Bioplastics for Agribusiness Market Overview: Sustainable Solutions & Growth Insights

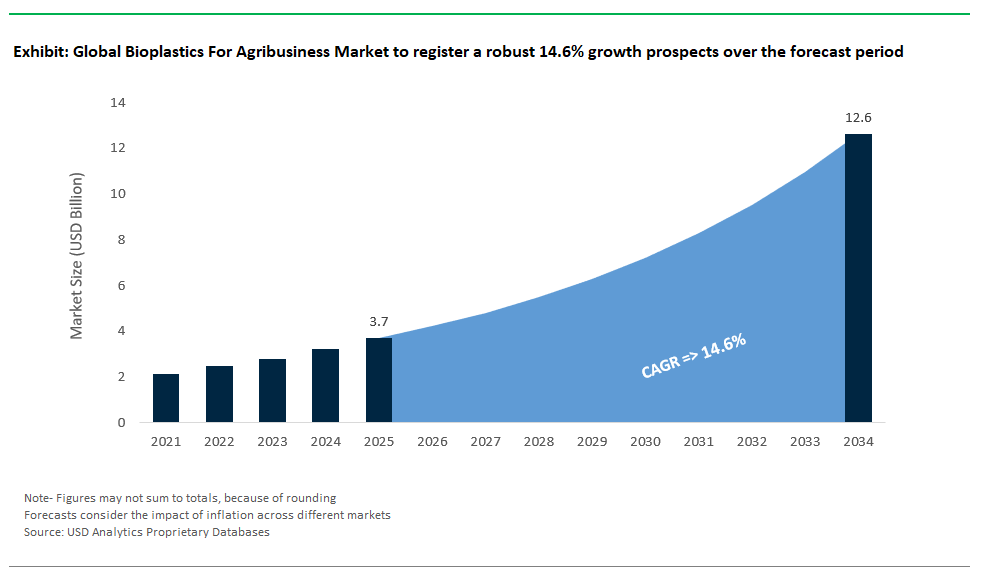

The Global Bioplastics for Agribusiness Market is entering a high-growth phase from 2025 through 2034, fueled by the agricultural sector’s transition toward sustainable materials that improve productivity and environmental stewardship. Industry projections show the market expanding from USD 3.7 billion in 2025 to USD 12.6 billion by 2034, achieving an impressive CAGR of 14.6%. This surge is driven by regulatory restrictions on traditional plastics, growing demand for biodegradable agricultural solutions, and technological advances that enhance bioplastic performance in diverse agricultural applications.

Through proprietary intelligence from USDAnalytics, the newest edition provides an authoritative analysis and forecast of the global Bioplastics for Agribusiness Market, mapping growth in 21 countries and profiling more than 20 leading industry names- By Biodegradable Bioplastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch-based Plastics, Polybutylene Succinate (PBS), Cellulose-based Plastics, Polycaprolactone (PCL)), By Non-Biodegradable Bioplastics (Bio-Polyethylene (Bio-PE), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA)), By Application (Mulch Films, Nursery Products, Porous and Drainage Pipes, Greenhouse Films & Sheeting, Crop Protection & Storage, Fertilizer & Pesticide Encapsulation, Soil Enhancers, Packaging for Agricultural Products, Others), By Feedstock (Sugarcane, Corn Starch, Cassava, Potato Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams), By Crop (Fruits & Vegetables, Grains & Oilseeds, Flowers & Ornamentals, Others).

Exploring the forces transforming modern agriculture, this report investigates how bioplastics are increasingly integrated into vital applications such as mulch films, greenhouse sheeting, and controlled-release fertilizer and pesticide formulations. It highlights innovations in feedstock utilization from cassava and potato starch to lignin and algae that are diversifying supply chains and reducing environmental footprints. The analysis also examines competitive strategies among polymer producers, emerging collaborations between bioplastic innovators and agricultural technology companies, and regulatory policies shaping sustainable agriculture practices worldwide. Supported by practical insights and verified market intelligence, this report is an invaluable resource for polymer manufacturers, agribusiness leaders, investors, and policymakers seeking to leverage bioplastics as a cornerstone of sustainable and profitable agricultural growth through 2034.

