Market Overview: Global Compostable Multilayer Films Industry Growth Outlook

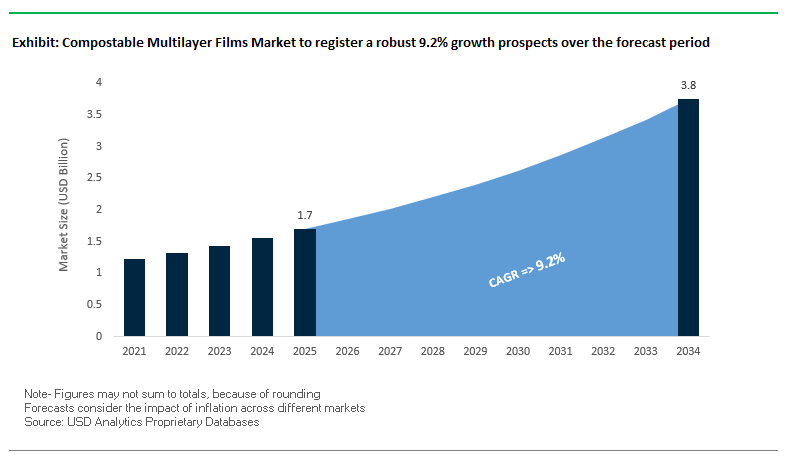

The Global Compostable Multilayer Films Market is projected to reach USD 1.7 billion in 2025 and expand to USD 3.8 billion by 2034, registering a robust CAGR of 9.2% during the forecast period. The market is gaining traction as industries accelerate their shift from fossil fuel–based plastics to certified biodegradable alternatives. Industrial compostability, verified through standards such as ASTM D6400 and EN 13432, is a critical benchmark ensuring that films biodegrade under controlled composting conditions without leaving harmful residues.

Key performance drivers include the dominance of Polylactic Acid (PLA) as a base polymer, known for its clarity and ability to combine with other biopolymers for superior barrier properties. Advancements in biopolymer blending are enabling compostable multilayer films to rival conventional plastics in protecting sensitive food categories such as snacks, bakery items, and fresh produce. At the same time, paper-based composite films with compostable inner layers are revolutionizing applications such as coffee pouches and snack packaging, aligning recyclability with sustainability.

Key Insights for Industry Professionals:

- Industrial compostability certifications (ASTM D6400, EN 13432) remain a decisive factor for adoption.

- PLA-based multilayer films dominate due to cost-effectiveness and superior clarity.

- Paper-composite films are a rising trend, combining recyclability and barrier performance.

- Food packaging applications (snacks, baked goods, fresh produce) remain the largest demand driver.

- Innovation in barrier properties is closing the performance gap with conventional plastics.

Market Analysis: Recent Strategic Developments in Compostable Multilayer Films

The market is highly dynamic, with continuous innovations and strategic moves from leading players. In September 2025, Mondi Group introduced its FunctionalBarrier Paper Ultimate, an ultra-high barrier paper-based solution, signaling a strong industry push toward paperization. Similarly, Cortec launched its Eco Works 100 film in August 2025, containing 100% USDA-certified bio-based content and designed for industrial compostability.

Graphic Packaging International advanced fiber-based innovation in August 2025 with child-resistant detergent pod packaging, further broadening the scope of compostable packaging applications beyond food. Around the same time, Amcor rolled out the Hector CRC closure, integrating PCR plastics into sustainable design. On the investment side, Futamura announced a £15 million expansion in June 2025 at its UK site to cut emissions and boost performance, reflecting the industry's deep commitment to circular economy principles.

Start-ups and innovators are also reshaping the market. The Lignin Industries secured €3.9 million in May 2025 to scale its tree-based thermoplastic, aiming to replace fossil polymers. Earlier in February 2025, TIPA launched a home-compostable metallized high-barrier film for snacks, solving a major barrier to sustainable snack packaging. Brand adoption is also accelerating: Australian skincare brand Conserving Beauty selected Futamura’s NatureFlex™ in January 2025, while Soy Silvestre in Chile moved to compostable packs in September 2024 for its liquid wheatgrass shots. Furthermore, Dow’s December 2024 acquisition of Circulus strengthens its circular packaging pipeline.

