Global Clear Brine Fluids Market Overview

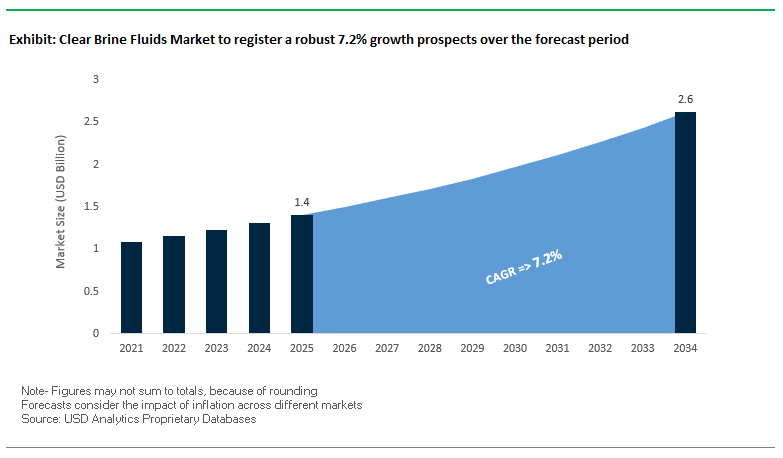

The global clear brine fluids market is projected to grow from $1.4 billion in 2025 to $2.6 billion by 2034, reflecting a CAGR of 7.2%. Clear brine fluids (CBFs) are critical in modern oil and gas drilling operations due to their solids-free composition, which minimizes formation damage and maintains wellbore integrity. These fluids are increasingly preferred for deepwater, unconventional, and enhanced oil recovery (EOR) operations, where stability under high-pressure and high-temperature conditions is essential.

The market is driven by technological advancements in biodegradable, low-toxicity brines and a growing focus on environmental compliance in offshore and sensitive drilling environments. Additionally, rising EOR activities and new deepwater discoveries in Latin America and Africa are expanding demand for clear brine fluids. For industry Stakeholders, CBFs not only enhance drilling efficiency but also support sustainable operations by reducing chemical usage and formation damage.

Key Insights for Industry Stakeholders:

- Optimizing Wellbore Integrity: Solids-free fluids prevent clay swelling, ensuring a clean and unobstructed wellbore.

- Deepwater and Unconventional Drilling: Essential for high-pressure, high-temperature wellbore stabilization.

- Environmental Focus: Biodegradable and low-toxicity brines meet stringent environmental regulations.

- Enhanced EOR Operations: Clear brine fluids improve reservoir performance in workover and completion phases.

- Operational Efficiency: Supports reduced chemical use, minimized formation damage, and maximized production rates.

Market Analysis: Recent Developments in Clear Brine Fluids

The clear brine fluids market has seen notable developments in 2024–2025 that signal both technological innovation and policy-driven demand growth. In August 2025, India launched the National Deep Water Exploration Mission, opening over 1 million square kilometers for offshore exploration, indicating a major market opportunity for CBFs in the region. During the same month, RSE and Siemens signed a Memorandum of Understanding to integrate digital, AI, and automation tools into water treatment systems, reflecting cross-industry trends in advanced fluid management technologies that could be leveraged for oilfield operations.

In July 2025, the City of Midland partnered with Gateway Collectors to modernize its Advanced Metering Infrastructure, signaling a broader infrastructure modernization trend that could influence fluid management in drilling. In March 2025, Siemens and KETOS announced a strategic partnership for real-time monitoring and analytics, highlighting rising demand for intelligent fluid tracking solutions. Veolia’s February 2025 partnership with Mistral AI further emphasized the integration of generative AI to optimize resource use and operational efficiency, which can be applied to managing clear brine fluids in drilling operations.

