Market Overview: High-Strength, Fire-Resistant Basalt Fiber Transforming Global Composite Engineering

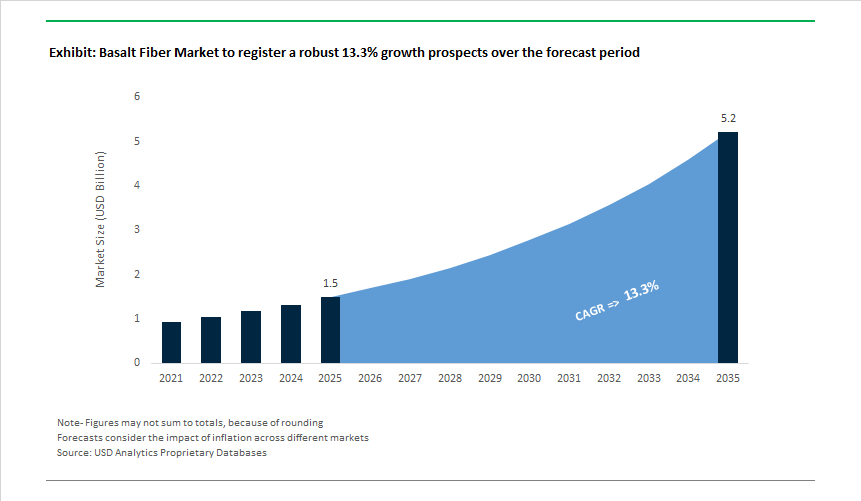

The Basalt Fiber Market (USD 1,549.2 million in 2025; projected to reach USD 5,400.2 million by 2035 at a 13.3% CAGR) is gaining strategic relevance as infrastructure owners, transportation OEMs, and industrial composite manufacturers prioritize materials that deliver longer service life, fire resistance, and corrosion immunity without cost escalation. Basalt fiber’s combination of high tensile strength, elevated thermal stability, and chemical inertness directly addresses failure modes that limit the lifespan of traditional E-glass and steel-reinforced systems, particularly in chloride-rich coastal infrastructure, high-temperature industrial environments, and lightweight mobility platforms.

Unlike conventional reinforcements, basalt fiber offers steel-like mechanical performance without corrosion risk and glass-fiber processability with materially higher thermal tolerance, enabling OEMs and civil engineers to reduce overdesign, extend maintenance cycles, and improve total lifecycle economics. In structural composites and reinforcement applications, basalt fiber-reinforced polymers (BFRP) are increasingly specified where durability under fire exposure, freeze-thaw cycling, and chemical attack outweighs initial material cost considerations. This shift is accelerating adoption across bridges, tunnels, marine structures, EV composite panels, wind turbine blades, and fire-resistant insulation systems.

Over the forecast period, market expansion will be driven less by raw material substitution and more by standards-driven adoption. Stricter fire safety codes, durability mandates for coastal and underground infrastructure, and sustainability-linked procurement policies are pushing engineers toward materials that deliver predictable long-term performance with lower embodied maintenance. Manufacturers that can supply consistent fiber quality, validated structural performance data, and scalable composite solutions - rather than commodity fibers - are positioned to capture disproportionate value as basalt fiber transitions from niche reinforcement to a mainstream engineering material.

Market Analysis: Capacity Expansions, Policy Support, and Composite Innovation Accelerating Growth

The global basalt fiber ecosystem witnessed a rapid escalation in technological upgrades, strategic partnerships, and composite material innovations between April 2025 and December 2025, demonstrating strong momentum across infrastructure, mobility, marine engineering, and renewable energy domains. In December 2025, a European composites manufacturer launched BFRP pultruded profiles optimized for high-speed rail systems, emphasizing basalt’s EMI immunity-a critical requirement in smart-rail modernization. Earlier in November 2025, Russia’s Kamenny Vek completed a furnace modernization to boost CBF roving output by 15%, increasing its supply reliability across Asia-Pacific’s fast-growing composites market. In October 2025, Basaltex entered a pivotal partnership with a leading shipbuilding engineering firm to deliver non-corrosive basalt fiber fabrics for marine hulls, aligning with stricter maritime corrosion standards.

The regulatory environment also shifted decisively in favor of basalt-based construction materials. In September 2025, a Chinese government agency introduced Green Building Material Standards promoting basalt fiber composites over traditional steel rebar in infrastructure renewal projects. This policy shift is expected to generate large-scale procurement opportunities for BFRP manufacturers, particularly in municipal applications. Growth momentum continued across new material formulations, with a U.S. composites startup in July 2025 unveiling a basalt/flax hybrid composite prepreg-a breakthrough that blended cost efficiency with comparable modulus performance to E-glass. In June 2025, Ukraine’s Technobasalt-Invest commissioned a dedicated line for Basalt Superfine Fiber mats, targeting cryogenic insulation markets where basalt's performance at -260°C provides a significant competitive advantage. Additionally, regional expansion progressed in April 2025, when Arab Basalt Fiber Company commenced construction of a major BFRP rebar facility supporting Middle East oil & gas infrastructure.

Basalt Fiber Market Trends and Opportunities

Automotive Qualification of Basalt Fiber for EV Thermal and NVH Systems

The electrification of vehicles has exposed a critical gap between lightweighting and safety, particularly around thermal runaway containment and NVH control in high-torque electric drivetrains. Basalt fiber is increasingly specified because it maintains mechanical integrity at temperatures where polymer housings, aluminum, and E-glass composites degrade.

In December 2025, next-generation solid-state battery packs co-developed by Welion and BASF were unveiled with basalt-compatible engineering plastics engineered to comply with GB 38031 fire and impact standards. These enclosures demonstrated ~50% weight reduction versus metal housings while delivering superior flame resistance—directly addressing EV safety certification bottlenecks.

Beyond fire protection, comparative studies conducted between 2024 and 2025 show that basalt fiber composites exhibit a 15–20% higher damping coefficient than E-glass, making them increasingly valuable in motor mounts, battery trays, and under-hood acoustic insulation. European Tier-1 suppliers are now leveraging this property to meet stricter NVH thresholds as electric drivetrains amplify high-frequency vibration. Basalt’s non-toxic behavior under combustion—no halogenated fumes or molten drip—has further positioned it as a preferred fiber for mass-transit EVs, autonomous shuttles, and rail platforms, where passenger safety certification is tightening.

Infrastructure Integration of BFRP for Seismic Retrofitting and Corrosion-Free Reinforcement

In civil engineering, basalt fiber reinforced polymer (BFRP) is rapidly gaining traction as a maintenance-free alternative to epoxy-coated and stainless steel rebar, particularly in seismic and corrosive environments. With tensile strengths routinely exceeding 1,000–1,100 MPa, BFRP offers high load capacity at a fraction of the weight, while eliminating chloride-induced corrosion.

A pivotal regulatory milestone was reached in 2025 when the German Institute for Construction Technology issued ETA-20/0599, certifying basalt reinforcement for a 50-year service life in concrete structures. This approval effectively unlocks EU-funded bridges, tunnels, and coastal infrastructure projects, where lifecycle cost and durability are now mandatory procurement criteria.

Seismic performance data released in April 2025 demonstrates that basalt fiber wrapping of beam–column joints delivers a ~25% increase in peak shear force and a ~20% improvement in displacement capacity, outperforming conventional retrofitting methods. As of January 2025, Digital Product Passports under EU Net-Zero rules further strengthen basalt’s position: project-level assessments show up to 85% CO₂-equivalent reduction versus steel when mass reduction and zero-corrosion maintenance are factored in. This positions basalt fiber as a cornerstone material for green, seismic-resilient urban infrastructure.

BFRP Pipelines and Liners for Corrosion-Proof Water Infrastructure

Government-led infrastructure renewal is creating a sustained demand environment for basalt fiber pipes, liners, and structural sleeves, particularly in water and wastewater networks where corrosion drives lifecycle costs. Europe alone faces the challenge of maintaining ~6.7 million kilometers of aging pipelines, with capital expenditure increasingly tied to material durability and embodied carbon.

Under European and North American “Buy Clean” frameworks, BFRP pipes are being specified because they are immune to alkaline attack, chlorides, and microbiologically induced corrosion. In trenchless rehabilitation projects, basalt fiber liners are proving particularly attractive: they are up to 4× lighter than steel, reducing transport emissions, crane requirements, and installation time.

In coastal and high-salinity regions, new 2025 technical specifications in the Middle East and Southeast Asia have pre-qualified BFRP as a structural material for seawater-exposed wastewater grids, where conventional reinforced concrete exhibits premature failure. This opportunity is driven not by novelty, but by predictable lifecycle economics—a critical differentiator as municipalities shift from lowest-cost procurement to total cost of ownership (TCO) models.

Mid-Span Reinforcement Opportunity in Next-Generation Wind Turbine Blades

As offshore wind turbines scale beyond 15 MW and blade lengths exceed 100 meters, the composite industry is reassessing its reliance on carbon fiber for mid-span reinforcement. Basalt fiber is emerging as a strategic middle-ground material—offering stiffness and fatigue resistance superior to glass, while avoiding the cost, supply concentration, and carbon intensity of carbon fiber.

Blade manufacturers are actively testing hybrid basalt–carbon spar caps, leveraging basalt’s UV stability and fatigue endurance in regions where carbon fiber is over-engineered. This material substitution is being accelerated by economics: 2025 carbon fiber tariffs (~25%) and anticipated CBAM surcharges of 8–12% are materially altering bill-of-material calculations. Basalt fiber, with lower energy intensity and regional producibility, is increasingly viewed as a price-stability hedge.

Investment patterns reinforce this shift. In January 2025, the Kyrgyz Republic signed a $34 million investment agreement with Basalt Evotek LLC to establish a continuous basalt fiber facility targeting European and Central Asian renewable energy markets. The focus on high-modulus fibers for wind and aerospace signals that basalt fiber is no longer confined to secondary reinforcement—it is moving decisively into performance-critical renewable energy components.

Market Share Analysis: Basalt Fiber Market

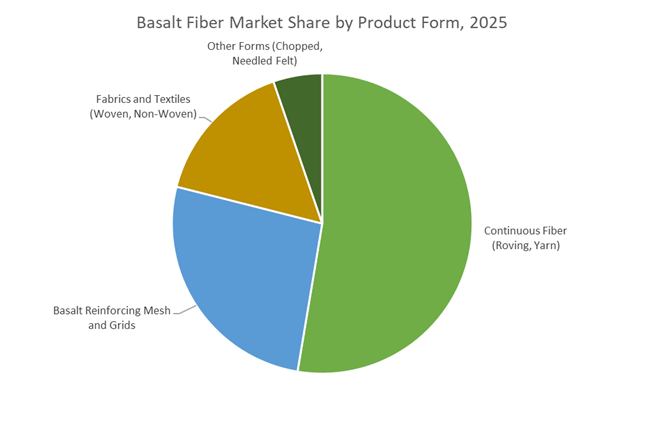

Market Share by Product Form: Continuous Basalt Fiber and Roving Anchor Industrial Supply

Continuous basalt fiber and roving account for approximately 50% of the global Basalt Fiber Market, reflecting their role as the foundational input material for nearly all downstream basalt-based products, including rebar, meshes, fabrics, and composite profiles. This segment dominates because continuous fiber delivers the highest specific strength-to-weight efficiency, allowing engineers to design load-bearing structures that outperform steel on a weight-adjusted basis while remaining significantly lighter. Market share is further reinforced by basalt fiber’s ability to retain structural integrity at elevated temperatures well beyond the limits of conventional glass fibers, positioning it as a preferred reinforcement in fire-resistant and high-heat industrial environments. Its inherent resistance to alkaline attack in concrete eliminates the need for protective chemical coatings, reducing system complexity and lifecycle costs for construction-grade applications. Manufacturing advances have also played a critical role, as tighter filament diameter control ensures consistent resin uptake and process stability in high-speed pultrusion and filament winding operations, supporting scalable industrial production. Together, these performance, durability, and manufacturability advantages establish continuous basalt fiber and roving as the core supply segment underpinning the entire basalt fiber value chain, securing its leading market share.

Market Share by Application: Construction and Infrastructure Drive Long-Term Adoption

Construction and infrastructure applications represent approximately 45% of total demand in the Basalt Fiber Market, making this segment the primary growth and volume driver. This dominance is structurally linked to the industry’s need to address corrosion-driven maintenance costs in reinforced concrete, a challenge that traditional steel solutions have failed to solve economically. Basalt fiber reinforced polymer (BFRP) systems offer complete immunity to rust, enabling infrastructure assets such as bridges, coastal structures, and tunnels to achieve service lives measured in decades without major intervention. Market share is further reinforced by significant logistics and installation efficiencies, as the low weight of basalt reinforcement dramatically reduces transportation costs and onsite handling requirements, aligning directly with sustainability and carbon-reduction goals. In road construction, basalt-based reinforcement grids extend pavement life by mitigating reflective cracking and rutting, delivering measurable savings for municipal budgets. Non-conductive and electromagnetically transparent properties also support adoption in smart infrastructure projects, where compatibility with digital systems is increasingly non-negotiable. As governments and developers prioritize durability, sustainability, and total lifecycle cost reduction, construction and infrastructure remain the central demand engine anchoring the basalt fiber market.

Competitive Landscape: Global Leaders Advancing High-Performance Basalt Fiber Technologies

The competitive landscape in the Basalt Fiber Market is defined by firms specializing in continuous basalt fiber (CBF), woven fabrics, BFRP rebar, and advanced thermal insulation materials. Global suppliers are scaling production capacity, optimizing melting furnace efficiency, and investing in fiber-matrix interface R&D to enhance mechanical properties and durability. Companies are also focusing on product certifications, alkali resistance benchmarks, and application diversification, targeting high-growth markets such as automotive composites, marine structures, aerospace insulation, railway components, and oil & gas infrastructure reinforcement.

Kamenny Vek: Leading Cbf Roving Producer Enhancing Global Infrastructure Composites

Kamenny Vek remains one of the world’s most technically advanced manufacturers of Continuous Basalt Fiber Rovings, utilizing a cutting-edge single-stage melting process to achieve exceptional energy efficiency and fiber uniformity. The company’s strict quality control standards deliver tensile modulus values exceeding 85 GPa and consistent filament diameters (12-17 μm), making their fibers ideal for pultrusion, geogrids, and BFRP rebar production. With a global distribution footprint, Kamenny Vek supports critical infrastructure, construction reinforcement, and composite manufacturing markets. Its product range includes chopped strands for concrete reinforcement and high-twist yarns suited for fire-resistant textiles and filtration systems.

Technobasalt-Invest LLC: Innovator in Basalt Superfine Fiber For Cryogenic and Defense Applications

Technobasalt-Invest is recognized for pioneering Basalt Superfine Fiber (BSTF) solutions, offering exceptionally low thermal conductivity (~0.030 W/(m·K) at -96°C) that meet the stringent insulation requirements of cryogenic storage and aerospace systems. The company’s furnaces and manufacturing lines are engineered for high energy efficiency, reducing energy consumption by nearly 30% compared to conventional glass fiber processes. Technobasalt-Invest holds certifications ensuring superior alkali resistance for BFRP rebar applications and serves sectors such as aviation and defense with specialty tapes and fabrics engineered for lightweight thermal protection.

Basaltex NV: Advancing High-End Woven and Multiaxial Basalt Fiber Fabrics

Basaltex is a prominent European producer of woven fabrics, multiaxial reinforcements, and NCF basalt fabrics, supplying high-end composite manufacturing environments that rely on resin infusion and advanced molding techniques. The company collaborates closely with automotive Tier 1 suppliers to develop composites that enhance NVH performance while addressing thermal and acoustic insulation needs. Through continual R&D investment-including EU-funded programs-Basaltex is improving basalt fiber sizing formulations to enhance fiber-matrix adhesion by up to 20%, strengthening its position as a specialist in sustainable and energy-efficient composite materials.

Haining Anjie Composite Material: High-Volume Cbf Producer Driving Apac Composite Adoption

Haining Anjie leverages large-scale APAC manufacturing capacity to provide competitively priced continuous basalt fiber rovings and chopped strands. The company supplies critical materials for friction components such as automotive brake pads, as well as composite pipes and industrial tanks used in chemical environments. With capabilities to customize chopped strand lengths (3-25 mm) and surface treatments, Haining Anjie supports tailored mechanical performance in asphalt, polymers, and concrete. Its ongoing investments in forehearth optimization ensure minimal crystallization defects and achieve a tensile strength variation tightly controlled within ±5%.

Arab Basalt Fiber Company (ABF): Expanding BFRP Rebar Capacity Across The Middle East

ABF benefits from access to high-quality regional basalt deposits containing ≥46% silica, ensuring consistent feedstock quality for fiber production. The company is strategically expanding in the GCC and MENA construction sector, emphasizing basalt rebar’s superior corrosion resistance in saline and alkaline conditions typical of regional environments. Following a multi-million-dollar investment in Q4 2024, ABF is establishing new pultrusion lines for high-volume BFRP rebar manufacturing. It is also pursuing ASTM and ISO certifications, particularly for UV durability performance, targeting long-life reinforced composites for harsh outdoor applications.

China has consolidated its position as the largest producer and consumer of basalt fiber by embedding the material into national “strategic new materials” planning. Under the Industry 4.0 framework led by the Ministry of Industry and Information Technology, basalt fiber capacity expanded by approximately 12% during 2024–2025, driven by state-backed industrial zones and preferential energy pricing. The strategic emphasis is on continuous basalt fiber (CBF) for wind energy, where turbine OEMs are increasingly replacing E-glass with basalt rovings to improve fatigue resistance and lifecycle durability. This demand is structurally aligned with China’s renewable push, which reached 2.09 billion kW of installed capacity by mid-2025, creating a sustained pull for corrosion-resistant composites.

From a manufacturing standpoint, leading producers such as Zhejiang GBF and Shanxi Basalt Fiber Technology are deploying AI-enabled melt-control and real-time viscosity monitoring systems. These upgrades directly address historical variability in filament diameter and tensile strength-long a bottleneck for structural-grade adoption-and have reportedly lifted high-grade output yields by around 15%. This shift positions China not only as a volume supplier but as a credible source of aerospace- and energy-grade basalt composites.

United States - Infrastructure Modernization Anchored by IP Protection

The U.S. basalt fiber market is being shaped by infrastructure renewal and a deliberate strategy to localize composite supply chains. A pivotal milestone was the commissioning of Mafic USA’s Shelby, North Carolina facility in August 2024, marking the first large-scale continuous basalt fiber production base in North America. This capacity build directly supports federal infrastructure spending programs and reduces reliance on imported composite reinforcements for bridges, roads, and coastal structures.

Equally critical is the emergence of a strong intellectual property moat. Basanite Industries secured multiple U.S. patents in late 2024 for high-speed basalt composite rebar (BasaFlex), targeting corrosion-prone concrete applications within the $1.2 trillion U.S. infrastructure renewal pipeline. Complementing this, the 2025 formation of ReforceTech Americas-a joint venture between Rock Fiber Inc. and ReforceTech Ltd.-signals a coordinated push to supply low-carbon basalt MiniBars for domestic construction, aligning sustainability goals with structural performance.

Uzbekistan - Central Asia’s Vertically Integrated Export Challenger

Uzbekistan has rapidly emerged as a competitive basalt fiber exporter by leveraging abundant volcanic rock reserves and low-cost domestic energy. The state-backed Basalt Uzbekistan group’s high-visibility debut at JEC World 2025 in Paris underscored the country’s ambition to move beyond raw material exports toward vertically integrated basalt solutions, spanning fibers, fabrics, and geogrids. This positioning directly challenges traditional suppliers in Eastern Europe and Russia.

Strategically, Uzbekistan is prioritizing high-performance Basalt-Reinforced Polymers (BFRP) for aerospace, automotive lightweighting, and renewable energy structures. A March 2025 agreement with European technical partners to deploy advanced surface-treatment technologies has accelerated the country’s ability to meet Western certification standards. With competitive pricing underpinned by energy economics, Uzbekistan is increasingly viewed as a “China-plus-one” sourcing option for global composite buyers.

Germany - Hybrid Conductive Basalt and Circular Economy Alignment

Germany’s basalt fiber strategy is defined by high-value material hybridization and regulatory alignment with EU decarbonization frameworks. In January 2025, the collaboration between Michelman and FibreCoat resulted in AluCoat-an aluminum-coated basalt fiber engineered for electromagnetic interference (EMI) shielding and EV battery enclosures. This innovation positions basalt as a functional alternative to carbon fiber in applications requiring conductivity without excessive cost or carbon penalties.

Automotive and rail OEMs in Germany are also advancing basalt–rPET hybrid composites that meet EN 45545-2 fire standards while improving recyclability versus glass fiber systems. Importantly, the 2025 rollout of the EU Carbon Border Adjustment Mechanism (CBAM) structurally favors basalt producers, as basalt’s lower embodied carbon translates into reduced carbon-adjustment exposure compared to carbon fiber imports.

United Arab Emirates - Salinity-Resistant Materials for Giga-Projects

The UAE is carving out a distinct basalt fiber demand profile centered on extreme-environment infrastructure. Announcements by the Arab Basalt Fiber Company at The Big 5 Exhibition 2025 highlighted the development of the region’s first fully integrated basalt ecosystem, including local production of basalt geogrids and reinforcements. These materials are being specified for mega-developments such as NEOM and the Dubai Urban Plan 2040.

A key adoption driver is basalt fiber’s immunity to chloride-induced corrosion. UAE infrastructure authorities are increasingly mandating basalt-reinforced concrete for marine piers, desalination plants, and coastal transport assets, with lifecycle models projecting maintenance intervals extending from ~15 years to nearly 50 years. This performance advantage, combined with climate resilience requirements, positions basalt fiber as a default material for Gulf-region coastal construction.

India - High-Volume Infrastructure and Technical Textile Integration

India’s basalt fiber market is anchored in large-scale civil construction and technical textiles, aligned with rapid urbanization and transportation upgrades. The July 2024 launch of high-tensile basalt reinforcements by JOGANI Reinforcement reflects a growing domestic capability to tailor basalt products for crack resistance and durability in Indian climatic conditions.

Policy support under the National Technical Textiles Mission is accelerating the adoption of basalt-based geotextiles for soil stabilization, erosion control, and rail corridors, contributing to India’s target of a $40 billion technical textiles market by 2026. Beyond construction, Indian research institutions are evaluating basalt fiber for cryogenic-tolerant applications in LNG terminals and nuclear containment structures, indicating a gradual move toward higher-specification, energy-sector uses.

2025 National Strategic Matrix - Basalt Fiber Market

Basalt Fiber Market Matrix

|

Country

|

Primary Application Focus

|

Key 2024–2025 Event

|

Strategic Advantage

|

|

China

|

Wind Energy & NEVs

|

12% Capacity Expansion

|

AI-enabled melt control, scale

|

|

United States

|

Infrastructure & Rebar

|

Mafic USA Plant Commissioning

|

Patent-protected domestic supply

|

|

Uzbekistan

|

Aerospace & Geogrids

|

JEC World 2025 Showcase

|

Low-cost energy, vertical integration

|

|

Germany

|

Conductive & Recyclable Composites

|

AluCoat Launch

|

CBAM-driven carbon advantage

|

|

UAE

|

Coastal Giga-Projects

|

ABFC Ecosystem Development

|

Zero corrosion in high salinity

|

|

India

|

Concrete & Geotextiles

|

High-Tensile Basalt Launch

|

Policy-backed infrastructure demand

|

Basalt Fiber Market Report Scope

Basalt Fiber Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1549.2 Million

|

|

Market Size (2035)

|

$5400.2 Million

|

|

Market Growth Rate

|

13.3%

|

|

Segments

|

By Product Form (Continuous Fiber, Fabrics & Textiles, Basalt Reinforcing Mesh, Other Forms), By Manufacturing Process (Pultrusion, Filament Winding, RTM, Centrifugal Casting, Vacuum Infusion), By Application (Construction & Infrastructure, Automotive & Transportation, Aerospace & Defense, Wind & Renewable Energy, Electronics & Electrical, Chemical & Marine)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kamenny Vek, Zhejiang GBF Basalt Fiber Co., Ltd., Mafic SA, Basaltex NV, Technobasalt-Invest LLC, Arab Basalt Fiber Company, Sichuan Aerospace Tuoxin Basalt Industrial Co., Ltd., Deutsche Basalt Faser GmbH, Jilin Huayang New Composite Materials Co., Ltd., Galen Ltd., Sudaglass Fiber Technology, Isomatex S.A., HG GBF Basalt Fiber Co., Ltd., Basalt Uzbekistan, ASA.TEC GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Basalt Fiber Market Segmentation

By Product Form

- Continuous Fiber

- Fabrics and Textiles

- Basalt Reinforcing Mesh

- Other Forms

By Manufacturing Process

- Pultrusion

- Filament Winding

- Resin Transfer Molding (RTM)

- Centrifugal Casting

- Vacuum Infusion

By Application

- Construction and Infrastructure

- Automotive and Transportation

- Aerospace and Defense

- Wind and Renewable Energy

- Electronics and Electrical

- Chemical and Marine

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Basalt Fiber Market

- Kamenny Vek

- Zhejiang GBF Basalt Fiber Co., Ltd.

- Mafic SA

- Basaltex NV

- Technobasalt-Invest LLC

- Arab Basalt Fiber Company (ABFC)

- Sichuan Aerospace Tuoxin Basalt Industrial Co., Ltd.

- Deutsche Basalt Faser GmbH

- Jilin Huayang New Composite Materials Co., Ltd.

- Galen Ltd.

- Sudaglass Fiber Technology

- Isomatex S.A.

- HG GBF Basalt Fiber Co., Ltd.

- Basalt Uzbekistan

- ASA.TEC GmbH

*- List not Exhaustive