Market Overview: Corundum’s Role in Abrasives, Refractories and Sapphire Optics

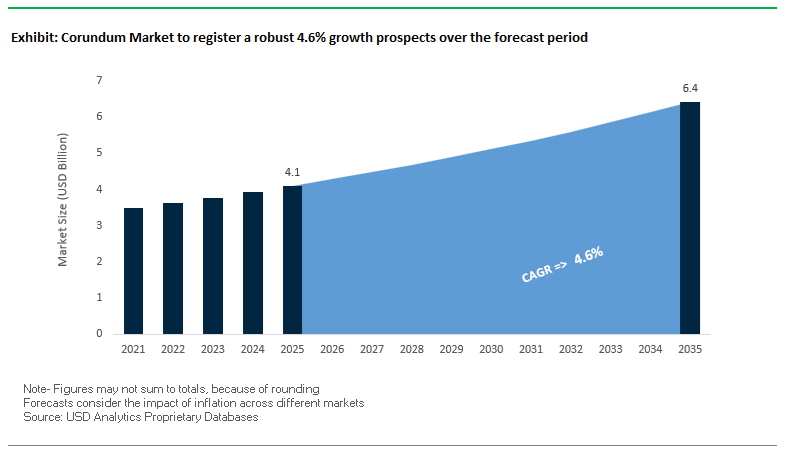

The global Corundum Market is projected to reach USD 4.1 billion in 2025 and grow to USD 6.4 billion by 2035, registering a steady CAGR of 4.6% (2025–2035). For manufacturers and vendors of abrasives, fused alumina refractories and single-crystal sapphire, this signals a stable, industrially anchored growth trajectory driven by machining, high-temperature processing and advanced optical/electronic applications. With Mohs hardness of 9, corundum (Al₂O₃) remains the benchmark high-performance abrasive for grinding wheels, sandpaper and cutting tools, while fused and tabular alumina underpin refractory linings in steel and cement production. On the premium end, single-crystal sapphire substrates and windows convert corundum into a critical strategic material for LEDs, high-intensity lasers and defense optics, particularly where broad UV–IR transmission and extreme durability are required.

For vendors, the combination of thermal stability (~2,044°C melting point), optical transparency (150 nm–5.5 μm) and the availability of high-purity white fused alumina (≥99.5% Al₂O₃, low Fe) allows product differentiation across abrasives, refractories and technical ceramics. Producers that can tightly control impurity levels, grain morphology and crystal orientation are well positioned to win specifications in precision surface finishing, advanced ceramics and semiconductor processing equipment.

Key market insights for corundum manufacturers and suppliers:

- Hardness advantage in abrasives: Mohs hardness of 9 cements corundum as the default high-performance abrasive for grinding wheels, coated abrasives and cutting tools in metalworking and automotive machining.

- Refractory reliability at extreme temperatures: Fused and tabular alumina support furnace linings and kiln furniture in steel and cement kilns, where thermal stability near 2,044°C is critical to refractory life and uptime.

- Optical-grade sapphire for UV–IR applications: Single-crystal sapphire corundum offers high light transmission from near-UV (~150 nm) to mid-IR (~5.5 μm), enabling robust optical windows, domes and LED substrates for lasers and defense sensors.

- High-purity WFA for low-contamination processes: White fused alumina (WFA) at ≥99.5% Al₂O₃ purity with ultra-low iron content minimizes discoloration and contamination in precision polishing, medical devices and advanced technical ceramics.

Market Analysis: Corundum Demand Driven by Abrasive Innovation, Refractory Capacity and Sapphire Optics

The global corundum industry has been shaped by simultaneous advances in sintered abrasive grains, fused alumina capacity, sapphire components and recycling technologies, all of which directly influence demand for aluminum oxide in various value chains. In November 2025, Saint-Gobain Abrasives launched a next-generation sintered corundum abrasive grain line, engineered with a microcrystalline structure that delivers roughly 25% higher material removal rate (MRR) in heavy-duty grinding. This reinforces corundum’s position as the workhorse abrasive for high-productivity grinding in automotive, aerospace and general engineering. At the same time, a major Chinese fused alumina producer commissioned a new brown fused alumina (BFA) plant in Zibo, Shandong in March 2025 with an initial capacity of 50,000 tonnes/year, explicitly targeting surging global refractory demand from steel, cement and non-ferrous metal industries seeking reliable high-temperature linings.

