Market Overview: Mechanical, Thermal, and Lifecycle Advantages Accelerating Continuous Basalt Fiber Adoption in Structural & High-Temperature Composites

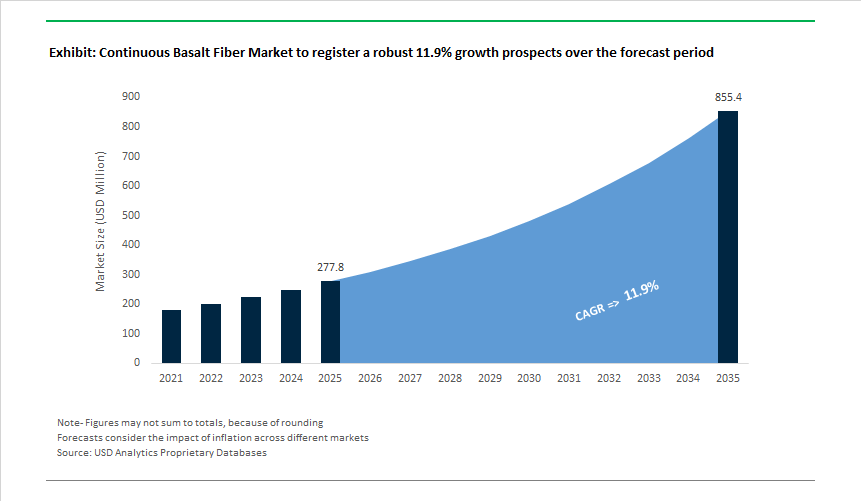

The Continuous Basalt Fiber (CBF) Market, valued at USD 277.8 million in 2025 and projected to reach USD 855.1 million by 2035 at a robust CAGR of 11.9%, is rapidly transitioning from a niche reinforcement material to a mainstream contender in civil, industrial, and high-temperature composite applications. Market momentum is driven by CBF’s mechanical superiority, high thermal resistance, natural corrosion immunity, and a highly competitive cost and sustainability profile compared with E-glass and carbon fiber. For seasoned procurement leaders and design engineers, CBF’s surging relevance aligns with long-term durability demands in infrastructure, stringent fire-performance requirements, and the rising need for cost-efficient, low-embodied-energy materials.

CBF delivers clear performance differentiation where traditional materials fall short. In reinforced concrete systems, BFRP rebars exceed 1,100 MPa in tensile strength, far surpassing conventional steel rebar (~375 MPa) and eliminating corrosion-the primary cause of structural failure in bridges, coastal assets, and municipal infrastructure. In high-temperature environments, CBF demonstrates thermal stability above 1,000°C, significantly outperforming E-glass (softening near 500°C) and enabling next-generation fire-resistant composites, thermal shields, and industrial insulation components. Its one-stage melting process, relying on low-cost basalt feedstock that constitutes <5% of production cost, provides compelling lifecycle economics while reducing embodied energy-an essential consideration for specifiers pursuing sustainable composites and low-carbon construction materials.

CBF's sectoral penetration is accelerating as industries align with durability, fire performance, and sustainability mandates. Early high-volume adoption is concentrated in civil infrastructure, driven by corrosion-free BFRP rebars and geogrids engineered for long service life. The material is also scaling in wind energy blades, marine laminates, CNG cylinder reinforcement, and high-temperature industrial components, while emerging opportunities are forming in EV battery thermal housings, EMI shielding hybrids, and pultruded structural systems.

Market Analysis: Capacity, Hybrid Innovations, and Regional Expansion Shape the Market Prospects

From October 2024 through December 2025, the Continuous Basalt Fiber market recorded a sequence of product launches, capacity investments, and R&D breakthroughs that are shaping near-term supply and application adoption. In October 2024, Kamenny Vek commissioned a production line for high-tex Direct Roving (22 μm, 2400 tex), a capability expansion targeted at pultrusion and filament-winding demand for wind-energy and industrial composites. Moving into May 2025, ISOMATEX rebranded its FILAVA product to TENRON, signaling a strategic push into high-performance defense and aerospace thermal-shield applications where elevated mechanical and chemical resistance is required. Also in May 2025, academic teams developed copper-deposited basalt fabrics for electrochemical CO₂ reduction, opening an environmental-energy applications vector that could materially broaden demand beyond structural uses.

