E-Series Glycol Ether Market to Reach $5.6 Billion by 2034 at 4.8% CAGR Amid Pricing Discipline, EO Rationalization, and High-Purity Semiconductor Demand

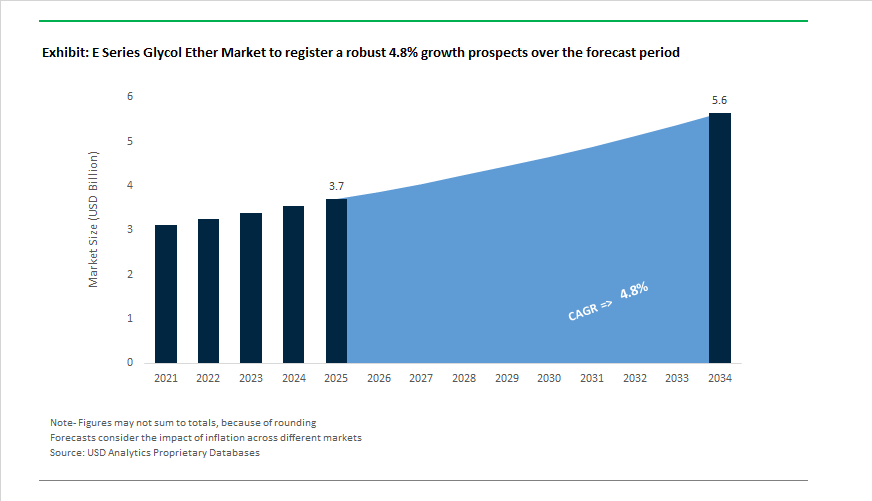

The E Series Glycol Ether Market is projected to grow from $3.7 billion in 2025 to $5.6 billion by 2034, registering a CAGR of 4.8%. Market performance through 2024–2026 reflects a structurally tightening ethylene oxide (EO) value chain, disciplined pricing actions by major producers, and a shift toward bio-based and high-purity specialty grades. In March 2025, Dow implemented a price increase across its DOWANOL™ E-series and P-series glycol ethers in North America, responding to tightening supply fundamentals and recovering demand from architectural coatings and industrial cleaning sectors after a prolonged inventory destocking phase. This upward pricing trajectory continued into 2026, with Eastman announcing an off-list increase effective February 12, 2026 across North America and Latin America, aimed at restoring specialty materials margins amid elevated operational costs.

INEOS Oxide followed with a $0.03 per pound price adjustment effective February 15, 2026 for select E-series glycol ethers, including EB, DB, and HB grades. These coordinated actions highlight the industry’s attempt to recalibrate margins following several quarters of feedstock volatility and distribution cost escalation. Complementing this trend, BASF increased prices for select diols and derivatives in April 2025, signaling broader inflationary pressure across the oxygenated solvent chain. Collectively, these pricing movements illustrate a shift from volume-driven competition toward disciplined profitability management across integrated EO producers.

Structural realignment in Europe has reshaped supply dynamics. In September 2025, Clariant confirmed the decommissioning of one of its two EO units at Gendorf, Germany, reflecting the rationalization of derivative capacity in response to high regional energy costs and structural oversupply. Despite these pressures, INEOS committed €250 million in 2025 to modernize its Lavera steam cracker and derivatives complex in France, reinforcing its long-term European footprint. Meanwhile, INEOS completed the $700 million acquisition of LyondellBasell’s EO and derivatives business in 2024, including the Bayport Underwood site in Texas. This transaction significantly expanded INEOS’s North American production base for E-series glycol ethers, strengthening its competitive position against Dow and BASF.

Portfolio optimization among global majors further influences supply allocation. In January 2026, LyondellBasell advanced its Cash Improvement Plan, targeting $1.3 billion in cumulative improvements by year-end 2026 through European asset divestments and higher-margin glycol sales into de-icing and industrial cleaning markets. These downstream sectors remain core demand drivers for E-series glycol ethers, particularly for EB and DB grades used in heavy-duty cleaning formulations and airport de-icing fluids.