These developments demonstrate a clear trajectory toward bio-based content expansion, investments in scaling sustainable production, and increasing brand adoption, reflecting how regulatory pressure and consumer demand are converging to reshape the compostable multilayer films market.

Key Trends and Emerging Opportunities Shaping the Compostable Multilayer Films Market

Material Innovation Focused on High-Barrier, Home-Compostable Performance

The compostable multilayer films market is undergoing significant innovation with a focus on high-barrier, home-compostable films. Traditionally, the challenge has been matching the oxygen, moisture, and aroma barrier properties of conventional plastics while achieving certification for home compostability, eliminating the need for industrial composting facilities. Companies like TIPA have introduced ultra-thin, metallized high-barrier films for snack packaging that combine excellent barrier protection with home compostable credentials, proving that performance and sustainability can coexist. Collaborative efforts by Biome Bioplastics and Futamura have created bio-based films compliant with EN13432, demonstrating strong oxygen and moisture resistance for dry food packaging. Academic research also supports this trend, exploring cellulose-based films with advanced coatings to enhance barrier properties while remaining compostable. This development addresses a major infrastructure gap, offering sustainable solutions for consumers lacking access to industrial composting facilities and enabling broader adoption across the food and e-commerce packaging markets.

Regulatory-Driven Shift Mandating Compostable Packaging for Specific Applications

Government regulations, particularly in the European Union, are increasingly mandating compostable packaging for hard-to-recycle items such as tea bags, coffee pods, and fresh produce packaging. The EU Packaging and Packaging Waste Regulation (2024) bans certain single-use plastics and mandates recyclability by 2030, with specific requirements for industrial compostability by 2028 for certain applications. This regulatory environment creates a strong adoption pull for compostable multilayer films, compelling brands to reformulate packaging for compliance. The focus on specific applications mitigates contamination issues in recycling streams caused by food-soiled plastics, promoting the circular economy. The regulation sends a clear market signal that compostable films are no longer optional, driving R&D investment, process retooling, and strategic collaboration across the value chain.

Development of Certified Home-Compostable Films for E-commerce Fresh Food Delivery

The growth of online grocery and meal-kit delivery has generated substantial flexible packaging waste, creating a high-value opportunity for home-compostable multilayer films. These films offer a sustainable alternative for packaging produce, meat, and meal kits, aligning with consumer sustainability expectations. Companies like KM Packaging have launched clear, stretchy, and sticky home-compostable cling films designed for industrial and catering use, suitable for wrapping fruits and vegetables in e-commerce applications. This segment presents a rapid growth avenue, particularly in urban markets where access to recycling or industrial composting is limited. Home-compostable packaging enhances consumer convenience and environmental impact, while fostering collaboration between material scientists, manufacturers, and online retailers to create circular solutions.

Scaling of PHA Production to Reduce Reliance on PLA and Lower Material Costs

Polyhydroxyalkanoates (PHAs) are emerging as a superior alternative to PLA, offering enhanced flexibility, barrier performance, and marine biodegradability. The high cost and brittleness of PLA have limited its broader adoption, whereas PHA production scaling promises to deliver cost-competitive, high-performance compostable films. Research is focusing on low-cost fermentation substrates, including agricultural residues and food waste, to reduce production costs, making PHA commercially viable. Global investment is supporting expanded fermentation capacity and improved yields, positioning PHA-based films as a sustainable and scalable solution. This presents a key growth opportunity for the compostable multilayer films market, enabling widespread adoption in food packaging, e-commerce, and consumer goods, while meeting evolving regulatory and sustainability demands.

Competitive Landscape: Leading Companies in Compostable Multilayer Films Market

The compostable multilayer films industry is moderately consolidated, with a mix of specialized biopolymer producers and large packaging multinationals competing on innovation, certifications, and sustainability strategies.

