Market Overview: Bleaching Clay Market Growth Linked to Renewable Diesel Filtration, PFAS-Free Processing, and Circular Spent Clay Recovery (2025–2034)

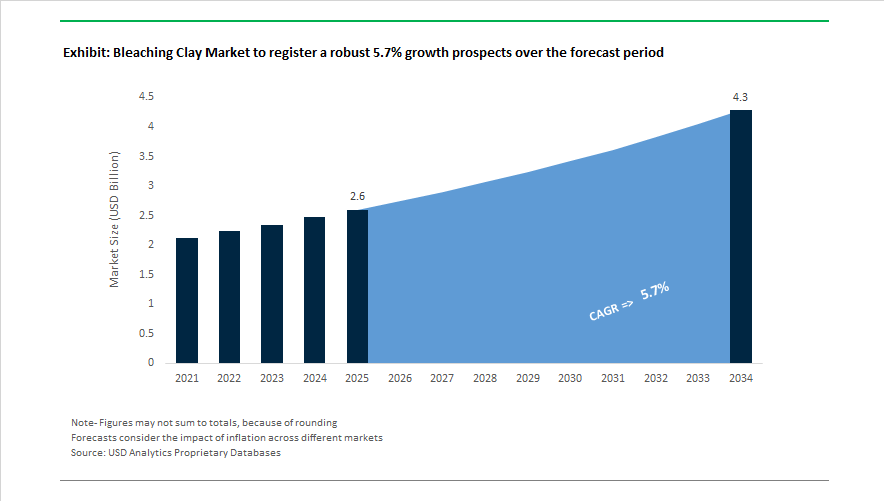

The bleaching clay market is projected to increase from USD 2.6 billion in 2025 to USD 4.3 billion by 2034, reflecting a CAGR of 5.7% supported by rising demand for edible oil purification, renewable diesel feedstock processing, biofuel upgrading, and specialty lubricant filtration. Sustainability and regulatory alignment became defining factors in 2024. In June 2024, Clariant highlighted advanced clay technologies at Metal China, underscoring high-surface-area mineral adsorbents designed to meet stricter environmental requirements. In November 2024, Clariant completed its transition to a PFAS-free additives portfolio, ensuring that its clay-based processing aids comply with tightening environmental regulations across Europe and North America. Circular resource utilization accelerated in late 2024 when Shell finalized its acquisition of EcoOils, enabling recovery of residual oil from spent bleaching clay for use in sustainable aviation fuel and biodiesel, while reusing mineral residues in construction materials.

Industrial demand strengthened through 2025 as renewable fuels and edible oil refining volumes expanded. In early 2025, the United States introduced targeted tariffs on imported bentonite and related bleaching clays, prompting refiners to prioritize domestic activation capacity and reshaping North American supply chains. Oil-Dri reported record B2B revenues in October 2025, with its Fluids Purification segment benefiting from a 19% rise in bleaching clay demand tied to edible oil filtration and renewable diesel production. In ASEAN markets, Indonesia advanced B40 biodiesel blending trials during 2024 and 2025, requiring more intensive double-bleaching processes and boosting captive demand for high-activity clays from producers such as Musim Mas, which launched its ZAKURO bleaching earth brand to support integrated palm oil refining and biofuel processing.

Corporate strategy realignment and specialty applications are reinforcing market resilience entering 2026. In October 2025, Clariant reported a 230 basis point improvement in EBITDA margins within its Adsorbents and Additives unit, reflecting operational efficiency and stable bleaching clay demand. The company also received a global supplier award in October 2025 recognizing its leadership in sustainable materials. EP Engineered Clays expanded its portfolio in 2025 with high-jetness adsorbents tailored for specialty lubricants, targeting removal of trace metals and oxidation by-products. In January 2026, Ingevity signaled integration of lignin chemistry with clay adsorbents to improve purification systems for renewable fuels, aligning adsorbent technology with bio-based feedstocks. Parallel developments in high-purity metallic salt research highlighted by 5N Plus in early 2026 also echo advances in catalytic and adsorptive mineral technologies.

Technology-Led Trends and Growth Opportunities Reshaping the Bleaching Clay Market

Acid-Activated Bleaching Clays Become Strategic for Biodiesel Purification

Biodiesel producers are rapidly replacing natural bleaching clays with acid-activated variants due to superior removal of phospholipids, chlorophyll pigments, and oxidation precursors that destabilize fuel quality. Widely referenced benchmarks published through 2024 and 2025 show that acid activation expands bentonite surface area from roughly 100 m² per gram to more than 300 m² per gram, supporting a 20 to 30% reduction in total clay usage per batch while still meeting fuel cleanliness requirements. This performance advantage is particularly important as fuel producers adopt lower-cost and more challenging feedstocks such as rapeseed, soybean, and distillers corn oil. To comply with fuel standards such as EN 14214, refiners are increasingly specifying sulfuric-acid-activated grades that consistently maintain phosphorus concentrations below 5 ppm, enabling longer catalyst life and fewer downstream purification stages.

