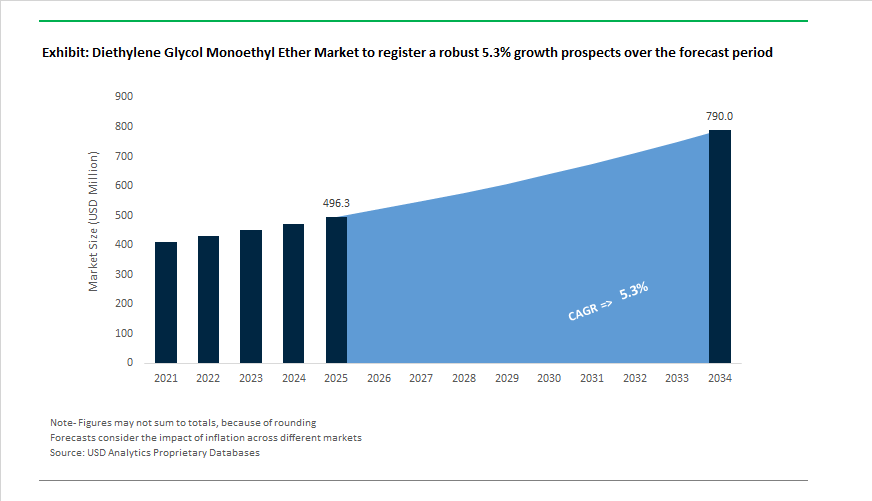

Diethylene Glycol Monoethyl Ether Market to Reach $790 Million by 2034 at 5.3% CAGR Driven by Feedstock Integration and Pharmaceutical-Grade Standards

The Diethylene Glycol Monoethyl Ether (DEGEE) Market is projected to expand from $496.3 Million in 2025 to $790 Million by 2034, registering a CAGR of 5.3%. DEGEE, widely marketed under Carbitol-type solvent grades, serves as a high-boiling glycol ether solvent in architectural coatings, printing inks, personal care formulations, agrochemical emulsions, and pharmaceutical processing. The 2024–2026 cycle marks a transition phase characterized by feedstock cost volatility in the ethylene oxide and diethylene glycol chains, stricter regulatory scrutiny in pharma-linked applications, and growing integration between upstream ethylene suppliers and downstream specialty solvent manufacturers.

In January 2024, Eastman Chemical introduced eco-friendly coating systems formulated with DEGEE, targeting low-VOC architectural materials aligned with tightening global environmental standards. During 2024–2025, India intensified regulatory inspections after incidents involving Diethylene Glycol contamination in pharmaceutical syrups. The Central Drugs Standard Control Organization conducted inspections across more than 400 facilities, triggering heightened quality benchmarks for glycols and glycol ethers. This regulatory tightening accelerated the shift toward pharmaceutical-grade DEGEE with stricter impurity thresholds, reinforcing demand for traceable, high-purity solvent streams in both domestic and export markets.

Pricing momentum strengthened through 2025 amid feedstock inflation. Dow implemented two major glycol ether price increases in North America, first in January 2025 and again in August 2025, each raising prices by $0.05 per pound. Indorama Ventures announced a DEG price adjustment in February 2025, reflecting rising production costs and tightening supply conditions for the DEG feedstock base. INEOS Oxide followed with price hikes for its E-series glycol ethers in February 2025, signaling margin compression across Europe due to high energy indices. In October 2025, Dow and MEGlobal expanded their ethylene supply agreement by an additional 100 KTA from Gulf Coast operations, strengthening feedstock security for integrated glycol ether production at Oyster Creek. This upstream integration is strategically important for stabilizing DEGEE output in a volatile ethylene oxide market.

Structural optimization continued into 2026. LyondellBasell reported a $738 million net loss for 2025 in January 2026, yet achieved $800 million in savings under its Cash Improvement Plan and raised its 2026 savings target to $1.3 billion through portfolio rationalization. BASF announced the opening of a Global Digital Hub in Hyderabad in Q1 2026, leveraging AI and digital twin modeling to refine specialty solvent manufacturing and formulation efficiency. In February 2026, Silox India secured ₹300–360 crore to expand Dahej operations, strengthening high-purity solvent capacity for pharmaceutical and export markets. Simultaneously, BASF showcased advanced plasticulture technologies at Plastindia 2026, reinforcing the integration of specialty solvent systems into high-performance polymer applications. By October 2025, Indorama Ventures launched deja™ Care for soft-skin cosmetic formulations, highlighting the diversification of DEGEE into premium personal care segments where low irritation and superior blending properties are critical. These developments illustrate a market increasingly anchored in feedstock integration, regulatory-driven quality upgrades, and value-added specialty applications across coatings, healthcare, and consumer formulations.

