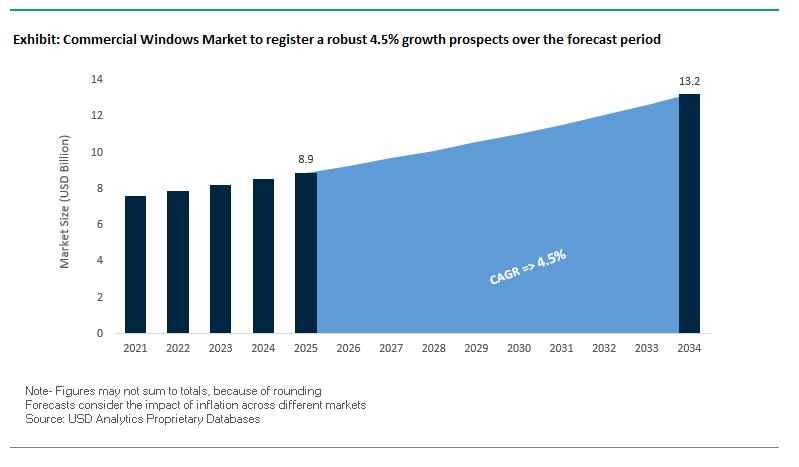

Market Overview: Commercial Windows Market Valued at $8.9 Billion in 2025

The Global Commercial Windows Market is valued at USD 8.9 billion in 2025 and forecasted to reach USD 13.2 billion by 2034, expanding at a CAGR of 4.5%. Growth is being driven by the convergence of stricter building energy codes, rising retrofit demand, and advancements in smart window technologies. For industry leaders and procurement managers, windows are no longer just structural elements; they are integral to energy efficiency strategies, acoustic performance, and digital building management systems.

Energy efficiency is the core driver of this market, with triple-pane windows and Low-E coatings becoming mainstream due to regulatory pressure. Renovation activity dominates in mature regions such as the DACH market (Germany, Austria, Switzerland), where over 60% of sales in 2025 are linked to retrofits, supported by government incentives and financing subsidies. At the same time, smart electrochromic glass is gaining traction, enabling buildings to optimize solar gain and indoor comfort through integration with facility management systems.

Another critical factor is acoustic insulation, especially in urbanized hubs. Multi-layer laminated glass and advanced sealing systems are being adopted at scale to minimize noise pollution and enhance workplace productivity. As buildings evolve into smart, sustainable, and wellness-driven spaces, commercial windows are now evaluated not only for durability and aesthetics but also for carbon performance and long-term operational savings.

Key Insights for Industry Professionals:

- Market Value 2025: USD 8.9 Billion | 2034: USD 13.2 Billion | CAGR: 4.5%

- Energy efficiency: Triple-pane and Low-E coatings are mandated under stricter codes.

- Renovation focus: 60%+ sales in the DACH region tied to retrofit projects.

- Smart windows: Electrochromic glass adoption accelerating for intelligent building control.

- Noise reduction: Laminated glass and advanced seals gaining demand in urban areas.

- Policy drivers: Renovation incentives and tariffs shaping regional cost dynamics.

Market Analysis: Recent Strategic Developments in the Commercial Windows Industry

The commercial windows industry in 2025 is undergoing transformation shaped by policy changes, regional pressures, and technological advancements.

In August 2025, a regional analysis highlighted that the DACH commercial windows market is under pressure with a slight decline projected, but the renovation segment remains resilient as lower financing and material costs are expected to drive recovery. The same month, Optiemus Infracom inaugurated a ₹870 crore tempered glass plant in Noida, strengthening India’s local glass production capacity. Meanwhile, Klöckner Pentaplast received a German Packaging Award, reflecting leadership in circular material innovation though packaging-focused, it signals broader recognition of sustainability achievements across the glass value chain.

Tariff policy also impacted the market. In April 2025, the U.S. imposed a 10% baseline tariff on imported building materials, increasing input costs for window manufacturers and pressuring margins. By March 2025, M&T Glass reported a trend toward minimalist frames and larger glass panels, driven by architectural preferences for natural light integration in commercial buildings. In February 2025, reports highlighted that renovation across Germany, Austria, and Switzerland would accelerate with easing costs, reinforcing the retrofit opportunity.