The latter half of 2025 saw commercial scale and product diversification accelerate: in July 2025, Fiber Elements secured €2.6 million to scale their 3D basalt reinforcement technology, positioning CBF for complex industrial geometries and advanced structural composites. In September 2025, Roman Stone & Rock Fiber Inc. formed a U.S. partnership to introduce basalt-based MiniBars into the precast concrete market, directly addressing stormwater and utility infrastructure corrosion issues. November 2025 featured both R&D and capacity headlines: a European consortium announced AluBas tapes (CBF + aluminum hybrid) for EMI shielding and thermal management in EV battery enclosures, and Basalt Evotek LLC signed a $34 million investment to build a CBF plant in Kyrgyz Republic’s Chui Oblast-an explicit supply response to Central Asian and regional demand growth. Closing the period, December 2025 saw Arab Basalt Fibre Company launch next-gen basalt geogrids for mega-projects in the Middle East, underlining infrastructure uptake where coastal anti-corrosion and soil stabilization are mission-critical.

Continuous Basalt Fiber (CBF) Market Trends and Opportunities

Trend 1: Strategic Substitution of Fiberglass in Public Infrastructure

Public infrastructure owners and civil engineering firms are increasingly standardizing Continuous Basalt Fiber–Reinforced Polymer (BFRP) rebar and mesh as a long-life alternative to steel and conventional fiberglass reinforcement, driven by lifecycle economics rather than upfront material costs. Field data emerging through 2024–2025 confirms that basalt-based reinforcement delivers materially superior durability in aggressive environments where corrosion is the dominant failure mechanism. Peer-reviewed studies and recent coastal deployments show BFRP bars experiencing mass loss of under 1% after prolonged exposure to simulated marine conditions, while maintaining tensile strength retention above 98%. This contrasts sharply with traditional reinforcement systems, where corrosion-induced section loss and bond degradation accelerate maintenance cycles and shorten design life. As a result, infrastructure authorities in high-salinity regions such as coastal India, Southeast Asia, and Central America have begun large-scale pilots specifying BFRP for bridge decks, seawalls, and drainage systems. The mechanical performance profile of basalt fiber—tensile strengths exceeding 1,100 MPa combined with stable behavior under alkaline concrete pore solutions—allows engineers to design thinner concrete covers without sacrificing safety margins. Advanced pullout testing conducted in 2025 further demonstrates that when BFRP is paired with modern admixture systems such as metakaolin-enhanced concrete, bond stress can exceed that of steel reinforcement by up to 50%. This enables lower material volumes and delivers an estimated 15–20% reduction in embodied carbon per structure, aligning durability upgrades directly with public-sector decarbonization targets.

Trend 2: Vertical Integration of CBF for Automotive Thermal Management Systems

Automotive OEMs and Tier-1 suppliers are no longer treating Continuous Basalt Fiber as a commodity insulation input but are integrating it vertically into complete thermal and fire-protection architectures for electric and internal combustion platforms. This shift is being driven by the rapid escalation of thermal risk associated with fast-charging EV batteries and higher exhaust temperatures in downsized, turbocharged ICE systems. In 2025, multiple automotive suppliers began deploying modular basalt-fiber insulation assemblies designed to withstand sustained temperatures above 600°C, a threshold at which conventional glass fibers begin to soften and lose dimensional stability. These basalt-based systems act as passive fire barriers during thermal runaway events, buying critical response time and preventing heat propagation to adjacent battery cells or vehicle compartments. From a vehicle mass perspective, CBF-based shields and enclosures are typically 20–40% lighter than stamped metallic alternatives, directly supporting range extension targets where a 10% weight reduction can translate into a 6–8% efficiency gain. To secure supply at automotive scale, CBF producers are investing in vertically integrated facilities that convert raw volcanic basalt into rovings, fabrics, and finished insulation components within a single processing footprint. This integration reduces logistics complexity, improves quality consistency, and ensures availability of high-purity fiber for 800V-class electrical insulation and acoustic-thermal modules demanded by next-generation EV platforms.

