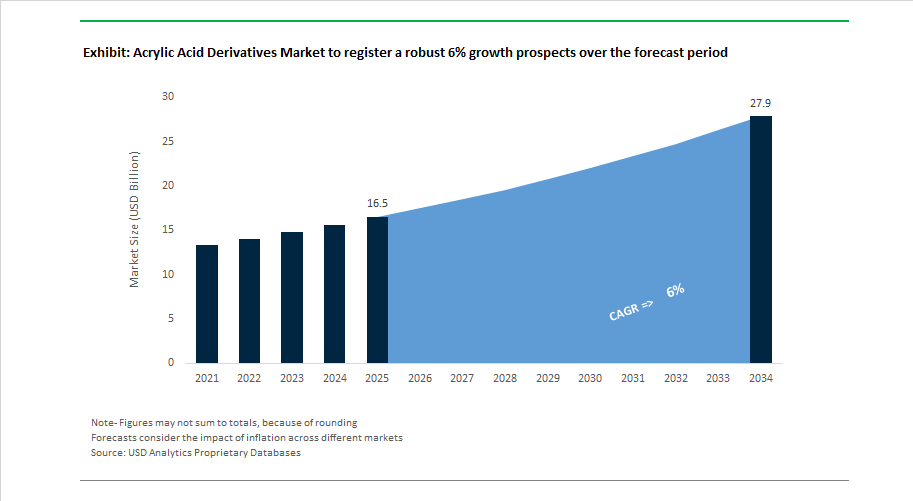

Market Overview: Acrylic Acid Derivatives Market Size Expansion to $27.9 Billion by 2034 Driven by Capacity Additions and Bio-Based Chemistry Shift

The global acrylic acid derivatives market is entering a structurally transformative cycle, with market value projected to grow from $16.5 billion in 2025 to $27.9 billion by 2034, reflecting a 6% CAGR. Expansion is being shaped by synchronized capacity additions in Asia, technology-driven process shifts, and portfolio migration toward specialty, high-margin acrylic monomers and downstream polymers. Demand fundamentals remain anchored in superabsorbent polymers (SAP), coatings binders, adhesives, sealants, textiles, and hygiene applications, while supply dynamics are being rebalanced through new mega-scale complexes and selective capacity rationalization in higher-cost regions. The industry is also witnessing a redefinition of competitiveness, where carbon intensity, feedstock flexibility, and process efficiency now influence investment decisions as strongly as traditional propylene economics.

In January 2025, BASF achieved mechanical completion of its glacial acrylic acid (GAA) and butyl acrylate (BA) units at the Zhanjiang Verbund site, marking one of the largest recent expansions serving Asia-Pacific hygiene and coatings demand. Meanwhile, the value chain is progressively decarbonizing. In late 2025, LG Chem launched a bio-acrylic acid pilot line based on 3-hydroxypropionic acid (3-HP), representing a foundational step toward renewable acrylic monomer production. Sustainability momentum intensified in mid-2025 when Arkema secured ISCC PLUS certification across all acrylic monomer sites, enabling mass-balance certified bio-attributed derivatives. Further reinforcing green chemistry adoption, Keyuan Holdings advanced its Guangdong green industrial park in November 2025, deploying direct propane oxidation technology that shortens process routes and lowers emissions intensity.

Technology evolution is increasingly defining competitive positioning. In March 2025, Roehm inaugurated its Texas LiMA plant using C2-based MMA technology, offering superior efficiency versus the traditional ACH route. At the same time, Arkema introduced bio-based acrylic thickeners in October 2025, targeting low-VOC architectural coatings and carbon-reduction mandates. Market structure is also being reshaped by strategic retrenchment and regional rebalancing. Mitsubishi Chemical Corporation canceled its Louisiana MMA project in March 2025, while Trinseo exited European MMA production in July 2025, reflecting energy cost pressure and Asian import competition. Conversely, Indian Oil Corporation advanced domestic self-sufficiency with its Gujarat BA line going live in August 2025. Strategic repositioning continued into January 2026 as Nippon Shokubai shifted focus toward integrated SAP value chains, signaling migration away from commoditized merchant acrylic acid. Simultaneously, China’s technology-premium strategy in early 2026 is accelerating demand for medical-grade and electronic-grade acrylic monomers, elevating margin structures and signaling a quality-driven phase in the acrylic acid derivatives market.

