Market Overview: Aluminum Nickel Catalysts Market to Reach $1,173.9 Million by 2034 as Hydrogen Economy, Green Ammonia, and AI-Led Catalyst Design Drive Industry Evolution

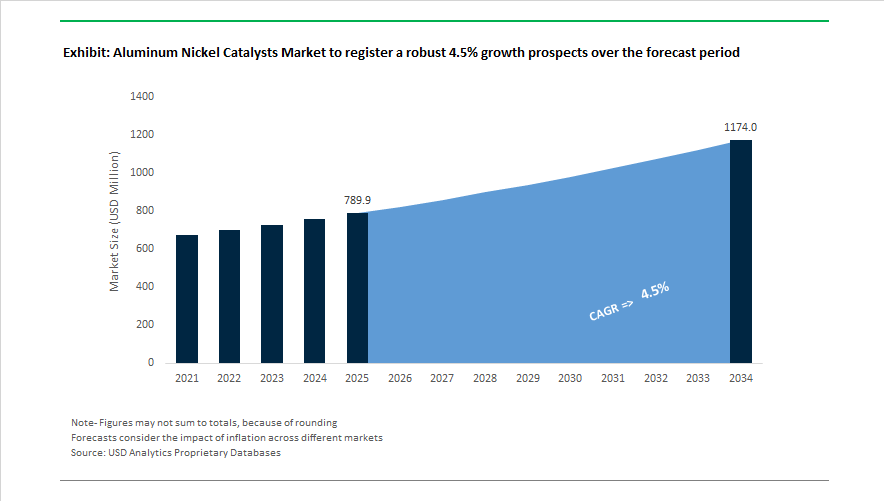

The global aluminum nickel catalysts market is projected to grow from $789.9 Million in 2025 to $1,173.9 Million by 2034, registering a 4.5% CAGR supported by expanding demand in hydrogen production, ammonia synthesis, methanol manufacturing, edible oil hydrogenation, pharmaceutical intermediates, and battery materials processing. Aluminum nickel catalysts are widely used for selective hydrogenation, reforming reactions, methanation, ammonia cracking, and catalytic synthesis loops, offering high surface area, stability, and resistance to deactivation. Market momentum is increasingly linked to the global transition toward green ammonia, Power-to-X technologies, sustainable fuels, and electrified chemical production, while traditional refining and biodiesel segments remain under pressure in developed regions. Innovation is focused on enhancing catalyst selectivity, durability, and performance under variable load conditions.

Capacity development and technological milestones accelerated in late 2024 when BASF and TODA expanded high-nickel cathode material production in Japan, strengthening battery material supply chains linked to nickel catalysis. Performance optimization advanced in mid-2025 as W.R. Grace & Co. upgraded its RANEY catalyst portfolio to improve pharmaceutical hydrogenation throughput. Structural realignment began in May 2025 when Johnson Matthey agreed to divest its Catalyst Technologies business to Honeywell International Inc., with completion expected by H1 2026. Digital transformation accelerated in August 2025 as BASF and Evonik Industries deployed AI and explainable machine learning to shorten catalyst development cycles. Trade policy shifts in September 2025 introduced new tariff considerations for nickel catalyst imports, prompting near-shoring strategies across North America. Industrial demand remained strong through 2025 as Clariant reported increased adoption of its hydrogenation catalysts in Asia-Pacific.

Energy transition applications intensified in December 2025 when the world’s first dynamic green ammonia plant in Denmark began operations using Topsoe nickel catalyst systems, earning industry recognition the same month at the S&P Platts Global Energy Awards. Leadership restructuring at Topsoe in January 2026 signaled accelerated commercialization of Power-to-X solutions. The same month, BASF introduced near-zero SVOC dispersion technologies relying on high-purity aluminum-nickel catalyst intermediates. Hydrogen infrastructure advanced in January 2026 as Topsoe validated its H2Retake ammonia cracking technology using DNK-series nickel catalysts. Financial resilience was confirmed in February 2026 when Evonik met EBITDA targets while prioritizing transformation toward advanced catalyst markets.