Opportunity 1: Recognition of Basalt Fiber as a Strategic, Low-Carbon Material

Industrial policy is emerging as a powerful demand accelerator for the Continuous Basalt Fiber market as governments seek to de-risk advanced material supply chains while lowering embodied emissions. In 2025, basalt fiber gained increased visibility in strategic material assessments due to its unique combination of domestic raw material abundance and comparatively low energy intensity during production. Unlike carbon or E-glass fibers, basalt fiber is produced through direct melting without complex chemical inputs, resulting in materially lower process emissions. This positioning aligns closely with policy frameworks in North America and Europe that prioritize materials capable of supporting infrastructure resilience, energy transition, and national security objectives simultaneously. Under emerging low-carbon procurement rules and net-zero industry strategies, basalt fiber producers are becoming eligible for tax incentives, accelerated permitting, and public funding support aimed at domestic scaling. Late-2025 resilience and manufacturing grants in both North America and Asia-Pacific are increasingly earmarked for melt-furnace efficiency upgrades and capacity expansion, directly addressing one of the historical bottlenecks in CBF adoption: cost competitiveness at scale. As these policy mechanisms mature, basalt fiber is moving from an alternative material to a strategically preferred input for public works, transport, and defense-adjacent applications.

Opportunity 2: Fire-Resistant Composite Cores for Marine and Rail Platforms

Global tightening of fire, smoke, and toxicity regulations across marine and rail sectors is opening a high-value replacement market for Continuous Basalt Fiber–reinforced composite cores. Updated standards under the IMO FTP Code and EN 45545-2 are progressively eliminating flammable polymer foams and organic cores from passenger vessels, rolling stock, and interior structural panels. Basalt fiber composites offer a rare combination of non-combustibility, mechanical strength, and low toxicity under fire exposure, making them ideally suited for compliance-driven retrofits and new-build platforms. Fire testing published in 2024–2025 demonstrates that basalt fiber–reinforced polysiloxane and inorganic matrices exhibit near-zero heat release rates and exceptionally low carbon monoxide emissions, outperforming fiber cement boards and PET-based sandwich cores while delivering three to ten times higher flexural strength. Beyond fire performance, these systems also deliver superior durability in extreme service conditions. Basalt-reinforced panels have been shown to retain structural integrity after more than 300 freeze–thaw cycles, making them particularly attractive for ice-class vessels, coastal ferries, and high-speed rail cars operating in cold or high-humidity environments. As safety regulation increasingly converges with lifecycle durability requirements, fire-resistant basalt composite cores are positioned as a structural, not cosmetic, upgrade across mass transit and marine fleets.

Continuous Basalt Fiber Market Share Analysis

Market Share by Product Type: Basalt Fiber Roving Underpins Industrial-Scale Composite Manufacturing

