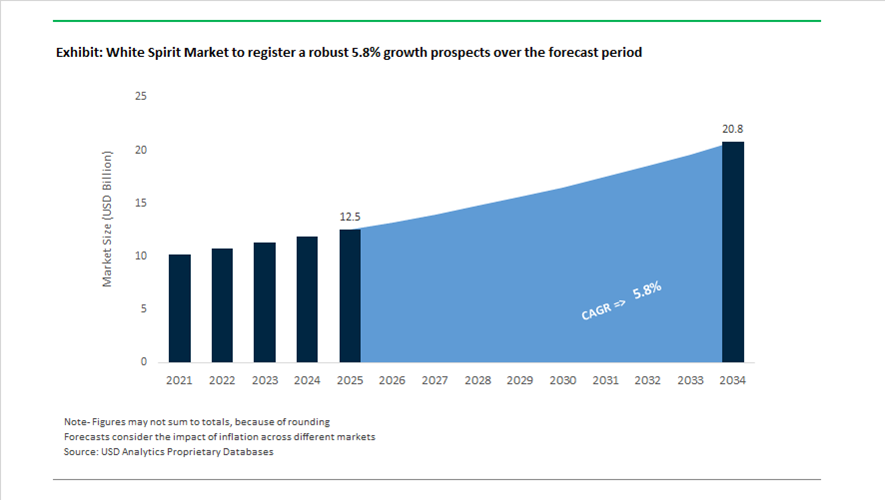

White Spirit Market Overview 2025–2034: $12.5 Billion to $20.8 Billion at 5.8% CAGR Driven by Low-VOC Reformulation, Coatings Demand, and Refinery Upgrades

The White Spirit market is valued at $12.5 billion in 2025 and is projected to reach $20.8 billion by 2034, expanding at a CAGR of 5.8%. White spirit, also referred to as mineral spirits or petroleum solvent, remains a critical hydrocarbon solvent for industrial paints, protective coatings, metal degreasing, agrochemical formulations, adhesives, printing inks, and DIY maintenance products. Demand growth is closely linked to construction activity, marine and subsea coatings, infrastructure maintenance, and expanding manufacturing output in Asia-Pacific. At the same time, regulatory tightening around volatile organic compounds (VOC) emissions is accelerating the shift toward low-aromatic, low-VOC, high-flash-point white spirit grades, particularly in India and Europe.

Capacity expansion and reformulation efforts intensified beginning in 2024. In February 2024, Bharat Petroleum (BPCL) and Indian Oil rolled out low-VOC white spirit formulations designed to meet India’s evolving environmental compliance standards while preserving solvency performance in decorative and industrial coatings. Between 2024 and 2025, Safex Chemicals commissioned a new manufacturing facility in Bharuch, Gujarat, targeting specialized solvent blends and mineral spirits for paints and agrochemicals, reinforcing Asia-Pacific supply resilience. In May 2025, the Shell, Reliance, and ONGC Panna-Mukta and Tapti offshore decommissioning project utilized substantial volumes of industrial-grade white spirits for degreasing and surface preparation, underscoring solvent demand in large-scale energy infrastructure dismantling.

Strategic consolidation reshaped competitive dynamics in 2025. In March 2025, Sudarshan Chemical completed the acquisition of the Heubach Group, integrating pigment dispersions dependent on high-purity mineral spirits into a broader coatings additive network. In July 2025, Shell Lubricants finalized the acquisition of Raj Petro Specialities, incorporating a significant specialty solvent and white oil portfolio into Shell’s South Asian distribution system. In September 2025, TotalEnergies confirmed growth in refining and chemical output through 2026, focusing on high-margin downstream assets that ensure stable white spirit supply for the European coatings sector. In December 2025, ExxonMobil raised its 2030 Product Solutions earnings target to $9 billion, highlighting refinery upgrades to prioritize higher-margin specialty solvents over bulk fuel streams.