Strategic Trends and Emerging Opportunities Reshaping the Acrylic Acid Derivatives Market

Market Trend: Shift Away from Butyl Acrylate Due to Feedstock Scarcity and Cost Instability

A critical transformation within the acrylic acid derivatives industry is the strategic shift away from butyl acrylate as manufacturers experience constrained feedstock supply, rising propylene costs, and vulnerability to import-driven pricing. Supply-chain disruptions in feedstocks, particularly n-butanol, have exposed downstream formulators—especially paints, adhesives, and coatings manufacturers—to unpredictable raw material expenses. This has led Tier-1 chemical producers to realign sourcing strategies, diversify monomer inputs, and accelerate vertical integration.

In markets such as India, where domestic output for butyl acrylate is insufficient, premium-priced imports continue to erode margin resilience for coatings and textile manufacturers. Producers are responding with investment-led mitigation strategies, best seen in IndianOil’s upcoming acrylic monomers project bringing 150 KTA capacity online, designed with advanced processing technology for cost stabilization. This trend signals that monomer market security, backward integration, and domestic availability will increasingly determine supplier preference and contract longevity within the acrylic acid derivatives industry going forward.

Market Trend: Onshoring and Local-for-Local Supply Chain Reconfiguration for Glacial Acrylic Acid (GAA)

As global hygiene markets scale rapidly—superabsorbent polymers (SAP) being the backbone of diaper and hygiene absorbents—the demand for high-purity glacial acrylic acid (≥99%) has triggered a geographic reconfiguration of supply chains. Asia Pacific—particularly China—has emerged as the focal point for onshoring initiatives as manufacturers emphasize local feedstock production to reduce import dependence, logistics risk, and carbon impact.

BASF’s nearing-completion Verbund-site acrylic acid complex in China and Nippon Shokubai’s recently-commissioned Indonesian plant exemplify the structural transition toward region-level self-sufficiency. These investments are aimed not only at output expansion but also at digital and energy-optimized production optimization—supported by membrane-based separation that can reduce energy use by 30%. Sustainability-aligned production, low-carbon acrylics, and proximity-based supply will increasingly be survival-level requirements—not differentiation—across GAA producers from 2025 onward.

Market Opportunity: PMMA Chemical Recycling Unlocks Circular MMA Feedstock and New Revenue Pools

The greatest structural long-term opportunity lies in chemical recycling of poly(methyl methacrylate) (PMMA), which converts plastic waste into recycled methyl methacrylate (r-MMA). This creates a new, circular, cost-efficient feedstock stream that reduces reliance on virgin petrochemicals while opening new ESG-led procurement channels. With Europe advancing regulatory pressure to eliminate landfilled PMMA by 2030, recycling infrastructure expansion is accelerating.

Commercial projects such as the NEXTCHEM–Röhm collaboration in Germany—designed to process approximately 5,000 tonnes of PMMA waste annually—demonstrate that the circular MMA business model will soon become profitable at scale. Meanwhile, horizontal automotive-grade recycling pilots between Mitsubishi Chemical Group and Honda reveal clear industrial demand for ultrapure, recycled monomers with preserved optical performance, which could reshape automotive glazing, lenses, interior panels, and premium polymer applications. This opportunity positions chemical recyclers and polymer producers for premium-priced ESG-certified supply contracts across automotive, signage, and consumer electronics segments.