Strategic Trends and High-Value Opportunities Transforming the Aluminum Nickel Catalysts Market

Market Trend: Pharmaceutical Sector Drives Demand for Designer Catalysts with High Selectivity and Safety Controls

Pharma is becoming the most influential downstream segment shaping future demand. As patent-protected APIs increasingly rely on complex stereochemistry, hydrogenation reactions must achieve ultra-high selectivity without introducing metal contaminants that would risk regulatory rejection. The market is therefore shifting from generic Raney nickel to modified aluminum nickel catalysts engineered with dopants such as chromium, molybdenum, and cobalt that enhance selectivity by up to 30 percent, allowing cleaner reaction paths and fewer downstream purification steps. This selectivity gain translates into lower solvent usage, shorter cycle times, and reduced waste disposal.

Global compliance frameworks are reinforcing this transition. The USP <232> and ICH Q3D elemental impurity thresholds are forcing manufacturers to prove that catalytic residues remain below sub-ppm levels. Producers like Evonik and W.R. Grace have commercialized enhanced-settling wet catalysts that enable cleaner filtration and safer reactor discharge, reducing the operational risk of trace metals persisting in finished pharmaceutical ingredients. In parallel, handling safety is becoming central to plant modernization. Multi-purpose kilopound labs have begun adopting encapsulated and wet-slurry catalyst formats, which lower pyrophoric ignition risk and reduce insurance liabilities—a corporate finance-driven factor now influencing procurement.

Market Trend: Nickel Price Volatility and New Waste Regulations Fuel Growth of Circular Catalyst Recovery Ecosystems

Catalyst procurement is no longer viewed purely as a consumable expense; it is now a circular-asset management strategy. With nickel having historically surged beyond $20,000 per MT in previous commodity cycles, manufacturers are transitioning to closed-loop catalyst lifecycles in which spent catalyst is collected, processed, and regenerated into secondary feedstock. This shift is structurally reinforced by environmental law. The European Commission’s revised 2025 Waste Framework Directive mandates cradle-to-grave traceability, meaning disposal is no longer permitted without certified recycling pathways.

Hydrometallurgical innovation has made the economics viable. New recovery systems announced in late 2025 now allow 85% nickel recovery from spent Raney-type catalysts, enough to re-enter supply chains as certified low-carbon circular metals. This provides dual advantages: producers hedge against nickel pricing fluctuations and can claim 40–50% lower manufacturing carbon footprint when using recycled inputs. Sustainability-linked lending instruments are emerging in Europe and East Asia that reward companies which adopt catalyst lifecycle management, indicating that environmental compliance is beginning to translate into capital-cost advantages.

Market Opportunity: Aluminum Nickel Catalysts as the Backbone of Global Liquid Organic Hydrogen Carrier (LOHC) Scale-Up

The commercialization of hydrogen supply chains is creating one of the highest-value growth vectors for this market. Nickel-based systems are rapidly becoming the standard catalyst for converting hydrogen into Liquid Organic Hydrogen Carriers, allowing safe, ambient-temperature transport using existing oil logistics. Hydrogenation of aromatic molecules—such as toluene into methylcyclohexane (MCH)—is the critical enabling step that aluminum nickel catalysts perform at industrial scale.

A 2025 partnership between ENEOS and Honeywell UOP validated the concept commercially, demonstrating that LOHC systems paired with nickel catalysts can reduce long-distance hydrogen transport cost by 25–30% compared to liquefaction or compressed gas. With global hydrogen investments projected to exceed $300 billion by 2030, this represents not only a chemical catalyst market expansion but a foundational infrastructure opportunity. It also dovetails with government-funded hydrogen corridors in Japan, Germany, and the U.S., where LOHC storage densities of approximately 57 kg of H₂ per cubic meter make the system financially attractive for shipping-scale logistics.

Market Opportunity: Expanding Role in Bio-Based Platform Molecules and Sustainable Fuel Upgrading

The market is also benefiting from the emergence of a global bio-economy, where biomass waste streams are being valorized into fuels and high-purity chemicals. Unlike noble metal catalysts, aluminum nickel catalysts can tolerate high water content, oxygen-rich feedstocks, and contaminants typical of agricultural residue, vegetable oils, and lignocellulosic sugars.

