Market Overview: Abrasion Reduction, Moisture Control, and VOC Compliance Accelerate Wax Emulsion Market Growth

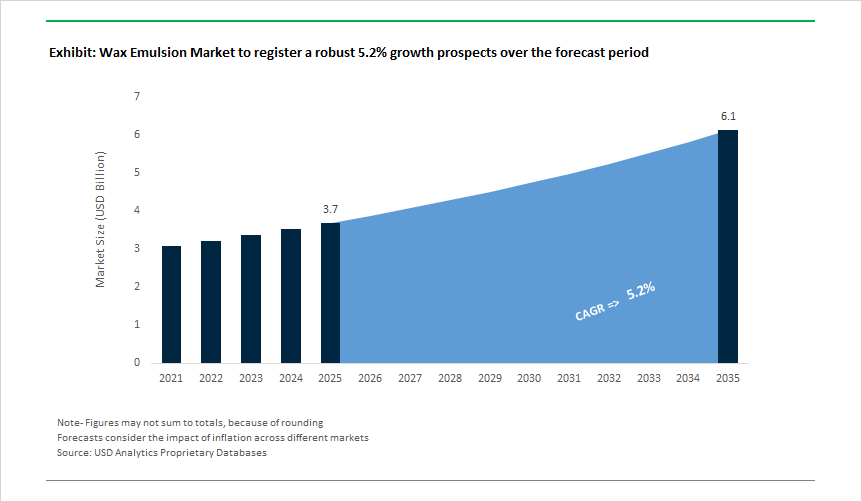

The Global Wax Emulsion Market is valued at USD 3.7 billion in 2025 and is projected to reach USD 6.1 billion by 2035, growing at a 5.2% CAGR as wax emulsions become enabling additives in the global transition toward low-VOC, water-based formulations. Market growth is not driven by end-use volume expansion alone, but by the system-level role wax emulsions play in helping formulators meet regulatory, performance, and cost targets simultaneously.

At a structural level, wax emulsions are benefiting from the irreversible shift away from solvent-based coatings. VOC regulations across construction, packaging, furniture, and industrial coatings are tightening year over year, making water-based systems the default rather than the alternative. Wax emulsions-particularly polyethylene, paraffin, and synthetic variants-have become non-negotiable formulation tools because they restore surface protection, durability, and handling performance that would otherwise be lost in solvent-free systems. For coatings and ink manufacturers, wax emulsions are less a value-add and more a license-to-operate ingredient.

Commercial adoption is further reinforced by clear cost-performance economics. Wax emulsions deliver abrasion resistance, slip control, moisture resistance, and anti-blocking behavior at low treat rates, allowing formulators to upgrade performance without materially increasing formulation cost. This has driven broad uptake across architectural coatings, wood finishes, packaging coatings, printing inks, and textiles, where surface damage, blocking, or moisture ingress directly translate into product failure or customer complaints.

The market is also seeing a shift toward efficiency-oriented product formats. Demand for high-solids wax emulsions is rising as manufacturers seek to lower logistics costs, improve plant throughput, and reduce handling volumes. These formats align well with the needs of large-scale coating and engineered wood producers, where material efficiency and operational simplicity are decisive procurement factors. As a result, suppliers that can deliver stable, high-solids emulsions at scale are increasingly favored in long-term supply agreements.

End-use trends are reinforcing durability and moisture protection as key value drivers. In engineered wood and construction materials, wax emulsions play a critical role in improving dimensional stability and extending product life, supporting the use of wood-based panels in more demanding environments. In printing and packaging, demand is shifting toward emulsions that maintain surface quality and visual appeal while remaining compatible with fast, high-speed, water-based printing processes. These requirements are pushing the market toward more refined emulsion technologies, including smaller particle sizes and tighter consistency control.

Market Analysis: Product Launches, Regulatory Shifts, and Bio-Based Wax Innovations Define the Industry Landscape

Strategic developments in 2025 reshaped the Wax Emulsion Market across packaging, coatings, electronics, construction, and printing ink applications. In October 2025, a major Chinese chemical supplier introduced new oxidized Polyethylene Wax emulsions stabilized with non-ionic systems-significantly improving abrasion resistance and compatibility in high-speed printing inks and flexible packaging coatings. In September 2025, European R&D institutes demonstrated breakthrough Fischer-Tropsch Wax Emulsion technology with bimodal particle distribution, delivering enhanced slip and anti-blocking performance for premium coatings. The regulatory environment tightened further in August 2025, as the US EPA enacted stricter VOC limits on industrial maintenance coatings, accelerating the shift toward water-based formulations that rely heavily on Wax Emulsions for film strength, mar resistance, and surface uniformity.