Corundum’s strategic importance is also rising in advanced optics, semiconductors and defense. In September 2025, CoorsTek introduced a new line of high-purity sapphire components with C-plane orientation for semiconductor processing equipment, optimized to withstand aggressive plasma etching and corrosive chemical vapors—this directly supports node shrinking and higher wafer throughput. In December 2025, a US defense contractor secured a major order for ballistic-grade synthetic sapphire windows for reconnaissance aircraft sensor systems, monetizing sapphire’s scratch resistance and broad wavelength transmission for high-value defense programs. Earlier, January 2024 R&D work demonstrated single-crystal sapphire fibers with a Young’s modulus >380 GPa at >1,200°C in high-temperature composites, opening a future high-end niche in aerospace engine components that require both stiffness and extreme thermal stability.

Corporate and policy initiatives are also shaping supply security and sustainability. In August 2024, Okamoto Industries (Japan) acquired Riken Corundum for about USD 15 million, consolidating expertise in coated abrasives and coated products and extending Okamoto’s reach in industrial abrasives. IMERYS further aligned corundum production with decarbonization by publishing its Climate Transition Plan in April 2025, targeting a 15% reduction in CO₂ intensity by 2030 across fused minerals operations, which include corundum smelting. On the circularity front, a European government technology fund invested €10 million in June 2024 into a startup developing advanced corundum recycling technology to recover high-purity spent abrasive grains from manufacturing sludge for reuse in technical ceramics, potentially lowering raw material costs and environmental impact. Together, these developments position corundum as a strategic industrial mineral at the intersection of abrasive productivity, refractory reliability, optical precision and sustainability.

Breakthrough Material Purity Requirements and Advanced Corundum Engineering Creating High-Value Market Opportunities

Market Trend 1: Rapid Growth in 5N–6N Ultra-High-Purity α-Alumina as a Critical Safety Enabler for Li-ion Battery Separator Coatings

The Corundum Market is undergoing a structural transformation driven by the explosive rise of EV lithium-ion batteries, where ultra-high-purity α-alumina (corundum) has become indispensable for next-generation ceramic-coated separator technologies. Automotive OEMs and cell manufacturers now demand 5N (99.999%) to 6N (99.9999%) purity grades, with total magnetic impurities (Fe, Ni, Cr) strictly capped below 5–10 ppm to eliminate the risk of internal micro-shorts and lithium dendrite formation. This level of purity directly correlates with the prevention of catastrophic thermal runaway events—making high-purity corundum a safety-critical material.

Equally essential is tight particle size control, with a required D50 between 0.3–0.8 μm, enabling uniform ceramic layers in the 2–5 μm range across polyolefin separators. Achieving a narrow PSD is vital for eliminating pinholes, improving puncture resistance, and ensuring homogeneous shutdown behavior. The high melting point of corundum (2,072°C) ensures the ceramic layer remains intact even as PE/PP separators melt (~140°C), acting as a physical firewall that can delay or prevent thermal runaway propagation. Additionally, α-alumina must maintain electrochemical stability ≥5.0 V vs. Li/Li+, aligning with the voltage requirements of high-nickel cathodes, solid-state batteries, and emerging 5V+ chemistries. These technical requirements are a dominant force reshaping production, purification, and quality-control standards across the corundum supply chain.

Market Trend 2: Transition Toward Synthetic White Fused Alumina (WFA) as a Cleaner, Higher-Performance Abrasive Alternative to BFA

A powerful market trend is the accelerated substitution of Brown Fused Alumina (BFA) with White Fused Alumina (WFA) in precision abrasives and engineered grinding tools. This shift is driven by WFA’s superior purity—≥99.5% Al₂O₃—compared to the typical 94–97% Al₂O₃ purity range of BFA, which contains higher levels of TiO₂, Fe₂O₃, and SiO₂ impurities. This purity advantage translates into higher Knoop hardness (2,000–2,200 kg/mm²), improved friability, and enhanced tool life, making WFA the preferred material for aerospace machining, hardened steel grinding, and semiconductor wafer polishing.