TIPA Corp Ltd. focuses on high-barrier compostable snack packaging

TIPA stands out as a leader in customizable biodegradable films and laminates for food, fashion, and consumer goods. In February 2025, it launched a metallized home-compostable high-barrier film targeting snack applications, a key breakthrough for scaling compostable packaging. TIPA emphasizes certified home and industrial composting solutions and positions itself as a frontrunner in addressing plastic waste through end-of-life circularity.

Futamura Chemical Co., Ltd. invests in cellulose film capacity expansion

Futamura is renowned for its NatureFlex™ cellulose films, widely adopted in food packaging. The company announced a £15 million sustainability-focused investment in June 2025 at its UK facility, underscoring its commitment to efficiency and emissions reduction. With expertise in renewable cellulose films and strong brand credibility, Futamura is a partner of choice for global brands transitioning away from conventional plastics.

Amcor PLC leverages global scale for sustainable innovation

Amcor is a global giant in packaging, actively integrating sustainability into its operations. Its July 2025 launch of the Hector CRC closure aligns with its 2025 target of making all packaging recyclable, compostable, or reusable. With strong expertise in multilayer film technology and a vast international presence, Amcor’s key advantage lies in delivering scalable and compliant packaging solutions across healthcare, food, and consumer goods sectors.

Mondi Group leads the paperization trend in flexible packaging

In September 2025, Mondi launched its FunctionalBarrier Paper Ultimate, underscoring its strategy to shift towards recyclable and compostable fiber-based packaging. With 87% of its portfolio already recyclable or compostable by 2024, Mondi’s membership in the 4evergreen alliance further strengthens its role in advancing fiber packaging recyclability at scale.

Ahlstrom accelerates innovation in fiber-based laminates

Ahlstrom launched a new base paper in March 2025 under its LamiBak portfolio, aimed at flexible food packaging. Its core strength lies in deep expertise in fiber-based solutions and a global footprint. The company is pushing forward with continuous improvements in safety, performance, and sustainability, expanding its role in composite packaging development.

Danimer Scientific expands PHA-based solutions post-acquisition

Danimer Scientific specializes in PHA-based biopolymers, particularly its marine-biodegradable Nodax PHA. In March 2025, Teknor Apex acquired Danimer, enhancing its sustainable materials portfolio. Danimer’s competitive edge lies in producing bioplastics that can biodegrade in diverse environments, expanding the market’s potential beyond industrial compostability.

Compostable Multilayer Films Market Share Insights

PLA Leads Market Share by Material Type in Compostable Multilayer Films

Polylactic Acid (PLA) secures the largest share at 40% in the compostable multilayer films industry, positioning itself as the performance benchmark among bio-based materials. PLA’s dominance is attributed to its excellent clarity, stiffness, and aroma barrier properties, which closely replicate conventional plastics such as PET and OPP while maintaining compostability. Its ability to run seamlessly on existing extrusion and film-processing lines makes it highly scalable for packaging manufacturers, reducing the barrier to adoption compared to niche polymers. Starch-based films, with a 25% share, play the role of cost-effective enablers, often blended with PLA to optimize both performance and economics. Meanwhile, PHA and cellulose-based films are carving out specialized positions by offering marine biodegradability and high gas permeability, respectively, making them indispensable for high-value applications such as fresh produce, sensitive foods, and premium consumer goods. A key market insight is that true competitiveness comes from co-extruded multilayer combinations for example, PLA for structural integrity combined with a thin PHA barrier layer for superior moisture resistance underscoring why PLA remains the anchor of this material segment.

Food Packaging Dominates Market Share by Application in Compostable Multilayer Films

Food packaging is the undisputed leader with a 75% share of compostable multilayer film applications, underscoring its critical role in replacing conventional plastic films in high-visibility, regulation-heavy sectors. The dominance of food stems from three converging factors: regulatory mandates on single-use plastic in retail and foodservice, consumer demand for sustainable packaging, and the technical necessity of barrier films to extend product shelf life. Applications range from fresh produce bags and bakery wraps to snack bar pouches and coffee laminates, where compostability enhances brand value while maintaining freshness. Personal care and agriculture represent meaningful secondary users, with personal care brands leveraging compostable sachets and wrappers as part of their premium “eco-conscious” positioning, while agriculture uses compostable multilayer films for mulch films, seed tapes, and fertilizer bags that degrade into the soil. Pharmaceuticals remain cautious adopters, limited mainly to secondary overwraps, but the potential for expansion exists as material innovation addresses regulatory hurdles. This distribution highlights how food remains the commercial anchor while other industries add diversification and margin growth.