Trends and Opportunities Reshaping the Diethylene Glycol Monoethyl Ether (DEGE) Market

Regulatory Phase-Out Accelerates Exit from Consumer and Architectural Applications

- Regulatory scrutiny is the dominant force reshaping the DEGE market. Following the European Chemicals Agency’s expansion of the REACH SVHC Candidate List to 251 substances as of November 5, 2025, DEGE has been firmly categorized under Category 1B reprotoxicants. Manufacturers are now obligated to declare any DEGE concentration exceeding 0.1% by weight in the SCIP database, significantly raising compliance costs and liability exposure for consumer-facing products.

- As a result, architectural coatings, household cleaners, and DIY formulations are undergoing rapid reformulation. Industry disclosures from early 2025 indicate that major North American and European brand owners have embedded Chemical Strategy for Sustainability principles into their product roadmaps. This has already translated into an estimated 20% decline in DEGE-based solvent usage within the retail paints segment, with propylene-based glycol ethers emerging as preferred substitutes due to their lower toxicological classification and smoother global regulatory acceptance. This trend reflects a managed and largely irreversible exit of DEGE from high-volume consumer markets rather than a cyclical downturn.

Concentration into High-Purity Pharmaceutical and Electronics Processing Uses

- While regulatory pressure is compressing volumes, DEGE is consolidating its relevance in applications where its technical performance is difficult to replicate. In the pharmaceutical sector, high-purity DEGE is increasingly utilized as a penetration enhancer in topical drug delivery systems. Marketed under pharmaceutical-grade specifications, it plays a critical role in dermatological formulations by enabling the formation of an intracutaneous drug reservoir for poorly water-soluble actives. Clinical and formulation data from 2024–2025 highlight its continued use in acne and anti-inflammatory therapies, where controlled skin permeation directly impacts therapeutic efficacy.

- In electronics manufacturing, DEGE is valued as a high-boiling-point tail solvent in printed electronics and conductive ink systems. Trials conducted in late 2024 demonstrated that silver-flake inks formulated with DEGE achieved approximately 15% higher electrical conductivity than ethanol-based systems. This performance gain is linked to DEGE’s ability to slow evaporation during printing, ensuring uniform particle orientation and minimizing defects. As printed electronics scale across sensors, RFID tags, and flexible circuits, this property is reinforcing DEGE’s position in niche but high-margin electronics applications.

Critical Solvent for Security Inks and Anti-Counterfeiting Applications

- One of the most resilient opportunities for DEGE lies in security and banknote inks, where performance requirements and regulatory exemptions create a high barrier to substitution. DEGE is among the limited number of solvents compatible with both cellulose acetate butyrate and nitrocellulose, which are the backbone resins for currency, passport, and high-security document printing. As governments continue currency modernization and anti-counterfeiting upgrades through 2032, the demand for precisely tuned ink rheology remains robust.

- In 2025, currency printing programs across the Asia-Pacific region increasingly favored DEGE due to its controlled evaporation profile. This property prevents premature skinning in ink reservoirs while enabling rapid downstream curing and chemical resistance during high-speed, multilayer printing. These characteristics make DEGE a mission-critical solvent in gravure and intaglio printing, positioning it within a stable niche where performance reliability outweighs regulatory risk.

Reaction Medium for Liquid Crystals and High-Performance Condensation Polymers

- Advanced materials manufacturing represents another structurally attractive growth avenue for DEGE. In liquid crystal synthesis, its high polarity and elevated boiling point make it an effective solvent for selective crystallization and purification. Industrial synthesis data from early 2025 indicates that DEGE-enabled purification can achieve liquid crystal intermediate purities of up to 99.999 %, a threshold required for OLED, 8K, and high-refresh-rate display panels. As display manufacturers push tighter defect tolerances, solvent selection is becoming a strategic variable rather than a cost decision.