Basalt fiber roving accounts for approximately 35% of total demand in the global Continuous Basalt Fiber Market, reflecting its role as the foundational input for high-volume, load-bearing composite applications. Roving dominates because it is the primary format required for pultrusion, filament winding, and automated composite manufacturing, where continuous reinforcement is essential for structural integrity and production efficiency. Compared with conventional E-glass fiber, basalt roving delivers a higher tensile strength profile, enabling manufacturers to design thinner and lighter composite components without compromising safety margins. This strength advantage, combined with a relatively high elastic modulus, allows composite structures to retain dimensional stability under sustained pressure—an increasingly important requirement in pressurized vessels, industrial piping, and infrastructure-related composites. Market share is further reinforced by basalt roving’s exceptional thermal stability, maintaining mechanical performance at temperatures far beyond the limits of fiberglass, which positions it as a preferred reinforcement in fire-exposed and high-temperature industrial environments. Chemical resistance also plays a decisive role, as basalt roving retains its strength in aggressive conditions such as saltwater, alkaline concrete matrices, and UV-intensive outdoor applications, significantly reducing lifecycle degradation compared to glass fiber alternatives. From a processing standpoint, single-end basalt roving integrates seamlessly into automated winding and pultrusion lines, supporting higher throughput and consistent quality in mass production. Collectively, these attributes position basalt fiber roving as the structural backbone of the continuous basalt fiber value chain, anchoring its leading market share as demand rises for durable, lightweight, and corrosion-resistant composite solutions.

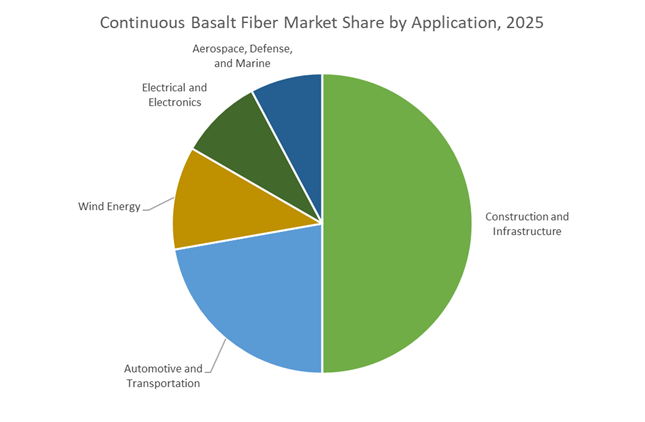

Market Share by Application: Construction and Infrastructure Drive Basalt Fiber Adoption at Scale

The construction and infrastructure segment commands roughly 45% of the Continuous Basalt Fiber Market, making it the largest and most strategically important application area. This dominance is driven by a global shift away from steel reinforcement toward Basalt Fiber Reinforced Polymer (BFRP) solutions that address corrosion, maintenance, and lifecycle cost challenges in concrete structures. Unlike steel rebar, which is susceptible to rust-induced failure, basalt reinforcement is inherently corrosion-proof, enabling projected service lives exceeding several decades without the need for costly repairs or protective coatings. Market adoption is further accelerated by basalt’s logistics and labor efficiency, as basalt rebar’s significantly lower weight reduces transportation costs and allows manual handling on construction sites, eliminating dependence on heavy lifting equipment. Thermal compatibility with concrete is another critical driver, as basalt’s near-identical coefficient of thermal expansion minimizes internal stresses and cracking during freeze–thaw cycles, a key requirement for bridges, marine structures, and cold-climate infrastructure. In modern green building projects, basalt fiber also supports energy-efficient construction by eliminating thermal bridges in building envelopes, directly contributing to compliance with high-performance building standards. Together, these structural, economic, and sustainability advantages make construction and infrastructure the primary engine of demand for continuous basalt fiber, firmly securing its leading share in the global market.

Competitive Landscape: Market Structure, Differentiation, and Company Positioning

The Continuous Basalt Fiber (CBF) competitive landscape is defined by a blend of high-volume producers in China and Russia, European advanced-material specialists, and emerging scale-up challengers focused on engineered composites. Market structure is increasingly shaped by differentiation around fiber tex/filament uniformity, high-tex direct rovings, application-specific reinforcements (woven/NCF fabrics, geogrids, prepregs), and hybrid material architectures that combine basalt with carbon, aramid, or metallic layers for enhanced multifunctionality. As CBF adoption expands across infrastructure, industrial, wind, and mobility applications, buyers are placing heightened emphasis on traceability, tight mechanical-property control, thermal/fire performance stability, and availability of composite-ready formats optimized for RTM, pultrusion, filament winding, vacuum infusion, and automated layup processes. The competitive edge is increasingly shifting toward suppliers capable of delivering validated application demonstrations (CNG cylinders, wind spar caps, precast concrete reinforcement) and global certification compliance, rather than commodity fiber outputs.