Reactivation and Oil Recovery from Spent Bleaching Clay Gain Strategic Priority

Spent Bleaching Clay (SBC) has emerged as a high-risk operational bottleneck, containing 20 to 40% entrapped oil and presenting disposal liabilities. Research published in 2025 demonstrates the improved efficiencies of Direct Heat Treatment (DHT) at nearly 500°C, which restores adsorption performance close to virgin clay and unlocks recoverable oil streams suitable for biogas feedstock or industrial fuel. Regulatory tightening is accelerating this trend. In October 2025, bodies such as the National Green Tribunal (NGT) and HSPCB reclassified certain wet-processing refiners as high-risk environmental units, increasing penalties for landfill disposal. As a result, Zero Liquid Discharge (ZLD) and on-site regeneration equipment are becoming procurement differentiators in refinery modernization programs.

Bleaching Clays Positioned as Critical Pretreatment Media for SAF and HVO Production

The scale-up of Sustainable Aviation Fuel (SAF) and Hydrotreated Vegetable Oil (HVO) is redefining the functional role of bleaching clays from commodity purification agents to high-performance catalyst protectants. Hydroprocessing units operating above 350°C require near-complete removal of polyethylene particles, metals, and chloride contaminants to avoid catalyst poisoning and unscheduled downtime. In March 2025, technology providers including Alfa Laval and GEA identified bleaching earth-based guard beds as essential assets in SAF production lines. Parallel innovation is emerging via enzymatic hybridization. Novozymes’ Quara LowP solution, introduced in late 2024, integrates enzymatic degumming with specialty bleaching clay to process high-impurity inputs such as palm oil mill effluent (POME) and tallow. This approach lowers clay-to-oil ratios and cuts hazardous waste volumes by approximately 15 percent, offering cost and ESG advantage to new SAF developers.

Pharmaceutical-Grade Omega-3 Refining Drives Demand for Ultra-Pure Specialty Clays

Nutraceutical and pharmaceutical refiners are adopting specialty activated clay systems capable of eliminating dioxins, polychlorinated biphenyls (PCBs), and PCDDs while maintaining the molecular integrity of EPA and DHA fatty acids. Scientific data from 2024 to 2025 indicates that activated carbon–clay composites can achieve up to 93% reduction in toxic equivalency values, enabling oil producers to meet stringent FDA and EFSA safety thresholds for prescription-strength omega-3 concentrates. Because polyunsaturated fatty acids oxidize rapidly at high temperatures, refiners are increasingly specifying clays suited for low-temperature bleaching cycles that maintain clarity, odor control, and nutritional quality. This niche but high-value segment is elevating bleaching clay specification criteria from cost-per-ton purchasing toward purity, thermal stability, and pharmaceutical compliance documentation.

Bleaching Clay Market Share and Segmentation Insights

Market Share by Product Type: Acid-Activated Grades Lead Volume While Specialty Adsorbents Capture Regulatory-Driven Growth

Acid activated bleaching earth holds a dominant 58% share of the Bleaching Clay Market in 2025, reflecting its superior adsorption efficiency in edible oil refining and industrial purification. Produced by acid-treating montmorillonite bentonite, this grade delivers high surface area, enhanced porosity, effective decolorization, trace metal removal, and oxidative stability improvement, making it the industry standard for palm, soybean, sunflower, and rapeseed oil processing. Natural bleaching earth ranks second, favored in cost-sensitive and environmentally regulated regions due to its lower carbon footprint and absence of acid effluent, despite reduced adsorption capacity. Activated bauxite occupies a niche role in continuous contact systems, mineral oil refining, and wax purification, valued for mechanical strength and attrition resistance. Specialty adsorbents represent the smallest but fastest-growing segment, encompassing engineered clays and blended systems designed to remove MCPD esters, glycidol esters, PAHs, and dioxins, driven by tightening global food safety standards and premium oil quality requirements.