- Additionally, DEGE is gaining attention as an azeotroping agent in condensation polymer reactions, particularly for high-performance polyimides and specialty polyesters. By facilitating efficient water removal during polymerization, DEGE supports the production of ultra-thin, heat-resistant films used in flexible circuits. This application is expanding in response to aerospace and defense demand for lightweight, thermally stable substrates in next-generation satellites, drones, and avionics platforms planned for 2026 and beyond.

Diethylene Glycol Monoethyl Ether (DEGEE) Market Share and Segmentation Insights

DEGEE Market Share by Application : Solvents and Solubilizers Anchor Demand Across Pharma and Coatings

Solvents and solubilizers account for 45% of global diethylene glycol monoethyl ether (DEGEE) consumption in 2025, underscoring its importance as a high-performance glycol ether solvent with amphiphilic properties. DEGEE’s ability to dissolve both polar and non-polar compounds makes it indispensable in pharmaceutical formulations, cosmetics, and specialty industrial applications requiring uniform dispersion of active ingredients. Penetration enhancers form the second-largest segment, driven by DEGEE’s widespread use in topical and transdermal drug delivery systems where it temporarily modifies skin barrier function to improve bioavailability without irritation. Coalescing agents represent another significant application in waterborne coatings and adhesives, supporting ambient film formation, flow, and leveling in low-VOC architectural and industrial paints. Chemical intermediates remain a niche, supplying DEGEE-derived esters and ethers for specialty synthesis, while additive applications leverage its coupling, wetting, and stabilization properties in advanced formulations across multiple end markets.

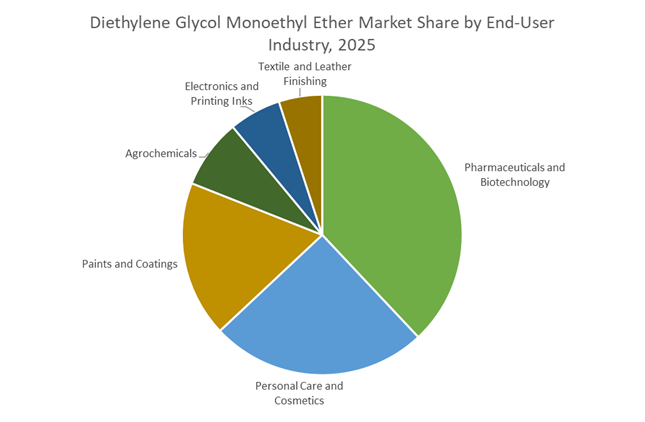

DEGEE Market Share by End-User Industry : Pharmaceuticals Lead as Personal Care and Coatings Expand

The pharmaceuticals and biotechnology sector commands 38% of DEGEE demand, positioning it as the dominant end-user industry in 2025. DEGEE is extensively used as a solubilizer, penetration enhancer, and processing solvent in topical, transdermal, and parenteral drug products, supported by its established safety profile and regulatory acceptance. Personal care and cosmetics represent a major secondary segment, incorporating DEGEE into skincare, hair care, and color cosmetics as a solvent, humectant, and penetration enhancer for premium formulations. Paints and coatings follow, utilizing DEGEE as a coalescing agent in waterborne architectural and industrial coatings to improve film integrity under low-VOC requirements. Agrochemicals maintain steady consumption through DEGEE-based co-formulants that enhance pesticide stability and spray performance. Electronics, printing inks, and textile and leather finishing remain smaller but strategic niches, relying on DEGEE’s solvency and controlled evaporation for precision processing and uniform surface treatment.

Competitive Landscape of the Diethylene Glycol Monoethyl Ether (DEGEE) Market

The Diethylene Glycol Monoethyl Ether (DEGEE) market in 2026 is shaped by restructuring petrochemical majors and specialty solvent innovators competing on LVP-VOC compliance, bio-based DEGEE production, ethylene oxide integration, and premium end-use penetration across coatings, EV fluids, pharmaceuticals, electronics, and industrial cleaning.

