, hardwood flooring, cabinets, and interior trim, replacing traditional solvent-borne nitrocellulose and polyurethane coatings. These coatings deliver high durability, scratch resistance, and long-term clarity, maintaining the natural appearance of wood while enhancing protection. A key advantage is their fast drying time of 30–60 minutes and low odor formulation, enabling faster production line throughput and safer indoor application environments. As manufacturers increasingly adopt low-VOC, environmentally compliant coatings, waterborne varnishes and lacquers continue to lead innovation and demand in the global waterborne wood coatings market.

Industrial and Specialty Distributors Lead with 44.8% Share Through B2B Supply and Technical Support

The industrial and specialty distributors segment leads the waterborne wood coatings market with a 44.8% market share in 2025, reflecting strong demand from furniture manufacturers, flooring producers, and cabinet makers. Within the wood finishing and industrial coatings distribution market, these distributors play a critical role in supplying bulk quantities such as pails, drums, and totes, ensuring consistent availability for high-volume production operations. A key growth driver is the concentration of B2B purchasing, where manufacturers rely on distributors for efficient logistics and inventory management. Additionally, industrial distributors provide technical support and application training, including spray equipment setup, coating optimization, and troubleshooting, which are essential for transitioning from solvent-borne to waterborne systems. Their ability to deliver value-added services, expertise, and supply chain efficiency reinforces their leadership in the global waterborne wood coatings market.

Competitive Landscape Analysis of the Waterborne Wood Coatings Market

AkzoNobel Drives Sustainable Waterborne Wood Coatings with Bio-Based Innovation

AkzoNobel N.V. is strengthening its position in the waterborne wood coatings market through its 2026 “Total Wood Protection” campaign, targeting a 15% reduction in carbon footprint for industrial wood producers. Its RUBBOL® WF 3350 coating integrates 20% bio-based content while maintaining high-gloss finishes comparable to solvent-based oils. Following the divestment of its Pakistan business in April 2026, AkzoNobel is reallocating capital toward North American and European wood hubs, focusing on global furniture and flooring renovation market. Its Global Aesthetic Center ensures alignment with “Warm Minimalism” design trends, reinforcing leadership in premium waterborne wood stains and lacquers.

PPG Expands Radiation-Curable Waterborne Wood Coatings for High-Speed Manufacturing

PPG Industries, Inc. is advancing in the waterborne wood coatings market through innovation and strategic expansion. In Q1 2026, the company reported a 7% increase in net sales to USD 3.9 billion, with its Performance Coatings segment achieving a 19.1% EBITDA margin. The acquisition of Ozark Materials strengthens its portfolio of durable water-based stains and infrastructure coatings. PPG is investing in a radiation-curable testing line in France to develop UV waterborne wood coatings capable of instant-dry cycles for high-speed furniture production. With 43% of revenue from sustainably advantaged products, PPG continues to lead in eco-friendly industrial wood coating solutions.

Sherwin-Williams Leads North American Wood Coatings with UV-Curable Innovation

The Sherwin-Williams Company dominates the waterborne wood coatings market in North America, holding a 39.9% market share. In early 2026, the company reported a 6.8% increase in net sales, driven by strong demand in its Performance Coatings Group. Its Lacroma™ and Laqva™ product lines set industry benchmarks for waterborne sealers and topcoats, offering self-leveling properties that reduce sanding requirements by 20%. Sherwin-Williams is investing heavily in UV-curable waterborne coatings, the fastest-growing segment with a 6.2% CAGR, particularly for scratch-resistant cabinetry finishes. Its extensive distribution network ensures reliable supply for small and mid-sized wood manufacturers.

Nippon Paint Expands Eco-Friendly Waterborne Wood Coatings in Asia-Pacific

Nippon Paint Holdings is strengthening its presence in the waterborne wood coatings market, particularly in Asia-Pacific, through capacity expansion and sustainable product development. In 2026, the company announced a 10–15% expansion at its Sriperumbudur facility in India to support rising furniture demand. Its water-based wood coatings have received eco-label certification, emphasizing no-odor and anti-formaldehyde properties for healthcare and educational infrastructure. Nippon Paint’s quick-dry enamel technology ensures coating performance even in high-humidity conditions (up to 85% RH). The company also leads in automotive wood refinish coatings, providing high-clarity lacquers for luxury interior applications.

Axalta Innovates High-Clarity Waterborne Coatings for Premium Wood Finishes

Axalta Coating Systems is advancing in the waterborne wood coatings market with its next-generation Cerulean industrial wood coatings, utilizing acrylic-polyurethane hybrids to deliver superior clarity and depth of image on premium veneers. The company is collaborating with furniture manufacturers to implement closed-loop coating systems, improving material efficiency by up to 18% through overspray recycling. Axalta’s new Wood Coatings Technology Center in North Carolina supports innovation for the USD 120 billion U.S. kitchen cabinet industry. Its expertise in high-solid waterborne formulations enables optimal dry-film thickness with fewer coats, reducing fibre-raising issues and enhancing production efficiency.