United States Compostable Multilayer Films Market Driven by Regulatory Push and Technological Innovation

The U.S. compostable multilayer films market is strongly influenced by evolving state-level regulations. Maryland and Washington’s Extended Producer Responsibility (EPR) bills in May 2025 incentivize producers to adopt recyclable or compostable materials. California’s SB 54, enacted in 2024, mandates a 25% reduction in plastic packaging by 2032 and requires full recyclability or compostability by that year, fueling the demand for innovative multilayer films.

Technological advancements are a key growth driver, with research focusing on high-barrier films that preserve moisture and oxygen-sensitive food products. Bio-based polymers like Polylactic Acid (PLA), derived from cornstarch and sugarcane, are increasingly used, with enhancements in heat resistance and printability. Corporate investments are rising, driven by sustainability targets from initiatives like the U.S. Plastics Pact, which aims for 100% reusable, recyclable, or compostable packaging by 2025. Key applications span food packaging, retail, and food service, with e-commerce growth and heightened hygiene awareness post-pandemic boosting sales. Academic research from institutions like the Georgia Institute of Technology is also contributing, developing films combining chitin and cellulose for superior oxygen barriers.

Germany Compostable Multilayer Films Market Strengthened by Circular Economy Leadership and Technological Innovation

Germany’s compostable multilayer films market is guided by the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, mandating fully recyclable or reusable packaging by 2030. Specific applications, including fruit stickers and tea bags, must be compostable by 2028, creating opportunities for new product development. Germany’s Packaging Act (VerpackG) enforces producer responsibility for the entire life cycle of packaging, driving designs that are compatible with recycling streams and circular economy goals.

Technological innovation is focused on modern extrusion, printing, and converting machinery for sustainable materials, ensuring quality and traceability. Investments in R&D support the creation of advanced multilayer films, with digital product passports and watermarks improving material transparency and end-of-life disposal. The market is particularly strong in the food, beverage, and retail sectors, with growing demand for organic and fresh produce packaging. Corporate collaborations between film producers and brand owners further accelerate the adoption of customized, high-performance compostable solutions.

China Compostable Multilayer Films Market Expands Through Green Policies and Domestic Manufacturing

China’s government-driven “dual carbon” goal is catalyzing the compostable multilayer films market, promoting recycling and sustainable material use through the March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement.” Regulatory reforms include phased reduction and banning of non-degradable products, aligning domestic production with environmental priorities.

Technological advancements focus on automation, AI, and “5G plus industrial internet” integration to optimize production processes and enhance flexible manufacturing. A key trend is the domestic substitution of imported technology, with local companies expanding capacity to meet demand in circular and sustainable packaging. Key applications include rapid growth in e-commerce, fresh food, and food delivery industries, driven by government initiatives to curb over-packaging through a “whole-chain administration system on over-packaging.” Investments in research and development have positioned China as a leader in innovative, high-performance compostable multilayer films.

Brazil Compostable Multilayer Films Market Strengthened by Sustainable Manufacturing and Regulatory Support

Brazil’s compostable multilayer films market is shaped by the National Solid Waste Policy and laws promoting sustainability. A 2024 law bans single-use items and mandates fully compostable or recyclable packaging by 2030, significantly impacting industry practices. Advanced technologies, including robotics and AI, are improving efficiency, quality control, and defect detection. Innovations such as biodegradable films using carboxymethyl cellulose (CMC) from sugarcane bagasse are notable developments.