Production capacity and raw material integration also advanced meaningfully. In July 2025, a leading Brazilian petrochemical player announced major upgrades to its specialty wax refining facilities to supply higher-purity feedstock for Paraffin Wax Emulsion production, particularly for the growing flexible packaging and corrugated board markets. At the same time, sustainability-focused innovation continued to scale, with a specialty chemical producer launching a 90%+ renewable carbon content Bio-Based Wax Emulsion line in June 2025, targeting clean beauty, compostable packaging, and food-contact coatings.

Technology adoption trends expanded across Asia. In April 2025, leading South Korean electronics manufacturers publicly detailed their integration of cationic Wax Emulsions to enhance solder mask dispersion and water repellency in PCB curing processes. Packaging sustainability efforts gained global momentum when two major US and European packaging firms established a partnership in February 2025 to co-develop repulpable, biodegradable Wax Emulsion coatings-a major advancement for circular e-commerce packaging systems. Earlier, in December 2024, India further strengthened its manufacturing footprint by commissioning new Polypropylene Wax Emulsion capacity designed for high-heat automotive and textile applications.

Wax Emulsion Market Trends and Opportunities

Trend 1: Reformulation Momentum Toward PFAS-Free Paper and Food Packaging

The accelerating global phase-out of per- and polyfluoroalkyl substances (PFAS) is fundamentally reshaping the wax emulsion market, particularly in food-contact paper and board applications. By early 2025, more than a dozen U.S. states had enacted enforceable bans on intentionally added PFAS in food packaging, with California’s AB 1200 and New York’s state-level prohibitions acting as reference frameworks for nationwide compliance. In parallel, the EU’s Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, has introduced substance-level thresholds as low as 25 ppb for PFAS in food-contact materials, forcing brand owners and converters to move immediately toward compliant aqueous barrier technologies. Wax emulsions—especially those based on paraffin, polyethylene, and bio-waxes—have emerged as the most scalable alternative due to their inherent hydrophobicity, food safety profile, and compatibility with existing coating lines. Performance gaps that historically favored fluorochemicals are rapidly closing. In 2025, pilot-scale trials at the Western Michigan University Paper Pilot Plant demonstrated that graphene oxide–reinforced wax emulsions reduced water absorption by roughly 40% while improving tensile strength by 27%, enabling grease and oil resistance comparable to legacy PFAS systems. Simultaneously, starch–wax hybrid emulsions scaled by major ingredient suppliers have enabled packaging lightweighting by reducing base paper grammage without compromising wet strength, a critical advantage for brands optimizing logistics emissions. Collectively, regulatory urgency and validated performance gains are pushing wax emulsions from interim substitutes to long-term structural solutions in sustainable paper packaging.

Trend 2: Hybrid Silane–Wax Emulsions Redefining Non-Fluorinated Textile Repellency

In textiles, wax emulsions are undergoing a parallel transformation as apparel and technical fabric producers move away from fluorinated durable water repellents (DWRs) while maintaining performance expectations. Traditional wax-only finishes historically suffered from limited wash durability, often failing after fewer than ten laundering cycles, which constrained their adoption in workwear and outdoor apparel. This limitation is being addressed through hybrid silane–wax emulsion systems that chemically anchor hydrophobic functionality to textile fibers via sol–gel mechanisms. Research collaborations during 2024–2025 demonstrated that alkyltrialkoxysilane-modified wax nanosols can achieve water contact angles exceeding 150°, while retaining repellency after repeated industrial laundering. Beyond durability, these hybrid emulsions deliver meaningful process efficiencies: sol–gel-based application routes reduce overall chemical loading by approximately 20–30%, helping textile finishers comply with tightened 2025 updates to OEKO-TEX® Standard 100 and emerging VOC limits. The functional scope is also expanding. Advanced formulations incorporating zinc oxide or titanium dioxide nanoparticles alongside wax are enabling multi-functional textiles with combined water repellency, UV shielding, and antibacterial activity. This is particularly relevant for medical textiles and high-performance sportswear, where regulatory scrutiny and end-use performance requirements are converging. As a result, silane–wax emulsions are becoming a cornerstone technology for PFAS-free textile finishing rather than a niche compromise.