In sorbitol and xylitol production, modified nickel catalysts enable glucose and xylose hydrogenation under elevated temperature without aluminum leaching, making them essential to large-scale sugar alcohol markets that support food, pharma, and polyol applications. In the climate-energy segment, aluminum nickel catalysts play a role in CO₂ methanation, with 2024–2025 research showing 87% CO₂ conversion at 250°C, enabling Power-to-Gas systems to store surplus renewable electricity as synthetic methane. The same catalytic families are used in hydrodeoxygenation of vegetable oils and fats to produce renewable diesel (HVO) and Sustainable Aviation Fuel (SAF)—both required to meet ICAO’s 2050 aviation Net Zero goals.

Aluminum Nickel Catalysts Market Share and Segmentation Insights

Market Share by Product Type: Activated Aluminum Nickel Leads While Supported Catalysts Accelerate

Activated aluminum nickel catalysts account for approximately 41% of global market demand in 2025, led by Raney-type systems used extensively in sugar alcohol production, pharmaceutical intermediates, and bulk chemical hydrogenations such as adiponitrile and aniline. Their high surface area delivers strong activity at moderate temperatures, making them cost-effective workhorse catalysts, although pyrophoricity requires strict handling protocols. Supported nickel catalysts rank second and represent the fastest-growing segment, favored for superior thermal stability, lower fire risk, and tunable selectivity in edible oil hydrogenation and benzene-to-cyclohexane processing. Non-activated aluminum nickel alloys retain a shrinking niche among integrated producers that perform in-house activation. Metal foam and monolithic catalysts remain the smallest but most advanced category, offering low pressure drop and enhanced mass transfer in continuous flow and renewable processing, although high fabrication costs currently limit broader adoption.

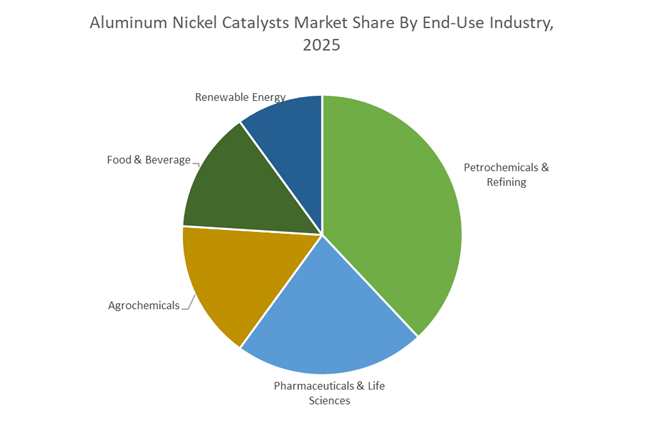

Market Share by End-Use Industry: Petrochemicals Anchor Volume While Renewables Drive Growth

Petrochemicals and refining represent roughly 38% of aluminum nickel catalyst consumption in 2025, supported by hydrogenation steps in cyclohexane production, sulfur removal, and C4 stream purification, with demand closely tied to refinery utilization and capacity additions in Asia and the Middle East. Pharmaceuticals and life sciences deliver the highest margins, using high-purity nickel catalysts for API intermediates, vitamin synthesis, and sugar alcohol excipients, with growth driven by contract manufacturing expansion in India and China. Agrochemicals provide steady, crop-cycle-linked volumes for herbicide and fungicide intermediates, while food and beverage applications remain mature, centered on selective hydrogenation of edible oils and low-calorie sweetener production. Renewable energy is the fastest-growing end-use, fueled by hydrodeoxygenation for renewable diesel, biomass upgrading, and emerging hydrogen carrier systems, positioning clean fuels as the primary growth frontier for aluminum nickel catalyst suppliers.