Sustainability and advanced applications are increasingly shaping growth vectors. In early 2024, Dow introduced a new line of bio-based glycol ethers derived from renewable feedstocks, enabling formulators in paints and coatings to meet low-VOC compliance requirements. Parallel circular initiatives emerged when Shell announced expanded research into glycol ether recovery and recycling technologies during 2024, aligning solvent use with broader circular economy targets.

On the high-end spectrum, KH Neochem launched semiconductor-grade E-series glycol ethers in 2024, engineered for ultra-low metal impurity profiles required in advanced photoresist stripping and wafer cleaning processes. This development aligns with expanding chip fabrication capacity in Taiwan and South Korea, where electronic-grade solvent demand is accelerating. The E-series glycol ether market is increasingly characterized by regional capacity rebalancing, specialty grade differentiation, and margin-focused pricing strategies across integrated EO producers.

Trends and Opportunities in the E-Series Glycol Ether Market

Accelerated Substitution of E Series Glycol Ethers with Safer Alternatives

- Regulatory pressure linked to reproductive toxicity classifications is forcing a decisive contraction of traditional E-series glycol ethers such as 2-ethoxyethanol and 2-ethoxyethyl acetate in consumer and professional use environments. Under EU Regulation 2024/2865, effective from December 2025, hazard communication rules were significantly tightened, including stricter labeling requirements and explicit restrictions on the sale of reproductive toxicants through refill stations. This has materially reduced the commercial viability of E-series glycol ethers in retail cleaning, personal care, and DIY formulations across Europe.

- In response, formulators in North America and Europe initiated wide-scale reformulation programs during 2025, replacing conventional ethylene-based solvents with propylene-based or bio-derived glycol ether blends that deliver comparable solvency with improved toxicological profiles. This shift is not optional. Updated Safety Data Sheet requirements for Substances of Very High Concern have made E-series retention a compliance risk for multinational consumer goods companies.

- The economic impact of this transition is already visible. In February 2025, Dow Chemical implemented price increases of up to USD 0.15 per pound across multiple glycol ether grades, citing higher costs associated with compliant raw materials, additional purification steps, and reformulated performance blends. As a result, E-series glycol ethers are steadily losing volume share in price-sensitive segments while maintaining relevance only where substitution compromises performance.

Rising Demand for Ultra-High-Purity Grades in Semiconductor Fabrication

- In contrast to consumer markets, semiconductor manufacturing is driving a structurally resilient and technically demanding demand stream for E-series glycol ethers. As advanced logic and memory nodes move below 5 nanometers, tolerance limits for metallic and ionic impurities in solvents have tightened to parts-per-trillion levels. This has repositioned select E-series glycol ethers as precision electronic materials rather than commodity solvents.

- In October 2025, leading US chemical producers introduced a new generation of ultra-high-purity glycol ethers specifically engineered for semiconductor cleaning and advanced packaging applications, including 2.5D and 3D integrated circuits. These materials are critical in edge bead removal and photoresist thinning, where solvent purity directly affects pattern fidelity and yield.

- Companies such as Eastman have expanded their EastaPure product line to offer ethylene glycol monobutyl ether with tightly controlled trace metal profiles for lithography processes. These electronic-grade solvents are now specified for ArF and KrF photoresists, where they function as viscosity modifiers and film-forming aids without introducing defect risks.

- Strategic investment is reinforcing this trend. In February 2025, a major Japanese petrochemical group partnered with a global solvent supplier to co-develop next-generation E-series derivatives aligned with the purity requirements of fabs operated by Intel and TSMC under the US CHIPS Act. This confirms that while volume growth is limited, ultra-high-purity E-series grades are becoming indispensable inputs in advanced semiconductor ecosystems.

Formulation Enabler for Next-Generation Low-VOC Industrial Coatings

- Despite regulatory pressure, E-series glycol ethers retain a critical role in industrial coatings where precise solvency and film formation are required under increasingly strict air quality standards. The updated US EPA AIM Rule has pushed coatings formulators toward low-VOC waterborne systems, where E-series ethers such as ethylene glycol monobutyl ether continue to function as highly effective coalescing and coupling agents.

- By August 2025, US architectural and industrial coatings producers had increased the selective use of compliant E-series glycol ethers to balance hardness, open time, and drying behavior. In these formulations, EGBE enables a 10 to 15% reduction in total VOC content without compromising gloss or durability, reinforcing its position as a performance benchmark rather than a commodity solvent.