Opportunity 1: Wax Emulsion Deinking Aids Supporting Circular Paper Systems

Rising recycling mandates are opening a structurally durable opportunity for wax emulsions as functional deinking and process aids in paper recycling. The EU’s push toward a 65% packaging recycling rate has materially increased the complexity of recovered paper streams, with higher ink loads, adhesives, and hydrophobic contaminants accumulating as fibers are reused across multiple cycles. This complexity directly threatens pulp yield, machine runnability, and finished paper quality. Specialized wax emulsion deinking aids are increasingly critical in stabilizing these systems. Pilot trials conducted at large European paper mills in 2025 showed that optimized wax emulsions can improve fiber recovery yields by up to 5% by effectively encapsulating hydrophobic ink particles and promoting their flotation during the deinking stage. This not only preserves fiber strength but also reduces fouling and downtime in the wet end of paper machines. Looking ahead, the EU’s Digital Waste Shipment System, scheduled for implementation in May 2026, will enhance traceability and consistency of recovered fiber streams across borders. This digitalization favors mills that deploy precisely tuned chemical programs, creating a predictable and recurring demand profile for wax-based deinking formulations tailored to specific wastepaper grades.

Opportunity 2: Fugitive Binders and Process Aids in Industrial Additive Manufacturing

The maturation of additive manufacturing from prototyping to serial production is unlocking a high-margin niche for wax emulsions as fugitive binders and rheology modifiers, particularly in binder jetting technologies. In this process, the mechanical integrity of the printed “green part” prior to sintering is entirely dependent on binder performance. Recent production-scale evaluations show that acrylic–wax copolymer emulsions can increase green strength by more than 50% compared with conventional polyvinyl alcohol binders, significantly improving handling robustness during automated depowdering and transfer operations. This advantage is critical as metal and ceramic binder jetting systems scale toward mass production in 2025 and beyond. Wax emulsions also offer a decisive benefit during thermal debinding and sintering: they volatilize cleanly without leaving carbonaceous residues, enabling final part densities exceeding 95% of theoretical limits with predictable shrinkage behavior. In aerospace and industrial casting applications, wax-emulsion-based binders are enabling the 3D printing of complex ceramic tooling and investment casting molds with intricate internal channels. Optimized viscosity control—often approaching 10,000 mPa·s—allows these binders to balance print resolution with stress relief during sintering, reducing crack formation under thermal gradients. As additive manufacturing penetrates regulated, high-reliability sectors, wax emulsions are evolving into critical enablers of repeatable, industrial-scale production rather than ancillary consumables.

Market Share Analysis: Wax Emulsion Market

Market Share by Type: Synthetic Wax Emulsions Set the Performance Baseline

Synthetic wax emulsions account for approximately 68% of the Wax Emulsion Market because they deliver engineered, repeatable performance that high-throughput industrial processes require and natural waxes cannot consistently achieve. In 2025, procurement decisions are anchored on thermal headroom and line efficiency: formulations from Clariant and BASF maintain integrity up to 330°C, enabling powder coating and plastics compounding without yellowing or breakdown—a non-negotiable threshold for modern processing windows. Surface durability further consolidates share; BYK reports ~40% gains in scratch resistance in clearcoats versus legacy natural oils, translating directly into fewer reworks and longer service life. Regulation has become a growth catalyst rather than a constraint: the 2025 PTFE-free transition has elevated modified PE alloy emulsions that reach COF ≈0.06, effectively matching fluoropolymer performance while clearing compliance hurdles—an SEO-critical driver under “green chemistry” and “regulatory compliance.” Finally, operational ROI seals the case at scale; benchmarks from Michelman and SK Nexilis show 56 km continuous coating runs without roll build-up, cutting downtime 15–20%. Together, thermal stability, surface protection, compliance-ready chemistry, and line productivity explain why synthetics remain the market’s structural majority.