Product innovation and sustainability initiatives accelerated into 2026. In 2025, ExxonMobil scaled its Proxxima thermoset resin facility in Texas, indirectly stimulating demand for high-flash-point mineral spirit thinners used in marine and subsea coating systems. In September 2025, Shell India introduced initiatives focused on bio-fermented solvent alternatives aimed at gradually displacing petroleum-derived white spirits in consumer and clean beauty applications. In February 2026, Neste opened a Nordic specialty lubricant and solvent hub in Sweden to distribute sustainably refined and bio-attributed solvent products across Northern Europe. That same month, BPCL received the Global Safety Award 2026 (Platinum Category), reflecting improvements in hazardous solvent production and handling.

White Spirit Market Trends and Opportunities: Low-Aromatic Transition, Feedstock Volatility, and High-Purity Growth Segments

Regulatory Push Toward Dearomatized White Spirits and Low-VOC Solvent Formulations

The White Spirit market is undergoing a decisive transformation driven by stringent VOC regulations and occupational health standards, accelerating the transition from traditional high-aromatic solvents to dearomatized and hydrogenated white spirit grades. Regulatory frameworks such as the EU Decopaint Directive and North American indoor air quality standards are compelling formulators to adopt low-toxicity, low-odor solvents that align with evolving Environmental, Health, and Safety (EHS) requirements.

Dearomatized white spirits, typically containing less than 20 ppm aromatics compared to 20%–25% in conventional grades, are becoming the preferred choice in architectural coatings, printing inks, and industrial cleaning applications. This shift is primarily driven by the need to reduce worker exposure risks, including central nervous system effects and long-term solvent toxicity. As a result, these high-purity solvents are commanding premium pricing in indoor coatings and professional-use formulations.

Technological advancements in refining are further supporting this transition. Narrow-boiling-range solvents such as Exxsol™ D and Spirdane® D offer up to 30% faster drying times, enabling improved formulation control and coating performance. By early 2026, over 40% of new solvent-based product launches in Europe and North America were classified as low-VOC or eco-friendly, reinforcing the market’s structural shift toward Type 3 hydrogenated white spirits and sustainable solvent systems.

Refinery-to-Chemicals Integration and Feedstock Volatility Impacting White Spirit Supply Dynamics

The White Spirit market is increasingly influenced by feedstock cost volatility and refinery integration strategies, where production is closely tied to the refinery-to-chemicals (RTC) balance. As refiners optimize output between fuels and higher-margin petrochemical intermediates, white spirit availability and pricing are becoming more sensitive to global energy market fluctuations.

In late 2025, unplanned refinery outages in key regions drove product margins to historic highs, highlighting the vulnerability of solvent supply chains to operational disruptions. Middle distillates, which serve as primary feedstocks for white spirit production, experienced tight supply conditions despite ample crude availability, reinforcing the importance of refinery uptime and operational efficiency.

Structural shifts in demand are also reshaping supply allocation. Petrochemical feedstocks are projected to account for over 60% of refinery demand growth in 2026, up from 40% in 2025, particularly in integrated refining hubs across Asia and the U.S. Gulf Coast. This has intensified competition between fuel blending and specialty solvent production, prompting manufacturers to adopt dynamic production strategies and flexible output configurations.

Additionally, evolving trade policies and tariffs introduced in 2025 have led to logistical re-routing and regional sourcing strategies. Procurement teams are increasingly prioritizing “local-for-local” supply chains to mitigate cost volatility and ensure consistent access to refinery intermediates, making supply chain resilience a key competitive factor in the white spirit market.

Bio-Based and Renewable White Spirits (HVO Derivatives) Unlocking Sustainable Solvent Demand

The transition toward bio-based and renewable white spirits is emerging as a major growth opportunity, driven by global decarbonization goals and increasing demand for low-carbon, sustainable solvents. Hydrotreated Vegetable Oil (HVO) technology is enabling the production of renewable alkanes that serve as drop-in replacements for mineral-based white spirits, without compromising performance characteristics.

