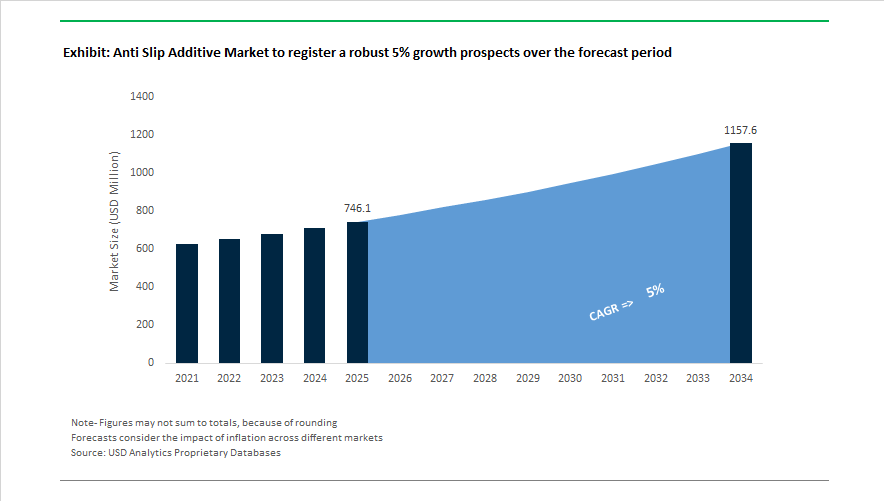

Market Overview: Anti Slip Additive Market Expands Toward $1,157.4 Million by 2034 as Safety Flooring, Marine Decks, and Industrial Infrastructure Drive High-Traction Coating Demand

The anti slip additive market is valued at $746.1 Million in 2025 and is projected to reach $1,157.4 Million by 2034, advancing at a 5% CAGR. Demand growth is anchored in industrial flooring systems, marine deck safety coatings, architectural floor paints, resinous safety surfaces, powder coating texturizers, and high-friction polymer dispersions used to meet tightening occupational safety standards. End-use sectors such as oil and gas platforms, ship decks, public infrastructure walkways, manufacturing plants, and commercial buildings increasingly require coatings engineered with traction-enhancing fillers, matting agents, wax-modified slip control additives, and abrasion-resistant resins. Market momentum reflects the shift from conventional grit-based systems toward engineered micro-texture technologies that balance slip resistance, cleanability, durability, and VOC compliance.

Strategic portfolio realignments began in 2024 when PPG Industries partnered with Shaw Industries to integrate anti-slip additives into full resinous flooring systems, while divesting its U.S. and Canada architectural coatings unit in December 2024 to concentrate on industrial protective technologies. Sustainability and regulatory shifts intensified during October 2025 when BASF agreed to a €7.7 billion coatings divestiture while expanding low-VOC dispersion capacity in Türkiye to support waterborne anti-slip floor paints. In the same month, Sherwin-Williams acquired BASF’s Suvinil business to strengthen its South American construction footprint, a region with strong demand for anti-slip walkways and safety flooring. Consolidation accelerated in November 2025 as AkzoNobel and Axalta announced a merger, combining marine deck safety technologies with industrial flooring additive expertise.

Technology innovation intensified through 2025 with AI-driven durability modeling adopted by major formulators to predict traction retention over long service cycles. In February 2026, Clariant introduced PFAS-free Ceridust 8170 M and highlighted Licocare RBW Vita bio-based waxes that deliver controlled slip resistance. Evonik Industries expanded HTPB binder capacity the same month to supply flexible, impact-resistant anti-slip coatings for offshore and heavy-duty infrastructure. Marine safety integration advanced in February 2026 as Hempel applied next-generation silicone technologies on Maersk vessels, aligning deck traction standards with hull coating performance. Leadership transition at Hempel announced in January 2026 reinforces long-term focus on sustainable, bio-based high-traction coatings for energy and marine sectors.