Dow Inc. restructures Europe while defending global DEGEE leadership through Sadara integration

Dow Inc. remains a dominant DEGEE supplier, even as its 2026 strategy pivots toward aggressive footprint optimization. In February 2026, Dow launched its Transform to Outperform plan, shutting its Böhlen ethylene cracker and Schkopau vinyl chain in Germany, moves expected to tighten European E-series glycol ether supply and constrain regional DEGEE availability through 2027. Despite this, Dow preserves a strong global cost advantage via its Sadara joint venture in Saudi Arabia, a primary export hub for Asia. Strategically, Dow is reallocating capital toward AI-driven autonomous production and fulfillment, targeting a $2 billion EBITDA uplift by 2027, while protecting high-value solvent derivatives from basic olefin overcapacity.

Eastman Chemical positions DEGEE as a premium LVP-VOC solvent for coatings and pharma delivery

Eastman Chemical Company has established itself as the quality leader in DEGEE, emphasizing high-compliance, low-VOC formulations. Its flagship Eastman™ DE Solvent carries LVP-VOC exemption status in California, making it a preferred choice for eco-conscious architectural coatings. In 2026, Eastman introduced the DE-HG Solvent blend, combining DEGEE with ethylene glycol to enhance freeze-thaw stability and wet-edge control in latex paints. The company also dominates personal care and pharmaceutical applications, where its high-purity grades improve topical drug absorption. Eastman continues shifting away from commodity cycles, expanding its circular economy portfolio using molecular recycling to deliver sustainable DEGEE-based chemical building blocks.

Clariant AG advances REACH-compliant DEGEE for EV brake fluids and industrial coatings

Clariant AG has transitioned from volume manufacturing to specialized DEGEE solutions for functional fluids and coatings. Marketed under DIETHYLENGLYKOL EE, its DEGEE serves as both solvent and defoamer in solvent-borne industrial paints. During 2025 to 2026, Clariant expanded its Functional Fluids division, integrating DEGEE into advanced EV brake fluid formulations to support electric mobility growth. Backed by strong EMEA supply chains and deep expertise in ethylene oxide derivatives, Clariant delivers customized alkoxylation services. Its core strength lies in regulatory leadership, maintaining front-runner status in REACH compliance and ensuring all DEGEE products meet stringent 2026 consumer chemical safety standards.

India Glycols Limited pioneers 100% bio-based DEGEE through green ethylene oxide chemistry

India Glycols Limited is the global trailblazer in bio-based DEGEE, producing renewable glycol ethers from molasses rather than petrochemicals. In January 2026, IGL secured NCLT approval for a strategic demerger, sharpening focus on its Performance Chemicals business. Its Bio-DEGEE is rapidly gaining traction in Europe as a drop-in replacement for fossil-derived solvents. Leveraging its position as the world’s first producer of green ethylene oxide, IGL holds a unique monopoly on 100% bio-based DEGEE. With strong APAC exposure, the company supplies India’s expanding textile and architectural coatings sectors, capitalizing on sustainability-driven solvent demand.

LyondellBasell targets aviation and industrial cleaning with high-efficiency DEGEE production

LyondellBasell Industries operates as a value chain powerhouse, delivering industrial-scale DEGEE from one of the most efficient production lines on the US Gulf Coast. Its Glycol Ether DE features 0.989 g/cc density and full water miscibility, supporting consistent performance across applications. In early 2026, LyondellBasell launched a Cash Improvement Plan to optimize European solvent assets, prioritizing high-margin intermediates. The company is a leading DEGEE supplier to aviation, where it functions as a de-icing additive and fuel system icing inhibitor (FSII). Strategically, LyondellBasell is targeting industrial cleaning, the fastest-growing DEGEE segment, driven by demand for low-toxicity grease-removal solvents.

Nippon Nyukazai delivers ultra-pure DEGEE for electronics, pharma, and optical materials

Nippon Nyukazai Co., Ltd. is Asia’s precision specialist, offering one of the industry’s broadest glycol ether portfolios. Its proprietary purification technologies enable ultra-low odor and low-metallic DEGEE grades, critical for semiconductor and high-end electronics manufacturing. DEGEE forms part of a catalog exceeding 500 specialty surfactants and ethers, built on advanced EO/PO polymerization. In 2026, Nippon Nyukazai advanced Aminoion®, a halogen-free ionic liquid leveraging glycol ether chemistry for anti-static and anti-fog optical films. The company’s strategic focus on halogen-free and bio-compatible materials positions it strongly in Japan and South Korea’s pharmaceutical synthesis and electronic materials markets.

