Biodegradable Lids Market Overview: Eco-Friendly Foodservice Solutions & Market Growth (2025–2034)

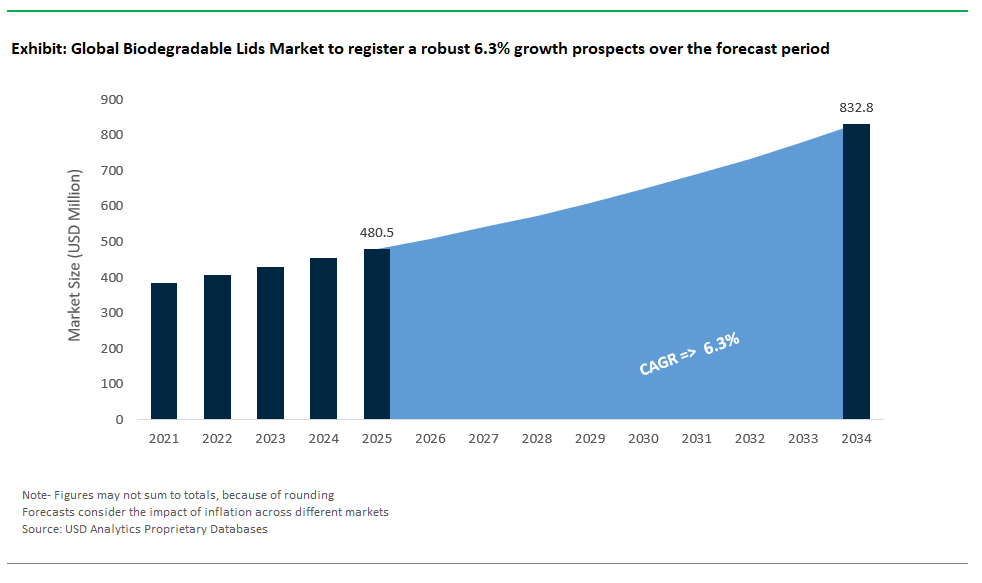

The Global Biodegradable Lids Market is on an upward growth trajectory between 2025 and 2034, as sustainability pressures and changing consumer preferences drive the replacement of traditional plastic lids with environmentally friendly alternatives across foodservice, retail, and household applications. Industry projections forecast the market to increase from USD 480.5 million in 2025 to USD 832.7 million by 2034, achieving a solid CAGR of 6.3%. This growth is driven by bans on single-use plastics, rising demand for compostable packaging solutions, and innovations in biodegradable materials delivering both functionality and sustainability.

USDAnalytics’ proprietary research underpins this latest edition, which presents a meticulous evaluation and future perspective on the global Biodegradable Lids Market, encompassing developments across 21 countries and insights into 20+ major firms- By Material Type (Paperboard, Polylactic Acid (PLA), Crystallized Polylactic Acid (CPLA), Bagasse (Sugarcane Fiber), Wheat Straw, Polyhydroxyalkanoates (PHA), Bio-PET, Wood, Others), By Application (Coffee Cups, Disposable Food Containers, Glass Jars, Plates, Bottles), By Design (Flat Lids, Domed Lids, Sipper Lids, Ventilated Lids, Customized Designs), By End-User (Food and Beverage Industry, Retail Sector, Hospitality Industry, Household Consumers, Institutional).

This report explores the innovations reshaping the biodegradable lids market, highlighting advances in materials like CPLA, bagasse, and wheat straw that provide heat resistance, strength, and aesthetic appeal for a wide range of foodservice and packaging applications. It examines how manufacturers are developing custom designs, including domed, sipper, and ventilated lids to meet diverse product and branding needs. The analysis details trends across end-user segments, from quick-service restaurants and hospitality venues to household consumers demanding sustainable everyday products. The study also covers evolving regulatory frameworks that are accelerating the transition toward compostable and bio-based solutions. Backed by actionable insights and verified market intelligence, this report is an essential resource for lid manufacturers, foodservice packaging suppliers, brand owners, retailers, investors, and policymakers navigating the sustainable packaging landscape through 2034.