Trends and Opportunities Reshaping Commercial Scale, Procurement Strategy and Material Science in the Anti Slip Additive Market

Flooring Specifications Are Shifting Toward “Embedded Safety” Using Integrated Anti-Slip Additives

In 2025, the Anti Slip Additive Market is seeing a decisive move away from “topical coatings applied after installation” toward integrated traction systems, where anti-slip particles are chemically bonded inside epoxy, polyaspartic and polyurethane flooring resins. This trend is directly aligned with industrial flooring procurement requirements set by ANSI A326.3 and EN 13845 (2025 update), which now define slip-resistance not as a one-time property, but as a performance metric that must remain above a 0.42 DCOF threshold after 100,000 abrasion cycles. Major producers like AkzoNobel and PPG have restructured their 2025 portfolios to support sustainability compliance: new systems incorporate up to 30% bio-derived resin content and use micronized polymer waxes that prevent the settling or granularity failures found in traditional sand-filled systems. EEAT-relevant technical data shows that Sherwin-Williams’ ResuGrip™ additive expansion (2025) specifically targets gloss-control optimization, meaning traction is enhanced without deteriorating visual finish, a strategic requirement for retail, hospitality and corporate interiors.

Cleanrooms and Food-Pharma Sites Require Chemically-Resistant, Transparent Anti-Slip Additives

Demand from semiconductor fabs, pharmaceutical plants and food-processing facilities is shaping a new category: “hygienic traction additives.” These systems require optical clarity, smooth microbiological cleanability and chemical resistance. Under the 2025 EU Health and Safety Welfare update, cleanroom flooring must be non-porous and cleanable to microbiological sterility, which has driven adoption of glass bead and clear polymer grit additives that do not trap contaminants. High-performance epoxy linings such as PPG PHENGUARD® 985 now pair with inert anti-slip particles to maintain a Pendulum Test Value >36, even when floors are contaminated with fatty acids or pharmaceutical reagents. In semiconductor fabs, traction compounds are increasingly co-formulated with Electrostatic Dissipative (ESD) fillers, enabling anti-slip control without interfering with robotic AGV laser-guided navigation systems—placing additives directly in the critical path of uptime and automation reliability.

Offshore Wind Infrastructure Creates a High-Volume Growth Window for Ultra-Durable Anti Slip Systems

Global renewable investments are directly expanding commercial volume for anti-slip additives. Offshore wind platforms, helipads, and turbine transition pieces require permanent safety surfaces compliant with ClassNK 2025 Floating Offshore Wind Guidelines, which mandate coatings capable of surviving C5-M marine corrosivity environments. Additives must enable textures that withstand 1,000+ hours of salt spray exposure while maintaining traction in oil-contaminated and continuously wet conditions. PPG highlighted in October 2025 that unmanned offshore platforms require zero-maintenance slip-resistant decks, using high-build epoxies with UV-resistant aggregates sourced from rPET waste streams. Worker safety mandates in EU offshore projects now require high-visibility additive pigmentation to prevent transfer-fall accidents, making anti-slip additives a compliance-driven must-have, not a discretionary accessory.

Additive Manufacturing and 3D-Printed Concrete Unlocks Customizable Traction Geometry

A new commercial frontier is forming where anti-slip additives are engineered directly into 3D-printable concrete (3DPC), enabling friction surfaces at the moment of extrusion. A 2025 RILEM Technical Letters study confirms that interlayer bond strength and surface porosity are materially influenced by recycled rubber or quartz anti-slip particles injected at the print nozzle. Municipal infrastructure pilots in Nanjing (2024) and Dubai (2025) showed that biomimetic surface geometries printed with embedded aggregates achieved 20% higher slip resistance than cast concrete. Demand is also tied to regulatory sustainability incentives: 40% of 3DPC projects in 2025 now use recycled glass or polymer aggregates to secure LEED or circular-economy credits while lowering raw material logistics costs. For governments and contractors, anti-slip additives are directly linked to reducing lifecycle maintenance and lowering injury liability exposure, shaping long-term procurement frameworks.