Market Opportunity: Acrylic-Based Binders Becoming Critical to Next-Generation EV and Silicon-Anode Batteries

Specialty acrylic binders—once a niche category—are now becoming strategically essential to the electric vehicle battery market, particularly silicon-anode chemistries. These polymers provide mechanical flexibility, allowing silicon electrodes to withstand up to 300% volumetric expansion without structural breakdown. Arkema’s commercial release of Incellion-grade binders demonstrates clear proof that acrylic derivatives are evolving into performance-critical materials rather than generic commodity components.

This presents a long-duration revenue expansion opportunity—given that lightweighting and extended battery life directly correlate with vehicle efficiency. With a 10% reduction in EV weight translating to a 6–8% increase in energy efficiency, automotive OEMs are actively evaluating next-generation polymer supply chains. Simultaneously, growth in Li-ion battery recycling infrastructure—such as BatX Energies’ new facility in India—suggests acrylic binders will eventually integrate into circular recovery systems, expanding their lifecycle value and relevance across EV manufacturing.

Acrylic Acid Derivatives Market Share and Segmentation Insights

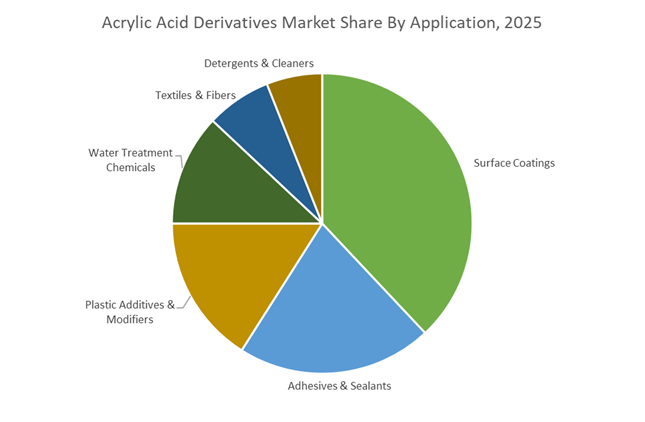

Market Share by Application: Surface Coatings Dominate While Adhesives & Sealants Deliver Fastest Growth

Surface coatings account for approximately 38% of global acrylic acid derivatives market revenue in 2025, driven by robust demand for super absorbent polymers (SAP) in hygiene products and acrylate polymers in architectural paints. The post-pandemic recovery in commercial construction has significantly lifted consumption across Asia-Pacific, North America, and Western Europe. Adhesives & sealants represent the fastest-growing application segment, expanding at +6.2% YoY, supported by automotive lightweighting trends that require plastic-to-metal bonding and the rapid expansion of e-commerce, which is increasing demand for high-performance packaging tapes. Plastic additives & modifiers and water treatment chemicals maintain steady market positions through polymer compounding and municipal infrastructure upgrades. Textiles & fibers benefit from specialty acrylic finishes in technical fabrics. Detergents & cleaners hold the smallest share, reflecting formulation maturity, yet volumes remain stable due to the essential nature of household cleaning products.

Market Share by End-Use Industry: Packaging Leads as Semiconductors Exhibit Highest Growth Velocity

Packaging & consumer goods command nearly 29% of acrylic acid derivatives market demand in 2025, surpassing construction & infrastructure due to surging flexible packaging volumes and increased use of acrylic-based inks and laminates for food safety compliance. Automotive & transportation follow, fueled by structural adhesives and composite bonding solutions that support vehicle lightweighting and electric mobility. Healthcare & personal care remain recession-resilient, anchored by SAP consumption in diapers and adult incontinence products, with aging populations in Japan, Western Europe, and North America sustaining long-term demand. Agriculture holds a limited share because acrylic-based superabsorbent polymers remain costlier than traditional hydrogels, restricting usage to high-value horticulture. Electronics & semiconductors, although currently the smallest segment, show the strongest growth trajectory, as acrylic derivatives are critical in photoresists for semiconductor lithography, with global fab expansions projected to double segment share by 2028.