- Innovation is extending this opportunity. In July 2025, Nouryon introduced the Ethylan EF-60 additive, designed to stabilize VOC-free coatings during low-temperature storage. This highlights an adjacent growth avenue where E-series producers can supply stabilization and performance chemistry that supports the broader transition to sustainable waterborne resins.

- Regionally, Asia-Pacific remains the most attractive volume market for this application. Rapid urbanization, high humidity, and temperature variability in these markets continue to favor E-series-based coalescents that deliver consistent film formation under challenging climatic conditions.

Role in Lithium-Ion and Next-Generation Battery Electrolytes

- A high-value, technology-driven opportunity is emerging for specialized E-series derivatives in lithium-based battery systems. Certain glycol ethers, particularly glymes, are gaining attention as functional electrolyte additives that enhance safety, ionic conductivity, and thermal stability.

- Research published in August 2025 demonstrated that diethylene glycol diethyl ether used in ternary electrolyte blends can achieve ionic conductivity of 3.8 mS per centimeter at 25 degrees Celsius when combined with non-flammable hydrofluoroethers. These formulations exhibit flash points up to 74 degrees Celsius, providing a pathway toward safer electrolytes for high-energy-density batteries.

- Further studies released in early 2025 through OSTI highlighted the potential of fluorinated glycol ethers to stabilize lithium-metal battery cycling. By improving anodic stability, these ethers enable the use of high-nickel cathodes such as NMC811 while suppressing dendrite formation, a primary failure mechanism in next-generation cells.

- From a market perspective, this positions electronic-grade E-series derivatives as premium inputs in advanced battery chemistries. As OEMs and cell manufacturers seek to reduce thermal runaway risk by 20 to 30% compared with conventional carbonate electrolytes, demand for high-purity, non-flammable glycol ether additives is expected to rise, creating a defensible niche for producers capable of meeting battery-grade quality and consistency standards.

E Series (Ethylene-Based) Glycol Ether Market Share and Segmentation Insights

Ethylene Glycol Monobutyl Ether Commands Majority Share Across Solvent Applications

Ethylene Glycol Monobutyl Ether (EGBE) accounts for 52% of total E Series glycol ether market share in 2025, reinforcing its dominance as a versatile solvent across paints and coatings, industrial cleaners, and chemical intermediates. Its optimal balance of solvency power, controlled evaporation rate, partial water miscibility, and cost efficiency makes it indispensable in hard surface cleaners, degreasers, and architectural coatings. Ethylene Glycol Monoethyl Ether (EGEE) holds a significant share, particularly in automotive coatings, wood finishes, and specialty printing inks where film formation and surface leveling are critical. Ethylene Glycol Monomethyl Ether (EGME) remains important in niche industrial coatings and resin processing, though regulatory restrictions in certain regions temper growth. Ethylene Glycol Monopropyl Ether and Monohexyl Ether occupy smaller but high-value segments in electronics cleaning, photoresist formulations, and high-performance coatings, where tailored evaporation characteristics and premium-grade purity justify higher pricing.