WFA also aligns with global sustainability goals. Traditional BFA smelting demands roughly 4,500 kWh/tonne, whereas WFA processes using purified Al₂O₃ feedstocks or recycled aluminum residues significantly reduce net energy consumption and greenhouse gas emissions. Environmentally, WFA production avoids bauxite refining, which generates up to 1.5 tonnes of Red Mud waste per tonne of alumina—one of the world’s largest industrial waste streams. As sustainability metrics become embedded in procurement frameworks, WFA’s low-impurity profile, reduced waste footprint, and performance advantages are accelerating its adoption in high-specification abrasive applications.

Market Opportunity 1: Expansion of Single-Crystal Sapphire (Corundum) Crucibles and Tubes for High-Purity Silicon, SiC, and GaN Crystal Growth

A major opportunity in the Corundum Market lies in the scaling of single-crystal sapphire tubes and crucibles, which are rapidly replacing fused quartz in high-purity semiconductor crystal growth processes. Sapphire crucibles demonstrate ultra-low contamination (<1 ppbw Fe/Al/Ni)—orders of magnitude cleaner than quartz—preventing micro-defect formation in silicon boules produced via the Czochralski (CZ) method. Their high melting point (2,050°C) and superior thermal shock stability allow for tighter temperature gradients and lower defect densities, which are essential for larger-diameter (300 mm and 450 mm) semiconductor wafers.

Sapphire crucibles are also indispensable for the growth of 4N–6N purity Silicon Carbide (SiC) and Gallium Nitride (GaN) boules used in power electronics, high-frequency RF systems, EV inverters, and fast-charging infrastructure. Maintaining extremely low contamination levels is critical to minimizing micropipe defects and dislocation densities in SiC crystals. Sapphire’s high flexural strength (≥400 MPa) ensures mechanical reliability during repeated thermal cycling in CZ pullers. This expanding demand from the semiconductor and wide-bandgap materials industries positions synthetic sapphire as one of the most strategically valuable corundum-based materials globally.

Market Opportunity 2: Valorization of Industrial Alumina-Rich Waste Streams into High-Value Tabular Alumina for Refractories

Another emerging opportunity is the upcycling of industrial waste streams—including spent alumina catalysts (>90% Al₂O₃)—into high-density tabular alumina, a premium refractory material. Tabular alumina requires density ≥3.90 g/cm³ and low apparent porosity (≤3–5%), attributes that provide exceptional thermal shock resistance, slag resistance, and wear performance in steel, cement, and petrochemical refractory linings.

Refractories made with tabular alumina endure 2–4× more thermal cycles (e.g., between room temperature and 1,000°C) than those produced with calcined alumina, due to the interlocking α-alumina crystal platelets that resist crack propagation. Waste valorization processes—combining thermal purification and acid leaching—can achieve ≥99.5% Al₂O₃ purity, matching commercial requirements for premium refractory formulations. Critically, converting waste catalysts into refractory-grade tabular alumina yields a 5:1 reduction in landfilled waste volume, aligning with circular-economy frameworks and lowering the carbon footprint of refractory raw material production.

Corundum Market Share Analysis

Market Share by Origin: Synthetic Corundum Dominates Due to Purity, Scalability, and Industrial Performance Advantages

Synthetic corundum holds an overwhelming ~85% share of the global corundum market, driven by its unmatched purity, uniformity, and engineered performance characteristics that natural corundum cannot reliably provide. Industrial processes such as the Verneuil method, fused alumina production, and controlled crystal growth techniques enable manufacturers to produce corundum with 99%+ alumina purity, precise grain morphology, and consistent hardness—attributes essential for high-performance applications in abrasives, refractories, ceramics, and optoelectronics. Natural corundum, limited in availability and containing impurities that affect mechanical behavior and color, cannot meet the quality requirements or volume demands of industrial customers. Synthetic corundum’s scalability also enables mass production at a significantly lower cost per ton, which is crucial for the abrasives and refractory sectors that rely on continuous, high-volume consumption. In engineered systems—such as synthetic sapphire windows, substrates for LEDs, and high-purity ceramics—synthetic corundum delivers the thermal stability, chemical resistance, and mechanical durability required for advanced manufacturing. These combined advantages secure synthetic corundum’s position as the dominant source of material supply across global industrial value chains.