China’s Regulatory Push and Industrial Relocation Driving Waterborne Wood Coatings Dominance

China continues to lead the global waterborne wood coatings market, driven by stringent environmental regulations and large-scale industrial restructuring. The implementation of GB 4806.10-2025 is significantly expanding safety requirements for coatings used in indirect food-contact applications such as kitchen cabinetry and dining furniture, accelerating the adoption of low-VOC waterborne systems. Government-backed initiatives, including the expansion of the “Green Factory” program, are offering incentives for manufacturers that eliminate solvent-based coating lines, reinforcing China’s leadership in sustainable wood coatings.

The country is also witnessing major structural shifts in manufacturing, with furniture production relocating to inland eco-industrial parks where waterborne coating infrastructure is mandatory. Technological innovation is advancing rapidly, with the development of waterborne 2K polyurethane systems that replicate the fast curing cycles of traditional solvent-based coatings. Additionally, the integration of UV-cured waterborne coatings in flooring applications is enabling near-zero VOC emissions while improving efficiency. China’s dominance in the ready-to-assemble (RTA) furniture segment further strengthens demand for high-performance waterborne coatings that offer low odor, durability, and export compliance.

Germany: Bio-Based Resin Innovation and Premium Wood Coating Technologies

Germany stands as the innovation hub for waterborne wood coatings in Europe, driven by its strong focus on sustainability and advanced material science. The commercialization of amine-free polyurethane dispersions (PUDs) is significantly improving the aesthetic performance of coatings, particularly by reducing yellowing in light-colored wood species such as oak and beech. Investments in circular economy infrastructure are enabling the production of waterborne binders derived from bio-based feedstocks, aligning with the EU’s sustainability goals.

The market is also witnessing the development of advanced functional coatings, including self-healing topcoats that repair micro-scratches in high-traffic furniture applications. Regulatory alignment with REACH and the EU Chemicals Strategy for Sustainability is driving the elimination of hazardous substances, further promoting the adoption of water-based formulations. Germany’s strict indoor air quality standards, including the Blue Angel certification, are key drivers for premium applications such as engineered wood flooring and acoustic panels. Additionally, digital color-matching systems optimized for waterborne pigments are enhancing production precision and consistency in industrial wood coating operations.

United States: AI-Driven Customization and Adaptive Coating Technologies

The United States waterborne wood coatings market is characterized by rapid technological innovation and digital integration. Advanced coating systems such as environmentally adaptive waterborne formulations are being developed to maintain consistent performance across varying humidity and temperature conditions, addressing one of the key challenges in wood finishing processes. The integration of artificial intelligence into coating formulation is further enhancing product performance, particularly in optimizing resin composition for improved scratch resistance and durability.

Government initiatives, including tax incentives under the Inflation Reduction Act, are encouraging manufacturers to upgrade to low-emission water-based finishing systems. Significant investments by leading companies are targeting high-growth segments such as kitchen cabinetry and residential furniture. Regulatory tightening of hazardous air pollutant emissions is further accelerating the shift toward waterborne technologies. Additionally, the outdoor wood applications market, including decking and siding, is driving demand for specialized waterborne coatings with enhanced UV resistance to withstand environmental exposure.

Vietnam: Export-Driven Growth and Compliance with Global Standards

Vietnam is rapidly emerging as a key manufacturing hub in the waterborne wood coatings market, driven by strong export demand and compliance with international environmental standards. The enforcement of VOC monitoring regulations in spray-booth operations is pushing manufacturers to transition toward water-based coating systems. This shift is particularly evident among small and medium enterprises seeking to maintain export competitiveness in European and North American markets.

Infrastructure development is supporting this transition, with the establishment of large furniture manufacturing clusters equipped with centralized water treatment facilities designed for waterborne coating processes. Government incentives aimed at attracting foreign direct investment in green manufacturing are further strengthening Vietnam’s position as a high-compliance production center. The growing demand for sustainable outdoor furniture is also driving the adoption of waterborne acrylic coatings that meet certifications such as LEED and EDGE. Additionally, the expansion of global coating companies into the Vietnamese market is enhancing technical support and accelerating the adoption of advanced waterborne technologies.