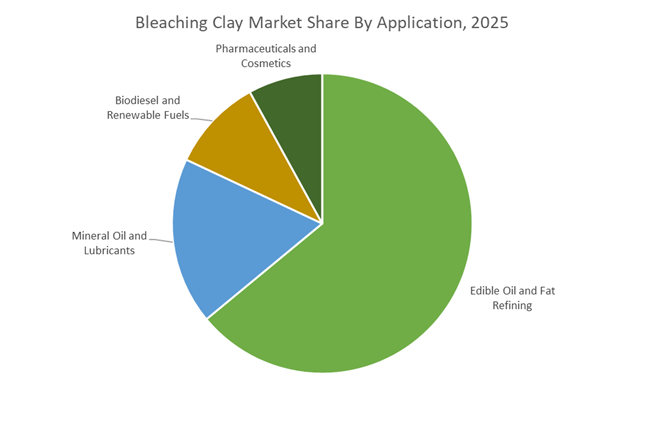

Market Share by Application: Edible Oils Dominate While Renewable Fuels Accelerate Adoption

Edible oil and fat refining accounts for 64% of bleaching clay consumption in 2025, anchored by its essential role in removing chlorophyll, phospholipids, soaps, trace metals, and oxidation by-products across major vegetable oils. Rising middle-class consumption in Asia, population growth, and processed food expansion continue to underpin demand. Mineral oil and lubricants form the second-largest segment, supported by re-refining of used motor oil, transformer oil purification, and wax treatment, reinforced by circular economy mandates and extended producer responsibility schemes. Biodiesel and renewable fuels represent the fastest-growing application, utilizing bleaching clay to purify used cooking oil, animal fats, and crude biodiesel prior to hydrotreating, with global biofuel mandates and SAF commitments from aviation accelerating uptake. Pharmaceuticals and cosmetics remain niche but high-value, requiring GMP-compliant, low-metal, inert clays for vitamin intermediates, cosmetic waxes, and pharmaceutical oils.

Competitive Landscape Analysis of the Bleaching Clay Market

The global bleaching clay market in 2026 is being reshaped by renewable diesel expansion, sustainable aviation fuel (SAF) pretreatment, edible oil refining upgrades, and circular economy filtration needs. Competitive advantage increasingly centers on low oil loss activated bentonite, high-surface-area adsorbents, and acid-activated bleaching earth engineered for pigment removal, phosphorus control, and trace metal adsorption. Market leaders are integrating dry-activation processes, zero-acid leaching, dual-media filtration, and solid acid catalyst technologies to serve biofuels, palm oil refining, aromatics purification, cosmetics, and recycled feedstock upgrading. Sustainability credentials, vertical integration, and proximity to palm oil and renewable diesel hubs now define supplier positioning across Asia-Pacific, North America, and Europe.

Clariant drives low oil loss standards and biofuel pretreatment innovation

Clariant remains the technological benchmark through its Tonsil portfolio, with Tonsil Supreme and Tonsil Optimum delivering high surface area and optimized pore volume for low-dosage removal of chlorophyll and pro-oxidative metals. In 2026, the company is aggressively targeting adsorbents for biofuels, supporting second-generation feedstock pretreatment where ultra-low phosphorus is mandatory for SAF catalyst protection. Following its Lucas Meyer Cosmetics acquisition, Clariant is also integrating bleaching clay into natural beauty formulations, using clay as UV filter stabilizers. Late-2025 innovations include Geko industrial clays and dry-activation processes that reduce water consumption by 30% , reinforcing its leadership in sustainable activated bentonite solutions.

Oil-Dri Corporation of America leverages mine-to-market control for renewable diesel demand

Oil-Dri operates a fully vertical mine-to-market model, giving it unmatched supply security in bleaching earth and sorbent minerals. In Q1 2026, its Fluids Purification segment posted record sales, fueled by a 19% surge in renewable diesel refining demand across North America. The Pure-Flo and Select series focus on high-float clays that prevent filter blinding in high-speed edible oil and industrial reclamation systems. After reducing corporate debt below $40 million, Oil-Dri reinvested heavily in R&D for agricultural carrier applications, extending bleaching clay substrates into precision pesticide delivery while strengthening digital infrastructure and mineral processing efficiency.

Taiko Group dominates Asian edible oil refining through volume and purity

Taiko Group is a major force across Asia, capitalizing on its proximity to palm oil production hubs to provide rapid, local-for-local bleaching earth supply. Its UltraPure 75 flagship is optimized for industrial edible oil and wax refining, removing oxidation byproducts while preserving fatty acid profiles. In 2025/2026, Taiko scaled its zero-acid leaching technology to meet stringent European food safety requirements for low residual acidity. With moisture-resistant packaging and inventory across more than 13 countries, Taiko buffers global shipping volatility while serving mass-market refiners demanding consistent tonnage, fast delivery, and dependable activated clay performance.