United States: Pharma-Led Demand Resilience and Domestic Supply Preference

The United States diethylene glycol monoethyl ether market in 2025 has been characterized by rapid price transmission and prioritization of pharmaceutical-grade supply. Effective March 15, 2025, Dow implemented a $0.04 per pound increase across its glycol ether portfolio, including DEGEE derivatives. This followed an earlier $0.05 per pound increase in January 2025, reflecting sustained pressure from energy costs, labor inflation, and strong downstream pull from prestige beauty and regulated pharmaceutical applications. Unlike bulk coating solvents, DEGEE has demonstrated limited price elasticity due to its functional role as a penetration enhancer and stabilizing co-solvent in sensitive formulations.

Supply chain fragility further reinforced domestic sourcing. The February 2025 Arctic Blast in the U.S. Gulf Coast caused freeze-offs in ethylene oxide feedstock units, leading to temporary force majeure conditions. During this period, producers reallocated high-purity DEGEE volumes toward essential pharmaceutical customers, underscoring its criticality in regulated value chains. From a demand perspective, the FDA recorded a notable rise in New Drug Applications utilizing DEGEE as a dermal penetration enhancer, including topical gels such as 5% dapsone. NIH-backed studies published in 2025 validated DEGEE’s intracutaneous depot behavior, improving therapeutic efficacy while lowering systemic exposure risks. Parallel to this, executive tariff measures introduced in February 2025 shifted procurement away from imports and toward integrated domestic suppliers such as Eastman and Dow. This trend has been reinforced by a 14.6% year-over-year surge in U.S. personal care e-commerce sales, prompting formulators to lock in DEGEE supply for premium skincare launches planned through 2026.

China: Capacity-Led Expansion Under Export Control Constraints

China’s DEGEE market is entering a structurally transformative phase, driven by large-scale petrochemical integration and tighter export governance. The $6.4 billion SABIC Fujian Petrochemical Complex reached 87% completion by Q3 2025, with CEO Abdulrahman Al-Fageeh confirming that ethylene glycol derivatives, including E-series ethers, will commence production in the second half of 2026. This project is expected to materially enhance China’s self-sufficiency in high-purity glycol ethers while reducing reliance on coastal import terminals.

In parallel, BASF announced cumulative capital expenditures of €16 billion through 2028, with the Zhanjiang Verbund site as a central pillar. The new steam cracker and downstream ethylene oxide units scheduled for 2025–2026 start-up will significantly increase regional DEGEE availability for electronics, coatings, and agrochemical formulations. However, policy oversight has intensified. Effective November 10, 2025, China’s Ministry of Commerce enforced Announcement 2025/73, adding North American destinations to the export licensing regime for precursor chemicals. This has increased documentation and lead times for DEGEE exports. At the same time, the Ministry of Agriculture proposed revised rules for export-only pesticides, which is expected to lift DEGEE consumption by 12–15% as a co-solvent in high-load liquid formulations destined for overseas markets. The net effect is a market that is expanding in volume but increasingly segmented between domestic consumption and tightly regulated exports.

India: Localization Momentum and Regulatory Quality Enforcement

India’s DEGEE market is being reshaped by policy-driven localization and stricter quality controls. As of June 2025, the Department of Pharmaceuticals reopened applications under the Production Linked Incentive scheme with a sharper focus on key starting materials. This has directly incentivized Indian manufacturers to scale anhydrous DEGEE production for injectable, topical, and transdermal drug delivery systems. DEGEE is increasingly viewed as a strategic solvent rather than a commoditized ether, particularly in complex formulations where impurity thresholds are critical.

Infrastructure development is reinforcing this shift. At the 2025 Gujarat Chem & Petchem Conference, state authorities highlighted new specialty chemical parks in Surat and Dahej, designed to attract investments in high-purity solvent manufacturing. These hubs are targeting a reduction in India’s current 22% import dependence on premium glycol ethers. Regulatory tightening has further altered market behavior. In early 2025, the Ministry of Chemicals and Fertilizers enforced mandatory BIS standards for glycol ethers, explicitly restricting the use of technical-grade DEGEE in consumer and healthcare products. This followed global safety alerts linked to ethylene glycol contamination, and it has raised compliance costs while improving long-term credibility for domestically produced DEGEE.