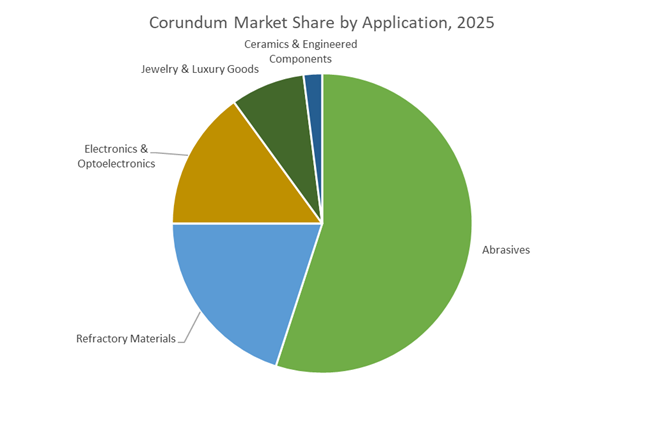

Market Share by Application: Abrasives Lead the Market Due to High Hardness Requirements and Continual Consumption Rates

The Abrasives segment accounts for ~55% of the global corundum market, reflecting the critical role of corundum-based abrasive grains in manufacturing, metalworking, and precision finishing industries worldwide. With a hardness of 9 on the Mohs scale, corundum—particularly fused alumina—provides the optimal balance of toughness, cutting efficiency, and fracture behavior required for grinding wheels, sanding belts, cutting discs, blasting media, and polishing compounds. Because abrasives are consumables that degrade during use, they require constant replenishment—driving significantly higher material turnover compared to refractories, ceramics, or electronics. This recurring demand is amplified by the scale of global metal fabrication, automotive manufacturing, construction, and machinery production, all of which rely heavily on corundum-based abrasives for shaping, finishing, and surface conditioning. In high-precision sectors such as optical components, semiconductor wafers, and fine mechanical systems, micro-grade synthetic alumina is favored for its controlled particle size and consistent cutting behavior. The combination of large-volume industrial usage, constant replacement cycles, and corundum’s unmatched performance-to-cost ratio ensures that abrasives remain the primary application and long-term growth engine of the global corundum market.

Country Analysis: Global Drivers in Corundum Development

China: Global Command of Fused Alumina Capacity and Synthetic Corundum for Electronics Manufacturing

China remains the undisputed leader in the global Corundum Market, particularly across the high-volume Brown Fused Alumina (BFA) and White Fused Alumina (WFA) categories, which form the backbone of the refractories and abrasives supply chain. By 2025, China accounted for the largest global production share of fused alumina, directly shaping international pricing trends and availability. The dominance is rooted in exceptionally large-scale smelter operations and the country’s expansive steel, cement, and metalworking sectors that consume massive volumes of refractory-grade corundum. Government-enforced quality upgrades further accelerate demand for high-purity fused alumina and tabular alumina, especially as steel mills and kiln operators transition toward longer-lifespan furnace linings to meet stricter industrial performance and energy efficiency standards.

Beyond industrial abrasives, China plays a critical role in the Synthetic Sapphire (corundum) substrate market, supplying the global LED, laser device, and semiconductor sectors. The country’s manufacturers are rapidly scaling advanced crystal growth technologies—supporting the shift to 6-inch and larger sapphire wafers essential for high-brightness LEDs and GaN-based power electronics. Companies such as Zhengzhou Yufa Abrasives Group are also expanding high-purity WFA production lines targeting precision grinding wheels, automotive machining applications, and fine-polishing sectors. This powerful combination of volume production, vertical integration, and accelerated capacity expansion secures China’s position as the largest and most influential force in the global corundum ecosystem.

United States: High-Performance Abrasives and Defense-Grade Synthetic Sapphire Expansion

The United States anchors its corundum market strength in specialty abrasives, advanced precision finishing solutions, and the high-value Synthetic Sapphire supply chain tailored for defense and aerospace. Companies like Washington Mills and 3M continue to dominate the U.S. high-end abrasives market by producing meticulously engineered fused alumina grains used in precision grinding and micro-finishing operations across aerospace turbine manufacturing, orthopedic implant machining, and medical instrumentation. The acquisition of Riken Corundum by Okamoto Industries (Aug 2024) further exemplifies the U.S. market’s consolidation trend, strengthening domestic capability in ceramic abrasives and performance-engineered grinding materials.

Simultaneously, the U.S. defense and optical industries depend heavily on domestically sourced synthetic sapphire for harsh-environment optical windows, missile domes, infrared sensors, and ballistic-resistant covers. Sapphire’s exceptional hardness, chemical stability, and thermal resistance make it a material of strategic significance for defense procurement. Additionally, rising investment in recycled alumina recovery, driven by supply chain security considerations, is fueling renewed interest in reclaiming alumina feedstock from industrial scrap. As geopolitical tensions reshape global materials logistics, the U.S. is increasingly prioritizing secure, localized, and high-purity corundum supply to sustain aerospace, optics, and precision engineering growth.