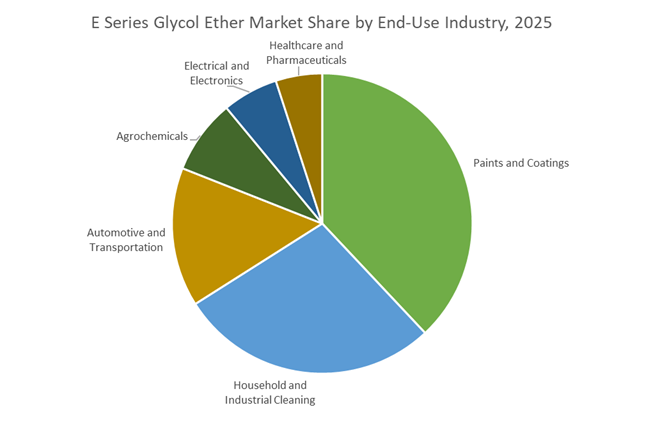

Paints and Coatings Sector Drives Primary Demand for E Series Glycol Ethers

The paints and coatings industry represents 38% of end-use consumption in 2025, positioning it as the largest revenue-generating segment in the E Series glycol ether market. These solvents function as coalescing agents and performance enhancers in waterborne and solvent-borne coatings, improving flow, leveling, and film integrity across architectural, industrial, and automotive applications. Household and industrial cleaning follows as a major segment, heavily utilizing EGBE for grease removal and oil solubilization in multipurpose cleaners and laundry formulations. Automotive and transportation applications incorporate glycol ethers into brake fluids, surface treatments, and specialty coatings requiring low-temperature fluidity and solvency. Agrochemical formulations depend on glycol ethers as co-solvents in pesticide and herbicide blends, enhancing stability and spray performance. Electrical and electronics manufacturing represents a growing segment requiring high-purity solvents, while healthcare and pharmaceutical usage remains limited due to strict regulatory oversight and safety considerations.

Competitive Landscape of the E Series Glycol Ether Market

The E Series Glycol Ether market in 2026 is characterized by deep vertical integration, aggressive sustainability roadmaps, and rising demand from water-based coatings, electronics cleaning, industrial degreasers, and low-VOC formulations, with Tier-1 producers competing on ethylene oxide integration, carbon footprint reduction, and specialty solvent performance.

Integrated ethylene oxide leadership and bio-based E-Series innovation at Dow Inc.

Dow remains the undisputed global leader in the E Series Glycol Ether market, controlling over 25% of worldwide capacity, including its 50% stake in Sadara. Its DOWANOL™ E-Series (EGBE, EGPE) continues to be the gold standard for water-based architectural coatings and industrial cleaners. In 2025–2026, Dow introduced Ecolibrium™ and Renuva™ E-series, incorporating bio-based and recycled feedstocks to cut carbon intensity by up to 30%. Leveraging the Sadara Chemical Company JV in Saudi Arabia, Dow secures low-cost ethylene oxide for MEA and APAC supply chains. Massive U.S. Gulf Coast integration keeps Dow in the first quartile of cash costs, reinforcing its role as the global merchant market price setter.

Circular economy driven E-Series production anchored by Verbund integration at BASF SE

BASF positions its E Series Glycol Ether portfolio around sustainable solvency and circular manufacturing, embedding production across its global Verbund sites. In late 2025, BASF achieved ISCC PLUS certification at Ludwigshafen, enabling Ccycled® E-series glycol ethers derived from chemically recycled plastic waste. The company dominates electronics and semiconductor cleaning, where ultra-high purity E-series solvents are essential for PCB fabrication. BASF is rolling out PCF Zero glycol ethers, produced using renewable energy and mass-balance raw materials. With full backward integration into ethylene oxide and alcohols, BASF shields customers from feedstock volatility while delivering compliant, low-carbon solvents to coatings, electronics, and specialty chemical formulators.

North American merchant supply strengthened through EO acquisition by INEOS Group Ltd.

INEOS rapidly emerged as a top-tier E Series Glycol Ether supplier after acquiring LyondellBasell’s Ethylene Oxide and Derivatives business for $700 million, including the 165 kt Bayport Underwood glycol ethers plant in Texas. By 2026, INEOS controls one of North America’s largest EO-derivative portfolios, primarily serving paints and coatings manufacturers with high-volume supply. Its strategy centers on operational resilience, offering multi-source logistics security for industrial customers navigating trade disruptions. INEOS focuses heavily on bulk merchant sales, pairing asset reliability with optimized distribution to deliver highly competitive pricing, making it a preferred partner for large-scale coating, cleaning, and formulation producers.

Cost-advantaged E-Series expansion powered by Middle East feedstocks at SABIC

SABIC leverages unparalleled access to low-cost ethane and ethylene to position itself as the most cost-effective E Series Glycol Ether supplier in the Eastern Hemisphere. Its SABIC® Butoxy Glycol Ether (EB) is widely adopted in heavy-duty degreasers and agrochemical formulations, offering balanced hydrophilic and hydrophobic performance. SABIC is also expanding specialty polyphenylene ether capacity in Asia, supporting downstream electronics growth tied to 5G and AI data centers. With strong traction in pesticide and insecticide coupling agents, SABIC’s feedstock advantage ensures profitability during global price cycles while strengthening its footprint across APAC and MEA solvent markets.