Anti-Slip Additive Market Share and Segmentation Insights

Market Share by Material Type: Aluminum Oxide Leads Abrasion-Resistant Systems as Glass Microspheres Gain Safety Traction

Aluminum oxide holds approximately 31% of the global anti-slip additive market in 2025, dominating due to extreme hardness (9 on the Mohs scale), superior abrasion resistance, and chemical stability in high-traffic industrial flooring and marine environments. It is the preferred aggregate for epoxy floor coatings, polyurethane deck systems, and high-friction surface treatments where durability is mission-critical. Silica remains a widely used, cost-effective alternative, with amorphous silica favored in water-based architectural coatings and crystalline silica specified for heavy-duty textured paints. Glass microspheres are expanding rapidly, offering slip resistance without sharp edges and added light reflectivity for safety markings. Sand and quartz continue in low-cost construction but are gradually losing share to engineered alternatives. Polymer beads serve soft-traction applications in consumer goods, while natural garnet occupies a niche eco-certified segment, particularly in European green building specifications.

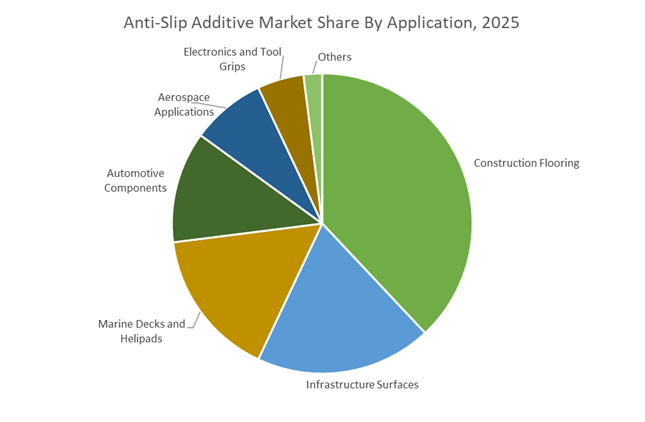

Market Share by Application: Construction Flooring Dominates as Infrastructure Safety Mandates Drive High-Friction Demand

Construction flooring represents roughly 38% of anti-slip additive demand in 2025, encompassing commercial kitchens, hospital operating rooms, ramps, and staircases, where OSHA and workplace safety regulations are intensifying slip-resistance requirements. Infrastructure surfaces form a critical secondary segment, including bridges, railway platforms, and pedestrian crossings, where high-friction surface treatments using aluminum oxide or calcined bauxite are mandated to reduce vehicular skidding and pedestrian accidents. Marine decks and helipads demand corrosion-resistant, heavy-duty aggregates capable of maintaining traction under wet and oily conditions. Automotive applications increasingly favor polymer beads in pedals and interior grips to support lightweighting strategies. Aerospace relies on lightweight microspheres for entry ramps and maintenance walkways. Electronics and tool grips remain a premium niche, embedding anti-slip additives into molded components to enhance tactile safety without abrasive sharpness.

Anti Slip Additive Market Competitive Landscape

The global anti slip additive market is evolving rapidly as coatings, packaging films, construction materials, automotive interiors, and industrial flooring increasingly demand PFAS-free, bio-based, and high-durability slip control solutions. Market leaders are investing in mass-balance chemistry, precision particle engineering, and automated R&D platforms to deliver consistent coefficient of friction (COF), enhanced surface feel, and long-term abrasion resistance. Strategic priorities across North America, Europe, and Asia-Pacific include sustainable surface modifiers, localized technical support, and integration of anti-slip performance directly into polymer matrices. Innovation in silica, alumina, wax, and acrylic-based additives is reshaping competitive dynamics, with suppliers aligning portfolios to regulatory pressure, EV mobility, and high-speed film extrusion.

PFAS-free process innovation and rapid R&D cycles anchor BYK-Chemie GmbH leadership

BYK remains the technological benchmark in anti slip additives, leveraging high-throughput screening to accelerate customized coating and film solutions. Effective February 2026, BYK implemented a 5.2% portfolio price adjustment to fund its Sustainability 2030 roadmap, prioritizing bio-based surface modifiers. At K 2025, the company launched BYK-MAX P 4110, a breakthrough PFAS-free process additive that prevents melt fracture and boosts production speed in anti-slip film extrusion. Early 2026 also saw an expanded distribution partnership with Krahn Chemie across Poland, Finland, and the Baltics. BYK’s automated HTS facility can evaluate up to 220 samples in 24 hours, dramatically shortening development cycles for industrial floor coatings and packaging films.

Mass-balance circular additives drive performance at Evonik Industries AG

Evonik has positioned itself as a global leader in circular anti slip additives through mass-balance chemistry and advanced particle engineering. In 2025, it launched TEGO® Wet 270 eCO and TEGO® Foamex 812 eCO, enabling a 40% to 60% reduction in fossil carbon footprint while maintaining premium wetting and slip control. October 2025 marked the opening of Evonik’s Alu5 fumed alumina plant in Yokkaichi, strengthening supply of aluminum oxide-based anti-slip and scratch-resistance solutions across Asia. A streamlined U.S. and Canada distribution overhaul in early 2026 further improved logistics for TEGO® and AERODISP® portfolios, supporting precision friction in automotive interiors and leather finishes.

Bio-based wax technologies redefine compliance at Clariant AG

Clariant continues to lead green chemistry adoption in the anti slip additive market with renewable waxes and PFAS-free micronized polymers. Its Licocare® RBW Vita range, derived from rice bran wax, was expanded in 2026 to deliver multifunctional slip control and matting for textile coatings in India and Southeast Asia. At PaintIndia 2026, Clariant introduced Ceridust® 8170 M, a PTFE-free additive engineered for fine powder-coating textures. Through its AddWorks® PPA series, Clariant integrates anti-slip performance directly into polyolefin film extrusion, ensuring durability from processing to end use while helping customers transition toward halogen-free, regulation-ready systems.

System-level verification strengthens PPG Industries, Inc. market presence

PPG combines additive science with real-world coating expertise, delivering total-system anti slip solutions across marine, protective, and industrial segments. Drawing on technologies from Laurel and PSI, PPG supplies PTFE and mica-based additives with tightly controlled particle size. In late 2025, its ENVIROLUXE™ powder coatings showcased PFAS-free anti-slip textures using recycled rPET. PPG’s 2026 service model includes on-site COF testing and digital color matching, ensuring safety upgrades preserve brand aesthetics. The company dominates offshore and marine applications with SIGMAGLIDE® and STEELGUARD® platforms, where reliable anti-slip performance is mission-critical for crew safety and corrosion resistance.

Precision particle control differentiates The Lubrizol Corporation

Lubrizol focuses on rheology and surface feel, offering one of the industry’s broadest portfolios of wax-based anti slip additives. Its PowderAdd™ range supports controlled friction and aesthetics in cured powder coatings, while micronized powders and liquid dispersions address anti-blocking in packaging films. Lubrizol’s particle size control, defined by Dv50, Dv90, and Dv98 metrics, enables formulators to optimize performance across thin can coatings and thick wood finishes. Expanded North American manufacturing capacity in late 2024 supported rising 2025 to 2026 demand for high-durability films. The company is also a leader in OEM wood coatings and digital inks, delivering soft-feel, non-sticking surfaces.

Specialty materials focus elevates Arkema S.A.

Arkema has sharpened its anti slip strategy by divesting commodity plastic additives in early 2026 and refocusing on high-value coating solutions. The company now targets urbanization and mobility trends, developing anti-slip additives for methacrylate structural adhesives and EV battery components. Through its Adhesive Solutions and Advanced Materials platforms, Arkema delivers integrated smart surfaces combining slip resistance with fire retardancy and UV stability. Its core strength in acrylic copolymer chemistry enables clear anti-slip additives that preserve optical clarity in architectural glass and premium plastics, positioning Arkema as a key innovator in transparent, high-performance surface engineering.

China Anti Slip Additive Market: Verbund Manufacturing, Silicone Depth, and Export-Led Scale

China remains the most aggressive capacity builder in the anti slip additive industry, leveraging integrated Verbund chemistry and export-oriented scale. In late 2025, BASF is scheduled to commence operations of a high-performance additive line at its Nanjing site, using Controlled Free Radical Polymerization technology to manufacture advanced dispersants and anti-slip surface modifiers for automotive OEM and industrial coatings. This approach enables tighter particle-size control and consistent friction coefficients, which are increasingly demanded by global OEM specifications.

Parallel investments are strengthening China’s silicone backbone. Wacker Chemie AG commissioned a specialty silicones complex in Zhangjiagang in May 2025, producing silicone emulsions and fluids used as high-durability anti-slip additives in construction coatings and architectural flooring across Asia. Additive durability and UV stability are further reinforced by Clariant, which began construction of a second multifunctional additive line in Cangzhou to support UV-resistant and process-stable anti-slip polymer systems. Sustainability is now embedded into production, as Evonik expanded green amine production in Nanjing using 100% renewable electricity, supporting epoxy and polyurethane anti-slip flooring systems. These investments coincide with a 27.72% year-on-year rise in exports of high-value coatings and additives in 2025, underscoring China’s pivot from volume chemicals toward globally competitive, low-VOC surface solutions.

Germany Anti Slip Additive Market: PFAS Exit, Mass-Balanced Chemistry, and Lifecycle Compliance

Germany is setting the global benchmark for regulatory-aligned innovation in anti slip additives, driven by environmental legislation and public safety standards. BYK Additives committed to transitioning its entire global portfolio to PFAS-free alternatives by the end of 2025, replacing fluorinated slip and leveling agents with environmentally compatible surface-active chemistries. This move directly addresses tightening EU chemical scrutiny while preserving controlled slip resistance across flooring and industrial coatings.

At the same time, carbon accounting is becoming a differentiator. In March 2025, Evonik launched its first mass-balanced coating additives, including TEGO® Wet 270 eCO, delivering anti-slip performance with more than 40% bio-based carbon. Evonik has also transitioned all PU-additive production assets to green electricity, aligning anti-slip cross-linkers with Scope 3 reduction targets required by European contractors. German R&D leadership was visible at the European Coatings Show 2025, where chemical leaders showcased “debonding on demand” concepts that allow anti-slip floor layers to be removed and recycled at end of life. These innovations directly support compliance with EN 13845 slip-resistance standards, driving increased adoption of PTV 36+ compliant additives in transport hubs, hospitals, and high-traffic public buildings.

India Anti Slip Additive Market: Food-Contact Regulation and Bio-Based Masterbatch Momentum

India’s anti slip additive industry is being reshaped by packaging regulation and bio-based policy incentives. The Food Safety and Standards Authority of India introduced Packaging Amendment Regulations in 2025 that reclassified food-grade packaging as critical, mandating non-migratory anti-slip additives for films, containers, and closures. This has accelerated demand for compliant additives that ensure stack stability and handling safety without contaminant migration.

Domestic capacity is expanding in response. AM Masterbatch Pvt Ltd scaled up silica-based anti-slip concentrate production in mid-2025 to serve pharmaceutical and consumer goods packaging. Policy support under India’s BioE3 framework is further encouraging the development of bio-fermented anti-slip agents, particularly for marine and port infrastructure where corrosion resistance and environmental safety are paramount. Together, regulatory clarity and targeted incentives are positioning India as a fast-growing hub for compliant, export-ready anti-slip masterbatches.

United States Anti Slip Additive Market: Infrastructure Safety and Nano-Enabled Transparency

In the United States, demand for anti slip additives is closely linked to infrastructure rehabilitation, workplace safety, and aesthetic performance. Under the Infrastructure Investment and Jobs Act, state authorities accelerated the deployment of anti-slip bridge deck coatings and pedestrian walkway treatments in 2025, with a preference for aluminum oxide aggregates that deliver extreme-load durability under freeze-thaw cycling.

Material innovation is advancing in parallel. U.S. manufacturers, including Dow, integrated nano-silica particles into their 2025 additive portfolios, enabling high-friction finishes that maintain optical clarity in decorative flooring and architectural coatings. Regulatory pressure is reinforcing adoption, as updates to OSHA workplace safety guidelines in 2025 contributed to a documented increase in epoxy-based anti-slip additives across warehouses and logistics centers. This combination of safety regulation and nanotechnology is driving a shift toward performance-transparent anti-slip systems rather than visibly textured legacy solutions.

Structural Drivers in the Anti Slip Additive Industry by Country

Anti Slip Additive Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Industry Implication

|

|

China

|

Verbund-scale capacity and export focus

|

Global supply of advanced, low-VOC anti-slip additives

|

|

Germany

|

PFAS-free transition and lifecycle compliance

|

Premium, regulation-ready anti-slip chemistries

|

|

India

|

Food-contact regulation and BioE3 incentives

|

Rapid growth in non-migratory, bio-based masterbatches

|

|

United States

|

Infrastructure safety and nano-material integration

|

Durable, transparent anti-slip solutions for public and industrial use

|

Anti Slip Additive Market Report Scope

Anti Slip Additive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$746.1 Million

|

|

Market Size (2034)

|

$1157.4 Million

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Material Type (Aluminum Oxide, Silica, Polyethylene and Polypropylene Beads, Glass Microspheres, Sand and Quartz, Natural Garnet), By Additive Nature (Powder, Liquid Dispersion, Masterbatches, Aggregate Mix), By Coating Compatibility (Acrylic Coatings, Epoxy Coatings, Polyurethane Coatings, Water Based Systems, Solvent Based Systems, UV Curable Coatings), By Application (Construction Flooring, Marine Decks and Helipads, Automotive Components, Aerospace Applications, Infrastructure Surfaces, Electronics and Tool Grips)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BYK Chemie GmbH, Evonik Industries AG, BASF SE, PPG Industries Inc, Clariant AG, Wacker Chemie AG, Dow Inc, Hempel AS, Axalta Coating Systems, Sherwin Williams Company, Lubrizol Corporation, RPM International Inc, Henkel AG and Co KGaA, Arkema SA, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti Slip Additive Market Segmentation

By Material Type

- Aluminum Oxide

- Silica

- Polyethylene and Polypropylene Beads

- Glass Microspheres

- Sand and Quartz

- Natural Garnet

By Additive Nature

- Powder

- Liquid Dispersion

- Masterbatches

- Aggregate Mix

By Coating Compatibility

- Acrylic Coatings

- Epoxy Coatings

- Polyurethane Coatings

- Water Based Systems

- Solvent Based Systems

- UV Curable Coatings

By Application

- Construction Flooring

- Marine Decks and Helipads

- Automotive Components

- Aerospace Applications

- Infrastructure Surfaces

- Electronics and Tool Grips

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Anti Slip Additive Industry

- BYK Chemie GmbH

- Evonik Industries AG

- BASF SE

- PPG Industries Inc

- Clariant AG

- Wacker Chemie AG

- Dow Inc

- Hempel AS

- Axalta Coating Systems

- Sherwin Williams Company

- Lubrizol Corporation

- RPM International Inc

- Henkel AG and Co KGaA

- Arkema SA

- Huntsman Corporation

*- List not Exhaustive