Russia: Global Feedstock Influence in Alumina and Industrial Corundum Supply

Russia plays a pivotal upstream role in the global Corundum Market due to its large-scale aluminum and alumina production network. RusAL, one of the world’s largest aluminum conglomerates, remains a key supplier of alumina and bauxite—both essential raw materials for producing fused alumina and related corundum derivatives. Fluctuations in Russian alumina output therefore exert material influence on global fused alumina pricing, particularly for refractory and abrasive manufacturers in Europe and Asia that depend on robust feedstock availability.

In addition to alumina, Russian industrial mineral exporters maintain steady supply flows of corundum-bearing raw materials and bauxite to global refractory producers, especially across Asia-Pacific manufacturing hubs. Despite geopolitical uncertainty affecting trade routes and secondary processing, Russia remains an indispensable upstream contributor, shaping cost structures and availability in the international corundum value chain.

Germany: Precision Abrasives for Automotive Engineering and High-Purity Refractory Innovation

Germany’s advanced automotive and engineering sectors drive strong demand for premium corundum abrasives, particularly electro-fused alumina used in high-precision grinding, deburring, and surface finishing of engine components, transmission systems, and high-strength metallic alloys. German manufacturers consistently require abrasive materials with strict particle uniformity, high hardness, and exceptional thermal resistance—criteria that position high-purity corundum as a cornerstone of the country’s industrial materials ecosystem.

In the refractory domain, German producers leverage tabular alumina and high-purity WFA for steelmaking ladle linings, blast furnace refractories, and casting vessels exposed to extreme thermal shock. Germany’s metallurgical sector increasingly prioritizes corundum-based refractories for their ability to withstand corrosive slags, enhance energy efficiency, and extend lining lifespan. This heightened focus on durability and high-temperature engineering continues to reinforce Germany’s influence within Europe’s advanced corundum and refractory materials segment.

Sri Lanka: Global Epicenter for Natural Sapphire Corundum and Ethical Gem Supply Chains

Sri Lanka is globally renowned for its natural corundum gemstones, particularly blue sapphires and star sapphires, which are prized for their clarity, traceability, and unique geological signatures. The Ratnapura region, often referred to as the “City of Gems,” remains one of the world’s richest natural corundum deposits, playing a central role in supplying premium-grade gemstones to the global jewelry industry. By 2025–2026, sapphire exports from Ratnapura alone carried an estimated economic impact of $780 million, underscoring their significance to the national economy.

The Sri Lankan gemstone sector is also emerging as a global model for ethical and transparent sourcing. With increasing pressure from international buyers for verifiable origin data, Sri Lanka is accelerating the deployment of Blockchain-based traceability platforms, ensuring transparent tracking from mine to market. These initiatives strengthen the country’s leadership in responsibly sourced gemstone corundum and reinforce its competitive position in the high-value natural sapphire market.

South Korea: Technology-Driven Demand for Sapphire Substrates in Displays and LEDs

South Korea’s leadership in consumer electronics and optoelectronics sustains strong national demand for synthetic sapphire (corundum), particularly for its use in high-durability display covers, smartphone watch faces, and premium wearable devices. Sapphire’s exceptional scratch resistance and clarity make it an ideal material for advanced display engineering, especially in luxury and high-performance product lines manufactured by Korean electronics giants.

The country is also a major consumer of sapphire substrates in the LED and GaN-based semiconductor industry. Sapphire wafers serve as the foundational substrate for GaN epitaxy used in high-efficiency LEDs, laser diodes, and high-electron-mobility transistors (HEMTs). As South Korea advances its semiconductor and mini-LED/micro-LED manufacturing roadmap, demand for ultra-flat, defect-minimized sapphire wafers continues to rise—cementing the country’s strategic importance to the global synthetic corundum ecosystem.