Strategic acquisitions also shaped the market: Xylem Inc. acquired Idrica in December 2024 to strengthen cloud-based monitoring and analytics capabilities, while Diehl Metering acquired PREVENTIO GmbH in November 2024 to enhance predictive maintenance and real-time leak detection. Additionally, in August 2024, ABB launched next-generation electromagnetic flowmeters with IoT connectivity, providing enhanced visibility and control of fluid flow and properties, signaling increasing adoption of smart monitoring solutions in clear brine fluid operations.

Key Trends Driving Clear Brine Fluids Adoption

Integration of IoT and AI for Real-Time Fluid Management

The clear brine fluids market is witnessing a significant transformation as operators integrate IoT sensors and AI analytics for real-time monitoring and management. A 2024 MDPI study highlights that sensors can continuously measure fluid properties such as density, pH, and temperature, while AI models predict wellbore instability and contamination, reducing downtime. Companies like SLB (Schlumberger) are deploying AI-powered platforms such as Lumi Data, enabling operators to make data-driven decisions that optimize fluid systems, enhance wellbore stability, and improve operational efficiency. The adoption of AI and IoT ensures that clear brine fluids are precisely managed, creating safer, more productive drilling operations.

Shift Toward Environmentally Friendly Brine Formulations

Sustainability is a key trend influencing the clear brine fluids market. Research published in MDPI’s Water shows that potassium acetate and potassium formate outperform traditional fluids like calcium chloride in minimizing clay swelling, while also being less environmentally harmful. Regulatory pressures are reinforcing this trend: stricter discharge regulations compel operators to adopt eco-friendly, compliant brines, reducing environmental impact and avoiding penalties. This trend aligns with the global oilfield services shift toward responsible, sustainable operations while maintaining operational performance.

Optimization of Completion and Workover Operations

Clear brine fluids are increasingly critical in optimizing completion and workover operations. Case studies from major oil companies demonstrate that advanced brines reduce non-productive time during wellbore displacement, ensuring thorough cleaning and preventing costly remedial work. Companies such as Halliburton are deploying digital fluid monitoring solutions to improve wellbore stability and mitigate formation damage during critical phases. These fluids enhance operational reliability and increase productivity across the well lifecycle, emphasizing their strategic value in both completion and intervention operations.

Emerging Opportunities in Clear Brine Fluids Market

The market offers opportunities in premium and customized brines, environmentally compliant formulations, and high-density fluids for HPHT wells. The trend toward digital fluid monitoring and real-time management creates demand for integrated solutions combining AI, IoT, and advanced chemistry, which can be leveraged to improve well performance, reduce operational costs, and meet evolving environmental regulations. Companies focusing on sustainable, high-performance brine solutions are positioned to capture high-margin market segments, particularly in deepwater and shale-rich formations.

Market Share Insights of Clear Brine Fluids Market

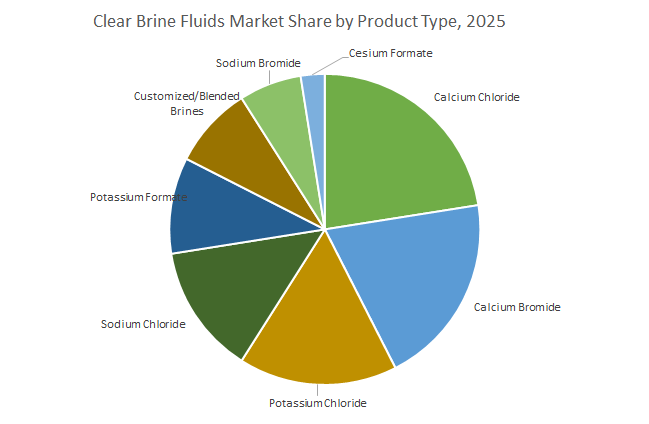

Market Share by Product Type: Calcium Chloride Dominates, Premium Brines Gain Traction

Calcium Chloride (22.5%) and Sodium Chloride (13.2%) dominate the market due to their low cost and versatility for medium-density applications, forming the volume backbone of the industry. Calcium Bromide (20.9%) and Potassium Chloride are critical for complex wells and clay-rich formations, offering high performance where formation protection is essential. Potassium Formate and Customized Blends are gaining traction as eco-friendly, high-performance alternatives, aligning with sustainability goals. Cesium Formate represents the ultra-premium segment for HPHT wells, commanding high value despite lower volumes, highlighting the market’s segmentation between standard and specialized fluids.