Capacity expansion is accelerating this shift. By March 2026, Neste confirmed that its Rotterdam refinery expansion will reach 2.7 million tons of renewable product capacity by 2027, supporting the growing adoption of renewable hydrocarbon solvents in coatings, cleaning, and personal care applications. These developments are positioning HVO-based white spirits as a scalable alternative within the green solvent market.

From an environmental perspective, bio-based solvents such as TotalEnergies’ Biolife range offer significant advantages, including up to 86% reduction in greenhouse gas emissions and compliance with OECD 306 biodegradability standards. These products are also odorless, colorless, and low-toxicity, making them highly suitable for indoor and sensitive-use applications.

Market adoption is particularly strong in regions such as the Nordics and Benelux, where sustainable procurement policies and ESG-driven purchasing behavior are driving premium demand for bio-sourced white spirits. This trend is expanding beyond niche applications into mainstream industrial cleaning and MRO (maintenance, repair, and operations) formulations, indicating strong long-term growth potential.

Ultra-High-Purity White Spirits for Electronics Cleaning and Advanced Manufacturing Applications

A high-value growth segment in the White Spirit market is the development of ultra-high-purity hydrocarbon solvents for electronics cleaning and advanced manufacturing processes. As semiconductor devices become increasingly miniaturized and complex, demand is rising for residue-free, low-contaminant solvents capable of meeting stringent performance standards.

The global electronics cleaning solvent market, valued at $1.3 billion in 2024, is expanding rapidly alongside advancements in PCB assembly, semiconductor fabrication, and precision electronics manufacturing. Ultra-pure white spirits and isoparaffinic solvents are widely used for flux residue removal and surface preparation, offering high cleaning efficiency without damaging sensitive components.

Next-generation semiconductor nodes, including 3nm and 2nm technologies, require solvents with extremely low metal and particulate contamination levels. Products such as Isopar™ L are gaining traction due to their low surface tension and high purity, enabling effective cleaning of complex geometries and micro-scale structures.

To meet these stringent requirements, manufacturers are integrating AI-driven quality control systems into production processes. These technologies enable real-time impurity detection and process optimization, ensuring consistent solvent purity and performance. As a result, ultra-high-purity white spirits are becoming essential in aerospace, medical electronics, and high-performance computing applications, positioning this segment as a high-margin, technology-driven growth frontier within the white spirit market.

White Spirit Market Share and Segmentation Insights

Product Type Market Share: Type 2 White Spirit Leads with Optimal Solvency and Industrial Utility

Type 2 white spirit accounts for 42.80% of the market in 2025, driven by its balanced aromatic content and effective solvency for paints, coatings, cleaning, and degreasing applications. Its ability to dissolve oils, resins, and greases makes it a preferred solvent in industrial and maintenance operations. Type 3, Type 1, and Type 0 variants serve applications requiring different evaporation rates and aromatic content levels. A key market trend is the optimization of aromatic content, where formulations are adjusted to meet health and safety regulations while maintaining performance, with dearomatized white spirits gaining traction in regulated environments.

End-Use Industry Market Share: Construction and Infrastructure Leads with Paint Thinning and Maintenance Demand

Construction and infrastructure hold a 38.60% share in the white spirit market in 2025, supported by its extensive use in paint thinning, surface preparation, and equipment cleaning in building and renovation activities. Automotive, consumer goods, printing, and textile industries contribute additional demand across cleaning and solvent applications. A key growth dynamic is the continued need for maintenance of existing infrastructure, where solvent-based coatings and repainting activities sustain white spirit consumption, even as waterborne coatings gain adoption in new construction projects across global markets.

White Spirit Market Competitive Landscape

The White Spirit market in 2026 is defined by high-purity differentiation, with a shift toward hydrogenated Type 3 and ultra-low aromatic solvents for coatings and industrial cleaning, alongside bio-attributed blending and AI-driven supply chain optimization to mitigate energy price volatility.