Competitive Landscape: Leading Corundum and Sapphire Producers Reshaping Global Supply

The global Corundum Industry is moderately consolidated, with a handful of vertically integrated players dominating abrasives, fused minerals, sapphire optics and coated products. These companies compete on grain engineering, purity levels, crystal growth technology, geographic footprint and security of supply. European majors such as Saint-Gobain and IMERYS control large portions of the fused alumina and abrasive grain market, while Washington Mills underpins North American fused minerals supply. In parallel, Kyocera and Rubicon Technology have carved out leadership positions in single-crystal sapphire for LEDs, semiconductors and optical defense components, and Riken Corundum remains a key brand in coated abrasives, now strengthened by its acquisition by Okamoto Industries. As demand grows for high-performance abrasives, high-temperature refractories and optical-grade sapphire, the competitive emphasis is shifting toward self-sharpening ceramic grains, high-purity fused minerals, large-diameter sapphire wafers and sustainable production practices.

Saint-Gobain accelerates next-generation sintered corundum abrasives

Compagnie de Saint-Gobain S.A. (Saint-Gobain) is a global abrasives leader, with its Norton Abrasives brand and broad portfolio of zirconia alumina, sintered bauxite, fused minerals (BFA/WFA) and ceramic grains at the core of high-performance grinding solutions. The company’s strategic focus is on high-efficiency, low-friction grinding for automotive, aerospace and precision engineering, where tool life and throughput drive total cost of ownership. Saint-Gobain invests heavily in advanced ceramic grain technology, including precision-shaped, self-sharpening grains that maintain cutting ability over longer cycles, thereby increasing productivity and reducing power consumption. Its recent launch of next-generation sintered corundum grains with ~25% higher MRR in heavy-duty grinding reinforces its ability to command premium specifications in the industrial abrasives value chain.

Imerys consolidates fused alumina leadership for refractories and fine ceramics

IMERYS S.A. is a dominant global supplier of fused minerals, particularly brown fused alumina, white fused alumina and tabular alumina, serving high-temperature refractory linings and specialty fine ceramics. Leveraging electric arc furnace technology, IMERYS emphasizes material purity, phase control and consistency, which are critical for steel and cement kiln linings and for advanced technical ceramics. Its integrated production sites across Europe provide reliable supply chains for industrial customers, reducing exposure to external raw material and logistics disruptions. Through its Climate Transition Plan announced in April 2025, IMERYS is investing in energy-efficiency and CO₂-intensity reduction across fused minerals operations, positioning its alumina products as sustainable refractory and ceramic solutions for environmentally conscious end users.

Washington Mills secures North American fused minerals and abrasive grain supply

Washington Mills Electro Minerals is a key North American producer of brown fused aluminum oxide, white fused aluminum oxide, bubble alumina and refractory grains, supporting both abrasives and high-temperature industries. Its core strength lies in providing a stable, domestic supply of fused minerals to US defense contractors, infrastructure projects and industrial manufacturers, reducing reliance on imported alumina sources. The company also targets specialty grades for coatings, blast media, lapping and polishing, where tight control over FEPA/JIS grain size distribution is essential for consistent performance. Washington Mills employs advanced sizing, separation and classification technologies to meet demanding specifications, allowing it to capture high-value share in precision surface finishing and specialized refractory applications.

Kyocera scales sapphire substrates and precision corundum-based components

Kyocera Corporation leverages its advanced materials expertise to produce single-crystal sapphire wafers and windows alongside a broad portfolio of fine ceramics components. Its strategic focus is firmly on high-tech electronics integration, particularly semiconductor and LED substrates where sapphire’s thermal conductivity, mechanical robustness and low dislocation density are decisive. Using proprietary crystal growth processes such as Kyropoulos, Kyocera is able to supply large-diameter sapphire wafers optimized for high-brightness LEDs and silicon-on-sapphire (SoS) architectures. Beyond electronics, Kyocera also manufactures sapphire rods, tubes and bearings for medical, precision mechanical and analytical equipment, capitalizing on corundum’s wear resistance and chemical inertness in harsh operating environments.

Riken Corundum expands coated abrasives capability under Okamoto

Riken Corundum Co., Ltd. specializes in coated abrasives, flexible abrasive products and bonded abrasives, with a strong brand presence in sandpaper, abrasive belts and specialty coated products for woodworking, metal finishing and surface preparation. Its core technical capability lies in optimizing the adhesion and distribution of fused alumina grains on backing materials to maximize cutting efficiency and product life. The August 2024 acquisition by Okamoto Industries is expected to scale Riken Corundum’s production, integrate it with broader polymer and material science capabilities, and expand its global market reach. This combination positions the company to offer more engineered abrasive solutions tailored to OEM and industrial customers seeking consistent surface quality and predictable belt/paper wear.