Kamenny Vek - High-Tex Continuous Rovings For Pultrusion, High-Pressure Vessels, and Industrial Composites

Kamenny Vek is recognized as one of the most technically advanced CBF producers globally, specializing in premium continuous basalt fiber rovings, including Direct Roving and Assembled Roving engineered for high-performance composite processes. Recent upgrades-such as 22 μm / 2400 tex high-tex rovings-strengthen its relevance in pultrusion, filament winding, and high-pressure CNG cylinder reinforcement. The company’s differentiation lies in exceptional filament uniformity, stable tensile characteristics, and a consistent quality profile that appeals to aerospace-grade and automotive composite programs with tight tolerance requirements. Kamenny Vek’s focus on industrial-grade high-tex offerings positions it strongly in infrastructure reinforcement, specialty insulation, and vibration-damping composite systems, where mechanical and dielectric properties are equally important.

Zhejiang GBF Basalt Fiber Co., Ltd. - High-Volume Chinese Producer Driving Cost-Competitive Construction and Industrial Substitution

Zhejiang GBF represents the high-volume, cost-advantaged segment of the global CBF industry, offering an extensive portfolio including roving, yarns, panels, bars, and structural elements. Its demonstrated applications in defense textiles, protective armor, and basalt-wrapped CNG cylinders highlight both scale and manufacturing breadth. GBF’s primary strategic positioning is its ability to displace E-glass across Asia-Pacific infrastructure and insulation markets through cost competitiveness, process scalability, and reliable bulk supply. As global construction sectors seek corrosion-free, longer-life reinforcement, GBF has become a central catalyst accelerating widespread migration from E-glass to basalt in civil engineering, industrial laminates, and thermal insulation solutions.

Basaltex NV - European Provider Of Premium Fabrics and Ncfs For Wind Energy, Marine, and High-Spec Composites

Basaltex stands out as a European specialist in engineered basalt reinforcements, offering woven fabrics, veils, and Non-Crimp Fabrics (NCFs) optimized for RTM, vacuum infusion, and infusion molding systems prevalent in wind-turbine blade and marine composite production. The company’s differentiation is anchored in European quality regimes, rigorous certification pathways, and long-standing collaborations with R&D institutes focused on high-performance composite architectures. Basaltex’s advanced hybrid research-combining basalt with carbon or aramid fibers-targets applications requiring balanced stiffness, enhanced vibration damping, and improved fatigue life, aligning with OEMs demanding traceability, predictable performance, and compliance with global composite standards.

ISOMATEX S.A. - TENRON High-Performance Fiber For Extreme Environments, Chemical Processing, and EV Thermal Shielding

ISOMATEX’s TENRON fiber line (formerly FILAVA) occupies the high-performance tier of the CBF market, designed specifically for extreme-environment durability and thermal resilience. Built on proprietary melting and fiberization processes, TENRON delivers superior mechanical strength, high-temperature stability, and outstanding acid/alkali resistance, enabling its use in chemical processing tanks, corrosive piping systems, defense components, and EV battery thermal shields. ISOMATEX’s strategy is to position itself away from commodity basalt fiber producers and toward sectors where material resilience, long service life, and regulatory compliance drive premium pricing. This premiumization approach has made TENRON a preferred option for OEMs seeking next-generation basalt solutions for harsh environments and thermal-protection applications.