Competitive Landscape: Strategic Positioning of Global Leaders in Acrylic Acid Derivatives

The global Acrylic Acid Derivatives Market is shaped by vertically integrated chemical majors and specialty materials innovators competing across glacial acrylic acid, acrylic esters, superabsorbent polymers, and high-performance coatings. Market leaders are accelerating capacity expansions, sustainability-driven product development, and downstream integration to secure share in hygiene products, architectural coatings, EV batteries, and advanced packaging. Competitive differentiation increasingly centers on bio-based acrylic routes, low-VOC water-borne technologies, and specialty additives, while regional investments in North America, China, and Southeast Asia reflect strong demand from construction, automotive, and electronics. Below is a structured analysis of the key players driving innovation, supply chain resilience, and value-added acrylic derivative applications.

BASF SE strengthens the acrylic v alue chain through fully integrated Verbund production

As the world’s largest chemical producer, BASF SE operates a fully integrated Verbund model that optimizes feedstock efficiency across glacial acrylic acid and acrylic ester production. The company leads globally in GAA, supported by a tightly integrated supply chain that reduces raw material volatility. Its portfolio spans butyl, ethyl, and methyl acrylates, superabsorbent polymers for hygiene, and high-performance dispersions for water-based architectural coatings. BASF is actively commercializing a bio-based acrylic acid route in partnership with Cargill and Novozymes, targeting sustainable diaper applications. In 2025, BASF prioritized capacity expansion in North America and China’s Zhanjiang site to meet rising demand for low-VOC coatings.

Arkema S.A. expands coating solutions with downstream integration and specialty acrylics

Arkema S.A. is a dominant force in specialty materials, with its Coating Solutions segment anchoring growth in acrylic monomers and resins. During 2024–2025, Arkema integrated Dow’s laminating adhesives business, strengthening its downstream presence in packaging and electronics. Operationally, the company commissioned a new 1233zd unit in the U.S. and completed construction of the Rilsan® Clear unit in Singapore, scheduled for Q1 2026. Arkema supplies high-value acrylic systems for 3D printing, UV curing, and sustainable construction, while its “one-stop-shop” model spans monomers, specialty additives, and resins, positioning the company as a full-spectrum coatings technology provider.

Nippon Shokubai Co., Ltd. leads the global SAP market with advanced polymer R&D

Nippon Shokubai Co., Ltd. is a global powerhouse in superabsorbent polymers, supplying roughly one-fourth of disposable diapers worldwide. Its acrylic derivative portfolio primarily supports hygiene applications while extending into specialty chemicals for EV batteries. The company recently established a global supply system for ISCC PLUS-certified SAPs using biomass-derived raw materials via mass balance. Under its MTMP 2027 strategy, Nippon Shokubai is shifting toward a Solutions Business model, doubling investments in specialty chemicals and electronics. Competitive advantage stems from deep polymerization expertise and a unique four-region manufacturing network across Japan, the USA, Europe, and Indonesia.

LG Chem Ltd. accelerates bio-acrylic innovation and LETZero expansion

LG Chem Ltd. is rapidly transforming into a sustainability-driven materials leader, leveraging its strong Asian footprint. In Q2 2025, the company began commercial production of 100% plant-based bio-acrylic acid derived from 3HP via microbial fermentation. Through its LETZero platform, LG Chem is scaling bio-circular balanced acrylates for cosmetics and automotive coatings. Core offerings include SAP for hygiene, neopentyl glycol for powder coatings, and high-performance adhesives for EV battery assembly. With a Net-Zero 2050 target, 2025 serves as a bridge year for expanding eco-friendly acrylic derivatives across North America and Europe.