Premium specialty E-Series and formulation consulting leadership at Eastman Chemical Company

Eastman differentiates itself through high-purity E Series Glycol Ethers tailored for premium applications where odor profile and performance outweigh bulk pricing. Its ethylene glycol propyl ether (EGPE) is increasingly replacing EGBE in industrial wipes and precision degreasers, driven by superior solvency and low odor. Eastman introduced low-odor E-series blends for indoor architectural paints, helping customers achieve 2026 indoor air quality certifications. The company’s molecular recycling platform supports circular precursors for oxygenated solvents, while its bench-level formulation consulting enables coatings manufacturers to meet evolving VOC regulations without compromising film formation or durability.

China: Integrated Verbund Scale-Up and Electronics-Grade Self-Sufficiency

China is rapidly repositioning its E Series Glycol Ether market around integrated petrochemical scale and electronics-grade specialization. In October 2025, BASF inaugurated its Neopentyl Glycol plant at the Zhanjiang Verbund site, lifting global capacity to 335,000 metric tons. While NPG is a distinct product, the significance for E-series glycol ethers lies in the site’s deep integration with ethylene oxide derivatives and its ability to serve low-emission coatings and high-purity solvent demand across Asia-Pacific. The Zhanjiang complex operates on advanced energy-efficient production systems, reinforcing China’s cost and compliance advantage in waterborne coatings and industrial solvent formulations.

Sustainability and electronics localization are converging as core drivers. BASF’s launch of reduced Product Carbon Footprint (rPCF) intermediates at Zhanjiang directly aligns with China’s 2026 low-carbon intermediate mandate, supported by 100% renewable electricity at the site. At the same time, MIIT’s 2025 roadmap has accelerated a pivot in Nanjing and Daya Bay toward electronics-grade glycol ethers used in 2nm wafer fabrication and high-density PCB cleaning. Domestic producers are targeting 70% self-sufficiency by late 2026, reducing dependence on imported ultra-purity solvents. In parallel, the 2025 Green Shipbuilding Initiative has pushed Chinese shipyards toward waterborne epoxy systems, structurally increasing demand for E-series glycol ethers as high-efficiency coalescing agents in marine and protective coatings.

United States: Pricing Volatility, Regulatory Scrutiny, and Niche Demand

The U.S. E Series Glycol Ether market in 2025 is defined by sharp pricing movements and heightened regulatory oversight. Dow Chemical Company implemented multiple price increases across North America, beginning with a $0.07 per pound hike on E-series products such as Propyl CELLOSOLVE™ in March 2025, followed by further $0.10 per pound increases in April. These adjustments reflect persistent raw material volatility and robust downstream demand from cosmetics and agrochemical formulations, where E-series ethers remain critical for solubility and formulation stability.

Regulatory developments are reshaping procurement and compliance strategies. In September 2025, the U.S. EPA proposed amendments to the TSCA risk evaluation framework that expand scrutiny to fenceline community exposure and occupational controls. For E-series glycol ethers, this means additional data submissions and risk management documentation by May 2026. Operational resilience was tested in February 2025 when an Arctic blast caused freeze-offs along the U.S. Gulf Coast, temporarily tightening supply and driving secondary market price spikes for Ethylene Glycol Monobutyl Ether used in architectural coatings. Despite these disruptions, Dow has continued to expand its DOWANOL™ EPH portfolio, prioritizing high-purity grades for the prestige beauty segment, which recorded 7% growth in late 2024 and increasingly demands traceable, low-impurity solvents.

Saudi Arabia: Downstream Diversification and EO Derivative Localization

Saudi Arabia’s E Series Glycol Ether trajectory is closely tied to downstream diversification and regional supply-chain localization. In December 2025, SABIC announced an incremental expansion of its specialty oligomers portfolio, which relies on glycol ether intermediates. Spanning assets in Saudi Arabia and the Netherlands, the project is scheduled for completion in H2 2026 and is aimed squarely at supplying advanced PCB materials for 5G and AI data-center infrastructure.