Musim Mas Group integrates bleaching earth across the palm oil value chain

Musim Mas deploys its ZAKURO calcium bentonite bleaching earth across its fully integrated palm oil operations, supporting food, biofuels, and paraffin purification. Unlike standalone suppliers, Musim Mas beta-tests new clay formulations directly in its own refineries before external commercialization. In 2025/2026, it became the first major group verified by the Palm Oil Innovation Group for downstream applications, ensuring responsible sourcing compliance. Its 2026 R&D emphasizes gentle purification, removing gums and impurities while preserving natural tocopherols, aligning bleaching clay performance with shelf-life optimization for specialty fats and high-value edible oil products.

EP Engineered Clays advances adsorption science for aromatics and catalytic applications

EP Engineered Clays specializes in high-complexity hydrocarbon and oleochemical purification through its F-Series activated clays, widely regarded in 2026 as the industry standard for removing olefin and nitrogen contaminants in BTX streams. Its dual-media approach combines bleaching clay with diatomaceous earth filter aids to deliver crystal-clear edible oils. The F-24X aromatic solution offers extended catalyst life for solid acid processes, minimizing unplanned refinery downtime. EP is shifting toward catalytic solutions, using modified clays to replace liquid acids in chemical reactions, enabling safer, greener manufacturing across petrochemical and specialty refining environments.

BASF positions bleaching clays as enablers of circular purification

BASF applies its Verbund integration to produce tech-intensive adsorbents supporting pharma-grade nutrition ingredients, EV battery precursor filtration, and recycled oil purification. Under its updated Winning Ways strategy, BASF is strengthening integrated value chains while expanding its Environmental Catalyst and Metal Solutions unit to serve high-purity applications. In-house acid production for clay activation ensures cost stability and reduced carbon footprint. Looking ahead, BASF is positioning bleaching clays as enabling technologies for the circular economy, particularly for purifying pyrolysis oils derived from plastic waste, reinforcing its role in sustainable materials recovery and advanced filtration systems.

Indonesia Bleaching Clay Market: Biodiesel Mandates Reshaping Adsorption Performance Requirements

Indonesia has become the single most influential demand center for bleaching clay, driven by aggressive biofuel blending mandates and downstream processing policies. Effective January 1, 2025, the mandatory B40 biodiesel program has materially increased the need for high-adsorption bleaching clay capable of removing phospholipids, metals, and color bodies from crude palm oil feedstocks. With the government signaling a transition toward B50 by late 2026, refiners are prioritizing acid-activated bleaching earth grades that can operate efficiently at higher free fatty acid levels without excessive oil retention. This shift has structurally raised technical specifications for bleaching clays used in palm oil refining.

Policy-led industrialization is reinforcing domestic value addition. Under the 2025–2026 hilirisasi plan, restrictions on raw bentonite exports are incentivizing local conversion into activated bleaching earth. This has accelerated investments by integrated refiners such as Musim Mas Group, which expanded its Medan refinery in mid-2025 with advanced filtration systems using low-retention clays to reduce neutral oil loss. Technological pilots are also emerging. Refineries in Riau and Kalimantan began testing in-situ bleaching earth regeneration in late 2025 to address spent clay disposal. Regulatory support followed when the Ministry of Environment and Forestry updated its 2026 waste guidelines, allowing spent bleaching earth to be reclassified as a secondary raw material for cement and brick manufacturing once de-oiling benchmarks are met.

Malaysia Bleaching Clay Market: Compliance-Driven Activation and Circular SBE Utilization

Malaysia’s bleaching clay market is being shaped by export compliance and technology-led differentiation. After the European Union recognized the Malaysian Sustainable Palm Oil scheme in September 2025, refiners upgraded bleaching protocols to ensure effective removal of 3-MCPD and glycidyl esters. This has driven demand for ultra-activated bleaching earth with higher surface acidity and controlled pore structure, especially for export-oriented palm and oleochemical derivatives.

Corporate capacity expansion has followed. Taiko Clay Group commissioned a new production line at its Perak facility in late 2025 using proprietary acid-activation technology to supply premium oleochemical applications. Circularity is gaining traction alongside performance. In November 2025, the Malaysian Palm Oil Board partnered with private firms to demonstrate a commercial bio-organic fertilizer plant that uses processed spent bleaching earth as a nutrient carrier. Parallel academic research is reinforcing efficiency gains. As of January 2026, Malaysian universities are patenting modified sepiolite-based bleaching agents that reduce phosphoric acid consumption during pre-treatment by roughly 20% , directly lowering refining chemical intensity.