Notably, in January 2025, the merger between Smurfit Kappa and WestRock reshaped the global packaging industry, creating ripple effects in supply chains and cross-sector material innovation. Separately, Huhtamaki secured its fifth EcoVadis Gold Medal in July 2025, underscoring the broader corporate momentum toward sustainability. While not direct window producers, these developments illustrate the interconnected supply chain dynamics where sustainability and cost optimization shape availability of raw materials.

Driving Trends and Emerging Opportunities in the Commercial Windows Market

Integration of Smart Glass and Dynamic Glazing Technologies

The commercial windows market is rapidly evolving from traditional high-performance solutions to dynamic glazing systems capable of electronically adjusting their tint. Smart glass is no longer a luxury addition but a core component of building energy management systems, driven by corporate sustainability initiatives and regulatory benchmarks. The U.S. Department of Energy (DOE) reports that electrochromic windows can reduce building energy consumption by up to 20% by controlling solar heat gain and daylighting, directly mitigating operational carbon emissions. Saint-Gobain’s SAGE Electrochromics has demonstrated real-world energy savings in corporate and educational buildings, including the University of Colorado Boulder's LEED Platinum-certified SEEC facility, where smart glass optimizes indoor lighting and reduces HVAC loads. Software integration, exemplified by J2 Innovations’ SageGlass Maestro®, enables dynamic window control via building sensors and orientation data, highlighting the convergence of fenestration with building automation systems. Regulatory incentives, such as the International Energy Conservation Code (IECC) and ASHRAE Standard 90.1, continue to set rigorous energy performance requirements, further accelerating smart glass adoption in commercial constructions.

Regulatory Push for Operational Carbon Reduction and Whole-Life Carbon Assessments

Government policies are increasingly mandating reductions in both operational and embodied carbon of buildings, pushing the commercial windows market toward low-carbon materials and processes. The European Union’s “Fit for 55” program and revised Energy Performance of Buildings Directive (EPBD) set ambitious targets for energy efficiency and zero-emission building stock by 2050. In the U.S., “Buy Clean” laws in California, New York, and Washington require manufacturers to disclose embodied carbon for materials in public projects, creating financial incentives for low-carbon window solutions. The International Energy Agency (IEA) recommends zero-carbon-ready codes for all commercial buildings by 2030, emphasizing global alignment toward net-zero emissions. Additionally, the U.S. Inflation Reduction Act (IRA) provides grants and funding for adopting updated building codes, reinforcing regulatory and financial drivers for energy-efficient window technologies.

Development of Highly Insulating, Thin-Profile Triple-Glazed Units for Retrofits

The retrofit segment represents a critical growth opportunity for manufacturers offering thin-profile, triple-glazed insulating glass units (IGUs). Traditional triple-glazed units are often too thick and heavy for existing frames, requiring costly structural modifications. Slim-profile solutions, such as Pilkington Spacia™ vacuum insulated glass (VIG), achieve the thermal performance of triple glazing while fitting within standard frame dimensions. Financing mechanisms like Commercial Property Assessed Clean Energy (C-PACE) programs make retrofits financially viable by covering up to 100% of upfront costs, with repayment via property tax assessments. By addressing both structural and financial barriers, thin-profile triple glazing enables deep energy retrofits without compromising architectural aesthetics or operational efficiency.

Standardized Integration of Building-Integrated Photovoltaics (BIPV) in Windows

Building-integrated photovoltaics (BIPV) represent a transformative opportunity by converting the building envelope into a power-generating surface. Transparent and semi-transparent photovoltaic technologies can be incorporated into vision glass, spandrel glass, or window frames, merging energy generation with fenestration. Ubiquitous Energy, a leading transparent solar technology provider, secured $30 million in Series B funding to scale U.S. production and deploy BIPV solutions in commercial facilities. Early installations demonstrate the dual functionality of electricity generation and daylighting while maintaining transparency. Federal and state-level incentives, alongside EU EPBD regulations mandating solar energy integration from 2027, further drive BIPV adoption. This market segment offers significant growth potential for window manufacturers and glass processors, aligning sustainability, energy efficiency, and regulatory compliance.

Competitive Landscape: Leading Companies in the Commercial Windows Market

The Global Commercial Windows Market is characterized by established leaders leveraging material science, energy efficiency innovation, and sustainability to defend market share.