Competitive Landscape: Flow Chemistry, Chemical Recycling, and Green Hydrogenation Redefining the Aluminum Nickel Catalysts Market

The Aluminum Nickel Catalysts Market is undergoing a structural shift as hydrogenation moves beyond conventional petrochemicals into renewable diesel, chemical recycling, pharmaceuticals, and circular polymers. Competitive advantage increasingly depends on catalyst safety (ready-to-use formats), continuous-flow compatibility, sulfur resistance, and lifecycle services including regeneration and metal recovery. Market leaders are integrating aluminum-nickel catalyst portfolios with refining technologies, bio-feedstock processing, and waste-plastic upgrading, positioning these systems as critical enablers of low-carbon manufacturing and next-generation chemical synthesis.

W. R. Grace & Co. anchors global hydrogenation standards with Raney® nickel leadership

W. R. Grace & Co. remains the global benchmark in aluminum nickel catalysts through ownership of the original Raney® brand. Its Active 2800 and 3200 series are industry standards for hydrogenating nitriles and nitro compounds into high-purity amines. In November 2025, Grace fully acquired the ART Hydroprocessing™ joint venture from Chevron, integrating catalyst manufacturing directly with refining technologies and EnRich® guard catalysts for renewable diesel. Backed by Standard Industries, Grace benefits from deep vertical integration and global logistics. Strategically, the company is expanding into chemical recycling, applying nickel catalysts to convert waste plastics into refined chemical feedstocks.

Evonik Industries AG advances ready-to-use aluminum nickel catalysts for continuous flow chemistry

Evonik Industries AG leads in high-performance specialty catalysts, emphasizing safer, pre-activated aluminum-nickel systems for modern flow reactors. Its Metalyst® portfolio delivers stabilized alloys that mitigate the pyrophoric risks of traditional nickel powders. In late 2025, Evonik launched the Noblyst® F series, engineered specifically for continuous pharmaceutical and fine chemical hydrogenation. The company also commissioned a world-scale alkoxides and catalyst facility in Singapore in August 2025, strengthening its Asia-Pacific supply base. Evonik’s Full-Loop Management model integrates catalyst supply with spent catalyst recycling, providing closed-loop sustainability for specialty chemical producers.

Johnson Matthey pivots from nickel catalysts toward recycling and hydrogen technologies

Johnson Matthey is reshaping its portfolio, historically known for Sponge Metal™ aluminum-nickel catalysts used in edible oil hydrogenation and polyol production. The company agreed to sell its Catalyst Technologies business to Honeywell International Inc., with completion expected in H1 2026, signaling a shift toward metal refining and hydrogen technologies. Concurrently, Johnson Matthey is commissioning a new PGM and base-metal refinery to support catalyst recovery and circularity. Its Lean and Cash Generative strategy prioritizes hydrogen systems and emission control while divesting legacy catalyst segments.

BASF SE integrates aluminum nickel catalysts into green industrial transformation

BASF SE leverages its Verbund system to deliver tightly integrated aluminum-nickel catalyst solutions for solvent dearomatization and cyclohexanol production. Under its Winning Ways strategy (2024–2026), BASF focuses on enabling customer decarbonization through lower-CO₂ and circular catalyst platforms. Its Ni 3354 E supported nickel extrudates are widely used in phenol-to-cyclohexanol conversion, while newer nickel-on-alumina catalysts with enhanced selectivity target cyclohexanone production for Nylon 6 intermediates. BASF’s Environmental Catalyst and Metal Solutions division continues to play a central role in clean energy transitions through 2026.

Axens combines aluminum nickel catalysts with refinery process licensing

Axens, a subsidiary of IFP Energies nouvelles, stands out by pairing aluminum-nickel catalyst manufacturing with proprietary hydroprocessing technologies. Its AX 746 and LD 746 catalysts are engineered for sulfur tolerance during olefin and aromatic saturation. The newly introduced Symphony® series boosts hydrogen production and reformate yields while lowering refinery carbon intensity. Axens’ dual capability in catalyst supply and process licensing ensures optimal integration in new refinery builds. Strategically, the company is transitioning toward bio-based feedstock processing, adapting nickel catalysts to higher oxygenate content in renewable naphtha streams.