Germany: Energy-Driven Premiums and Circular Solvent Pathways

Germany represents a high-cost but strategically important DEGEE market within the European Union. In mid-2025, German spot prices for DEGEE reached $2,021 per metric ton, the highest regional benchmark globally. This premium reflects elevated energy costs, the cumulative impact of REACH fee increases effective November 2025, and the cost of compliance with tightening occupational exposure limits. Despite these pressures, demand remains robust due to DEGEE’s alignment with low-VOC and high-performance coating requirements.

Strategic investments are reinforcing this position. BASF announced the construction of a new sustainable automotive paint production plant in Münster, scheduled for 2025 start-up. The facility will utilize low-product-carbon-footprint DEGEE as a primary solvent to meet the EU’s stricter 2026 VOC thresholds. Additionally, BASF’s Ludwigshafen site initiated a modernization program in 2025, targeting completion in 2026, to integrate mass-balanced bio-feedstocks into its etherification units. This circular economy pilot positions DEGEE within Europe’s broader transition toward traceable, low-carbon solvent systems without compromising formulation performance.

Comparative Overview: Diethylene Glycol Monoethyl Ether Market by Region

Diethylene Glycol Monoethyl Ether Market Country Level Snapshot

|

Region

|

Core Demand Driver

|

Policy or Structural Catalyst

|

Market Outcome

|

|

United States

|

Pharma and prestige personal care

|

Tariffs, FDA scrutiny, EO supply shocks

|

Domestic sourcing and price resilience

|

|

China

|

Integrated petrochemical expansion

|

Export licensing and pesticide reform

|

Rising capacity with controlled exports

|

|

India

|

Pharmaceutical localization

|

PLI incentives and BIS enforcement

|

Import substitution with higher purity norms

|

|

Germany

|

Low-VOC automotive coatings

|

REACH fees and energy costs

|

Premium pricing with circular innovation

|

Diethylene Glycol Monoethyl Ether Market Report Scope

Diethylene Glycol Monoethyl Ether Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$496.3 Million

|

|

Market Size (2034)

|

$790 Million

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Purity Grade (Pharmaceutical and Cosmetic Grade, Industrial Grade, Low-VOC Grade), By Application (Penetration Enhancers, Coalescing Agents, Solvents and Solubilizers, Chemical Intermediates, Additives), By End-User Industry (Pharmaceuticals and Biotechnology, Personal Care and Cosmetics, Paints and Coatings, Agrochemicals, Electronics and Printing Inks, Textile and Leather Finishing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., BASF SE, SABIC, LyondellBasell Industries N.V., Eastman Chemical Company, Huntsman Corporation, Gattefossé, Clariant AG, INEOS Group Limited, Indorama Ventures Public Company Limited, Nippon Shokubai Co., Ltd., Jiangsu Yida Chemical Co., Ltd., Shiny Chemical Industrial Co., Ltd., Balaji Amines Limited, Tokyo Chemical Industry Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diethylene Glycol Monoethyl Ether Market Segmentation

By Purity Grade

- Pharmaceutical and Cosmetic Grade

- Industrial Grade

- Low-VOC Grade

By Application

- Penetration Enhancers

- Coalescing Agents

- Solvents and Solubilizers

- Chemical Intermediates

- Additives

By End-User Industry

- Pharmaceuticals and Biotechnology

- Personal Care and Cosmetics

- Paints and Coatings

- Agrochemicals

- Electronics and Printing Inks

- Textile and Leather Finishing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Diethylene Glycol Monoethyl Ether Industry

- Dow Inc.

- BASF SE

- SABIC

- LyondellBasell Industries N.V.

- Eastman Chemical Company

- Huntsman Corporation

- Gattefossé

- Clariant AG

- INEOS Group Limited

- Indorama Ventures Public Company Limited

- Nippon Shokubai Co., Ltd.

- Jiangsu Yida Chemical Co., Ltd.

- Shiny Chemical Industrial Co., Ltd.

- Balaji Amines Limited

- Tokyo Chemical Industry Co., Ltd.

*- List not Exhaustive