Bioplastics for Agribusiness Market Analysis: Environmental Benefits

The global bioplastics market for agribusiness is undergoing a profound transformation as sustainability, regulatory mandates, and technological innovation converge to reshape agricultural inputs and practices. Traditionally reliant on conventional plastics for critical farming operations, from mulch films and irrigation components to seed coatings and fertilizer encapsulation, agribusiness is increasingly adopting bioplastics as essential tools for achieving sustainability goals while enhancing crop productivity. Recent developments reveal a market rapidly moving from niche pilot projects to large-scale commercial deployment, driven by clear environmental benefits and tangible agronomic advantages.

Innovative Product Launches Drive Agronomic and Environmental Performance

Bioplastics innovation is rapidly expanding its role in agriculture. BASF’s ecovio® M2351 is a soil-biodegradable mulch film certified to European standards that breaks down naturally after harvest, offering sustainable benefits for high-value crops like strawberries and tomatoes. Novamont’s MATER-BI® range, made from starches and vegetable oils, goes beyond simple barriers by enhancing seed germination and early growth, potentially adding multifunctional benefits. The agribusiness sector is also moving toward sustainable slow-release agrochemicals using biopolymers to control nutrient delivery while reducing plastic residue in soils, a critical environmental concern driving research into biodegradable coatings for fertilizers.

Capacity Expansions Reflect Growing Market Confidence

Leading manufacturers are expanding production capacity in response to rising demand for sustainable agricultural films. Companies like RKW Group are investing in innovative biodegradable agricultural films, supported by strong environmental policies, particularly in Europe. Berry Global is scaling up production of biodegradable silage wraps to reduce plastic waste in animal feed preservation. Regional strategies are also emerging, with producers like Plastika Kritis developing climate- and crop-specific films, such as those tailored for Mediterranean crops like olives and vineyards, ensuring optimal agronomic performance and environmental compatibility.

Strategic Partnerships Focus on Integrating Bioplastics into Agricultural Systems

Collaboration is key to integrating bioplastics into farming. Partnerships like Bayer CropScience and Novamont’s work on MATER-BI® twine and clips address logistical and mechanical challenges for farmers adopting biodegradable films, ensuring they work smoothly with existing machinery. Research into herbicide-embedded films for soybeans and collaborations on biodegradable drip irrigation tapes demonstrate how bioplastics are enhancing sustainability by reducing plastic waste and improving soil health. Irrigation technology firms and bioplastics manufacturers are joining forces to develop solutions that biodegrade safely after use, supporting sustainable water management.

Regulatory and Policy Frameworks Accelerate Market Adoption

Global regulations are shifting bioplastics from voluntary choices to compliance necessities. The EU’s Common Agricultural Policy (CAP) 2023–2027 strongly promotes environmental sustainability, incentivizing growers to adopt biodegradable mulch films. North American regulations are also moving toward banning non-biodegradable plastic mulches, especially in organic farming, creating urgency for suppliers and farmers to transition. Emerging markets like India are recognizing bioplastics’ role in sustainable intensification and environmental stewardship, with government initiatives supporting adoption in smallholder farms through incentives and education programs.

Technological Breakthroughs Enhance Agronomic Value and Sustainability

Advances in material science are transforming bioplastics from passive coverings to active contributors to crop health. Research at Fraunhofer UMSICHT shows biodegradable mulch films can improve soil conditions and nutrient availability, boosting yields and resource efficiency. New “smart bioplastics” are being developed with integrated pest-repellent properties using natural extracts like neem, reducing pesticide reliance and chemical residues. Innovations in biodegradable seed coatings, including hydrogel formulations derived from agricultural byproducts, enhance seed germination and early growth under stress conditions like drought, supporting climate-resilient farming and global food security.

Commercial Adoption Validates Market Viability and Economic Impact

Large agricultural brands are driving commercial adoption of bioplastics, signaling strong market viability. Driscoll’s is piloting biodegradable materials amid consumer and retailer demand for sustainable fruit production. Biodegradable mulch films like BASF’s ecovio® M2351 demonstrate agronomic benefits such as water savings and yield increases, vital in water-limited regions. The use of biodegradable silage wraps by major food and agriculture companies showcases sustainability efforts extending from farms through supply chains, highlighting the commitment to reducing plastic waste and advancing sustainable intensification across agriculture.