Evonik Industries AG targets high-margin specialty acrylic additives and next-generation solutions

Evonik Industries AG focuses on premium specialty additives rather than bulk acrylic commodities. Its portfolio includes specialty methacrylates, crosslinkers, and the TEGO® and VESTAGON® series for high-performance coatings. At the 2025 European Coatings Show, Evonik introduced biodegradable biosurfactants and mass-balanced wetting agents, reinforcing its sustainability roadmap. Key applications span pharmaceutical blister packaging binders and adhesion promoters for thermal interface materials in EV batteries. Strategically, Evonik is divesting non-core Performance Intermediates to concentrate fully on Specialty Additives and Next Generation Solutions with strong environmental credentials.

Dow Inc. advances downstream acrylic applications with circularity-led innovation

Dow Inc. is a major force in downstream acrylic applications, particularly architectural and industrial coatings. The company brings deep expertise in acrylic emulsion technology for low-VOC, water-borne formulations. Its product suite includes acrylic monomers, pressure-sensitive adhesive binders, and floor care polymers. Dow is actively advancing circularity by launching renewable-based acrylic solutions and recycling technologies for acrylic plastics. Supported by strong vertical integration from ethylene and propylene feedstocks through finished formulations, Dow remains well positioned to serve consumer, construction, and industrial markets with scalable, sustainable acrylic derivative systems.

China Acrylic Acid Derivatives Market: Capacity Expansion Meets Regulatory Tightening and Price Compression

China remains the largest global production and consumption hub for acrylic acid derivatives, driven by aggressive capacity additions and deepening vertical integration. The mechanical completion of BASF’s Zhanjiang Verbund site in July 2025 marks a major milestone, with a world-scale GAA unit and a 400,000-metric-ton butyl acrylate complex scheduled for full startup in 2026. Parallelly, Wanhua Chemical Group’s 400,000-ton-per-year Penglai facility came online in early 2025, pushing China’s domestic butyl acrylate capacity beyond 3.7 million tons and reinforcing its position as a global supply anchor.

However, capacity-led growth is now intersecting with regulatory pressure. Under the 14th Five-Year Plan, stricter VOC emission standards enforced by MIIT are accelerating the transition from solvent-based systems toward water-borne acrylic emulsions in coatings, adhesives, and construction chemicals. This structural shift is reshaping downstream demand patterns while increasing compliance costs for legacy plants. Strategic players such as Satellite Chemical are mitigating margin pressure through feedstock security, leveraging ethane-to-ethylene integration at Lianyungang to ensure cost-competitive acrylic acid and SAP production. Despite these strengths, market oversupply has weighed heavily on pricing; by mid-2025, domestic butyl acrylate prices declined 5.99% year-on-year, falling to multi-year lows near RMB 7,500 per ton. This price environment is forcing consolidation and accelerating R&D investments into high-performance acrylic elastomers aligned with China’s rapidly expanding New Energy Vehicle (NEV) ecosystem.

France Acrylic Acid Derivatives Market: Decarbonized Acrylics and High-Purity Specialization

France plays a disproportionate role in Europe’s acrylic acid derivatives landscape by combining scale, process innovation, and regulatory leadership. Arkema’s €130 million investment at its Carling site underscores this position, introducing a patented acrylic acid purification technology scheduled for completion in 2026. The upgrade is expected to improve energy efficiency by 25% while reducing carbon intensity by 20%, directly aligning acrylic monomer production with Europe’s tightening sustainability benchmarks.

Beyond operational efficiency, France is emerging as a center for decarbonized acrylic monomers. Arkema’s integration of bio-renewable raw materials at Carling enables a differentiated portfolio for the European coatings and packaging markets, where demand for low-carbon and recyclable adhesive systems is accelerating under the Loi AGEC framework. The Carling complex also functions as Arkema’s global Acrylic Research and Process Center, with a strong focus on ultra-high-purity GAA for medical-grade superabsorbents. With annual shipments exceeding 350,000 metric tons, the French site remains the second-largest acrylic monomer production hub globally, balancing volume manufacturing with high-margin specialty innovation.