ExxonMobil Strengthens High-Purity Solvent Leadership with Varsol™ and Exxsol™ Portfolio Optimization

ExxonMobil maintains leadership in high-purity white spirits through its integrated refinery-to-chemical model and globally consistent solvent portfolio. In March 2026, the company implemented price increases up to $0.06/lb across Varsol™ and Exxsol™ lines, reflecting rising feedstock and operational costs. Varsol™ continues to serve high-aromatic applications, while Exxsol™ D series targets low-odor, de-aromatized coatings and indoor formulations. With $36 billion in 2025 earnings, ExxonMobil sustains high utilization of world-scale solvent plants. Its focus on precision cleaning applications in aerospace and automotive sectors leverages narrow boiling ranges for residue-free performance. This positions the company strongly in premium industrial solvent segments.

Shell Advances Circular White Spirit Production with Low-Aromatic ShellSol™ Portfolio Realignment

Shell is transitioning toward circular and low-carbon white spirit production through integration of recycled feedstocks and electrified operations. Its 2025 collaboration with Freepoint Eco-Systems enables pyrolysis oil supply for circular solvent manufacturing at Monaca. By 2026, Shell is reducing Scope 1 and 2 emissions via industrial electrification initiatives with Siemens. The ShellSol™ portfolio is being optimized toward low-aromatic and de-aromatized grades, addressing demand for low-odor paint thinners in DIY and architectural coatings. Its global terminal network supports just-in-time delivery across Asia-Pacific and India. This logistics advantage enhances supply chain resilience amid fluctuating solvent demand.

TotalEnergies Expands De-Aromatized Spirdane® Portfolio with Bio-Paraffinic Blending Strategy

TotalEnergies is investing in future-proof white spirits aligned with EU environmental regulations and low-carbon solvent demand. With $15.6 billion adjusted net income in 2025, the company has allocated $16 billion in 2026 Capex, including upgrades to Spirdane® production for enhanced de-aromatization. Bio-paraffinic blending initiatives at the La Mède biorefinery are enabling development of hybrid white spirits with reduced carbon footprint. Its Marketing & Services segment continues to deliver strong margins, offsetting crude price volatility. Spirdane® L1 remains widely used in textile and dry-cleaning applications due to controlled evaporation rates and compliance with occupational safety standards. This strategic positioning supports growth in regulated industrial solvent markets.

Reliance Industries Scales Integrated White Spirit Production with Jamnagar Refinery Dominance

Reliance Industries is leveraging its fully integrated oil-to-chemicals value chain to dominate the Asia-Pacific white spirit market. High utilization at the Jamnagar refinery supports strong operating cash flow contribution, expected to reach 40% in FY2026. The company’s ability to source 100% internal feedstock insulates its white spirit production from global supply disruptions. Strategic price adjustments in petrochemicals indicate strong domestic pricing power extending to solvent products. Investments of ₹75,000 crore in downstream chemicals are enhancing solvent production efficiency and export capabilities. Reliance’s scale and vertical integration enable competitive pricing and high-margin exports to Africa and the Middle East.

Neste Leads Renewable White Spirit Innovation with Bio-Based Drop-In Solvent Solutions

Neste is redefining the white spirit market through renewable hydrocarbon solvents derived from waste-based feedstocks. Its Neste MY Renewable Hydrocarbons are positioned as 100% bio-based, drop-in replacements for fossil-derived white spirits in premium coatings. In 2025, the company reported €1,683 million EBITDA, enabling accelerated expansion of its Rotterdam refinery for renewable solvent production. Performance improvement initiatives delivered a €376 million EBITDA uplift, funding further R&D in circular solvent technologies. These solutions are increasingly adopted by eco-conscious paint manufacturers seeking Scope 3 emission reductions. Neste’s focus on renewable and circular chemistry secures its leadership in sustainable solvent innovation.