United States Bleaching Clay Market: Renewable Diesel Pretreatment and Purity Enforcement

In the United States, bleaching clay demand is increasingly linked to renewable fuels and regulatory purity standards rather than traditional edible oil volumes. The rapid expansion of hydrotreated vegetable oil facilities along the Gulf Coast throughout 2025 has created a secondary but fast-growing requirement for bleaching clay used to pretreat distillate-grade soybean and corn oil feedstocks. These applications demand consistent adsorption of trace metals and chlorophyll to protect downstream catalysts in renewable diesel units.

Regulatory oversight is tightening simultaneously. Updates to the Food Safety Modernization Act in 2025 increased scrutiny of heavy-metal leaching from bleaching clays, favoring high-purity bentonites sourced from Wyoming and Mississippi. Pricing dynamics adjusted accordingly when Oil-Dri Corporation of America announced a strategic price increase across its fluid purification portfolio in May 2025 to offset higher sulfuric acid and logistics costs for its Pure-Flo line. Innovation remains active. EP Minerals launched the CelaClear series in 2025, combining diatomaceous earth with activated clay to address high-chlorophyll oils that are difficult to bleach using conventional products. At the policy level, the United States Geological Survey classified bentonite as a Mineral of Interest in its 2025 biennial report, unlocking new federal grants to explore high-montmorillonite domestic deposits.

India Bleaching Clay Market: Edible Oil Self-Sufficiency and Export-Oriented Processing

India’s bleaching clay industry is expanding in parallel with national edible oil self-sufficiency goals. Under the National Mission on Edible Oils–Oil Palm, twelve new mega-refineries were under construction in Andhra Pradesh and Telangana by late 2025. These facilities are designed around modern degumming and bleaching configurations, directly increasing domestic consumption of consistent-quality bleaching earth for palm, soybean, and sunflower oil refining.

Industrial policy support is accelerating innovation. Leading producers such as Ashapura Perfoclay leveraged Production Linked Incentive benefits in 2025 to upgrade R&D capabilities focused on natural and eco-bleach formulations that reduce acid usage and spent clay generation. Export competitiveness is strengthening as well. According to the Ministry of Commerce, India recorded a 12% increase in bleaching clay exports to the Middle East and North Africa in 2025, capitalizing on cost-efficient bentonite mining and improving activation technology to meet refinery standards in those markets.

Strategic Snapshot: Bleaching Clay Industry by Country

Bleaching Clay Market County Level Snapshot

|

Country

|

Core Demand Driver

|

Structural Shift Observed

|

|

Indonesia

|

B40/B50 biodiesel mandates

|

High-adsorption clays and SBE circular use

|

|

Malaysia

|

EU palm oil compliance

|

Ultra-activated grades and fertilizer reuse

|

|

United States

|

Renewable diesel and FSMA

|

High-purity bentonites and hybrid adsorbents

|

|

India

|

Edible oil self-sufficiency

|

Refinery-linked demand and export growth

|

Bleaching Clay Market Report Scope

Bleaching Clay Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Acid Activated Bleaching Earth, Natural Bleaching Earth, Activated Bauxite, Specialty Adsorbents), By Technology (Dry Bleaching, Wet Bleaching), By Application (Edible Oil and Fat Refining, Mineral Oil and Lubricants, Biodiesel and Renewable Fuels, Pharmaceuticals and Cosmetics), By Form (Fine Powder, Granular)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Clariant, Oil Dri Corporation of America, Taiko Clay Group, Ashapura Perfoclay, Musim Mas, EP Minerals, BASF, Minerals Technologies, W Clay Industries, Refoil Earth, Sibelco, Mizusawa Industrial Chemicals, 20 Microns, Global Bleach Chem, Manek Active Clay

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bleaching Clay Market Segmentation

By Product Type

- Acid Activated Bleaching Earth

- Natural Bleaching Earth

- Activated Bauxite

- Specialty Adsorbents

By Technology

- Dry Bleaching

- Wet Bleaching

By Application

- Edible Oil and Fat Refining

- Mineral Oil and Lubricants

- Biodiesel and Renewable Fuels

- Pharmaceuticals and Cosmetics

By Form

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bleaching Clay Industry

- Clariant

- Oil Dri Corporation of America

- Taiko Clay Group

- Ashapura Perfoclay

- Musim Mas

- EP Minerals

- BASF

- Minerals Technologies

- W Clay Industries

- Refoil Earth

- Sibelco

- Mizusawa Industrial Chemicals

- 20 Microns

- Global Bleach Chem

- Manek Active Clay

*- List not Exhaustive