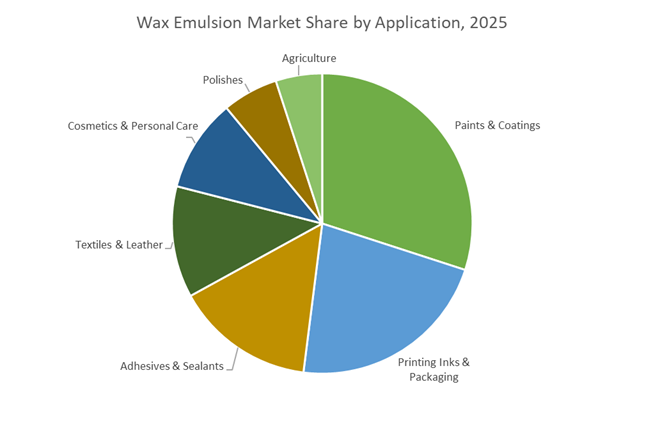

Market Share by Application: Paints & Coatings Absorb Innovation at Scale

Paints and coatings hold about 30% of total demand, the largest application segment, because wax emulsions are now embedded in the performance architecture of waterborne, EV-adjacent, and infrastructure coatings. The shift to water-based systems is decisive: BASF documents ~15% YoY increases in scuff resistance using its Joncryl® waxes without gloss loss, a balance that specifiers prioritize for architectural finishes. Electrification adds a high-value layer—specialty emulsions are increasingly specified in EV battery enclosure coatings to improve moisture barriers by ~30%, protecting high-voltage systems and extending pack life, as highlighted by Lubrizol. Volume momentum is anchored by public works: 2025 infrastructure outlays across China and the EU favor wax-enhanced cool-roof and road-marking coatings that must deliver 5-year durability under heat and UV stress, pushing wax-modified surface tension control into mainstream specs. ESG execution closes the loop; producers including Clariant and BASF report ~84% process-water recovery, a metric procurement teams use to justify premium formulations in regulated projects. These converging drivers—waterborne adoption, EV protection, infrastructure scale, and circular manufacturing—keep paints and coatings at the center of wax emulsion demand.

Competitive Landscape: Advanced Emulsification, Fischer-Tropsch Integration, and VOC-Compliant Innovations Shape Global Competition

The Wax Emulsion Market is characterized by deep technical specialization, vertically integrated feedstock strategies, and the rapid expansion of high-solids, bio-based, and high-performance emulsion systems. Leading suppliers differentiate through global production networks, proprietary emulsification technologies, synthetic wax processing capabilities, and strong partnerships with coatings, packaging, construction, and printing ink manufacturers. Competition increasingly centers on VOC compliance readiness, sustainability certifications, dispersion stability, and the development of nano-scale emulsions for advanced surface finishes.

Michelman, Inc. - Water-Based Emulsification Expertise Drives Innovation in High-Performance Coatings Additives

Michelman maintains a strong leadership position through advanced emulsification platforms supporting high-solids (up to 45%) wax dispersions for architectural, industrial, and wood coatings. Its Polyethylene Wax Emulsions deliver superior scratch resistance, abrasion reduction, and anti-blocking performance, making them essential for premium surface coatings. The company has launched new natural wax emulsions engineered for recyclable packaging and food-contact applications, aligning with global sustainability mandates. Michelman’s global technical service infrastructure enables real-time support for formulators across 50+ countries.

BASF SE - Integrated Wax Intermediate Production Strengthens VOC-Compliant Emulsion Supply

BASF leverages its extensive chemical value chain to produce high-quality Polyethylene Wax intermediates, ensuring consistent feedstock security for its Wax Emulsion portfolio. Its emulsions are widely used across construction materials and fiberglass insulation, offering strong water repellency and stability in gypsum board and building products. BASF continues investing in Asian manufacturing sites to localize supply for high-volume Water-Based Coatings. Recent R&D improvements in surfactant systems have enhanced freeze-thaw stability, enabling reliable performance in colder climates.

Sasol Limited - Fischer-Tropsch Wax Integration Underpins Specialty Synthetic Emulsion Leadership

Sasol’s competitive edge lies in its vertically integrated coal-to-liquids and gas-to-liquids pathways, providing ultra-high-purity synthetic wax feedstocks for emulsion production. Its Fischer-Tropsch Wax Emulsions are valued for narrow molecular weight distribution and consistent hardness-ideal for premium polishes, industrial coatings, and metal protection. Sasol is expanding output of oxidized FT waxes with higher acid values to improve emulsifiability for anionic systems. Growing distribution capacity in Europe and North America reinforces its global market reach.

The Lubrizol Corporation - High-Performance Wax Emulsions Optimized For Lubrication and Industrial Fluids

Lubrizol specializes in performance additives, offering Wax Emulsions engineered to improve lubricity, reduce friction, and enhance wear resistance in water-based metalworking fluids and industrial lubricants. Recent advancements include rheology-tailored emulsions capable of reducing the coefficient of friction by up to 20%, boosting equipment longevity and energy efficiency. Its multifunctional emulsions act as both surface modifiers and dispersants, reducing formulation complexity for coatings manufacturers. Lubrizol leverages its established additives portfolio to cross-integrate wax solutions across multiple industrial sectors.