Pella Corporation: Strength in Fiberglass and Customization

Pella is a recognized leader in aluminum, fiberglass, and wood windows for commercial applications. Its proprietary Impervia fiberglass series combines strength, energy efficiency, and durability, making it a preferred choice for institutional and office projects. Pella’s strategic focus is on developing high-performance windows that integrate security and aesthetic flexibility. The company’s core strength lies in its ability to customize finishes, grilles, and hardware, catering to diverse architectural requirements.

Andersen Corporation: Driving Sustainable Window Innovation

Andersen offers a broad commercial portfolio for high-rises, hospitals, and educational facilities. Its Eco-Friendly window series, developed with high recycled content, positions Andersen as a sustainability innovator. The company is actively investing in lightweighting and advanced materials to reduce environmental impact while maintaining premium performance. Andersen’s commercial windows are deployed in both new construction and large-scale renovation projects, reinforcing its cross-segment relevance.

YKK AP America Inc.: Aluminum Expertise with Thermo-Break Technology

YKK AP specializes in aluminum windows, curtain walls, and entrances for commercial buildings. A notable strength is its thermo-break technology, which significantly reduces heat transfer, aligning with stricter U.S. and EU energy codes. YKK AP’s focus is on delivering durable, energy-efficient architectural solutions tailored to offices, schools, and retail spaces. Its reputation for design flexibility and long lifecycle performance makes it a trusted partner for architects and contractors.

Kawneer Company, Inc.: Thermal Framing Systems for Energy Compliance

Kawneer is a major provider of architectural aluminum products, with a strong footprint in curtain walls, windows, and storefronts. Its innovation pipeline includes the Trifab® VG thermal framing system, engineered to meet the highest energy performance standards through advanced thermal break technology. Kawneer’s strategy is to integrate sustainability with architectural design goals, making it a go-to brand for energy-conscious commercial developers.

Vitro Architectural Glass: Leadership in Low-E and Solar Control Glass

Vitro (formerly PPG Glass) is a global leader in architectural glass manufacturing. Its flagship Solarban® and Sungate® series offer superior solar control and low-emissivity properties, directly reducing energy costs for commercial facilities. Vitro’s glass processing technologies are among the most advanced, allowing for custom solutions that balance aesthetics with performance. Its ability to meet the strictest regulatory and architectural requirements positions it at the forefront of the smart and sustainable window revolution.

Commercial Windows Market Share Insights

Double-Pane Leads Market Share by Glazing Type in Commercial Windows Industry

Double-pane glazing holds a commanding 72% share of the commercial windows industry, reflecting its position as the cost-optimal solution for balancing thermal insulation, acoustic control, and affordability. This dominance is primarily driven by regulatory compliance: in most major markets, double-pane is the minimum acceptable standard for meeting building energy codes. Its widespread use across office complexes, retail outlets, and mixed-use developments underscores its role as the “new normal” for developers balancing upfront construction budgets with energy performance targets. While triple-pane is gaining traction in high-performance projects, double-pane remains the preferred option for large-scale commercial builds, as it achieves significant energy efficiency improvements at a fraction of the cost of advanced glazing systems. This entrenched role secures double-pane as the workhorse of commercial fenestration.

Commercial Buildings Secure Market Share by End-Use in Commercial Windows Industry

Commercial buildings dominate end-use demand with 55% of the commercial windows market, making this segment the largest consumer of fenestration solutions. The sheer scale of office towers, shopping malls, and retail developments ensures commercial projects represent the bulk of installed volume, while their sensitivity to both upfront cost and operational efficiency positions double-pane glazing as the default choice. Tenant expectations for natural light, improved indoor comfort, and reduced utility bills reinforce developer decisions to prioritize window performance in this sector. Additionally, green building certifications such as LEED and BREEAM, often pursued in commercial developments, are pushing adoption of higher-performing fenestration systems, particularly in premium office spaces. As urbanization accelerates in emerging economies, the demand from commercial buildings will remain the dominant engine of growth, shaping the innovation trajectory for glazing and framing technologies.

United States: Energy Efficiency Mandates and Smart Window Technologies Fuel Market Growth

The commercial windows market in the United States is undergoing significant transformation, driven by evolving regulations and the growing demand for energy-efficient building materials. States such as New York are enforcing strict building energy codes that mandate U-factors of 0.32 or less for windows in certain climate zones, pushing manufacturers toward high-performance glazing systems. The U.S. Environmental Protection Agency’s ENERGY STAR program is further accelerating adoption, with certified windows meeting rigorous thermal and solar performance criteria. In addition, the Inflation Reduction Act of 2022 provides tax credits of up to $3,200 annually for energy-efficient upgrades, directly benefiting the commercial sector through retrofit and modernization projects.