Market Share by Density: High-Density Brines Capture Premium Value

High-Density Brines (58.5%) dominate the value share due to their essential role in HPHT and deepwater wells, including blends like CaBr₂, ZnBr₂, and CsFo. These fluids are complex and costly but critical for precise pressure control in high-value drilling projects. Low-Density Brines (44.1%), primarily NaCl and KCl, constitute the majority of volume in conventional-pressure land and offshore wells, providing cost-effective solutions for standard drilling operations.

Market Share by Application: Completion Fluids Lead Critical Operations

Completion Fluids (44.1%) are the largest and most critical application, requiring high purity to prevent formation damage and maximize productivity. Drilling Fluids (26.9%) are used selectively in drilling phases where clear brines provide superior pressure control and wellbore stability. Workover & Well Intervention Fluids (22.5%) maintain and enhance production in existing wells, while Packer Fluids provide permanent pressure control and corrosion inhibition. The segmentation illustrates the market’s focus on high-value, operationally critical applications where precision and performance directly impact drilling efficiency and well economics.

United States: Shale Gas and Deepwater Exploration Driving Demand for High-Performance Clear Brine Fluids

The United States clear brine fluids market remains a global leader, fueled by advancements in shale gas and tight oil exploration across regions such as Texas, North Dakota, and the Gulf of Mexico. With over 40% of oil and gas operators in North America now using clear brine fluids (CBFs) for high-pressure wells, demand is escalating for fluids that ensure wellbore stability, pressure control, and thermal resistance in complex drilling environments.

Government backing further strengthens the U.S. market. Federal support for unconventional hydrocarbon resource development has accelerated deep-well drilling projects, boosting adoption of high-density clear brine fluids in deepwater and unconventional drilling campaigns. As a result, the U.S. is witnessing significant growth in completion fluid consumption, particularly in high-temperature, high-pressure (HTHP) wells.

Saudi Arabia: Oil Reserve Dominance and Offshore Investments Fueling Clear Brine Fluids Market

The Saudi Arabia clear brine fluids market is deeply rooted in the country’s position as the world’s largest crude exporter, with 17% of global proven oil reserves. Saudi Aramco continues to operate a vast fleet of drilling rigs despite oil price volatility, creating steady demand for drilling fluids, including clear brines.

Future growth is tied to the region’s offshore focus. The Middle East offshore oil and gas sector is set to receive $40 billion in investments by 2025, where advanced, high-density clear brine fluids play a vital role in ensuring well integrity and operational efficiency. Saudi Arabia’s drilling strategy emphasizes multi-lateral wells and pressure-isolated completions, driving reliance on specialized completion brines that meet the technical requirements of complex wells.

China: Shale Gas Expansion and Bromine Innovations Strengthening Market Potential

The China clear brine fluids market is expanding rapidly as the government invests in shale gas exploration, leveraging the country’s 15% share of global shale gas reserves. These reserves require HPHT drilling solutions, making high-density clear brines essential for safe and efficient operations.

China is also positioning itself at the forefront of bromine-related innovations, a critical component of clear brine formulations. In April 2024, the Chinese Academy of Sciences unveiled a bromine-iodine battery prototype with 1,200 Wh/L energy density, signaling broader advancements in bromine applications and highlighting the country’s focus on technological innovation. With rising exploration activity and a strong R&D pipeline, China is set to become a major growth hub for clear brine fluids in unconventional resource development.

Norway: Environmental Regulations Driving Adoption of Low-Toxicity Clear Brines

The Norway clear brine fluids market is shaped heavily by the country’s stringent offshore drilling regulations. With strong emphasis on environmental protection, operators are increasingly adopting low-toxicity, biodegradable clear brine fluids to meet compliance requirements.