Nippon Seiro Co., Ltd. - Precision Paraffin and Synthetic Waxes Power Moisture-Resistant Packaging Coatings

Nippon Seiro offers high-purity Paraffin Wax with oil content below 0.5%, enabling highly stable and clean emulsions for sensitive packaging and paper sizing applications. Its Wax Emulsions significantly improve Cobb Value performance in moisture-resistant boards. The company has expanded its specialty synthetic wax lineup, including EVA copolymers for flexible, high-adhesion emulsion systems. With strong regional supply chains and technical support across Southeast Asia, Nippon Seiro is a preferred supplier to cost-sensitive yet performance-driven packaging manufacturers.

China continues to anchor the global wax emulsion market through a combination of infrastructure-led demand and regulatory-driven formulation upgrades. Under the 14th Five-Year Plan, cumulative infrastructure investment of approximately $4.2 trillion (2021–2025) has materially expanded consumption of wax emulsions in concrete curing agents, waterproofing systems, and protective wood coatings, where water-based systems are now favored to meet VOC and durability standards. This large-scale public works pipeline has structurally shifted demand toward high-solids, fast-drying wax emulsions capable of performing in extreme construction environments.

On the regulatory front, updates by the National Medical Products Administration (NMPA) to the IECIC in October 2025 have accelerated adoption of polyethylene (PE) wax emulsions in cosmetics, particularly in domestic skincare brands targeting premium positioning. Parallel initiatives led by the National Institute for Food and Drug Control (NIFDC) emphasize domestic substitution and green development, encouraging Chinese producers to replace imported paraffin emulsions with locally synthesized, high-purity and PFAS-free alternatives—reshaping China from a volume exporter to a technology-upgrading producer.

United States – Bio-Based Innovation and FDA-Compliant Packaging

The United States wax emulsion market in 2025 is defined by bio-based innovation, food-contact compliance, and e-commerce packaging growth. A major inflection point has been the widespread adoption of FDA-compliant wax emulsions (21 CFR 175.105) for paper and board coatings used in food packaging. These water-based systems provide grease resistance and moisture barriers without relying on plasticizers or fluorinated additives, making them central to sustainable packaging strategies for online grocery and quick-service restaurants.

Industrial applications are also expanding. Hexion, now part of the Westlake group, has continued to scale its Bord’N-Seal® and Cascowax® wax emulsion lines for OSB and engineered wood panels, where uniform dispersion and lower applied costs outperform molten slack wax. Meanwhile, tighter Environmental Protection Agency (EPA) low-VOC mandates have driven a double-digit increase in water-based wax emulsions for automotive and aerospace coatings, reinforcing the U.S. position as a performance-driven, regulation-led market.

Germany – Precision Additives and Circular Chemistry

Germany’s wax emulsion market is strategically aligned with the EU’s circular economy and PFAS-free materials agenda, emphasizing high-performance specialty additives rather than commodity volumes. In 2025, MÜNZING CHEMIE completed the IRMa (Integrative Resource Efficiency Management) project, integrating digital resource tracking and heat recovery into wax additive manufacturing—lowering energy intensity while ensuring traceability demanded by European customers.

Product innovation is accelerating in fiber-based and biodegradable barrier coatings. At the VILF Conference 2025, German suppliers showcased WÜKOSEAL® and OMBRESEAL® emulsions designed for plastic-free packaging applications. In parallel, H&R Group redirected R&D toward “label-free” paraffin emulsions that comply with evolving European Chemicals Agency (ECHA) guidelines. These moves position Germany as the reference market for regulatory-compliant, high-engineering wax emulsions.

India – Paints, Coatings, and Post-Harvest Protection Growth

India has emerged as one of the fastest-growing demand centers for wax emulsions, driven by its rapid expansion in paints, coatings, packaging, and agriculture. By 2024–2025, India overtook Japan as Asia’s second-largest paints and coatings market, structurally increasing demand for wax emulsions that deliver scratch resistance, matting control, and surface durability in architectural and industrial coatings.

Beyond construction, agricultural applications are gaining prominence. Government-backed initiatives by the Ministry of Agriculture are promoting edible wax emulsions—notably carnauba- and beeswax-based systems—to extend fruit shelf life and reduce post-harvest losses. International suppliers have responded accordingly; MÜNZING CHEMIE highlighted India-specific fiber-based packaging solutions at PaperEx India 2025, underscoring India’s evolution into a high-volume, multi-sector consumption hub for wax emulsions.