Biodegradable Lids Market Booms Amid Home Composting Trends and EU Sustainability Mandates

Trend: Surge Toward Home-Compostable Materials Reshapes Biodegradable Lid Innovation

The global biodegradable lids industry is undergoing a significant shift as manufacturers focus on developing home-compostable solutions to address the limitations of industrial composting. While industrial composting facilities are expanding, small items like lids are often excluded due to contamination risks and processing challenges. This has fueled a surge in innovation, with a rise in patent filings specifically targeting home-compostable lid technologies. New material blends, featuring combinations of PHA, PLA, and starch, are being engineered to deliver strong mechanical performance suitable for foodservice while ensuring biodegradability under composting conditions. Importantly, some of these advanced materials are formulated to break down effectively in home composting environments, aligning with the practical realities of residential waste management.

Consumer behavior is a key driver behind this transition. Although industrial composting infrastructure continues to grow, issues with collecting and separating small-format items like lids remain significant. Increasing consumer engagement in home composting, particularly in regions like the EU and UK, is accelerating demand for products designed for residential compost systems. This trend highlights the need for biodegradable lids that can integrate seamlessly into home composting practices. As consumers become more eco-conscious, home-compostable lids are emerging as a vital differentiator in the future of sustainable food packaging.

Opportunity: Regulatory Mandates Drive Explosive Growth Potential in Foodservice Lids Market

A significant growth opportunity in the biodegradable lids market lies within the foodservice sector, where major regulatory changes are transforming material demand. The European Union’s Packaging and Packaging Waste Regulation (PPWR) will require all packaging to be recyclable or reusable by 2030, setting the stage for a massive shift away from single-use plastic lids. As of 2023, biodegradable options represent only a small fraction of the global foodservice disposables market, leaving a vast untapped opportunity. With billions of single-use items consumed annually, the push for sustainable alternatives in lid manufacturing signals a substantial addressable market poised for rapid expansion.

Cost competitiveness for biodegradable lid materials is improving steadily. Advances in production technology and economies of scale are helping close the price gap with traditional plastics like PET, making biodegradable lids increasingly practical for high-volume use. Material innovations are also addressing performance challenges, for example, cellulose-fiber-reinforced PLA formulations are enhancing heat resistance, making biodegradable lids viable for hot beverages and broader applications. Simultaneously, recyclability remains a critical focus, with industry leaders like Huhtamaki and Stora Enso investing in R&D to ensure that biodegradable and fiber-based lids integrate seamlessly into existing paper recycling systems, reducing contamination risks and supporting a circular economy. As regulatory pressure grows and sustainability becomes a crucial competitive edge, biodegradable lids are positioned for significant adoption, reshaping the global foodservice packaging landscape.

Biodegradable Lids Market Share Insights: Material, Application, and End-User Trends Shape Sustainable Packaging

By Material Type: Paperboard Leads the Market, CPLA and PHA Deliver Fastest Growth

In 2025, paperboard leads the biodegradable lids market with a 27.8% share, valued for its cost-effectiveness and compatibility with both hot and cold beverages, making it the preferred choice for global coffee chains and foodservice providers. Crystallized PLA (CPLA) is the fastest-growing material (CAGR 15%), as its heat resistance makes it ideal for hot beverage lids in coffee shops and QSRs. PHA (polyhydroxyalkanoates) is also expanding rapidly due to marine biodegradability, gaining traction with eco-conscious brands and regulators. Bagasse and wheat straw materials are increasingly adopted for compostable food container lids, targeting both foodservice and retail.

By Application: Coffee Cups Dominate, Food Container Lids See Rapid Growth

Coffee cups remain the dominant application of the biodegradable lids market in 2025. This leadership is driven by international coffeehouse chains and local cafés transitioning from conventional plastic to compostable or recyclable alternatives. Disposable food container lids are the next largest and rapidly growing application with a CAGR of 7.2%, fueled by takeout packaging regulations and rising demand for sustainable food delivery solutions. Lids for bottles, glass jars, and plates are also emerging segments supported by innovations in PHA and bagasse for juices, smoothies, and ready-to-eat meals.

By End-User: Food & Beverage Industry Leads Demand, Hospitality Sector Expands Fastest

The food & beverage industry is the primary end-user, capturing 52.1% of total demand in 2025. Quick service restaurants (QSRs) and coffee chains such as Starbucks drive the adoption of PLA, CPLA, and paperboard lids to meet sustainability goals and regulatory requirements. The hospitality sector is the fastest-growing, as hotels and catering services phase out single-use plastics and shift toward compostable and biodegradable packaging. The retail sector is also important, with supermarkets and convenience stores embracing pre-packaged foods sealed with eco-friendly lids.