Market Dynamics: Trends & Opportunities in the Global Bioplastics for Agribusiness Industry

Trend: Regulatory Phase-Out of Conventional Agri-Plastics Accelerates Bioplastics Adoption

Regulatory pressure is mounting globally, especially in the European Union, where policies like Delegated Regulation (EU) 2024/2770 set firm biodegradability targets for agricultural polymers. This is speeding up the shift from conventional agri-plastics to biodegradable alternatives. Other important regions, such as Canada, Japan, and Brazil, are also enhancing their regulatory frameworks to curb plastic waste in agriculture, although broad bans with direct fines on non-biodegradable mulch and silage films are not yet widespread across these markets for 2025–2027. Still, the overall global regulatory environment is unmistakably driving the adoption of more sustainable agricultural practices.

At the same time, the cost competitiveness of bioplastics is steadily improving. Biodegradable mulch films and silage wraps are becoming increasingly viable alternatives to traditional plastics, with some mulch films now priced on par with or even below conventional LDPE films in select markets. Bio-based silage wraps are also nearing the cost levels of LLDPE. PBAT mulch films show nearly 90% biodegradation within six months under real soil conditions, meeting standards like ISO 17556 and certifications such as TÜV Austria OK SOIL. Driven by tightening environmental regulations and growing awareness, markets in North America and Europe are witnessing strong demand growth, with especially high adoption rates among organic farmers committed to sustainable field practices.

Opportunity: Bio-Based Seed Coatings and Pesticide Encapsulation Unlock Next-Gen Agronomic Performance

A major growth area in the bioplastics agribusiness market is bio-based seed coatings and advanced pesticide encapsulation technologies. By replacing synthetic polymer coatings with biodegradable bioplastics, agribusinesses are achieving measurable improvements. Innovative seed coatings using materials like chitosan show promise in enhancing seed vigor and germination, even under challenging conditions such as drought. These advanced coatings offer significant potential to improve early crop growth and resilience.

The environmental benefits are equally important. New bioplastic encapsulation methods enable controlled-release of agrochemicals, reducing pesticide use and limiting chemical runoff. These technologies support regenerative farming by delivering agrochemicals more precisely and lowering environmental harm. Innovation in this space is accelerating, evidenced by a rise in patent filings focused on advanced features like enzyme-triggered degradation. This research aims to optimize bioplastic coating performance and ensure they break down safely in the environment.

Competitive Landscape of the Global Bioplastics for Agribusiness Market

The global bioplastics market for agribusiness is rapidly expanding in 2024, fueled by growing regulatory restrictions on traditional plastics, sustainability commitments across the agricultural value chain, and rising consumer awareness of environmental impacts. Bioplastics, ranging from PLA and PBAT blends to bio-based polyethylene and biodegradable starch polymers, are finding increasing adoption in mulch films, seed coatings, greenhouse covers, and other farming applications. Key market players are scaling production, investing in regional facilities, and forming strategic partnerships with agricultural equipment manufacturers and agribusiness giants to meet evolving demands. The competitive landscape reflects a fast-moving sector poised to revolutionize sustainable farming practices worldwide.

BASF SE: Global Leader in Biodegradable Mulch Films

BASF SE (Germany) BASF SE remains a global leader in the agricultural bioplastics market with its ecovio® brand, offering biodegradable mulch films that help reduce soil contamination and eliminate plastic waste in farming operations. ecovio® M2351 is a certified soil-biodegradable biopolymer for use in agriculture, certified according to the European standard EN 17033. Films made of ecovio® M 2351 can be manufactured with layer thicknesses of 8 to 25 µm and can be laid out with the same machines used for conventional mulch films. In June 2024, BASF SE introduced a biomass-balanced ecoflex PBAT variant called ecoflex F Blend C1200 BMB, which uses renewable feedstock derived from residual and waste biomass. BASF’s global reach and regulatory certifications position it as a trusted supplier for sustainable agribusiness solutions worldwide.

Novamont: Driving Innovation in Starch-Based Bioplastics for Agriculture

Novamont (Italy) Novamont continues to drive innovation in starch-based bioplastics for agriculture, strengthening its market presence through strategic collaborations and production expansions. Novamont produces Mater-Bi® resins used to manufacture agricultural mulch film, which can be plowed back into the soil where it will biodegrade at the end of the growing season. Novamont's new Mater-Bi plant at Patrica has increased its bioplastics production capacity to 200 ktons (as per its 2021 Sustainability Report), enabling it to meet growing market demand. Novamont's commitment to using renewable resources is evident, with around 58% of its raw materials being renewable. The company continues to offer compelling advantages for farmers seeking sustainable, residue-free alternatives.