United States Acrylic Acid Derivatives Market: Sustainability Incentives and Application-Led Innovation

The United States acrylic acid derivatives market is increasingly shaped by sustainability policy and downstream application growth rather than sheer capacity expansion. Dow Chemical’s commitment to sourcing 750 MW of renewable power by 2025 is materially lowering the carbon footprint of its US-based acrylic acid operations, reinforcing ESG-driven procurement trends among coatings, hygiene, and packaging customers. At the same time, Dow’s product innovation pipeline—highlighted by acrylic-based SURLYN™ REN Ionomers and EVOAIR™ polyolefin elastomers—reflects rising demand for bio-circular and high-performance materials in luxury and flexible packaging.

Supply chain resilience has also become a strategic priority. BASF expanded North American acrylic acid capacity during 2024–2025 to reduce logistics risk and support the fast-growing market for water-based architectural coatings. On the demand side, healthcare remains a key growth engine, with strong consumption of specialty acrylic amides for adult incontinence products using advanced SAP formulations. Policy support under the Inflation Reduction Act is further incentivizing investment into bio-based acrylic acid routes, while automotive lightweighting trends are driving R&D into high-adhesion acrylic resins for bonding carbon-fiber-reinforced plastics in electric vehicle platforms.

Japan Acrylic Acid Derivatives Market: Proprietary Chemistry and Bio-Based Transition Leadership

Japan’s acrylic acid derivatives sector is defined by proprietary process technology and a long-term transition toward bio-based chemistries. Nippon Shokubai continues to advance its catalytic oxidation platforms, building on its legacy as the first company to commercialize direct propylene oxidation for acrylic acid production. The company is now scaling biomass-derived acrylic acid technologies, targeting commercial deployment before 2030 to serve the global demand for sustainable diapers and hygiene products.

Japan also sits at the intersection of acrylic chemistry and advanced electronics. The development of SEAHOSTAR™ silica nanoparticles with acrylic-based hard coatings is enabling next-generation 5G displays and semiconductor materials. Simultaneously, specialty monomers such as VEEA™ and AOMA™ reactive diluents are gaining traction in UV inkjet and 3D printing applications across Europe and North America. Strategic collaboration between Nippon Shokubai and Mitsubishi Heavy Industries on ammonia cracking catalysts indirectly supports feedstock decarbonization, while METI-certified circular economy projects using low-carbon ammonia derived from waste plastics reinforce Japan’s systemic approach to sustainable chemical synthesis.

Germany Acrylic Acid Derivatives Market: Integrated Verbund Efficiency and Regulatory-Driven Innovation

Germany represents the technological and regulatory benchmark for acrylic acid derivatives in Europe. BASF’s Ludwigshafen Verbund complex remains the global reference model for integrated acrylic value chains, maximizing resource efficiency through interconnected production streams. This integration is increasingly critical as German producers adapt to the EU Green Deal and Carbon Border Adjustment Mechanism (CBAM), transitioning acrylic ester production toward green hydrogen-based feedstocks.

Specialty innovation is equally prominent. Evonik Industries has launched bio-based acrylic resins tailored for European wood coatings, while investments in microencapsulation technologies are expanding the use of acrylic-based latent heat storage materials in thermal energy systems. The automotive sector remains a high-value demand driver, with German OEMs prioritizing high-durability acrylic elastomers for battery cooling and high-temperature sealing applications. Regulatory leadership under the REACH2.0 framework is further pushing German firms toward “safe-by-design” acrylic monomers, embedding compliance directly into molecular design.

South Korea Acrylic Acid Derivatives Market: Export-Oriented Scale and Smart Materials Focus

South Korea has positioned itself as a critical export hub for acrylic acid derivatives, particularly in superabsorbent polymers and electronics-grade materials. LG Chem leverages its large-scale domestic capacity to supply high-purity glacial acrylic acid across Southeast Asia, supporting hygiene and coatings markets. Korea is also a major SAP exporter to the broader APAC region, benefiting from demographic-driven demand growth in Northeast Asia.