.png)

Biodegradable Lids Market Analysis: Regulatory Shifts and Advanced Materials

The global market for biodegradable lids is growing fast. Regulations, major brands' sustainability goals, and new materials are transforming how lids are made. This market, once dominated by traditional plastics, is now a key focus for eliminating single-use plastics, especially visible items like coffee cup lids. Biodegradable lids are shifting from niche products to widespread, essential solutions.

Product Innovation Delivers Functional and Environmental Advantages

New lids show big steps in being both sustainable and functional. Companies like Huhtamaki are developing innovative, sustainable lid solutions for various uses. Dart Container offers molded fiber lids that meet commercial composting standards. Tetra Pak is using sugarcane-based polymers in its lids to significantly cut its carbon footprint while fitting existing recycling. These innovations balance environmental benefits with performance.

Capacity Expansions Signal Industrial Scale Readiness

Investments in production capacity show confidence in the large-scale manufacturing of bio-based lids. Major manufacturers like Berry Global are investing in advanced materials for lids to meet demand from coffee chains. Stora Enso is expanding molded fiber lid production due to a growing preference for fiber alternatives in quick-service restaurants. This indicates regional supply chains are emerging to localize biodegradable lid production.

Strategic Partnerships Accelerate Adoption and Innovation

Collaborations between major brands and material innovators are speeding up market adoption. Starbucks is piloting compostable molded fiber lids in select markets with Huhtamaki to scale biodegradable solutions globally. McDonald's is also using fiber-based lids in various markets, showing how big brands are localizing sustainable options. Other companies are exploring innovative bio-based coatings for packaging components to reduce waste.

Regulatory Frameworks Propel Market Transformation

Global policies are making biodegradable lids a necessity. The EU Packaging and Packaging Waste Regulation (PPWR) aims for all packaging to be recyclable or reusable, phasing out many non-biodegradable plastics, including lids. California’s AB 1276 is pushing to reduce single-use foodware accessories, encouraging sustainable alternatives. Regulators in countries like India are also promoting innovative and sustainable packaging solutions.

Technological Breakthroughs Elevate Performance and Sustainability

Advanced material research is improving what biodegradable lids can do. Research into bio-based laminates is improving heat resistance and composting speed for biodegradable lids. Leading institutions are also exploring enzyme-triggered degradation mechanisms within polymer structures to ensure plastics break down more effectively. These breakthroughs are crucial for making biodegradable lids perform as well as traditional plastics.

Commercial Adoption Demonstrates Market Readiness

Major brands are now widely using biodegradable lids, showing market maturity and consumer acceptance. Leading coffee chains are integrating biodegradable alternatives, proving these solutions can handle high-volume demands. Large events and sports venues are also adopting sustainable lids. The aviation industry is also exploring advanced biodegradable and edible packaging to reduce waste.

Competitive Landscape of the Global Biodegradable Lids Market

The global biodegradable lids market is surging in 2024, fueled by stringent single-use plastic bans, rising sustainability commitments from major foodservice brands, and growing consumer demand for eco-friendly alternatives. Innovations in PLA, PHA, molded fiber, bagasse, bamboo, and even edible materials are transforming the lid segment across hot and cold beverage applications, soup containers, frozen foods, and single-serve pods. Leading manufacturers are scaling capacity, forging high-profile partnerships, and developing unique material blends to capture market share. The competitive landscape reflects a rapidly evolving industry where sustainability and performance go hand-in-hand.

Huhtamaki: Leading with Innovative Fiber Lids

Huhtamaki (Finland) Huhtamaki to lead the biodegradable lids market with its innovative Future Smart fiber lids, reinforcing its position as a major industry player. These lids are crafted from renewable plant-based fibers, either a blend of natural bagasse and wood fiber or pure wood fiber, and contain no plastic coatings, making them recyclable. They are designed for a secure fit on paper cups and are suitable for both hot and cold beverages. In August 2024, Starbucks announced a partnership with Huhtamaki to pilot fiber-based, compostable cups and lids for cold beverages at selected locations in California and Minnesota. Huhtamaki remains deeply committed to fiber-based and compostable packaging solutions, with its Bioware Love Nature cups and matching lids certified compostable to EN13432 standards in industrial composting facilities.