Futerro: Expanding PLA-Based Films for Farming

Futerro is rapidly expanding its footprint in the global agribusiness bioplastics sector. The company has developed PLA-based biodegradable films for various farming applications, providing sustainable alternatives to traditional plastic films. PLA is increasingly used in agricultural applications, such as biodegradable mulch films, plant pots, and seed coatings. Research indicates that over 30% of biodegradable mulch films are now PLA-based, reducing soil pollution and plastic waste accumulation in farmlands. Futerro will become the world's second-largest producer of LA and PLA, with a new plant located in Normandy, France, as an estimated total investment of €500 million, set to be Europe's first fully integrated, circular, and sustainable biorefinery, with an annual production capacity of 125,000 tons of LA and 75,000 tons of PLA.

Braskem: Leading Producer of Bio-Based Polyethylene for Agricultural Films

Braskem (Brazil) Braskem, the largest bioplastics producer in Latin America, continues to expand its “I’m green™” bio-based polyethylene portfolio for agricultural films. In October 2023, Braskem and FKuR Kunststoff GmbH expanded their distribution agreement to include further products from the I'm green™ bio-based portfolio, including I'm green™ bio-based EVA, for distribution in the EU, Switzerland, Norway, the UK, Turkey, Israel, and India. Braskem launched its Renewable Innovation Center in Lexington, MA, USA, in 2024, dedicated to accelerating early-stage innovations in renewable chemicals and sustainable materials. Braskem's bio-based PE offers farmers a drop-in solution that reduces greenhouse gas emissions while maintaining performance, making Braskem a key supplier in the transition to sustainable agricultural plastics.

Mitsubishi Chemical Corporation: Advancing with Innovative BioPBS™ Materials

Mitsubishi Chemical Corporation (Japan) Mitsubishi Chemical Corporation is advancing its presence in the agricultural bioplastics market with innovative materials like BioPBS™, a biodegradable polymer engineered for mulch films and other farming applications. BioPBS™ (polybutylene succinate) is a biodegradable plastic that decomposes into water and carbon dioxide with microorganisms under the soil and offers high heat resistance. Mitsubishi Chemical Corporation (MCC) established PTT MCC Biochem Company Limited, a 50-50 joint venture with PTT Global Chemical Public Company Limited (PTTGC), which has been producing and selling bio-based PBS (BioPBS™) since 2017. This growth trajectory indicates strong positioning for companies like Mitsubishi Chemical in the evolving regional needs for sustainable agriculture.

NatureWorks: Leveraging PLA Expertise for Agricultural Applications

NatureWorks (US) NatureWorks, a subsidiary of CJ CheilJedang, is leveraging its PLA expertise to expand into agricultural applications. Its Ingeo™ PLA materials are used in agricultural products such as mulch film, landscape fabric, plastic pots, and twine. In October 2023, NatureWorks began the construction of a fully integrated Ingeo PLA biopolymer plant in Thailand, which is expected to begin operations in 2025, supporting regional growth. NatureWorks' materials are designed to enhance plant growth, drain landscapes, or control weeds, providing unique ways to make it grow. NatureWorks is a significant player in bringing sustainable solutions to the farming sector.

TIPA Corp: Emerging Supplier of Biodegradable Films for Agriculture

TIPA Corp (Israel) TIPA Corp is an emerging supplier of biodegradable films for various applications, including agriculture. In May 2023, TIPA Compostable Packaging acquired Bio4Pack, a Germany-based packaging firm specializing in sustainable packaging solutions, including biodegradable films, to broaden TIPA's product portfolio and strengthen its foothold in the European market. TIPA has a total funding of $130 million over 6 rounds, with its latest funding round being a Series C round on January 2, 2022, for $70 million. TIPA's innovative approach and focus on fully compostable solutions position it as a dynamic force in the agricultural bioplastics market.

Segmentation Analysis: Bioplastics for Agribusiness Market

By Application: Mulch Films Dominate, Fertilizer & Pesticide Encapsulation Delivers Fastest Growth

In 2025, mulch films lead the bioplastics market for agribusiness, holding a 29.4% market share, reflecting widespread adoption in sustainable farming and strong regulatory momentum against conventional plastic mulch. The increasing need for improved soil health and reduced residue in the field underpins this leadership. Fertilizer and pesticide encapsulation is the fastest-growing segment with a CAGR of 15.3%, as bioplastics enable controlled-release formulations that optimize yield and minimize environmental impact. Packaging for agricultural products is also growing rapidly, driven by consumer and retailer demand for eco-friendly food packaging and improved supply chain sustainability.