Innovation is increasingly centered on energy storage and smart electronics. Acrylic-based binders developed for lithium-ion battery electrodes are improving cycle life and mechanical stability in EV batteries, while pressure-sensitive adhesives are being engineered for flexible and foldable OLED displays used by domestic electronics leaders. Internally, LG Chem is optimizing acrylic polymerization efficiency through AI-driven digital transformation across its 29 global sites. Strategically, the company is targeting the emerging “blue ocean” of bio-acrylics, exploring partnerships for bio-based 3-hydroxypropionic acid (3-HP) production as a future acrylic acid precursor.

Country-Level Strategic Positioning in Acrylic Acid Derivatives

Acrylic Acid Derivatives Market County Level Snapshot

|

Country

|

Strategic Focus Areas

|

Key Industry Impact

|

|

China

|

Capacity expansion, VOC regulation, NEV-driven R&D

|

Global pricing pressure, scale-driven competitiveness

|

|

France

|

Decarbonized monomers, high-purity GAA, packaging innovation

|

Premium specialty positioning in Europe

|

|

United States

|

Sustainability incentives, healthcare & EV applications

|

Application-led demand growth, supply resilience

|

|

Japan

|

Proprietary oxidation, bio-based acrylics, electronics

|

High-value specialty and future bio-transition

|

|

Germany

|

Verbund integration, green hydrogen, REACH2.0 compliance

|

Regulatory-driven innovation and efficiency

|

|

South Korea

|

Export-oriented SAP, battery binders, smart adhesives

|

APAC supply leadership and smart materials growth

|

Acrylic Acid Derivatives Market Report Scope

Acrylic Acid Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.5 Billion

|

|

Market Size (2034)

|

$27.9 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Derivative Type (Acrylic Esters, Acrylic Polymers, Acrylic Amides, Glacial Acrylic Acid (GAA)), By Application (Surface Coatings, Adhesives and Sealants, Plastic Additives and Modifiers, Water Treatment Chemicals, Textiles and Fibers, Detergents and Cleaners), By End-Use Industry (Healthcare and Personal Care, Construction and Infrastructure, Automotive and Transportation, Packaging and Consumer Goods, Electronics and Semiconductors, Agriculture), By Physical Form (Liquid, Powder/Granule, Emulsion/Solution)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Arkema S.A., Dow Inc., Nippon Shokubai Co., Ltd., LG Chem Ltd., Mitsubishi Chemical Group, Sibur Holding, Wanhua Chemical Group Co., Ltd., Satellite Chemical Co., Ltd., Evonik Industries AG, Formosa Plastics Corporation, Sasol Limited, Shanghai Huayi Acrylic Acid Co., Ltd., Sinopec, Sumitomo Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Acrylic Acid Derivatives Market Segmentation

By Derivative Type

- Acrylic Esters

- Acrylic Polymers

- Acrylic Amides

- Glacial Acrylic Acid (GAA))

By Application

- Surface Coatings

- Adhesives and Sealants

- Plastic Additives and Modifiers

- Water Treatment Chemicals

- Textiles and Fibers

- Detergents and Cleaners

By End-Use Industry

- Healthcare and Personal Care

- Construction and Infrastructure

- Automotive and Transportation

- Packaging and Consumer Goods

- Electronics and Semiconductors

- Agriculture

By Physical Form

- Liquid

- Powder/Granule

- Emulsion/Solution

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Acrylic Acid Derivatives Market

- BASF SE

- Arkema S.A.

- Dow Inc.

- Nippon Shokubai Co. Ltd.

- LG Chem Ltd.

- Mitsubishi Chemical Group

- Sibur Holding

- Wanhua Chemical Group Co. Ltd.

- Satellite Chemical Co. Ltd.

- Evonik Industries AG

- Formosa Plastics Corporation

- Sasol Limited

- Shanghai Huayi Acrylic Acid Co. Ltd.

- Sinopec

- Sumitomo Chemical Co. Ltd.

*- List not Exhaustive