Dart Container: Expanding Influence in Sustainable Foodservice Packaging

Dart Container (US) Dart Container is expanding its influence in sustainable foodservice packaging through its Solo® brand. Dart offers compostable* fiber bowls and cups, which can be paired with compatible plastic lids. Their Dart® Compostable Fiber Containers* are PFAS-Free fiber blend products that are BPI-certified to be commercially compostable. Keurig Dr Pepper is committed to making 100% of its packaging recyclable or compostable by 2025. Dart Container offers various lids, including polypropylene plastic lids for food containers, but their compostable offerings primarily focus on the containers themselves, with compatible lids often made from conventional plastics or other certified compostable materials.

Vegware: Renowned for Compostable Packaging Innovation

Vegware (UK) Vegware is renowned for its innovative approach to compostable packaging. Vegware offers a range of compostable lids, including clear PLA lids for cold food containers and hot cups, made from plants and designed for industrial composting. Their Nourish Molded Fiber range includes plates, platters, and bowls that are sturdier than foam or paper and suitable for hot or cold foods. Vegware's overall product catalog and brand positioning emphasize certified plant-based and compostable solutions across its lines, reinforcing its status as a sustainability pioneer in the European foodservice sector.

Footprint: Driving Advancements in Fiber-Based Solutions

Footprint (US) Footprint is driving significant advancements in fiber-based solutions, bringing new sustainability options to food packaging. Footprint offers plant-based fiber hot and cold cup lids that are plastic-free, contain no plastic liners or coatings, and have no PFAS added. These lids are designed to be paired with their plant-based fiber drink cups, which can handle hot, cold, carbonated, sugary, creamy, and even alcoholic beverages. Footprint has partnered with Conagra Brands, and Footprint's plant-based fiber frozen food packaging (including lids) has helped Conagra decrease its carbon footprint by over 34,000 metric tons and reduce plastic in its food chain. Footprint's commitment to plastic-free, plant-based fiber solutions is evident across its product range.

Biotrem: Unique Edible Wheat Bran Technology

Biotrem (Poland) Biotrem brings a unique angle to the biodegradable lids market with its edible wheat bran technology. Biotrem produces plates and bowls from wheat bran that are fully biodegradable (decompose within 30 days) and can also be consumed. These products are suitable for hot and cold meals and can be used in ovens or microwaves. Biotrem's production line has a capacity of approximately 15 million pieces of biodegradable disposable plates or bowls a year. Biotrem is recognized for its innovative and truly edible tableware solutions, offering a highly differentiated and sustainable product line.

Yash Pakka: Emerging Powerhouse in Bagasse-Based Solutions

Yash Pakka (India) Yash Pakka is emerging as a powerhouse in bagasse-based packaging solutions through its CHUK brand. CHUK manufactures compostable and biodegradable tableware and lids using bagasse (sugarcane waste) as a raw material. All CHUK products are biodegradable and compost within 180 days. Yash Pakka's current paper production capacity is 39,100 tonnes per annum, with a pulp mill capacity of 42,900 tonnes per annum. Yash Pakka emphasizes its commitment to global expansion and providing sustainable packaging solutions derived from agricultural waste.

United States Leads Innovation and Regulation in Biodegradable Lids

The United States is solidifying its position as a significant hub for both regulatory advancement and innovation in biodegradable lids. Leading manufacturers like Eco-Products continue to specialize in PLA lids for cold beverages, while World Centric offers bagasse-based compostable lids, providing performance-driven and sustainable alternatives. Starbucks continues to prioritize sustainable packaging and reduce single-use plastics, with ongoing research and trials for various cup and lid solutions. Policy is a critical driver: California’s SB 54, enacted in 2022, is a landmark law that aims to reduce plastic pollution and mandates that by 2032, all single-use packaging and plastic food service ware must be recyclable or compostable. While the law does not specifically mandate 100% compostable lids for all quick-service restaurants (QSRs) by 2025, it strongly incentivizes the shift towards such materials. For instance, expanded polystyrene (EPS) food service ware is effectively prohibited in California from January 1, 2025, due to failure to meet recycling targets under SB 54, pushing businesses towards alternatives like compostable lids. Significant investment continues to be channeled into biopolymer R&D for lid solutions, positioning the U.S. to lead both technological development and widespread adoption of biodegradable lid solutions.