China White Spirit Market Defined by Feedstock Surplus and Low-Aromatic Export Strategy

China’s white spirit market in 2025–2026 is structurally shaped by a pronounced upstream feedstock surplus and a clear policy-backed push toward higher-value solvent grades. According to ICAR and ICIS energy outlooks, China’s refining capacity for C2 and C3 derivatives is projected to exceed domestic demand by 121%, creating abundant availability of naphtha-range streams suitable for Regular-flash and Low-flash white spirit production. This surplus has materially lowered marginal production costs, enabling Chinese refiners to aggressively position white spirits in export markets, particularly for paint thinners and industrial cleaning applications. Infrastructure-led growth has reinforced domestic pull-through. National transport and urban development targets for 2026 have driven a reported 15% year-on-year increase in procurement of white spirits for bridge and tunnel protective coatings, where consistent solvency and evaporation rates are critical for large-area applications.

Strategically, China is moving up the quality curve. In late 2025, Sinopec announced hydro-cracking upgrades in Zhejiang to produce low-aromatic white spirits with aromatic content below 0.5%, explicitly targeting European architectural and industrial coatings markets. This aligns with the tightening of domestic automotive VOC standards in 2025, which has accelerated adoption of Type 3 odorless white spirits in Guangzhou and Shanghai refinish clusters. At the same time, BASF’s Zhanjiang Verbund site, approaching full operational status in early 2026, has integrated dedicated logistics for high-purity solvents used in water-reducible and high-solid coatings. On the trade front, the Ministry of Commerce initiated solvent import reviews in 2025, indirectly favoring domestic suppliers such as Shanghai Chemex Group to stabilize availability for the fast-growing construction sector.

India White Spirit Market Anchored in Refinery Modernization and MSME Consumption

India’s white spirit market is being reshaped by refinery-level investments combined with demand formalization among small and mid-sized downstream users. In mid-2025, Bharat Petroleum Corporation Limited announced a ₹2,500 crore modernization program at its Mumbai refinery, specifically targeting higher yields of high-flash grade white spirits. This investment reflects rising demand from industrial cleaning and maintenance applications, where higher flash points improve safety compliance in enclosed manufacturing environments. Parallel policy initiatives are reinforcing consumption. The Ministry of Cooperation’s National Cooperation Policy 2025 is enabling digital integration of MSME paint manufacturers, which remain the primary consumers of paint thinner grade white spirits across semi-urban and rural markets.

From a strategic standpoint, India is positioning white spirits within its broader self-sufficiency agenda. The Department of Chemicals and Petrochemicals has prioritized aliphatic hydrocarbon solvents under its 2026 roadmap to reduce reliance on Middle Eastern imports. Operational efficiency is also improving. In 2025, Indian Oil Corporation deployed AI-driven demand forecasting at its Panipat refinery to optimize low-flash grade production during peak construction seasons. Policy discussions around GST rationalization for industrial solvents are expected to lower input costs for furniture and textile manufacturers, while APEDA’s processed food excellence strategy for 2025–2026 has indirectly increased demand for ultra-refined white spirits used in food-grade machinery cleaning.

United States White Spirit Market Driven by Specialty Solvents and Regulatory Transition

The U.S. white spirit market in 2025 is characterized by a decisive pivot away from legacy solvent grades toward high-purity, low-VOC alternatives. Feedstock availability remains a competitive advantage. ExxonMobil tripled Permian Basin output to over 600,000 oil-equivalent barrels by 2025, ensuring a stable supply of light crude streams for Gulf Coast solvent manufacturing. This upstream strength underpins ExxonMobil’s broader Product Solutions strategy, which was revised upward in December 2025 to target $9 billion in incremental earnings by 2030, with white spirits positioned as a core high-value industrial solvent.

Regulatory pressure is accelerating product substitution. Stricter air quality enforcement scheduled for 2026 in California and the Northeast has forced a market-wide shift from traditional Stoddard Solvent toward hydro-treated Type 1 white spirits with lower VOC profiles. Innovation in feedstock circularity is also emerging. In May 2025, Shell entered a collaboration with Freepoint Eco-Systems to explore pyrolysis oil as a future bio-circular feedstock for next-generation green white spirits. Beyond coatings and cleaning, niche demand is rising from the semiconductor sector. CHIPS Act-driven fab expansions in Arizona and Texas have created specialized requirements for electronic-grade white spirits used in precision degreasing of sensitive tool components.