Norway’s offshore sector, particularly in the North Sea, remains a major driver for the market. Drilling activities in this region require fluids capable of withstanding extreme pressures and low temperatures, while minimizing environmental risk. As a result, demand is strong for specialized, environmentally compliant completion fluids, positioning Norway as a pioneer in sustainable clear brine fluid adoption.

India: Energy Security Goals and Expanding Refining Capacity Fueling Clear Brine Fluids Demand

The India clear brine fluids market is gaining momentum as the government targets energy security and seeks to increase the share of natural gas in the energy mix to 15% by 2030. The Oilfields (Regulation and Development) Amendment Act, 2025, introduced to streamline upstream regulations, is attracting foreign investment in exploration and production (E&P) a key growth catalyst for drilling and completion fluids.

On the infrastructure front, India’s refining capacity is projected to expand to 310 million tonnes per annum by 2028, supported by megaprojects such as the West Coast Refinery in collaboration with Saudi Arabia. The demand for high-performance clear brines is directly tied to this expansion, as efficient fluids are needed to support increased drilling, completion, and well servicing activities.

United Kingdom: North Sea Offshore Projects and Enhanced Oil Recovery Sustaining Market Growth

The United Kingdom clear brine fluids market is anchored in the North Sea’s offshore oil and gas operations, where strict environmental regulations necessitate the use of high-purity, environmentally compliant clear brines. Operators are under pressure to minimize ecological impact while maintaining drilling efficiency, creating steady demand for advanced completion fluids.

A key growth driver in the UK is its focus on mature field development and enhanced oil recovery (EOR) initiatives. Clear brines are increasingly utilized for maintaining reservoir pressure and improving recovery rates in aging fields. This makes the UK market highly reliant on specialized, high-performance brines that balance technical performance and regulatory compliance.

Competitive Landscape of Clear Brine Fluids Market

The clear brine fluids market is highly competitive, driven by the demand for solids-free, environmentally compliant, and high-performance fluids. Leading players differentiate through technological innovation, operational reliability, and the integration of digital and predictive tools to optimize drilling and completion efficiency.

Schlumberger Limited (SLB) dominates wellbore fluid technologies

SLB leverages its extensive portfolio of drilling and completion fluids through its M-I SWACO division. The company offers engineered formate and halide brine solutions designed to maximize production while minimizing environmental impact. SLB’s focus on digital tools for predictive maintenance and an integrated monitoring approach ensures clean, unobstructed wellbores, reducing non-productive time and operational costs for clients.

Halliburton Company provides high-performance drilling solutions

Halliburton delivers engineered clear brine fluids and additives tailored for complex wellbore conditions. Its BaraHib® Nano water-based drilling fluid enhances wellbore stability and reduces fluid loss, offering a viable alternative to nonaqueous fluids. The company emphasizes customized fluid systems that protect drill bits, stabilize wellbores, and improve productivity while mitigating operational risks.

Albemarle Corporation specializes in bromine-based clear brines

Albemarle offers WELLBROM®, a leading clear brine completion fluid used in fracturing, workover, and packer applications. The company’s vertically integrated operations ensure a consistent supply of high-quality products. Planned investments of $540 million in Magnolia, Arkansas, strengthen its production capacity, emphasizing Albemarle’s commitment to delivering reliable, high-purity fluids for high-temperature, high-pressure drilling environments.

TETRA Technologies, Inc. focuses on high-purity, application-specific brines

TETRA provides hybrid and application-specific clear brine fluids, including zinc-free TETRA CS Neptune Completion fluids. Its vertically integrated operations and emphasis on sustainability ensure consistent supply and market resilience. TETRA’s hybrid product offerings are designed to optimize operational efficiency while maintaining environmentally responsible standards.