Germany Advances High-Performance Biodegradable Lid Materials

Germany continues to set global benchmarks in developing high-performance biodegradable lid materials, combining innovative materials science with stringent environmental policy. BASF has engineered materials suitable for high-performance applications. Ecovio® PS 1606, a fully compostable biopolymer composed of Ecoflex® and PLA, is highlighted for its heat resistance, high melt strength, and barrier properties against fat and liquids, making it suitable for hot and cold drink cups and potentially lids, without compromising compostability. Meanwhile, Südzucker continues its focus on sustainable products, indicating its work with starch-based materials. The country’s regulatory environment is highly influential: McDonald’s in the EU has been progressing with sustainable packaging initiatives, including the use of fiber-based cups and lids where local regulations allow. The European Union’s Packaging and Packaging Waste Regulation (PPWR), provisionally agreed upon in March 2024, includes ambitious targets for reducing packaging waste and promoting reusable and recyclable packaging. Germany’s dual focus on advanced biopolymer innovation and rigorous regulatory compliance positions it as a key driver of sustainable lid adoption across Europe.

China Emerges as the Mass Production Hub for Biodegradable Lids

China has firmly established itself as a mass production center for biodegradable lids, reflecting the country’s dominant role in global bioplastics manufacturing. The nation's production capacity for PLA and PBAT lid products is substantial. Key producers include Kingfa Science, which continues to be a major player in modified plastics and biodegradable products, including PBAT-based materials that can be used for flexible lids. Zhejiang Hisun is known for high-volume PLA production, including injection-molded grades suitable for lids. The market is experiencing rapid changes, with prominent foodservice brands actively adopting sustainable packaging. Luckin Coffee continues to expand aggressively in China with a focus on market share, and the broader trend in China's foodservice sector strongly favors biodegradable options due to policy drivers. China's national policies are catalysts, with ongoing efforts to curb plastic pollution and promote biodegradable alternatives in the foodservice sector. As demand surges domestically and abroad, China’s manufacturing scale and cost advantages will play a crucial role in making biodegradable lids accessible to global markets.

Netherlands Innovates in Circular Biodegradable Lid Design

The Netherlands is emerging as a leader in sustainable and circular-design biodegradable lid solutions, driven by advanced materials and commercial partnerships. Avantium has developed PEF (polyethylene furanoate), a plant-based polymer with excellent barrier properties and heat resistance, making it ideal for various packaging applications, including potentially hot drink lids. Avantium is actively progressing towards the commercial production and sale of PEF in 2025. DSM (now DSM-Firmenich for some divisions, with others like engineering plastics spun off or sold) continues to focus on sustainable solutions. Commercialization efforts are underway, with Heineken actively exploring sustainable packaging solutions as part of its sustainability strategy outlined in its 2024 annual report (published February 2025). Heineken's commitment to reducing plastic and exploring innovative packaging aligns with such initiatives. As the European Union intensifies efforts to phase out single-use plastics, Dutch innovations are helping redefine what sustainable lid solutions look like in the beverage and food industries, with a strong emphasis on circularity and recyclability targets set by the EU PPWR.

Thailand Expands Role as ASEAN’s Biodegradable Lid Production Hub

Thailand has solidified its role as Southeast Asia’s primary production hub for biodegradable lids, supported by abundant local resources and strategic industry investments. Manufacturers are capitalizing on native agricultural materials such as cassava starch and rice husks to produce compostable lids for both domestic use and export markets, including the European Union and Australia. PTT MCC Biochem continues to be a key player in the bioplastics industry in Thailand, with joint ventures focusing on PLA production capacity, and their materials are suitable for various applications, including lids for the booming bubble tea industry, meeting demands for clarity and heat resistance. The sector’s capacity continues to grow, with SCG Packaging (SCGP) focused on sustainable packaging solutions. SCGP's business highlights for 2024 (published Feb 2025) indicate expanded production capacity of corrugated cartons and strategic acquisitions to strengthen healthcare packaging, aligning with their broader commitment to innovative and sustainable offerings. Thailand’s bioplastics industry combines local innovation with export-driven strategies, positioning it as a significant global supplier of sustainable lid solutions.

Biodegradable Lids Market Report Scope

Biodegradable Lids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$480.5 Million

|

|

Market Size (2034)

|

$832.7 Million

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Material Type (Paperboard, Polylactic Acid (PLA), Crystallized Polylactic Acid (CPLA), Bagasse (Sugarcane Fiber), Wheat Straw, Polyhydroxyalkanoates (PHA), Bio-PET, Wood, Others), By Application (Coffee Cups, Disposable Food Containers, Glass Jars, Plates, Bottles), By Design (Flat Lids, Domed Lids, Sipper Lids, Ventilated Lids, Customized Designs), By End-User (Food and Beverage Industry, Retail Sector, Hospitality Industry, Household Consumers, Institutional)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj (Finland), Pactiv Evergreen (U.S.), Vegware (UK), Eco-Products, Inc. (U.S.), Biotrem (Poland), BioPak (Australia), Novolex (U.S.), Ancheng (China), Ecoware (India), Chuk (India), MVI ECOPACK (China), GreenGood USA (U.S.), Get Bio Pak Co., Ltd. (China), Biopuric Private Limited (India), Nascentkraft (India), Genpak LLC (U.S.), NatureWorks LLC (U.S.), Danimer Scientific (U.S.), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Lids Market Segmentation