Rubicon Technology targets high-purity sapphire for optics and defense

Rubicon Technology, Inc. focuses on high-purity sapphire single crystals, large-diameter sapphire boules and optical blanks, supplying some of the most demanding defense, aerospace and industrial optics markets. The company’s specialization in large-diameter wafers (e.g., 6- and 8-inch) supports next-generation microLED displays and silicon-on-sapphire (SOS) electronics, where wafer size, defect density and thermal properties are critical to device yield. Rubicon also positions itself as a secure US-based supplier, an increasingly important differentiator for sensitive government and defense programs that require domestic, trusted supply chains for optical windows and sensor systems. Its expertise in crystal growth, orientation control and optical finishing allows Rubicon to meet stringent requirements for UV–IR transmission, scratch resistance and mechanical strength in hostile environments.

Corundum Market Report Scope

Corundum Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2035)

|

$6.4 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Origin (Natural Corundum, Synthetic Corundum), By Type – Industrial (Brown Fused Alumina, White Fused Alumina, Tabular Alumina, Monocrystalline Sapphire), By Type – Gemstone (Ruby, Blue Sapphire, Fancy Sapphires, Star Corundum), By Application (Abrasives, Refractory Materials, Electronics & Optoelectronics, Jewelry & Luxury Goods, Ceramics & Engineered Components)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain, Imerys Corp, Rusal, Washington Mills, CUMI, 3M Company, Kyocera, Monocrystal, Okamoto Industries, Rubicon Technology, Greenland Ruby, Alteo, Zhengzhou Yufa Abrasives, HarbisonWalker International, Heraeus

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corundum Market Segmentation

By Origin

- Natural Corundum

- Synthetic Corundum

By Type (Industrial)

- Brown Fused Alumina (BFA)

- White Fused Alumina (WFA)

- Tabular Alumina

- Monocrystalline Sapphire

By Type (Gemstone)

- Ruby

- Blue Sapphire

- Fancy Sapphires

- Star Corundum

By Application

- Abrasives

- Refractory Materials

- Electronics & Optoelectronics

- Jewelry & Luxury Goods

- Ceramics & Engineered Components

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Corundum Market

- Saint-Gobain

- Imerys Corp

- Rusal

- Washington Mills

- CUMI

- 3M Company

- Kyocera

- Monocrystal

- Okamoto Industries

- Rubicon Technology

- Greenland Ruby

- Alteo

- Zhengzhou Yufa Abrasives

- HarbisonWalker International

- Heraeus.

*- List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global Corundum Market in depth, mapping how alumina-based abrasives, refractories, sapphire optics and gemstone corundum are evolving across manufacturing, energy-intensive industries and high-tech electronics. It highlights demand inflection points such as ultra-high-purity α-alumina for Li-ion battery separator coatings, the shift toward cleaner synthetic fused alumina in precision grinding, and expanding use of sapphire wafers and windows in LEDs, GaN power devices and defense-grade optics. The study delivers rigorous quantitative and qualitative analysis reviews of production capacity, trade flows, technology upgrades, and sustainability measures, while benchmarking pricing dynamics against alumina feedstock and energy costs. Breakthroughs in corundum purification, advanced grain engineering, sapphire crystal growth and waste-derived tabular alumina are assessed in the context of decarbonization and circular-economy strategies. By integrating market sizing, competitive moves, policy developments and case studies of high-performance applications, this report is an essential resource for abrasives manufacturers, refractory formulators, sapphire growers, optical component suppliers, investors and strategic planners seeking data-backed insight into the future of the corundum value chain.

Scope Highlights

- Segmentation: by Origin (Natural Corundum, Synthetic Corundum); Industrial Type (Brown Fused Alumina, White Fused Alumina, Tabular Alumina, Monocrystalline Sapphire); Gemstone Type (Ruby, Blue Sapphire, Fancy Sapphires, Star Corundum); and Application (Abrasives, Refractory Materials, Electronics & Optoelectronics, Jewelry & Luxury Goods, Ceramics & Engineered Components).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2025 and detailed forecast projections from 2026 to 2034.

- Companies: Competitive profiling and strategic analysis of 15+ leading producers and technology players across fused alumina, sapphire, coated abrasives, refractories and gemstone corundum.