Italy: High-End Design Innovation and Sensory Waterborne Coatings

Italy is a leader in the development of premium waterborne wood coatings, particularly in applications where aesthetics and tactile experience are critical. The market is focused on creating ultra-matte coatings that replicate the natural look and feel of untreated wood while maintaining high chemical resistance. These innovations are particularly relevant for luxury furniture and interior design applications.

Product development is also advancing in functional coatings, including antimicrobial finishes that incorporate silver-ion technology for healthcare and residential applications. Regulatory frameworks such as Green Public Procurement (GPP) are promoting the use of waterborne coatings in public-sector furniture contracts. Investments in automated manufacturing systems, particularly in the Brianza Wood District, are optimizing the application of water-based coatings through advanced robotic spray technologies. Key application areas include bespoke cabinetry and luxury yacht interiors, where low-odor and non-flammable waterborne coatings are essential for safety and performance.

India: Rising Middle-Class Demand and DIY Transformation

India is witnessing strong growth in the waterborne wood coatings market, driven by increasing urbanization and changing consumer preferences. Government initiatives, including tax incentives for home renovation, are expected to boost demand in the DIY and home improvement segments. Leading domestic manufacturers are expanding their service offerings to include waterborne coating solutions, particularly in residential interior applications.

Technological advancements are enabling the development of hybrid waterborne-alkyd coatings that combine the ease of application with the high-gloss finish traditionally associated with solvent-based systems. Regulatory influence from green building organizations is encouraging the adoption of low-VOC coatings in commercial real estate projects. Large-scale residential developments in major cities are further driving demand for waterborne floor coatings, particularly those offering fast drying and quick return-to-service capabilities. This shift highlights India’s transition toward healthier, sustainable wood coating solutions.

Poland: High-Speed Manufacturing and Export-Oriented Innovation

Poland has emerged as a key production hub for waterborne wood coatings within the European market, driven by its strong furniture manufacturing sector and export-oriented growth strategy. Investments in fully automated waterborne UV coating lines are supporting high-volume production while improving efficiency and reducing environmental impact. These advancements are aligned with the growing demand for sustainable furniture in international markets.

Innovation in Poland is focused on the development of bio-based waterborne stains that utilize renewable pigments, catering to environmentally conscious consumers in Scandinavian markets. The expansion of e-commerce furniture distribution is also influencing coating requirements, with increased demand for high block resistance to ensure product durability during packaging and transportation. Technological advancements, including low-energy infrared drying systems optimized for waterborne resins, are further enhancing production efficiency. Key application areas include kitchen furniture and home office solutions, reflecting evolving consumer lifestyles and the continued growth of remote work trends.

Waterborne Wood Coatings Market Report Scope

Waterborne Wood Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2032)

|

$2.1 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Resin Type (Acrylic, Polyurethane, Alkyd, Nitrocellulose, Polyester, Vinyl, Hybrid Systems), By Coating (Stains and Dyes, Varnishes and Lacquers, Shellacs, Wood Preservatives, Water Repellents and Sealers, Primers and Fillers), By Application (Furniture, Flooring and Decking, Joinery and Millwork, Siding and Cladding, Fencing and Garden Sheds, Wooden Artifacts and Decorative Items), By End-User Industry (Residential, Commercial, Industrial), By Technology (Air Drying, Oven, Waterborne UV Curing, Dual Cure Systems), By Sales Channel (Direct Sales, Industrial and Specialty Distributors, Retail, Online B2B)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., The Sherwin-Williams Company, PPG Industries, Inc., Axalta Coating Systems, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Asian Paints Limited, RPM International Inc., BASF SE, Jotun A/S, Hempel A/S, Teknos Group, ICA SpA, Becker Acroma, IVM Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Waterborne Wood Coatings Market Segmentation

By Resin Type

- Acrylic

- Polyurethane

- Alkyd

- Nitrocellulose

- Polyester

- Vinyl

- Hybrid Systems

By Coating

- Stains and Dyes

- Varnishes and Lacquers

- Shellacs

- Wood Preservatives

- Water Repellents and Sealers

- Primers and Fillers

By Application

- Furniture

- Flooring and Decking

- Joinery and Millwork

- Siding and Cladding

- Fencing and Garden Sheds

- Wooden Artifacts and Decorative Items

By End-User Industry

- Residential

- Commercial

- Industrial

By Technology

- Air Drying

- Oven

- Waterborne UV Curing

- Dual Cure Systems

By Sales Channel

- Direct Sales

- Industrial and Specialty Distributors

- Retail

- Online B2B

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Waterborne Wood Coatings Industry

- AkzoNobel N.V.

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Axalta Coating Systems

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- RPM International Inc.

- BASF SE

- Jotun A/S

- Hempel A/S

- Teknos Group

- ICA SpA

- Becker Acroma

- IVM Chemicals

*- List not Exhaustive