Germany White Spirit Market Focused on Renewable Substitutes and REACH Alignment

Germany’s white spirit market is transitioning from volume-based consumption to innovation-led substitution, driven by sustainability regulation and premium end-use requirements. In late 2025, Haltermann Carless, part of the HCS Group, launched renewable-based white spirit substitutes derived from waste oils. These products are targeted at eco-conscious architectural coatings customers seeking to reduce Scope 3 emissions without compromising solvency performance. This innovation aligns with broader EU decarbonization objectives and positions Germany as a testbed for next-generation solvent systems.

Compliance remains a central driver. German manufacturers completed the transition to aromatic-free Type 3 white spirits for indoor household cleaning products ahead of the EU REACH 2026 audits, effectively resetting the baseline specification for the domestic market. Industrial collaboration continues to support technical development. The renewal of the Shell–BMW M Motorsport partnership in March 2025 signals ongoing R&D into high-performance lubricants and specialty cleaners, where white spirit remains a critical cleaning and formulation base. Additionally, Shell’s 2025 introduction of Direct Liquid Cooling fluids for data centers reflects a broader diversification of specialty fluid portfolios that leverage the same high-purity refining infrastructure used for premium white spirits.

White Spirit Market Country Snapshot

White Spirit Market County Level Snapshot

|

Country

|

Primary Growth Lever

|

Key White Spirit Grades

|

Strategic Direction

|

|

China

|

Feedstock surplus and export orientation

|

Low-aromatic, Type 3

|

Scale-driven with quality upgrade

|

|

India

|

Refinery modernization and MSME demand

|

High-flash, paint thinner

|

Self-sufficiency and domestic reach

|

|

United States

|

Regulatory shift and specialty solvents

|

Hydro-treated Type 1

|

Premiumization and circular feedstocks

|

|

Germany

|

Sustainability regulation and innovation

|

Aromatic-free, renewable substitutes

|

Compliance-led, innovation-focused

|

White Spirit Market Report Scope

White Spirit Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.5 Billion

|

|

Market Size (2034)

|

$20.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Product Type (Type 0, Type 1, Type 2, Type 3), By Grade (Low-Flash Grade, Regular-Flash Grade, High-Flash Grade), By Application (Paint Thinner, Cleaning Agent, Degreasing Agent, Fuel Additive, Disinfectant and Pesticide Solvent), By End-Use Industry (Construction and Infrastructure, Automotive and Aerospace, Textile and Leather, Printing and Packaging, Consumer Goods and Household Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell plc, Exxon Mobil Corporation, TotalEnergies SE, BP p.l.c., Sinopec Corporation, Bharat Petroleum Corporation Limited, Indian Oil Corporation Limited, HCS Group GmbH, Neste Oyj, Compañía Española de Petróleos, Reliance Industries Limited, DHC Solvent Chemie GmbH, Kuwait Petroleum Corporation, Petróleo Brasileiro S.A., Shanghai Chemex Group Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

White Spirit Market Segmentation

By Product Type

- Type 0

- Type 1

- Type 2

- Type 3

By Grade

- Low-Flash Grade

- Regular-Flash Grade

- High-Flash Grade

By Application

- Paint Thinner

- Cleaning Agent

- Degreasing Agent

- Fuel Additive

- Disinfectant and Pesticide Solvent

By End-Use Industry

- Construction and Infrastructure

- Automotive and Aerospace

- Textile and Leather

- Printing and Packaging

- Consumer Goods and Household Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the White Spirit Market

- Shell plc

- Exxon Mobil Corporation

- TotalEnergies SE

- BP p.l.c.

- Sinopec Corporation

- Bharat Petroleum Corporation Limited

- Indian Oil Corporation Limited

- HCS Group GmbH

- Neste Oyj

- Compañía Española de Petróleos

- Reliance Industries Limited

- DHC Solvent Chemie GmbH

- Kuwait Petroleum Corporation

- Petróleo Brasileiro S.A.

- Shanghai Chemex Group Ltd.

*- List not Exhaustive