Spain – Petrochemical Strength and Food-Contact Formulations

Spain plays a critical role as a Mediterranean refining and formulation hub for paraffin-based wax emulsions, leveraging advanced petrochemical infrastructure and proximity to EU end markets. In 2024–2025, Repsol expanded its Redemul wax emulsion portfolio, targeting automotive clear-coat and industrial finishes where enhanced gloss and abrasion resistance are essential.

Food-contact compliance is another strategic pillar. Repsol’s 2025 emulsions portfolio includes FDA- and EU-compliant paraffin systems for food wrapping, paper cups, and corrugated transport packaging. Discussions at Paint & Coatings Barcelona 2025 further highlighted Spain’s focus on energy-efficient, cationic wax emulsions for construction materials—reinforcing the country’s position as a formulation bridge between petrochemicals and sustainable applications.

Brazil – Carnauba Wax and Natural Emulsion Leadership

Brazil holds a structurally unique position in the wax emulsion market as the world’s primary source of carnauba wax, enabling leadership in natural and bio-based wax emulsions. In 2024–2025, DEUREX AG launched micronized carnauba wax emulsions sourced from Brazil, designed for high-luster automotive polishes and food-grade applications, reinforcing Brazil’s dominance in premium natural wax segments.

Policy support further enhances this role. Brazil’s RenovaBio program has indirectly stimulated demand for soy-based wax emulsions as renewable alternatives to petroleum-derived paraffins, particularly in textiles and leather finishing. Together, carnauba and soy derivatives position Brazil as the global anchor for natural wax emulsions, aligned with sustainability-driven demand in North America and Europe.

2025 Strategic Matrix: Wax Emulsion National Benchmarking

Wax Emulsion National Benchmarking

|

Country

|

Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

China

|

Infrastructure & regulation

|

$4.2T Five-Year Plan / IECIC updates

|

Concrete curing, cosmetics

|

|

United States

|

Bio-based & compliance

|

FDA-approved food barrier adoption

|

Packaging, wood coatings

|

|

Germany

|

Circular chemistry

|

IRMa efficiency project completion

|

PFAS-free specialty additives

|

|

India

|

Manufacturing expansion

|

Asia’s 2nd-largest paints market

|

Coatings, fruit protection

|

|

Spain

|

Petrochemical integration

|

Redemul automotive range launch

|

Food wrapping, auto clear-coats

|

|

Brazil

|

Natural feedstocks

|

Global carnauba emulsion expansion

|

Polishes, leather & food

|

Wax Emulsion Market Report Scope

Wax Emulsion Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.7 Billion

|

|

Market Size (2035)

|

$6.1 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Type (Synthetic Wax Emulsions, Natural Wax Emulsions), By Emulsion Charge (Ionic—Anionic & Cationic, Non-Ionic), By Application (Paints & Coatings, Printing Inks & Packaging, Textiles & Leather, Adhesives & Sealants, Cosmetics & Personal Care, Agriculture, Polishes), By End-Use Industry (Building & Construction, Automotive & Transportation, Packaging & Paper, Textile & Apparel, Consumer Goods & Healthcare)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Altana AG, Dow Inc., Hexion Inc., Wacker Chemie AG, Clariant AG, Honeywell International Inc., Lubrizol Corporation, Nippon Seiro Co. Ltd., Sasol Limited, Nanjing Tianshi New Material Technologies, Michelman Inc., Keim-Additec Surface GmbH, Euroceras (DEUREX Group), Kao Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wax Emulsion Market Segmentation

By Type

- Synthetic Wax Emulsions

- Natural Wax Emulsions

By Emulsion Charge

- Ionic: Anionic, Cationic

- Non-Ionic

By Application

- Paints & Coatings

- Printing Inks & Packaging

- Textiles & Leather

- Adhesives & Sealants

- Cosmetics & Personal Care

- Agriculture

- Polishes

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Wax Emulsion Market

- BASF SE

- Altana AG

- Dow Inc.

- Hexion Inc.

- Wacker Chemie AG

- Clariant AG

- Honeywell International Inc.

- Lubrizol Corporation

- Nippon Seiro Co., Ltd.

- Sasol Limited

- Nanjing Tianshi New Material Technologies

- Michelman, Inc.

- Keim-Additec Surface GmbH

- Euroceras (DEUREX Group)

- Kao Corporation

*- List not Exhaustive