By Feedstock: Sugarcane and Corn Starch Lead Supply, Algae and Waste Streams Show Highest Growth

Sugarcane and corn starch are the leading feedstocks for bioplastics in agribusiness, accounting for over half the market in 2025. Their dominance stems from established supply chains, cost-effectiveness, and scalability for use in films, pots, and packaging. Algae and waste streams are the fastest-growing feedstocks with a CAGR up to 16.1%, as the industry seeks out new, highly sustainable sources to improve circularity and lower environmental footprints. Lignin-based bioplastics are also gaining attention for use in durable, high-performance products such as pipes, films, and crop protection materials.

By Crop: Fruits & Vegetables Lead Usage, Grains & Oilseeds Hold Significant Share

Fruits and vegetables represent the dominant crop segment, capturing 43% of market demand in 2025. This is driven by intensive use of mulch films, protective packaging, and biodegradable trays in high-value produce farming. Grains and oilseeds hold a significant market share, reflecting the use of bioplastic silage covers, seed coatings, and storage solutions in large-scale field crops. The flowers and ornamentals segment is also notable, with increasing use of bioplastic nursery pots, plant tags, and protective wrappings to support export compliance and sustainability standards.

.png)

China Leading Global Bioplastics Production and Adoption in Agribusiness

China stands as the world’s largest market and producer of bioplastics for agribusiness, underpinned by massive production capacities and state-led sustainability policies. The country produces approximately 580,000 tons per year of biodegradable mulch films, primarily from PBAT/PLA blends, significantly reducing plastic pollution in agriculture. Additionally, innovations such as starch-based controlled-release fertilizer capsules are improving soil health and nutrient efficiency. Recent government initiatives, including subsidies covering 30% of biodegradable mulch film costs, are fueling widespread adoption among farmers. The bioplastics market in China is projected to register a strong CAGR during 2025-2030, driven by rising demand from flexible packaging and increasing adoption of bioplastics. Sinopec has introduced PBS-based mulch films featuring 120-day soil degradation timelines, showcasing China’s capability to deliver practical, scalable bioplastic solutions tailored for its diverse agricultural regions. Backed by the Ministry of Agriculture, China’s bioplastics sector continues to expand, serving both domestic demand and global export markets.

Italy Pioneering Compostable Bioplastics for Sustainable Agriculture

Italy has emerged as a technology leader in compostable solutions for agribusiness, driven by decades of research and policy support. Novamont’s Mater-Bi® mulch films, made from starch-based materials, degrade fully in soil within 90 days, helping reduce plastic residues in agricultural lands. Novamont, headquartered in Italy, continues to be a world leader in bioplastics and biochemicals in 2025, known for its Mater-Bi family of biodegradable and compostable bioplastics used widely in agriculture. Bio-on has advanced bioplastics further with the development of PHA-based seed coatings, enhancing crop protection while maintaining biodegradability. Italy mandates the use of biodegradable materials in EU organic farming programs, contributing to significant domestic adoption about 70% of Italian tomato farms already employ biodegradable mulch films. Italy's strong regulatory environment and focus on the circular bioeconomy ensure continued domestic adoption of biodegradable agricultural solutions. Italy’s leadership in biopolymer innovation, combined with strong regulatory frameworks, positions it as a crucial driver of sustainable agriculture across Europe and beyond.

United States Accelerating Growth in Bioplastics for Agribusiness

The United States is the fastest-growing market for bioplastics in agribusiness, fueled by technological innovation, environmental policy shifts, and consumer demand for sustainable food systems. Companies like NatureWorks and Danimer are producing PLA/PHA blended greenhouse films that offer compostability and high-performance agricultural protection. The U.S. bioplastic market is projected to reach USD 4.9 billion in 2025 and grow significantly, driven by increasing demand for eco-friendly plastics due to government regulations and consumer preferences. Other notable products include biodegradable twine and netting from BioBag Americas, reducing plastic waste in horticulture and crop management. Policy frameworks such as the USDA BioPreferred Program prioritize bioplastic agricultural inputs, while California’s SB 54 legislation is phasing out conventional agricultural plastics. The global bioplastic for agribusiness market is valued at approximately $2.5 billion in 2025 and is projected to exhibit a strong CAGR from 2025 to 2033, with North America holding a significant market share. The result is robust market growth and increasing adoption of bioplastics across diverse farming applications, positioning the U.S. as a significant force in sustainable agriculture.