Technological innovation is reshaping the U.S. commercial windows market, with growing use of smart glass, advanced low-E coatings, and multi-pane systems that enhance thermal insulation, daylighting, and security. Federal agencies, including the Department of Energy, are funding R&D for next-generation fenestration systems integrated with smart building management technologies. Demand is particularly strong in commercial retrofits and new construction for institutional buildings such as hospitals, schools, and LEED-certified projects. A growing trend of urban retrofits, replacing outdated windows with advanced solutions, is further boosting demand, underscoring the U.S. position as a leader in sustainable and intelligent window technologies.

Germany: Stringent EU Standards and Circular Economy Principles Shaping Market Dynamics

Germany’s commercial windows market is strongly influenced by European Union policies and national sustainability goals. The introduction of the EU Energy Performance of Buildings Directive (EPBD) and other climate-focused regulations require windows with exceptional insulation and recyclability, pushing German manufacturers to the forefront of energy-efficient design. The country’s emphasis on a circular economy, reinforced by the Verpackungsgesetz (Packaging Act) and similar producer responsibility frameworks, ensures that materials used in fenestration must be recyclable and compliant with long-term sustainability goals.

German window manufacturers are innovating with triple glazing, vacuum-insulated glass, and advanced frame technologies to meet stringent energy standards. The EU’s 2030 targets for carbon reduction and full recyclability of building components directly impact the commercial windows sector. In addition, Germany’s leadership in green building certifications, such as DGNB (German Sustainable Building Council), is creating strong demand for windows that align with high-performance construction and retrofit projects across offices, business centers, and institutional buildings.

China: Dual Carbon Goals and Smart City Development Driving Window Innovation

China’s commercial windows market is expanding rapidly under the government’s “dual carbon” initiative, which aims for carbon peak and neutrality. Regulations encourage the use of eco-friendly construction materials, leading to rising demand for high-performance, energy-efficient windows. As urbanization accelerates, commercial projects in smart cities are increasingly incorporating advanced fenestration systems with integrated sensors, automated shading, and building automation compatibility.

Chinese manufacturers are leveraging automation, artificial intelligence, and “5G plus industrial internet” technologies to optimize production efficiency and scalability. The Made in China 2025 plan emphasizes localization of high-tech manufacturing, ensuring more domestic production of advanced glazing materials. In addition, government regulations restricting non-sustainable construction inputs are pushing the adoption of recyclable and high-performance laminates. These developments, paired with the rise of smart buildings and sustainable city planning, make China a hotspot for commercial window innovation and mass adoption.

India: Urbanization, Infrastructure Expansion, and Green Building Codes Boost Demand

India’s commercial windows market is being propelled by large-scale government initiatives and rapid urban growth. The “Make in India” and “Zero Effect Zero Defect” programs promote quality domestic production of construction materials, while rapid urbanization has created strong demand for windows in IT parks, office complexes, and mixed-use commercial buildings. The country’s regulatory landscape, including updated Energy Conservation Building Codes (ECBC), emphasizes high-performance fenestration to reduce cooling loads and improve building efficiency.

The surge in infrastructure projects, coupled with the expansion of pharmaceutical, healthcare, and service industries, is generating strong demand for durable, tamper-resistant, and energy-efficient windows. Rapid urban retrofits are also emerging as developers replace outdated fenestration systems to meet modern energy standards. Rising disposable incomes and the push for green-certified commercial projects are further expanding opportunities. Together, these factors position India as one of the fastest-growing markets for commercial windows, with a focus on combining affordability, sustainability, and performance.

Brazil: Sustainability Regulations and Smart Building Investments Driving Window Market Growth

Brazil’s commercial windows market is evolving under strong sustainability mandates and regulatory frameworks. The National Energy Efficiency Policy and urban building codes encourage the adoption of energy-saving windows to reduce cooling loads in commercial spaces. The country’s emphasis on a circular economy, supported by its National Solid Waste Policy, is indirectly influencing fenestration design through sustainability-driven construction standards.