Solvay S.A. drives chemical innovation in clear brines

Solvay applies advanced salt chemistry to develop high-purity, performance-driven clear brine formulations. Its 2025 sustainability initiatives demonstrate a company-wide focus on green solutions. Solvay leverages its R&D capabilities to support environmentally compliant drilling operations, delivering fluids that meet regulatory standards and industrial performance requirements.

Dow Inc. enhances thermal stability and shale inhibition

Dow offers calcium chloride-based clear brines and other formulations for drilling, completion, and workover applications. Its global supply network ensures reliable sourcing, while its R&D focus on thermal stability and shale inhibition enhances operational efficiency. Dow’s clear brine fluids maintain wellbore integrity and reduce formation damage, supporting safe and productive drilling operations.

Clear Brine Fluids Market Report Scope

Clear Brine Fluids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$2.6 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Product Type (Calcium Chloride, Calcium Bromide, Sodium Chloride, Sodium Bromide, Potassium Chloride, Potassium Formate, Cesium Formate, Customized/Blended Brines), By Density (Low Density Brines, High Density Brines), By Application (Drilling Fluids, Completion Fluids, Workover & Well Intervention Fluids, Packer Fluids), By End-Use Industry (Oil & Gas)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Schlumberger Limited, Halliburton, Baker Hughes Company, TETRA Technologies, Inc., Newpark Resources, Inc., Albemarle Corporation, LANXESS, ICL Group Ltd., Cabot Corporation, Solvay SA, Zirax Limited, GEO Drilling Fluids, Inc., Clements Fluids, TOTAL Specialties USA, Inc., Chemcon Speciality Chemicals Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Clear Brine Fluids Market Segmentation

By Product Type

- Calcium Chloride

- Calcium Bromide

- Sodium Chloride

- Sodium Bromide

- Potassium Chloride

- Potassium Formate

- Cesium Formate

- Customized/Blended Brines

By Density

- Low Density Brines

- High Density Brines

By Application

- Drilling Fluids

- Completion Fluids

- Workover & Well Intervention Fluids

- Packer Fluids

By End-Use Industry

- Oil & Gas Onshore

- Oil & Gas Offshore

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Clear Brine Fluids Industry include-

- Schlumberger Limited

- Halliburton

- Baker Hughes Company

- TETRA Technologies, Inc.

- Newpark Resources, Inc.

- Albemarle Corporation

- LANXESS

- ICL Group Ltd.

- Cabot Corporation

- Solvay SA

- Zirax Limited

- GEO Drilling Fluids, Inc.

- Clements Fluids

- TOTAL Specialties USA, Inc.

- Chemcon Speciality Chemicals Pvt. Ltd.

*- List not Exhaustive

Research Coverage

The Clear Brine Fluids Market Report by USDAnalytics this report investigates how solids-free brines are advancing completion, workover, and HPHT drilling performance; it highlights breakthroughs in low-toxicity/biodegradable formulations, digital fluid monitoring, and real-time density/chemistry control; delivers analysis reviews on HPHT pressure management, clay-control chemistries, and sustainability compliance; and maps procurement and logistics strategies for deepwater and unconventional campaigns. Anchored in recent offshore awards, EOR programs, and digitalization of fluids management, this report is an essential resource for drilling/completions leaders, fluids engineers, and supply-chain managers seeking to reduce formation damage, shorten NPT, and maximize wellbore integrity across challenging reservoirs. Scope Includes-

- Segmentation: By product type (chlorides, bromides, formates, customized blends), density class, application, and end-use industry

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Schlumberger (SLB); Halliburton; Baker Hughes Company; TETRA Technologies, Inc.; Newpark Resources, Inc.; Albemarle Corporation; LANXESS; ICL Group Ltd.; Cabot Corporation; Solvay SA; Zirax Limited; GEO Drilling Fluids, Inc.; Clements Fluids; TOTAL Specialties USA, Inc.; Chemcon Speciality Chemicals Pvt. Ltd.