Germany Pioneering High-Tech Bioplastics for Precision Agriculture

Germany is spearheading high-tech applications of bioplastics in agribusiness through advanced research and innovation. BASF’s Ecovio® mulch films integrate nutrient-release technologies, simultaneously providing weed control and fertilization benefits. As of 2025, BASF continues to showcase its Ecovio® products at major industry events like K 2025, emphasizing its circularity solutions and high performance, including tailored compostable coatings for agricultural applications. The Fraunhofer Institute has developed sensor-embedded biodegradable films capable of real-time monitoring of soil conditions, supporting precision agriculture practices. The EU Soil Strategy mandates the elimination of non-degradable agri-plastics by 2026, providing strong regulatory support for bioplastic adoption. BASF's Performance Materials division plants in Europe have fully transitioned to renewable electricity as of January 2025, underscoring their commitment to sustainability in material production, which includes bioplastics. Germany’s blend of technological leadership and environmental regulation ensures it remains at the forefront of sustainable agriculture innovations in Europe.

Brazil Offering Tropical Solutions Through Bio-based Agricultural Plastics

Brazil’s bioplastics industry is focused on solutions tailored to tropical agriculture, leveraging its natural resources and expertise in sustainable materials. Braskem’s development of sugarcane-based polyethylene (PE) provides UV-resistant mulch films capable of withstanding intense solar exposure, crucial for tropical farming conditions. Braskem is the leading global producer of bio-based plastics from sustainably sourced, sugarcane-based bio-ethanol, which captures CO2 from the atmosphere and is used in various applications, including packaging and films. Additionally, innovative products like banana fiber-reinforced biodegradable pots contribute to Brazil’s unique positioning in sustainable horticulture. Government support through a 25% tax credit for sustainable agricultural plastics further accelerates the transition toward bioplastics. Brazil's petrochemical sector, including bioplastics producers like Braskem, is seeing positive momentum in 2025 with proposed government incentive programs aiming to enhance competitiveness and sustainability, such as Bill 892/2025. As global agribusiness looks to tropical regions for expansion, Brazil’s bioplastics sector is set to play a pivotal role.

India Emerging as a Key Player in Bioplastics for Agribusiness

India is rapidly emerging as a crucial market for bioplastics in agribusiness, driven by environmental policies, cost incentives, and local innovations. The Indian government has banned conventional plastic mulch films in eight states, creating substantial demand for biodegradable alternatives. The Indian bioplastics market was valued at around ₹3,730 crore in 2023 and is expected to grow significantly by 2030, driven by regulatory pushes, public awareness, and international market access. Subsidies covering up to 40% of the cost are encouraging farmers to adopt sustainable materials. Local R&D is thriving, with IIT Madras pioneering tamarind seed biopolymers for water-retention mulch films suitable for India’s diverse climatic zones. Government initiatives and schemes in 2025 are increasingly prioritizing sustainable farming and eco-friendly practices, including financial support for inputs like biodegradable mulch films, aiming to boost adoption rates. Demand for bioplastic mulch has surged, demonstrating India’s significant potential to become a global hub for sustainable agriculture solutions.

Bioplastics For Agribusiness Market Report Scope

Bioplastics For Agribusiness Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.7 Billion

|

|

Market Size (2034)

|

$12.6 Billion

|

|

Market Growth Rate

|

14.6%

|

|

Segments

|

By Biodegradable Bioplastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch-based Plastics, Polybutylene Succinate (PBS), Cellulose-based Plastics, Polycaprolactone (PCL)), By Non-Biodegradable Bioplastics (Bio-Polyethylene (Bio-PE), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA)), By Application (Mulch Films, Nursery Products, Porous and Drainage Pipes, Greenhouse Films & Sheeting, Crop Protection & Storage, Fertilizer & Pesticide Encapsulation, Soil Enhancers, Packaging for Agricultural Products, Others), By Feedstock (Sugarcane, Corn Starch, Cassava, Potato Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams), By Crop (Fruits & Vegetables, Grains & Oilseeds, Flowers & Ornamentals, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE (Germany), Novamont S.p.A. (Italy), NatureWorks LLC (U.S.), BioBag International AS (Norway), Kingfa Sci. & Tech. Co., Ltd. (China), FKuR Kunststoff GmbH (Germany), Danimer Scientific (U.S.), Mitsubishi Chemical Group Corporation (Japan), Organix Ag (U.S.), Green Dot Bioplastics (U.S.), AB Rani Plast Oy (Finland), Armando Alvarez Group (Spain), RKW SE (Germany), TotalEnergies Corbion (Netherlands), Good Natured Products Inc. (Canada), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bioplastics For Agribusiness Market Segmentation