China continues to anchor the global continuous basalt fiber (CBF) market through large-scale industrialization and vertically secured raw material supply. The country’s “New Materials” roadmap has enabled rapid expansion of basalt fiber filament capacity, positioning CBF as a cost-competitive and corrosion-resistant alternative to E-glass and steel reinforcements. Manufacturing hub expansions in Sichuan province illustrate how regional governments are aligning composite materials with automotive lightweighting and civil infrastructure resilience. Integration of basalt fiber reinforced polymer (BFRP) laminates into high-traffic highway bridges reflects China’s willingness to deploy basalt composites in mission-critical public works, validating long-term durability and load-bearing performance. Raw material security remains a decisive advantage; upstream expansion by China National Petroleum Corporation has stabilized access to high-grade volcanic rock, lowering fiber production costs and supporting downstream demand from wind energy and transport infrastructure. This combination of scale, deployment confidence, and feedstock control reinforces China’s dominance across the continuous basalt fiber value chain.

United Arab Emirates Building the Gulf’s First Integrated Basalt Fiber Ecosystem

The United Arab Emirates is rapidly emerging as the MENA region’s focal point for basalt fiber technology, driven by giga-project construction and sustainability mandates. The launch of a dedicated basalt fiber manufacturing base in Fujairah marks a strategic shift from imported reinforcements to localized production of continuous basalt fiber and BFRP rebar. This move aligns with the UAE’s broader low-carbon construction agenda, where non-corrosive and heat-resistant materials are critical for extreme climate infrastructure. Regional demand projections shared at major construction exhibitions indicate strong growth for value-added basalt products across Saudi Arabia and Egypt, particularly for megaprojects emphasizing lifecycle durability. By establishing early industrial capacity, the UAE is positioning itself as a regional exporter of basalt composites rather than a passive consumer.

United States Legislative Momentum Accelerating Non-Corrosive Infrastructure Adoption

In the United States, the continuous basalt fiber market is gaining structural momentum through updated building codes and federal research funding. The formal adoption of ACI 440.11-22 has lowered specification barriers for basalt FRP bars in public infrastructure, enabling wider use in bridges, coastal structures, and transportation assets where corrosion resistance is paramount. Parallel funding from the U.S. Department of Energy is expanding basalt fiber applications beyond construction into fire-resistant composites for EV battery enclosures and aerospace structures. Domestic producers such as Basanite Industries and American Basalt Company are expanding localized production to serve high-tech facilities that require non-conductive, electromagnetically neutral reinforcements. The U.S. market trajectory is defined by standards-driven adoption rather than volume pricing, favoring certified, infrastructure-grade basalt solutions.

Uzbekistan’s Export-Oriented Disruption Through Vertical Integration

Uzbekistan has positioned itself as a disruptive exporter in the global continuous basalt fiber market by modernizing furnace technologies and adopting a vertically integrated production model. Participation at global composites exhibitions has elevated the country’s visibility as a supplier of high-performance basalt fibers, fabrics, and geogrids. By controlling the entire value chain-from basalt rock extraction to finished composite intermediates-Uzbek producers are able to meet European sustainability and traceability expectations under the Green Deal framework. This export-centric strategy allows Uzbekistan to compete directly with established Russian and Chinese suppliers while emphasizing quality differentiation and treatment technologies rather than sheer scale.

Germany’s Lightweighting Innovation and Advanced Coating Leadership

Germany leads Europe’s innovation agenda in continuous basalt fiber through advanced coatings, hybrid materials, and automotive-grade composites. Strategic collaboration between Michelman and FibreCoat has resulted in aluminum-coated basalt fiber engineered for electromagnetic shielding, aerospace applications, and lightweight electronics enclosures. Concurrently, German research institutes are leveraging Horizon Europe “Cluster 4” funding to develop 3D-printed basalt structures for sustainable urban development. Germany’s role in the CBF market is defined less by volume production and more by high-value innovation that expands basalt fiber into premium industrial and mobility applications.