The food, beverage, and cosmetics sectors are major drivers, with Brazil’s expanding food processing industry fueling demand for technological solutions. Government decrees targeting 30% mandatory recycling this year and 50% by 2040 directly influence materials and product design. Corporate investments in machinery and sustainable technologies are increasing to meet demand for high-quality, circular economy-compliant compostable films.

India Compostable Multilayer Films Market Boosted by Government Initiatives and Corporate Partnerships

India’s compostable multilayer films market is supported by initiatives such as “Swachh Bharat Abhiyan” and plastic waste management rules, alongside the nationwide single-use plastic ban. These policies are driving demand for biodegradable and compostable packaging solutions. Companies are producing films derived from certified materials like cornstarch and other compostable biopolymers for both home and industrial composting applications.

Technological advancements include automated production systems and the development of plastic-free laminate-grade films suitable for lamination with paper and foil. Domestic market growth is fueled by the rapid expansion of e-commerce, food & beverage, and pharmaceutical sectors. Strategic partnerships, including the CIRCLE Alliance launched by Unilever, USAID, and EY in August 2024 with USD 21 million in funding, promote circular packaging initiatives in India, further accelerating the adoption of sustainable compostable multilayer films. Key applications include ready-to-drink beverages and processed foods, highlighting the increasing importance of eco-friendly packaging solutions in India’s food processing industry.

Compostable Multilayer Films Market Report Scope

Compostable Multilayer Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$3.8 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Material Type (Polylactic Acid, Polyhydroxyalkanoates, Starch-based Films, Cellulose-based Films, Other Materials), By Layer Type (2-Layer, 3-Layer, 5-Layer, 7-Layer, Others), By Application (Food Packaging, Non-Food Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Futamura Group, Novamont S.p.A., TIPA Compostable Packaging, Taghleef Industries LLC, Walki Group Oy, Billerud AB, Innovia Films, BASF SE, NatureWorks LLC, Suvjay Industries India LLP, Kingfa Sci. & Tech. Co., Ltd., Novolex, Mondi Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Compostable Multilayer Films Market Segmentation

By Material Type

- Polylactic Acid

- Polyhydroxyalkanoates

- Starch-based Films

- Cellulose-based Films

- Other Materials

By Layer Type

- 2-Layer

- 3-Layer

- 5-Layer

- 7-Layer

- Others

By Application

- Food Packaging

- Non-Food Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Compostable Multilayer Films Market

- Amcor plc

- Mondi Group

- Futamura Group

- Novamont S.p.A.

- TIPA Compostable Packaging

- Taghleef Industries LLC

- Walki Group Oy

- Billerud AB

- Innovia Films

- BASF SE

- NatureWorks LLC

- Suvjay Industries India LLP

- Kingfa Sci. & Tech. Co., Ltd.

- Novolex

- Mondi Group

* List Not Exhaustive

Methodology

The analysis presented in this report on the Compostable Multilayer Films Market has been compiled by USDAnalytics using a comprehensive and industry-focused research methodology designed for professionals and investors. Primary research involved in-depth interviews with key stakeholders, including biopolymer producers, packaging manufacturers, brand owners, and regulatory experts, to understand technological innovation, material adoption, and application-specific challenges. Secondary research encompassed an extensive review of company press releases, product launches, patent filings, government policies, sustainability initiatives, trade publications, and industry reports to identify trends in PLA, PHA, starch, and cellulose-based multilayer films. The methodology also examined regulatory frameworks, including ASTM D6400, EN 13432, and EU Packaging and Packaging Waste Regulations, alongside market drivers such as food packaging demand, e-commerce growth, and home-compostable innovations. Quantitative approaches, including market sizing, CAGR analysis, and material-application segmentation, were integrated with qualitative insights on corporate strategies, mergers, and circular economy initiatives. USDAnalytics further analyzed regional market dynamics across North America, Europe, Asia-Pacific, and Latin America, assessing policy impacts, local manufacturing expansion, and technological advancements in high-barrier, compostable films. By combining these insights, USDAnalytics provides a comprehensive, actionable, and forward-looking overview of market opportunities, material innovations, and strategic growth pathways for industry professionals navigating the evolving compostable multilayer films sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.