By Biodegradable Bioplastics

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Starch-based Plastics

- Polybutylene Succinate (PBS)

- Cellulose-based Plastics

- Polycaprolactone (PCL)

By Non-Biodegradable Bioplastics

- Bio-Polyethylene (Bio-PE)

- Bio-Polypropylene (Bio-PP)

- Bio-Polyamides (Bio-PA)

By Application

- Mulch Films

- Nursery Products

- Porous and Drainage Pipes

- Greenhouse Films & Sheeting

- Crop Protection & Storage

- Fertilizer & Pesticide Encapsulation

- Soil Enhancers

- Packaging for Agricultural Products

- Others

By Feedstock

- Sugarcane

- Corn Starch

- Cassava

- Potato Starch

- Cellulose

- Vegetable Oils

- Lignin

- Algae

- Waste Streams

By Crop

- Fruits & Vegetables

- Grains & Oilseeds

- Flowers & Ornamentals

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Bioplastics for Agribusiness Market

- BASF SE (Germany)

- Novamont S.p.A. (Italy)

- NatureWorks LLC (US)

- BioBag International AS (Norway)

- Kingfa Sci. & Tech. Co., Ltd. (China)

- FKuR Kunststoff GmbH (Germany)

- Danimer Scientific (US)

- Mitsubishi Chemical Group Corporation (Japan)

- Organix Ag (US)

- Green Dot Bioplastics (US)

- AB Rani Plast Oy (Finland)

- Armando Alvarez Group (Spain)

- RKW SE (Germany)

- TotalEnergies Corbion (Netherlands)

- Good Natured Products Inc. (Canada)

* List Not Exhaustive

Methodology:

The research for the Global Bioplastics for Agribusiness Market integrates rigorous primary interviews with stakeholders, including polymer manufacturers, agricultural technology providers, distributors, agribusiness firms, sustainability managers, and policymakers, to gather first-hand insights into market dynamics, technological advancements, regulatory impacts, and evolving end-user preferences. This primary intelligence is corroborated by comprehensive secondary research utilizing corporate reports, regulatory documents (e.g., EU CAP 2023–2027, USDA BioPreferred Program, India’s Plastic Waste Management Rules), patent databases, scientific publications, and trusted industry sources such as European Bioplastics, FAO, and regional trade associations. A robust triangulation process ensures the accuracy and reliability of market size estimates, segmentation data, and forecast modeling. This analytical approach guarantees actionable, validated insights, providing a robust foundation for market projections through 2034.

Research Coverage:

- Geographic Scope: In-depth coverage of 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Segmentation: Detailed analysis by:

- Biodegradable Bioplastics: Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch-based Plastics, Polybutylene Succinate (PBS), Cellulose-based Plastics, Polycaprolactone (PCL).

- Non-Biodegradable Bioplastics: Bio-Polyethylene (Bio-PE), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA).

- Application: Mulch Films, Nursery Products, Porous and Drainage Pipes, Greenhouse Films & Sheeting, Crop Protection & Storage, Fertilizer & Pesticide Encapsulation, Soil Enhancers, Packaging for Agricultural Products, Others.

- Feedstock: Sugarcane, Corn Starch, Cassava, Potato Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams.

- Crop: Fruits & Vegetables, Grains & Oilseeds, Flowers & Ornamentals, Others.

- Competitive Landscape: Profiles and strategic analysis of 20+ leading global and regional producers, technology innovators, and specialty polymer suppliers.

- Trends & Disruptions: Examination of cutting-edge developments in biopolymer chemistry, sustainable feedstock utilization, regulatory shifts, circular economy principles, and integration of bioplastics into advanced agricultural technologies like precision farming.

- Industry Dynamics: Assessment of market drivers, restraints, investment flows, capacity expansions, cost structures, regulatory frameworks, and supply chain evolution.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

Deliverables:

- Full Market Research Report (PDF, Excel): Inclusive of detailed data tables, charts, and visualization tools.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034).

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker.

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.