Russia’s Resource-Backed Capacity Expansion and Specialized Applications

Russia remains one of the world’s largest producers of continuous basalt fiber, benefiting from extensive volcanic reserves and deep metallurgical expertise. Capacity expansion at established producers has strengthened Russia’s position in direct roving and basalt fabric exports. Beyond construction and composites, research initiatives supported by the Russian Academy of Sciences are extending basalt fiber into functional applications, such as copper-deposited fabrics for electrochemical CO₂ reduction. This diversification underscores Russia’s strategy of leveraging natural resource advantages while pushing basalt fiber into environmental and energy-transition technologies.

National Strategic Development Matrix: Continuous Basalt Fiber Market (2025)

Continuous Basalt Fiber Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

Key Development Milestone

|

Core Application Focus

|

|

China

|

Industrial scale & raw material security

|

Expansion of filament workshops and BFRP bridge use

|

Infrastructure, automotive, wind energy

|

|

United Arab Emirates

|

Giga-projects & sustainability

|

Fujairah basalt fiber manufacturing base

|

Extreme climate infrastructure, BFRP rebar

|

|

United States

|

Building codes & resilient infrastructure

|

Adoption of ACI 440.11-22 and DOE funding

|

Bridges, EV enclosures, aerospace

|

|

Uzbekistan

|

Export competitiveness

|

Vertically integrated basalt fiber supply chain

|

EU Green Deal infrastructure

|

|

Germany

|

Lightweighting & advanced coatings

|

Aluminum-coated basalt fiber innovation

|

Aerospace, electronics, automotive

|

|

Russia

|

Natural reserves & capacity expansion

|

New roving and fabric production facilities

|

Construction, environmental technologies

|

Continuous Basalt Fiber Market Report Scope

Continuous Basalt Fiber Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$277.8 Million

|

|

Market Size (2035)

|

$855.1 Million

|

|

Market Growth Rate

|

11.9%

|

|

Segments

|

By Form (Roving, Chopped Strands, Woven Fabrics & Meshes, Non-Woven Materials, Felt), By Product Type (Continuous Basalt Fiber Products, Basalt Fiber Reinforced Polymer Products, Hybrid Composites), By Application (Construction & Infrastructure, Automotive & Transportation, Aerospace & Defense, Wind Energy, Electrical & Electronics, Marine), By Usage Type (Composite, Non-Composite)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kamenny Vek, Technobasalt-Invest LLC, Zhejiang GBF Basalt Fiber, Mafic SA, Jilin Tongxin Basalt Technology, Basaltex NV, Sudaglass Fiber Technology, Basalt Fiber Tech, ARMBASALT CJSC, Shanxi Basalt Fiber Technology, Fiberbas Construction Technologies, Incotelogy GmbH, Basanite Industries LLC, Jiangsu Tianlong Continuous Basalt Fiber

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Continuous Basalt Fiber Market Segmentation

By Form

- Roving

- Chopped Strands

- Woven Fabrics and Meshes

- Non-Woven Materials

- Felt

By Product Type

- Continuous Basalt Fiber

- Basalt Fiber Reinforced Polymer

- Basalt Fiber Reinforced Polymer Rebar

- Basalt Fiber Reinforced Polymer Profiles

- Basalt Fiber Reinforced Polymer Laminates

- Hybrid Composites

By Application

- Construction and Infrastructure

- Automotive and Transportation

- Aerospace and Defense

- Wind Energy

- Electrical and Electronics

- Marine

By Usage Type

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Continuous Basalt Fiber Market

- Kamenny Vek

- Technobasalt-Invest LLC

- Zhejiang GBF Basalt Fiber Co., Ltd.

- Mafic SA

- Jilin Tongxin Basalt Technology Co., Ltd.

- Basaltex NV

- Sudaglass Fiber Technology

- Basalt Fiber Tech

- ARMBASALT CJSC

- Shanxi Basalt Fiber Technology Co., Ltd.

- Fiberbas Construction and Building Technologies

- Incotelogy GmbH

- Basanite Industries LLC

- Jiangsu Tianlong Continuous Basalt Fiber Co., Ltd.

*- List not Exhaustive