Sinopec scales aluminum nickel catalysts through domestic innovation and massive internal demand

Sinopec is rapidly expanding aluminum-nickel catalyst production to achieve technological sovereignty across China’s chemical sector. The company dominates catalysts for caprolactam production from cyclohexane, supporting a roughly 30% capacity expansion across Asia-Pacific. Heavy investment in nano-catalyst design is improving surface area and reaction kinetics for bulk chemical manufacturing. Sinopec’s unique advantage lies in its vertically integrated ecosystem: internal refineries and petrochemical plants serve as real-world testing platforms, accelerating optimization of aluminum-nickel formulations for large-scale deployment.

United States Aluminum Nickel Catalysts Market: Domestic Manufacturing Pull and AI-Led Catalyst Development

The United States has strengthened domestic production of aluminum nickel catalysts following 2025 tariff adjustments on imported chemical intermediates. These changes favored local manufacturers supplying activated aluminum-nickel catalysts for high-pressure hydrogenation used in pharmaceutical APIs and fine chemicals. Capacity modernization has been central to this shift. W. R. Grace & Co. completed a 25% expansion at its South Haven, Michigan site in late 2024, adding a 4,000-gallon Hastelloy centrifuge engineered to withstand corrosive catalyst processing environments.

Innovation momentum accelerated in 2025 as W. R. Grace partnered with Molecule.one to integrate AI and automation into nickel catalyst discovery, shortening development cycles for proprietary systems used in peptide synthesis and specialty building blocks. Demand from energy markets also rose as U.S. refineries increased utilization of nickel catalysts for desulfurization to comply with stricter U.S. Environmental Protection Agency Tier 3 fuel standards and to support renewable diesel production. To manage raw material volatility, producers implemented tiered pricing frameworks to hedge exposure to aluminum and nickel ore costs.

Germany Aluminum Nickel Catalysts Market: Flow Chemistry Adoption and Net-Zero Catalyst Manufacturing

Germany is positioning aluminum nickel catalysts at the intersection of sustainability and pharmaceutical process safety. Evonik Industries embedded its Next Generation Solutions targets into 2025 operations, with a significant share of its catalyst portfolio now meeting enhanced sustainability criteria. Production of high-efficiency Raney-type catalysts at Hanau has benefited from advanced process controls and waste-heat upcycling, enabling the site to approach net-zero Scope 1 and 2 emissions by late 2025.

Process innovation is equally important. In October 2025, Evonik introduced the Noblyst F series of nickel catalysts tailored for continuous flow chemistry, which is increasingly replacing batch hydrogenation in German pharmaceutical manufacturing to improve throughput and operator safety. Circularity is advancing through regeneration. German firms are leading Europe’s shift to ex-situ activation and rejuvenation of spent catalysts, reinforced by acquisition strategies from Axens that strengthen closed-loop metal recovery and reuse.

India Aluminum Nickel Catalysts Market: Critical Minerals Policy and Agrochemical Demand Expansion

India’s aluminum nickel catalysts landscape is being shaped by national policy focused on critical mineral resilience. The National Critical Mineral Mission became operational in January 2025, allocating ₹1,500 crore to incentivize domestic recycling of nickel and cobalt from spent catalysts and industrial residues. Complementing this, the Ministry of Mines introduced a 20% capital subsidy for projects commencing production by 2026, directly supporting recovery of nickel from used industrial catalysts and reducing import dependence.

End-use demand is rising alongside policy support. Aluminum nickel catalysts saw increased utilization in 2025 as India expanded Make in India initiatives for agrochemical intermediates, particularly hydrogenation steps in herbicide and insecticide production. Long-term feedstock security is being reinforced through public sector exploration, with the Geological Survey of India scaling nickel-rich ore exploration to hundreds of projects for the 2025 to 2026 field season. This combination of recycling, exploration, and downstream demand is anchoring a more self-reliant catalyst ecosystem.

China Aluminum Nickel Catalysts Market: Hydrogenation Efficiency and Export-Oriented Scale

China continues to emphasize performance efficiency and scale in aluminum nickel catalysts. In 2025, activated Raney nickel surpassed half of domestic catalyst revenue relevance, reflecting its superior reactivity in fine chemical hydrogenation. Refining remains a dominant application as national mandates to produce low-sulfur fuels for maritime and logistics uses sustained high catalyst utilization into early 2026.