Methodology

USDAnalytics combines primary interviews with drilling/completions managers, fluids specialists, and procurement teams across key basins with secondary validation from operator filings, MSDS libraries, environmental approvals, port/import records, and service-company disclosures. We build bottom-up demand models by rig count, well class (HPHT/deepwater/shale), and completion intensity, then reconcile with top-down brine production/TradeMap flows and service backlogs. Scenario forecasts (2025–2034) incorporate offshore FIDs, EOR project pipelines, density-tier mix shifts, additive price indices, and regulatory constraints on discharge/toxicity. Competitor benchmarking assesses purity specs, corrosion inhibition, clay-swelling performance, recyclability, logistics footprint, and digital monitoring readiness to produce decision-grade market sizing and share estimates.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Clear Brine Fluids Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Clear Brine Fluids Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.4 Billion

2.2.2. Forecasted Market Size (2034): $2.6 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 7.2%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Deepwater and Unconventional Drilling, and Environmental Regulations

2.3.2. Challenges: Oil Price Volatility and Competition from Other Fluids

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Integration of IoT and AI for Real-Time Fluid Management

3.2. Shift Toward Environmentally Friendly Brine Formulations

3.3. Optimization of Completion and Workover Operations

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Government Policy Initiatives

3.4.2. Technology Integration and Partnerships

4. Clear Brine Fluids Market – Segmentation Insights

4.1. By Product Type

4.1.1. Calcium Chloride (22.5% Market Share)

4.1.2. Calcium Bromide (20.9% Market Share)

4.1.3. Sodium Chloride (13.2% Market Share)

4.1.4. Other Brine Types (Potassium, Cesium, Customized Blends)

4.2. By Density

4.2.1. High-Density Brines (58.5% Market Share)

4.2.2. Low-Density Brines (44.1% Market Share)

4.3. By Application

4.3.1. Completion Fluids (44.1% Market Share)

4.3.2. Drilling Fluids (26.9% Market Share)

4.3.3. Workover & Well Intervention Fluids (22.5% Market Share)

4.3.4. Packer Fluids

4.4. By End-Use Industry

4.4.1. Oil & Gas Onshore

4.4.2. Oil & Gas Offshore

5. Country Analysis and Outlook: Clear Brine Fluids Market

5.1. United States: Shale Gas & Deepwater Exploration

5.2. Saudi Arabia: Oil Reserve Dominance & Offshore Investments

5.3. China: Shale Gas Expansion & Bromine Innovations

5.4. Norway: Environmental Regulations & Low-Toxicity Brines

5.5. India: Energy Security Goals & Expanding Refining Capacity

5.6. United Kingdom: North Sea Offshore Projects & EOR

6. Clear Brine Fluids Market Size Outlook by Region (2025–2034)

6.1. North America Clear Brine Fluids Market Size Outlook to 2034

6.1.1. By Product Type

6.1.2. By Application

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Clear Brine Fluids Market Size Outlook to 2034

6.2.1. By Product Type

6.2.2. By Application

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Clear Brine Fluids Market Size Outlook to 2034

6.3.1. By Product Type

6.3.2. By Application

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Clear Brine Fluids Market Size Outlook to 2034

6.4.1. By Product Type

6.4.2. By Application

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Clear Brine Fluids Market Size Outlook to 2034

6.5.1. By Product Type

6.5.2. By Application

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Competitive Landscape: Key Companies

7.1. Schlumberger Limited (SLB)

7.1.1. Company Overview

7.1.2. Dominance in Wellbore Fluid Technologies

7.2. Halliburton Company

7.2.1. Company Overview

7.2.2. High-Performance Drilling Solutions

7.3. Albemarle Corporation

7.4. TETRA Technologies, Inc.

7.5. Solvay S.A.

7.6. Other Prominent Companies

7.6.1. Baker Hughes Company

7.6.2. Newpark Resources, Inc.

7.6.3. Dow Inc.

7.6.4. LANXESS

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures