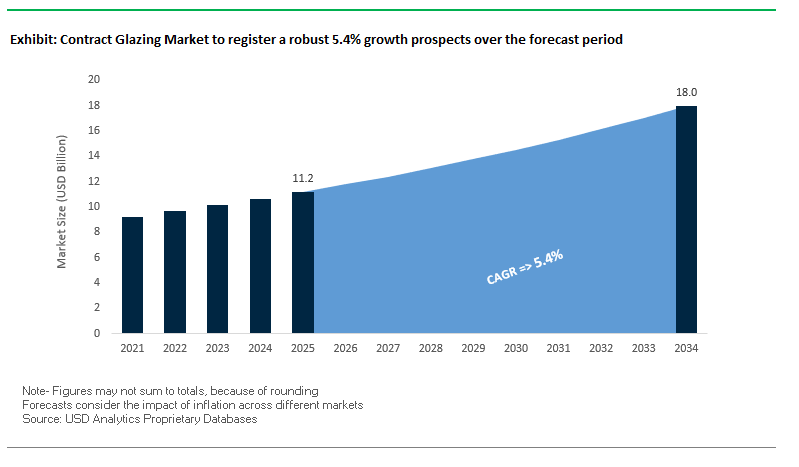

Market Overview: Contract Glazing Market Valued at $11.2 Billion in 2025

The Global Contract Glazing Market is valued at USD 11.2 billion in 2025 and is projected to reach USD 18 billion by 2034, expanding at a CAGR of 5.4%. This specialized sector is a critical enabler of modern architectural design, energy efficiency, and building performance, with glaziers now offering integrated facade solutions that go beyond simple installation.

High-performance systems such as triple-glazed insulated glass units (IGUs) are being specified in colder regions and projects targeting net-zero energy certification, directly addressing climate change and energy efficiency targets. The rise of Building-Integrated Photovoltaics (BIPVs) is transforming facades into power-generating assets, creating new revenue streams for developers and value chains for glazing contractors.

Dynamic solutions such as electrochromic smart glass are also gaining momentum in commercial buildings, where automation of tinting supports daylighting strategies and reduces HVAC loads. However, the industry faces skilled labor shortages in fabrication and installation, driving adoption of prefabricated and panelized glazing systems to improve project timelines and reduce on-site complexity.

Key Insights for Industry Professionals:

- Market Size 2025: USD 11.2 Billion | 2034: USD 18 Billion | CAGR: 5.4%

- Triple-glazed IGUs gaining share in net-zero and cold-climate projects.

- BIPV curtain walls creating energy-positive commercial facades.

- Smart and dynamic glass adoption rising in corporate and institutional projects.

- Prefabricated systems mitigating labor shortages and reducing installation risk.

- Contract glaziers shifting from subcontractors to full building envelope solution providers.

Market Analysis: Recent Developments Driving the Contract Glazing Industry in 2025

The contract glazing industry in 2025 is experiencing accelerated transformation through material innovation, renewable energy integration, and automated fabrication.

In August 2025, a leading European glass manufacturer committed capital to expand low-carbon glass production, directly addressing embodied carbon reduction targets in commercial construction. In July 2025, a major U.S. glazier secured a landmark corporate campus project featuring photovoltaic curtain walls, signaling the mainstream adoption of energy-generating facades.

Technology partnerships are shaping next-generation materials. In May 2025, a strategic alliance between a glass producer and a tech firm advanced self-healing glass using polymers to extend service life and reduce maintenance cycles. In April 2025, a European trade body issued guidelines on vacuum insulated glass (VIG), spotlighting its thin profile and thermal efficiency for retrofit markets.

Regional capacity expansion is also notable. In March 2025, a new fabrication line for jumbo-sized panels came online in the Middle East to support giga-projects demanding seamless glazing formats. By February 2025, a U.S. university unveiled a research building with electrochromic smart glass integrated into BMS systems, proving the operational benefits of dynamic facades.

Awards and events further demonstrate industry direction. In January 2025, an Australian high-rise featuring acoustic insulation glass facades was recognized for mitigating urban noise without sacrificing daylight. Also in January, India announced the glasspex INDIA & glasspro INDIA 2025 exhibitions, highlighting AI-driven production optimization and sustainable glassmaking in one of the fastest-growing regional markets.

Key Trends and Strategic Opportunities Shaping the Contract Glazing Market

Accelerated Adoption of High-Performance, Energy-Modeled Glazing Systems

The contract glazing market is witnessing a rapid shift towards high-performance glazing systems, driven by stringent building energy codes, corporate net-zero commitments, and third-party sustainability certifications. Compliance with ASHRAE Standard 90.1 requires glazing contractors to deliver products with superior U-factors and Solar Heat Gain Coefficients (SHGC), elevating the technical complexity of installations. Corporate sustainability mandates, supported by DOE guidance on energy-efficient building envelopes, further reinforce the adoption of triple glazing, dynamic glass, and high-performance coatings. Leading solutions, such as Saint-Gobain’s SAGE Electrochromics smart glass, illustrate how early-stage design integration is critical to achieving optimal energy performance. Moreover, glazing contractors now play a pivotal role in attaining LEED and Living Building Challenge certifications, ensuring that thermal, daylighting, and ventilation performance align with evolving project benchmarks.

Integration of Prefabricated and Unitized Curtain Wall Systems for Speed and Safety

To address the dual challenges of labor shortages and construction efficiency, the market is increasingly embracing prefabricated, unitized curtain wall systems. Studies from the Harvard Joint Center for Housing Studies indicate that these off-site assembled systems can cut on-site construction time by 25% to 35%, accelerating project completion and reducing labor costs. Factory-based assembly also enhances quality control, as highlighted by the AIA, ensuring tighter tolerances and rigorous water and air infiltration testing in controlled environments. By relocating high-risk, complex assembly tasks off-site, contractors can mitigate safety hazards on high-rise projects. This approach also optimizes skilled labor deployment, allowing smaller, specialized teams to focus on precise on-site installation, thereby improving overall project efficiency and reliability.

Development of Glazing Systems with Integrated Photovoltaic (PV) Technology

There is a growing opportunity to advance glazing systems that integrate transparent or semi-transparent PV cells, turning building facades into active energy-generating surfaces. Ubiquitous Energy exemplifies this trend, securing over $30 million in Series B funding to scale transparent solar window technology and establish high-volume manufacturing capabilities in the U.S. Real-world pilot projects demonstrate that such systems can generate approximately 30% of a building’s energy demand while maintaining visual aesthetics and functionality. Adoption of these next-generation BIPV glazing solutions supports net-positive energy targets and aligns with increasingly stringent sustainability certifications, making it a strategic growth area for contract glazing specialists.

Expansion into Modernization and Retrofit of Existing Building Stock

Retrofit projects targeting decarbonization of existing commercial buildings represent a high-value opportunity for glazing contractors. Modernization of aging glazing systems requires advanced engineering to install high-performance solutions within existing structural constraints. C-PACE financing programs allow building owners to fund up to 100% of energy efficiency upgrades, including window replacements, with repayment via long-term property tax assessments, removing financial barriers. U.S. policy initiatives, such as the Inflation Reduction Act (IRA), and EU directives like the revised EPBD, emphasize "retrofit-first" strategies to achieve zero-emission building stocks by 2050. Contractors specializing in retrofits can thus capitalize on regulatory incentives and a growing demand for sustainable upgrades to existing commercial properties.

Competitive Landscape: Leading Companies in the Global Contract Glazing Market

The contract glazing industry is shaped by specialized firms with deep engineering, fabrication, and project management expertise. Competitive differentiation lies in delivering landmark facades, leveraging BIM and digital twins, and offering integrated building envelope solutions.

Harmon Inc.: North American Leader in Complex Curtain Walls

Harmon is a recognized leader in North America for custom curtain wall design and installation. Its expertise spans aluminum and glass systems for office towers and institutional buildings. With strong engineering and project management teams, Harmon positions itself as a single-source building envelope provider, capable of handling the most technically demanding projects.

Permasteelisa Group / Benson Industries: Global Powerhouse in Façade Systems

Following its acquisition of Benson Industries, Permasteelisa has consolidated its role as a global facade giant. With vertically integrated operations across design, engineering, fabrication, and installation, it delivers some of the world’s most architecturally complex high-rises and cultural landmarks. Its unitized curtain walls, monumental glazing, and stick systems are benchmarks in the premium segment.

Enclos Corp.: Digital Twin and BIM Pioneer in Façade Engineering

Enclos is a U.S.-based contract glazier renowned for digital design integration. Its use of Building Information Modeling (BIM) and digital twins enables precise coordination for projects with complex geometries. Its portfolio includes cultural centers, skyscrapers, and academic buildings, where advanced engineering of bespoke envelopes is mission-critical.

W&W Glass, LLC: Specialization in Structural Glass Systems

W&W Glass focuses on structural and point-supported glazing, delivering transparent and visually minimal facades for retail, transport, and commercial spaces. Its expertise in spider fittings and canopies has positioned it as a go-to partner for high-visibility architectural projects. The company emphasizes engineering consultancy alongside delivery, supporting architects with bespoke facade solutions.

Viracon, Inc.: Advanced Coatings for Energy-Efficient and Secure Glass

Viracon is a leading U.S. fabricator of architectural glass, supplying insulated, laminated, and silkscreened products for commercial buildings. It is recognized for solar control coatings that maximize daylight while reducing solar heat gain, aligning with energy code compliance and green building standards. Viracon’s customized performance solutions make it a preferred partner for developers seeking both energy efficiency and architectural flexibility.

Contract Glazing Market Share Insights

Insulated Glass Units Dominate Market Share by Product Type in the Contract Glazing Industry

Insulated Glass Units (IGUs) account for nearly 45% of the contract glazing industry, reflecting their role as the non-negotiable baseline for modern commercial building envelopes. Their dominance stems directly from energy code compliance, as IGUs typically double-pane with argon gas fills offer the thermal insulation and condensation resistance required to meet ASHRAE standards, IECC codes, and Europe’s EN regulations. Virtually every vision glass installation in curtain wall and window wall applications begins with IGUs, with Low-E coatings further enhancing solar heat gain control. Developers and architects specify IGUs not only for thermal efficiency but also for acoustic performance, as office towers, mixed-use developments, and healthcare facilities demand reduced noise infiltration. Their scale of production, compatibility with advanced coatings, and broad global adoption secure IGUs as the cornerstone of high-performance facades.

Commercial Buildings Drive Market Share by End-Use in the Contract Glazing Industry

Commercial buildings represent roughly 50% of the demand in the contract glazing market, underscoring their role as the volume driver for glazing contractors and façade system integrators. Office towers, corporate campuses, and mixed-use commercial complexes rely on high-performance glazing to deliver occupant comfort, natural daylighting, and striking aesthetics that boost property value. Codes such as ASHRAE 90.1 in the U.S. and Europe’s Energy Performance of Buildings Directive (EPBD) compel developers to select insulated and coated glass that minimizes HVAC loads. Large-scale urbanization projects in Asia-Pacific, combined with North American retrofit activity for energy upgrades, further support the dominance of this segment. With glass often accounting for 30–40% of commercial façade surface area, this end-use sector remains the single largest consumer of advanced IGUs, laminated glass, and coated products.

United States: High-Performance Contract Glazing Driven by Energy Codes and Urban Retrofits

The U.S. contract glazing market is experiencing rapid growth due to a combination of stringent building regulations, technological advancements, and increasing demand for sustainable solutions. States like New York are enforcing strict energy codes that mandate U-factors of 0.32 or less in certain climate zones, pushing adoption of high-performance glazing systems designed to improve insulation and reduce heat transfer. At the federal level, the U.S. Environmental Protection Agency’s ENERGY STAR certification and tax incentives under the Inflation Reduction Act of 2022 are encouraging commercial property developers and homeowners alike to adopt energy-efficient glazing solutions.

The U.S. market is also seeing a surge in smart glass, advanced low-E coatings, and multi-pane glazing systems, which not only enhance thermal performance but also integrate with smart building management systems for greater occupant comfort. Key applications are concentrated in commercial new construction, retrofit projects, and LEED-certified green buildings, while institutional sectors such as schools and hospitals are also driving demand. Urban centers are witnessing large-scale retrofits of aging glass façades to comply with modern energy standards. Corporate moves such as Permasteelisa’s acquisition of Benson in 2024 underscore the sector’s consolidation and expansion strategy in North America, strengthening expertise in façades and curtain walls.

Germany: Contract Glazing Market Influenced by EU Circular Economy Mandates

Germany’s contract glazing industry is shaped by one of the most stringent regulatory environments in Europe. The EU Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025, requires all packaging to be fully recyclable by 2030 and establishes minimum recycled content targets. Although designed for broader packaging applications, this regulation heavily influences glass and façade manufacturers, pushing them toward sustainable material innovation. The Verpackungsgesetz (Packaging Act) further holds producers accountable for the life cycle of their products, incentivizing innovation in recyclability and circular economy compliance.

In addition to regulation, Germany’s glazing sector is defined by advanced product innovations, particularly in façades designed for energy efficiency and recyclability. Manufacturers are increasingly developing solutions that align with EU waste reduction targets, and corporate players like Gerresheimer AG are pioneering sustainable packaging initiatives that spill over into architectural glazing practices. Governmental mandates and sustainability goals are accelerating the development of materials that not only meet performance criteria but also align with the broader European commitment to resource efficiency.

China: Dual Carbon Goals and Smart City Developments Boost Glazing Innovation

China’s contract glazing market is expanding rapidly under the country’s dual carbon goal, which aims for carbon peak and carbon neutrality. These objectives are reshaping the construction industry by enforcing eco-friendly material usage, stimulating demand for advanced glazing systems in both commercial and residential projects. At the same time, “Made in China 2025” policies are designed to increase domestic content of core materials to 70% by 2025, fostering innovation in high-tech manufacturing, including in glass and façade systems.

On the technological front, Chinese manufacturers are investing heavily in automation, artificial intelligence, and “5G plus industrial internet” applications to streamline production and enhance flexible capacity. The growth of smart cities is also fueling demand for glazing integrated with sensors and building automation systems, while e-commerce expansion indirectly supports demand through logistics hubs and retail infrastructure. With policies restricting non-degradable plastics, China’s construction and packaging sectors alike are leaning toward sustainable alternatives, positioning glazing as a premium, eco-friendly solution in modern urban development.

India: Infrastructure Growth and Urbanization Fuel Contract Glazing Demand

India’s contract glazing market is witnessing accelerated momentum due to strong governmental support and rapid urban development. Programs such as “Make in India” and “Zero Effect, Zero Defect” are encouraging local production of high-quality glazing systems, while regulatory reforms like the Plastic Waste Management (Amendment) Rules have further boosted demand for sustainable building materials. The Production Linked Incentive (PLI) Scheme, with an investment outlay of INR 10,900 crore for the food processing and related sectors, indirectly enhances demand for standardized and high-quality contract glazing as part of broader infrastructure development.

Urbanization is a defining driver in India, with expanding IT parks, business hubs, and commercial complexes requiring advanced façades and glazing systems. Rising disposable incomes and lifestyle upgrades are also increasing expectations for modern, energy-efficient, and aesthetically appealing buildings. Additionally, India’s pharmaceutical and healthcare industries are pushing demand for secure, tamper-resistant glazing solutions in specialized facilities. Leading domestic players like PGP Glass are leveraging premium glass packaging expertise to diversify into architectural applications, catering to both local and global demand.

Brazil: Regulatory Policies and Sustainability Push Propel the Glazing Industry

Brazil’s contract glazing market is undergoing significant transformation as sustainability becomes central to construction practices. The National Solid Waste Policy promotes a circular economy, driving both packaging and building industries toward recyclable and durable materials, including advanced glass systems. Additionally, the ban on solid waste imports in January 2025 is fostering domestic waste management innovation, indirectly benefiting contract glazing manufacturers by ensuring greater local resource utilization.

Technology adoption is another key growth factor, with Brazilian manufacturers integrating robotics and AI for quality assurance, automated defect detection, and precision engineering. Strategic investments, such as the expansion of facilities in São Paulo to meet surging demand from beverage and commercial infrastructure projects, are further strengthening the supply chain. Meanwhile, stricter traceability requirements from ANVISA for food and beverage supply chains are raising performance standards for glass and glazing products, making sustainability and efficiency non-negotiable for industry stakeholders.

Japan: Advanced Recycling and Seismic-Resilient Glazing Define Market Growth

Japan’s contract glazing sector stands out globally for its unique combination of advanced recycling systems and seismic resilience. Under the Containers and Packaging Recycling Law, businesses are obligated to recycle, ensuring that glass and other rigid materials are continuously repurposed into new applications. Additionally, regulatory updates by the Ministry of Health, Labour and Welfare (MHLW) in May 2025 introduced new standards for food-contact packaging, reflecting Japan’s commitment to safety and high-performance materials that extend to the construction industry.

Japan is also a hub for innovation in bio-based materials and high-functionality glazing. For example, the partial adoption of bio-based polypropylene by Shiseido in September 2025 reflects a nationwide shift toward sustainability across multiple industries. In the contract glazing sector, innovations are focused on dimensional stability, deformation resistance, and seismic resilience, making Japanese products ideal for earthquake-prone environments. This dual focus on sustainability and safety positions Japan as a global leader in contract glazing solutions tailored to both regulatory compliance and extreme performance requirements.

Contract Glazing Market Report Scope

Contract Glazing Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.2 Billion

|

|

Market Size (2034)

|

$18 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Insulated Glass Units, Laminated Glass, Tempered Glass, Coated Glass, Specialty Glass), By End-Use (Commercial Buildings, Institutional Buildings, Hospitality, Industrial Facilities, Retail & Shopping Centers), By System Type (Curtain Walls, Storefronts, Skylights, Windows & Doors, Interior Glazing), By Application (New Construction, Renovation & Retrofit)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Permasteelisa Group, Albéa S.A., AptarGroup, Inc., Berry Global Inc., Amcor plc, O-I Glass, Gerresheimer AG, Aluplast GmbH, AGC Inc., SCHOTT AG, Pella Corporation, JELD-WEN Holding, Inc., YKK AP Inc., The Kawneer Company, Inc., LIXIL Group Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Contract Glazing Market Segmentation

By Product Type

- Insulated Glass Units

- Laminated Glass

- Tempered Glass

- Coated Glass

- Specialty Glass

By End-Use

- Commercial Buildings

- Institutional Buildings

- Hospitality

- Industrial Facilities

- Retail & Shopping Centers

By System Type

- Curtain Walls

- Storefronts

- Skylights

- Windows & Doors

- Interior Glazing

By Application

- New Construction

- Renovation & Retrofit

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Contract Glazing Market

- Permasteelisa Group

- Albéa S.A.

- AptarGroup, Inc.

- Berry Global Inc.

- Amcor plc

- O-I Glass

- Gerresheimer AG

- Aluplast GmbH

- AGC Inc.

- SCHOTT AG

- Pella Corporation

- JELD-WEN Holding, Inc.

- YKK AP Inc.

- The Kawneer Company, Inc.

- LIXIL Group Corporation

* List Not Exhaustive

Methodology

The Contract Glazing Market analysis provided by USDAnalytics is derived from a rigorous blend of primary and secondary research, designed to offer actionable insights for industry professionals. Primary research involved direct engagement with leading glazing contractors, manufacturers, architects, and project developers across key markets including the U.S., Germany, China, India, Brazil, and Japan, providing first-hand data on adoption of high-performance glazing systems, smart glass technologies, and BIPV integration. Secondary research encompassed the study of company reports, government regulations, building codes, trade publications, and project databases to validate trends in prefabricated curtain walls, energy-efficient glass solutions, and retrofit opportunities. USDAnalytics employed advanced forecasting models, analyzing historical growth (2015–2024), current technological advancements, and regulatory drivers to project market expansion to 2034. The methodology emphasizes holistic assessment of material innovations, sustainable building mandates, labor dynamics, and regional construction practices to deliver precise, data-backed insights for stakeholders navigating complex architectural, energy, and facade design requirements.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.