By Material Type

- Paperboard

- Polylactic Acid (PLA)

- Crystallized Polylactic Acid (CPLA)

- Bagasse (Sugarcane Fiber)

- Wheat Straw

- Polyhydroxyalkanoates (PHA)

- Bio-PET

- Wood

- Others

By Application

- Coffee Cups

- Disposable Food Containers

- Glass Jars

- Plates

- Bottles

By Design

- Flat Lids

- Domed Lids

- Sipper Lids

- Ventilated Lids

- Customized Designs

By End-User

- Food and Beverage Industry

- Retail Sector

- Hospitality Industry

- Household Consumers

- Institutional

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Lids Market

- Huhtamaki Oyj (Finland)

- Pactiv Evergreen (US)

- Vegware (UK)

- Eco-Products, Inc. (US)

- Biotrem (Poland)

- BioPak (Australia)

- Novolex (US)

- Ancheng (China)

- Ecoware (India)

- Chuk (India)

- MVI ECOPACK (China)

- GreenGood USA (US)

- Get Bio Pak Co., Ltd. (China)

- Biopuric Private Limited (India)

- Nascentkraft (India)

- Genpak LLC (US)

- NatureWorks LLC (US)

- Danimer Scientific (US)

* List Not Exhaustive

Methodology

This report on the Global Biodegradable Lids Market utilizes a comprehensive research methodology integrating both primary and secondary research. Primary research includes in-depth interviews and structured discussions with industry stakeholders, including lid manufacturers, biopolymer developers, sustainability managers at foodservice brands, regulatory authorities, and technology innovators. These qualitative insights are corroborated through secondary research from corporate disclosures, regulatory publications (e.g., EU PPWR, California SB 54), scientific studies on biopolymer performance, and industry-specific databases. Market sizing and forecasting for the period 2025–2034 are derived using robust data triangulation techniques, ensuring accuracy across all market segments, regions, and applications. This ensures that all market dynamics, emerging trends, and technological developments are validated and quantified with high precision.

Research Coverage

- Geographic Scope: Encompassing over 25 countries across North America, Europe, Asia Pacific, South America, the Middle East & Africa.

- Segmentation: Comprehensive coverage across multiple dimensions:

- Material Type: Paperboard, Polylactic Acid (PLA), Crystallized PLA (CPLA), Bagasse (Sugarcane Fiber), Wheat Straw, Polyhydroxyalkanoates (PHA), Bio-PET, Wood, Others.

- Application: Coffee Cups, Disposable Food Containers, Glass Jars, Plates, Bottles.

- Design: Flat Lids, Domed Lids, Sipper Lids, Ventilated Lids, Customized Designs.

- End-User: Food and Beverage Industry, Retail Sector, Hospitality Industry, Household Consumers, Institutional.

- Competitive Landscape: Detailed profiles and strategic insights on over 20 leading market participants, spanning major multinationals to emerging niche innovators.

- Key Themes Explored:

- Advances in biodegradable materials (e.g., CPLA, PHA, bagasse, wheat straw).

- Regulatory frameworks are reshaping sustainable packaging adoption worldwide.

- Emerging lid designs are enhancing functional performance and brand differentiation.

- Technological innovations such as home-compostable materials and bio-based coatings.

- Regional production capacities and supply chain shifts in biodegradable lid manufacturing.

- Historical data from 2021 to 2024, and forecasts through 2034.

Deliverables

- Comprehensive Market Research Report (PDF and Excel), including detailed charts, tables, and visual analyses.

- Country-specific insights and market forecasts.

- Segment-wise revenue and volume projections for 2025–2034.

- Competitive benchmarking, SWOT analyses, and strategic profiles of key industry players.

- Analysis of new product innovations and material technology tracking.

- Executive summary highlighting strategic trends and analyst perspectives.

- Post-delivery analyst support to address custom data queries or clarifications.