Technological adoption is reshaping Brazil’s construction sector, with robotics and AI increasingly used in building component manufacturing, including windows. The National Agency of Sanitary Surveillance (ANVISA) has enforced stringent traceability requirements for construction materials used in sensitive industries, indirectly supporting the demand for high-quality commercial windows. Investment in new commercial infrastructure, combined with rising adoption of sustainable and energy-efficient materials, highlights Brazil’s transition toward modern, eco-conscious fenestration solutions.

Japan: Seismic Resilience and Bio-Based Materials Redefining Commercial Windows

Japan’s commercial windows market is characterized by advanced material innovation and the need for seismic resilience in building design. The Containers and Packaging Recycling Law and broader sustainability frameworks have fostered a culture of recycling and bio-based material adoption, extending into construction materials such as window frames and glass coatings. Japan is also transitioning toward bio-based inputs, with companies exploring sustainable polymers and resins for window components.

Innovation in functionality is central to the Japanese market. Windows are designed with properties such as dimensional stability, resistance to deformation, and enhanced thermal insulation to meet the requirements of high-performance commercial buildings. Given Japan’s seismic risks, commercial windows are engineered with earthquake resilience, ensuring structural safety while maintaining performance. The combination of regulatory rigor, advanced recycling systems, and functional innovation makes Japan a leader in sustainable and disaster-ready commercial window solutions.

Commercial Windows Market Report Scope

Commercial Windows Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.9 Billion

|

|

Market Size (2034)

|

$13.2 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Material Type (Aluminum, Wood, Plastic/uPVC, Metal, Fiberglass, Composite), By Glazing Type (Single-pane, Double-pane, Triple-pane), By Product Type (Sliding Windows, Casement Windows, Awning Windows, Fixed Windows, Other Window Types), By End-Use (Commercial Buildings, Institutional Buildings, Industrial Facilities, Hospitality)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

JELD-WEN Holding, Inc., Andersen Corporation, Pella Corporation, Fenesta Building Systems, Masco Corporation, VELUX Group, Aluplast GmbH, REHAU AG + Co, SCHOTT AG, The Kawneer Company, Inc., YKK AP Inc., Deceuninck N.V., Veka AG, LIXIL Group Corporation, OKNA Designs

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Commercial Windows Market Segmentation

By Material Type

- Aluminum

- Wood

- Plastic/uPVC

- Metal

- Fiberglass

- Composite

By Glazing Type

- Single-pane

- Double-pane

- Triple-pane

By Product Type

- Sliding Windows

- Casement Windows

- Awning Windows

- Fixed Windows

- Other Window Types

By End-Use

- Commercial Buildings

- Institutional Buildings

- Industrial Facilities

- Hospitality

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Commercial Windows Market

- JELD-WEN Holding, Inc.

- Andersen Corporation

- Pella Corporation

- Fenesta Building Systems

- Masco Corporation

- VELUX Group

- Aluplast GmbH

- REHAU AG + Co

- SCHOTT AG

- The Kawneer Company, Inc.

- YKK AP Inc.

- Deceuninck N.V.

- Veka AG

- LIXIL Group Corporation

- OKNA Designs

* List Not Exhaustive

Methodology

USDAnalytics conducted a rigorous, multi-layered research methodology to deliver an authoritative analysis of the global Commercial Windows Market. The study combined primary research, including interviews with manufacturers, architects, commercial building developers, and facility managers, with secondary research covering regulatory codes, energy efficiency mandates, smart window innovations, and industry publications. Market sizing, trends, and forecasts were derived from historical data, retrofit demand analysis, smart glass adoption rates, and regional building regulations in key markets such as the U.S., Germany, China, India, Brazil, and Japan. Segmentation was performed by material type (aluminum, wood, uPVC, fiberglass, composite), glazing type (single, double, triple-pane), product type (sliding, casement, awning, fixed), and end-use applications (commercial, institutional, industrial, hospitality). Competitive intelligence on leading companies like Pella Corporation, Andersen Corporation, YKK AP America, Kawneer, and Vitro Architectural Glass was analyzed to evaluate strategies in sustainability, energy-efficient technology, and smart building integration. By integrating regulatory drivers, technological innovations, and retrofit dynamics, USDAnalytics provides actionable insights for industry professionals seeking strategic guidance, procurement intelligence, and market expansion opportunities.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.