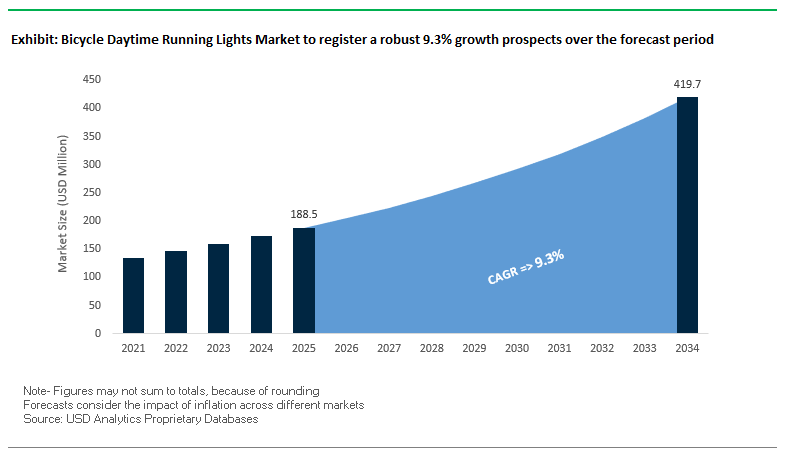

The global bicycle daytime running lights (DRL) market is projected to expand from USD 188.5 million in 2025 to USD 419.7 million by 2034, growing at a CAGR of 9.3%. At the nexus of cycling technology and safety, this market is experiencing intense demand from commuter cyclists, recreational cyclists, as well as competitive riders. European regulatory requirements and heightened public recognition of the importance of cyclist visibility have driven adoption faster, while integration of technology, e-bike expansion, and online retail are reshaping the competitive dynamic. DRLs are increasingly becoming multi-purpose safety products that include lighting, connectivity, radar, and even camera functionality, making them an integral part of contemporary cycling equipment.

The bike DRL market is changing swiftly with product announcements, strategic alliances, and differentiation through innovation. In August 2025, Garmin launched the Varia VUE, a front light that comes with a built-in dash cam and live radar display. All-weather use is made possible by it, and it provides up to 20 hours of battery life, combining several safety features in one device. In the same vein, Topeak's 2025 lineup also put more emphasis on safety-oriented lights, specifically on e-bikes, indicating the company's intention to redirect its accessory line towards the trend of e-mobility.

In the same month, American Exchange Group's VENUS Fashion acquisition although out of the DRL segment represented an overarching trend towards diversification in consumer product lines, a move which will shape future consolidations among accessory brands. Lupine kept the pressure on in the high-performance lighting segment with new products aimed at professional and enthusiast-level cyclists in 2025. Media attention continues to be an important driver of consumer selection, as during June 2025, Bicycling.com included the Cygolite Metro Plus 800 and Hotshot lights among their top recommendations, highlighting the competitive significance of established DRL brands.

In November 2024, Bontrager Outdoors (previously Braxton Creek) showed a new 2025 product line, with backdoor implications for Trek's accessory development cycle. This continued incorporation of DRLs into overall bike design strategies guarantees lights will continue to be an expected safety feature instead of an aftermarket option.

Advanced drag-reduction technologies, previously reserved for Olympic-level competition, are now available in the mass-market swimwear marketplace. Following on from the advances such as NASA collaboration on the "Fastskin" suit designed to replicate the shark's dermal denticles to achieve quantifiable drag reduction brands are transferring similar principles to consumer-level performance swimwear. Textile engineering studies verify that drag-reducing swimwear can shave off swim times by tiny but significant fractions, of interest to competitive amateurs, triathletes, and serious lap swimmers. Tech suits are being introduced with specific compression panels, hydrophobic finishes, and body-streamlining technologies, marketed not just for elite competition but for recreational swimmers as well who appreciate added speed, confidence, and water efficiency.

Smart fabrics with UV-responsive capabilities are revolutionizing sun-protective swimwear. Following research proving dramatic improvements in Ultraviolet Protection Factor (UPF) using advanced dyestuffs and UV-absorbing compounds, brands now manufacture swimwear that responds dynamically to sunlight by altering color or alerting when UV intensity hits dangerous levels. This technology addresses increasing consumer demand for active skin health precautions as skin cancer awareness continues to grow. With photochromic dyes and sensor-fabric integration, such products enable wearers to see their sun exposure, assisting them in determining when it is time to reapply sunscreen or get into the shade. The technology not only enhances functionality but also provides an interactive and informative swimwear experience.

Adaptive and inclusive swimwear is a low-developed but high-potential niche segment. A study on adaptive sports identifies the requirement for bespoke designs to improve comfort, minimize drag, and maximize mobility for para-athletes. Cross-industry collaborations between large swimwear brands and sporting organizations such as collaborations with Aquatics GB are resulting in bespoke compression garments for top-level para-athletes. The greater exposure of adaptive sports through the likes of the Paralympic Games is driving demand for fashionable yet functional swimwear that satisfies both competition and leisure requirements, offering a clear opportunity for growth for those brands that will innovate within this area.

The seasonality inherent in swimwear makes it perfectly suited to rental and subscription-driven retail models. Sustainability-conscious consumers and holidaymakers looking for novelty without purchase increasingly welcome such services. Research into apparel rental shows short-term, occasion-specific rentals are growing, and swimwear perfectly aligns with months 4–9 of the retail season. Platforms such as Rent the Runway and Nuuly have already demonstrated the sustainability of edited rental bundles, and likewise, models specifically designed for swimwear can provide access to high-end designs for resort occasions, competitions, and holiday affairs, curbing overconsumption and textile loss.

LED technology holds the 78% market share, favored for its greater energy efficiency, long life, and brightness, and is the standard for front- and rear-lights. Advancements in smart LED systems such as automatic brightness control based on ambient light are creating a premium subsegment in the market. Laser lights, with a 15% market share, represent a fast-growing niche based on their ability to project safety zones and enhance the visibility of riders in difficult traffic scenarios. While incandescent lighting is virtually extinct due to its inefficiency and limited lifespan, it still sees limited use in low-cost, legacy designs. The shift to LEDs and lasers reflects customer demands for high-performance, low-maintenance products.

.png)

Battery lights are the leaders at 55%, driven by the popularity of USB-rechargeable, convenient and portable products among city cyclists. Dynamo systems are 30%, popular among tour and endurance riders who desire low-maintenance, self-recharging light solution. Solar lights although a niche category are advancing at the fastest rate, driven by trends toward sustainability and technological advancements enabling them to perform in inclement weather. Hybrid models that integrate solar and battery storage are also catching up as all-weather solutions that are easy and reliable for riders who desire environmentally friendly, low-maintenance light solutions.

DRLs for bikes are dominated by well-established cycling brands with a positive safety record, integrated designs, and product engineering creativity. Industry leaders among large companies included Garmin, Lezyne, NiteRider, CatEye, Knog, Exposure, Blackburn, Trek (Bontrager), Specialized, Cygolite, Magicshine, Light & Motion, Busch + Müller, Spanninga, Moon, Others.

Garmin Varia product line brings together DRL functionality with advanced radar technology, detecting oncoming vehicles behind and alerting riders. Together, this is a unique competitive edge, especially when integrated with Garmin Edge bike computers and smartwatches. The latest introduction of Varia VUE with a built-in dash cam and live radar further reinforces Garmin's dominance in multi-functional cycling safety devices.

As its own accessory brand, Bontrager enjoys vertical integration, and DRLs are thus bundled up with new Trek bikes in an integrated, streamlined package. Proprietary Blendr mounting systems are often included in products to provide clean, secure mounts. Daylight visibility is actively promoted in marketing and design, employing flash patterns and levels of brightness optimized for daylight safety.

Its wide variety of cycling accessories has made Topeak a known name, and it's expanding its DRL series with mounting systems like Duo Fixer, where cyclists have the facility to mount various accessories tool-free. Its 2025 vision includes lighting solutions that are specifically designed for e-bike compatibility and lifespan, which would address the fastest-growing urban cycling category.

The United States is at the forefront of smart DRL technology adoption, with manufacturers introducing features such as radar-based proximity alerts and AI-powered rearview cameras that stream live video to a rider’s smartphone. Advanced safety solutions now include brake-sensor integration to automatically increase brightness during deceleration, alongside high-lumen outputs that can be visible from over a mile away. The growing e-bike market has spurred the development of DRLs that connect directly to e-bike power systems, improving reliability and runtime exemplified by Garmin’s recent rearview radar/taillight designed for e-bikes.

Consumer demand is robust in both the competitive and recreational segments, with buyers seeking sleek, aerodynamic, and lightweight designs that complement modern bicycle aesthetics. The aftermarket remains a critical growth driver, with features such as USB-C fast charging, extended battery life, and customizable beam patterns influencing purchase decisions. The country’s extensive competitive cycling network from collegiate events to pro circuits sustains demand for performance-grade DRLs that merge safety with aerodynamics.

China continues to dominate global DRL production thanks to its integrated supply chain, large-scale manufacturing capacity, and export-oriented infrastructure. The domestic market is also expanding rapidly as urbanization and rising middle-class incomes increase the number of daily cycling commuters and e-bike users. Government initiatives promoting green transportation and cycling infrastructure are further boosting domestic demand for bicycle safety lighting.

Chinese brands excel at leveraging e-commerce marketplaces and livestream sales to reach diverse consumer bases, enabling quick product launches and rapid scaling. The combination of high-volume manufacturing, low production costs, and a growing local customer base makes China both a supply hub for global brands and a competitive domestic DRL market in its own right.

Germany enforces some of the strictest bicycle lighting regulations worldwide under StVZO standards, dictating beam patterns, light intensity, and the prohibition of certain flashing modes. This regulatory framework has elevated the engineering standards for DRLs, with German brands producing precision-built, durable, and road-compliant lighting systems.

German manufacturers are also pioneering automatic light-sensor technology that adapts beam output based on ambient conditions switching from DRL to low beam when entering tunnels, for example. With an established cycling commuter culture and a high penetration of e-bikes, the demand for integrated cockpit lighting systems continues to grow, reinforcing Germany’s position in the premium DRL segment.

The Netherlands’ world-class cycling infrastructure and high cycling population create an ideal environment for widespread DRL adoption. Strictly enforced lighting regulations ensure that demand remains steady for compliant, weather-resistant, and reliable lighting systems. Dutch brands are known for their co-design partnerships with bicycle manufacturers, resulting in factory-integrated DRLs that blend seamlessly into a bike’s frame and electrical system.

This collaborative approach turns lighting from a simple accessory into a core design element, aligning with the Dutch commitment to functional yet elegant cycling products. Given the country’s high year-round cycling rates, demand for durable, low-maintenance DRLs remains consistently strong.

Australia’s outdoor lifestyle and extended cycling season contribute to steady DRL market growth. Competitive cycling events, triathlons, and recreational riding all create a broad customer base for both high-performance and casual-use lighting systems. While UV protection is more relevant to apparel, the same consumer mindset toward durable, sun-resistant outdoor gear influences expectations for long-lasting, weatherproof DRLs.

Brands catering to the Australian market prioritize impact-resistant housings, waterproofing, and high-output beams suitable for both urban commuting and rural training environments. Competitive cycling’s popularity ensures a continuous demand for lightweight, aerodynamic DRLs that meet the performance needs of elite athletes.

In India, bicycle DRL adoption is still in its early growth stages but is benefiting from a surge in urban cycling for commuting due to congestion and fuel costs. While there are no national DRL regulations for bicycles, rising awareness from motor vehicle DRL mandates is influencing consumer safety behavior.

The market is highly shaped by e-commerce platforms and Direct-to-Consumer (D2C) brands, offering affordable, feature-rich lighting systems accessible to price-sensitive buyers. With cycling gaining traction in metro cities as a fitness and commuting option, demand for DRLs is expected to grow alongside increased public focus on road visibility and accident prevention.

|

Parameter |

Details |

|

Market Size (2025) |

$188.5 Million |

|

Market Size (2034) |

$419.7 Million |

|

Market Growth Rate |

9.3% |

|

Segments |

By Type (Front Lights, Rear Lights, Light Sets), By Technology (LED, Incandescent, Laser), By Power Source (Battery-Powered, Dynamo-Powered, Solar-Powered), By Application (Road Biking, Mountain Biking, Urban Commuting, Casual Riding), By Distribution Channel (Online Stores, Specialty Bike Shops, Department Stores, Mass Merchandisers) |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Garmin, Lezyne, NiteRider, CatEye, Knog, Exposure, Blackburn, Trek (Bontrager), Specialized, Cygolite, Magicshine, Light & Motion, Busch + Müller, Spanninga, Moon, Others. |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

* List Not Exhaustive

This report investigates the Bicycle Daytime Running Lights (DRL) Market, delivering strategic breakthroughs, analysis reviews, and highlights on how regulation, e-bike electrification, and smart-safety integration are reshaping product roadmaps and channel performance. Produced by USDAnalytics, the study decodes the shift from standalone lights to connected safety systems—radar, cameras, adaptive brightness, and app ecosystems—while benchmarking brand strategies across commuter, road, MTB, and casual segments. It quantifies mix changes by technology and power source, maps country-level demand drivers, and evaluates partnership patterns between bike/OEM platforms and accessory brands. This report is an essential resource for product leaders, investors, and policymakers seeking evidence-backed pathways to scale DRL adoption, de-risk supply, and capture premium margins through design and software differentiation. Scope includes-

USDAnalytics applies a triangulated approach that blends executive interviews (lighting engineers, e-bike OEMs, retailers, race organizers, regulators) with secondary intelligence (trade statistics, certification listings, patent filings, product teardowns, retail price trackers, and brand disclosures). Market size is modeled bottom-up from country-level unit volumes by bike segment and attachment rates, and reconciled top-down against import/export flows and channel sell-through. Forecasts use scenario analysis that captures regulatory expansion, e-bike parc growth, battery/LED efficiency curves, and component cost trajectories. Competitive benchmarking evaluates portfolios on lumen-per-watt, runtime, IP rating, mounting ecosystems, radar/camera integration, and software features; sensitivity tests validate results across multiple data sources.

Table of Contents: Bicycle Daytime Running Lights Market

1. Executive Summary

2. Bicycle Daytime Running Lights Market Overview (2025–2034)

3. Next-Generation Innovations and Emerging Opportunities

4. Market Share and Segmentation Insights

5. Competitive Landscape: Leading Brands

6. Country Analysis and Outlook of Bicycle Daytime Running Lights Market

7. Market Size Outlook by Region (2025–2034)

8. Company Profiles: Leading Players

9. Methodology

10. Appendix

Integrated rear units that combine taillight, radar, and camera are scaling fastest due to clear safety benefits and ecosystem lock-in with head units/phones. On the front, high-lumen, low-drag form factors with adaptive brightness win commuters and road cyclists. Bundled “light sets” increase basket size and simplify compliance for first-time buyers.

E-bikes favor hard-wired lights with stable voltage, theft-resistant mounts, and auto day/night modes—shifting value to OEM partnerships. Suppliers that certify compatibility with Bosch/Shimano and offer CAN-bus friendly controllers gain spec wins, while aftermarket SKUs evolve toward plug-and-play harness kits for retrofit fleets.

Radar fusion with vision (dash-cam) enables event recording and proximity alerts; laser lane projection creates visible safety buffers; and solar-assist trickle charging extends runtime for commuters. Firmware updatability, crash-event logging, and app analytics support recurring revenue via feature packs and insurance tie-ins.

Europe expands on regulatory enforcement and commuter incentives; China advances on urban cycling and e-commerce reach; the U.S. grows via performance/fitness culture and club networks. Netherlands and Germany lead factory-integrated lighting, while India and Latin America add volume through affordable, durable SKUs sold online.

Focus on certified beam patterns/visibility in daylight, IP/IPX water-ingress ratings, true runtime at constant lumen output, USB-C fast charging, and mount ecosystem compatibility across racks/seatposts/aero bars. For e-bike fleets, require vibration-tested housings, over-voltage protection, and field-swappable batteries to cut service downtime.