Export capability is a defining strength. China recorded a peak in catalyst shipments to Southeast Asia and the Middle East during 2025, leveraging cost-competitive manufacturing and supportive trade policies for chemical processing agents. R&D priorities are shifting toward structural innovation, with Chinese laboratories advancing X3D printing of catalyst architectures to increase surface area and lower energy consumption in large hydrogenation reactors.

Singapore Aluminum Nickel Catalysts Market: Regional Hub for Circular Catalysts and Biofuels

Singapore has consolidated its role as a regional hub for aluminum nickel catalysts serving Asia’s biodiesel and chemical recycling sectors. In August 2025, Evonik Industries inaugurated a world-scale facility on Jurong Island, designed to supply catalysts across Asia with high logistical efficiency and quality consistency.

Government support has been instrumental. Through JTC Corporation, Singapore has provided infrastructure and utilities that enable catalyst producers to scale circular chemical production. This ecosystem supports regeneration, reuse, and efficient distribution of aluminum nickel catalysts within an integrated petrochemical and logistics network.

Strategic Positioning in Aluminum Nickel Catalysts by Country

Aluminum Nickel Catalysts Market County Level Snapshot

|

Country

|

Strategic Focus

|

Implication for Aluminum Nickel Catalysts

|

|

United States

|

Domestic production and AI-enabled design

|

Faster development cycles and secure hydrogenation supply

|

|

Germany

|

Flow chemistry and net-zero manufacturing

|

Safer processes and sustainable Raney catalyst production

|

|

India

|

Critical mineral recycling and agrochemicals

|

Reduced import reliance and rising hydrogenation demand

|

|

China

|

High-efficiency Raney nickel and exports

|

Cost-competitive scale with advanced reactor designs

|

|

Singapore

|

Circular hub and regional logistics

|

Reliable catalyst supply for biofuels and recycling

|

Aluminum Nickel Catalysts Market Report Scope

Aluminum Nickel Catalysts Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$789.9 Million

|

|

Market Size (2034)

|

$1173.9 Million

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Product Type (Activated Aluminum Nickel Catalysts, Non Activated Aluminum Nickel Catalysts, Supported Nickel Catalysts, Metal Foam and Monolithic Catalysts), By Form (Powder, Granules and Pellets, Extruded Structures), By Application (Hydrogenation, Desulfurization, Methanation, Dehydrogenation and Polymerization, Ammonia Cracking), By End Use Industry (Petrochemicals and Refining, Pharmaceuticals and Life Sciences, Agrochemicals, Food and Beverage, Renewable Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, W R Grace and Company, Johnson Matthey, Axens, Haldor Topsoe, Clariant AG, Nikko Rica Corporation, Shandong Jiahong Chemical, Himalaya Industries, Gorwara Chemical Industries, Vineeth Chemicals, Hangzhou Jiali Metal Technology, Sinopec Catalyst Company, Ketjen

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aluminum Nickel Catalysts Market Segmentation

By Product Type

- Activated Aluminum Nickel Catalysts

- Non Activated Aluminum Nickel Catalysts

- Supported Nickel Catalysts

- Metal Foam and Monolithic Catalysts

By Form

- Powder

- Granules and Pellets

- Extruded Structures

By Application

- Hydrogenation

- Desulfurization

- Methanation

- Dehydrogenation and Polymerization

- Ammonia Cracking

By End Use Industry

- Petrochemicals and Refining

- Pharmaceuticals and Life Sciences

- Agrochemicals

- Food and Beverage

- Renewable Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aluminum Nickel Catalysts Industry

- BASF SE

- Evonik Industries AG

- W R Grace and Company

- Johnson Matthey

- Axens

- Haldor Topsoe

- Clariant AG

- Nikko Rica Corporation

- Shandong Jiahong Chemical

- Himalaya Industries

- Gorwara Chemical Industries

- Vineeth Chemicals

- Hangzhou Jiali Metal Technology

- Sinopec Catalyst Company

- Ketjen

*- List not Exhaustive