Electrification and regional integration are reinforcing demand. Under SABIC’s BLUEHERO™ initiative, E-series derivatives are being deployed as thermal management fluids in EV battery systems for 2026 vehicle platforms, valued for their chemical resistance and heat-transfer efficiency. At the 19th GPCA Annual Forum in December 2025, executives from Saudi Aramco and SABIC emphasized the strategic need to localize ethylene oxide derivative production. This push is designed to reduce the Middle East’s reliance on imported E-series technical grades and position the region as a competitive exporter of specialty solvents.

Germany (European Union): Compliance-Driven Process Optimization

Germany’s E Series Glycol Ether market is being reshaped by regulatory pressure and digital efficiency gains. Updated REACH Annex XVII restrictions effective in late 2025 have tightened controls on VOC-intensive solvents, accelerating the adoption of closed-loop recovery systems and metal-free dispensing solutions for E-series ethers used in industrial degreasing. These measures are not merely compliance-driven but are increasingly seen as cost-stabilization tools amid high European energy prices.

At the production level, BASF has committed €200 million to deploy Digital Twin technology at its Ludwigshafen Verbund site. According to the company’s 2025 Factbook, this investment enables real-time optimization of E-series production lines, cutting energy intensity by 12% for the 2026 cycle. This positions Germany as a hub for digitally optimized, low-energy solvent manufacturing within the European Union.

India: Domestic EO Integration and Pharma-Grade Pull

India’s E Series Glycol Ether market is benefiting from integrated EO capacity expansion and pharmaceutical demand. In 2025, Indovinya expanded its integrated EO/EG facility in Gujarat, strengthening domestic supply for the paints and coatings sector. This expansion aligns with anticipated demand growth linked to PM MITRA textile park rollouts beginning in 2026, which are expected to stimulate waterborne coating consumption.

Pharmaceutical applications are emerging as a high-value demand driver. As India’s pharma industry accelerates the development of complex injectable and advanced drug delivery systems, procurement of pharmaceutical-grade ethylene glycol ethers has increased. These solvents are being used as co-solvents in sensitive formulations where purity, toxicological compliance, and batch consistency are critical, reinforcing India’s transition from commodity consumption to application-specific solvent demand.

E Series Glycol Ether Market: Country-Level Strategic Snapshot

E-Series Glycol Ether Market County Level Snapshot

|

Country

|

Core Strategic Driver

|

Key Application Focus

|

Structural Direction

|

|

China

|

Verbund integration and electronics localization

|

Electronics-grade solvents, marine coatings

|

High-purity self-sufficiency and low-carbon scale

|

|

United States

|

Regulatory scrutiny and pricing volatility

|

Architectural coatings, cosmetics

|

Compliance-led differentiation and niche growth

|

|

Saudi Arabia

|

Downstream diversification

|

EV batteries, advanced PCBs

|

EO derivative localization

|

|

Germany

|

REACH compliance and digital optimization

|

Industrial degreasing, coatings

|

Energy-efficient, digitally optimized production

|

|

India

|

EO integration and pharma demand

|

Paints, injectables

|

Shift toward application-specific grades

|

E-Series Glycol Ether Market Report Scope

E Series Glycol Ether Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.7 Billion

|

|

Market Size (2034)

|

$5.6 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Ethylene Glycol Monomethyl Ether, Ethylene Glycol Monoethyl Ether, Ethylene Glycol Monobutyl Ether, Ethylene Glycol Monohexyl Ether, Ethylene Glycol Monopropyl Ether), By Grade (Industrial Grade, Electronics Grade, Pharmaceutical and Cosmetic Grade), By Application (Solvents, Chemical Intermediates, Functional Fluids, Formulation Components), By End-Use Industry (Paints and Coatings, Automotive and Transportation, Electrical and Electronics, Healthcare and Pharmaceuticals, Household and Industrial Cleaning, Agrochemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., BASF SE, LyondellBasell Industries N.V., SABIC, Indorama Ventures, Shell plc, INEOS Group Limited, Huntsman Corporation, China Petroleum & Chemical Corporation, PetroChina Company Limited, Nippon Nyukazai Co., Ltd., Hannong Chemicals Inc., Sasol Limited, India Glycols Limited, Lotte Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

E-Series Glycol Ether Market Segmentation

By Product Type

- Ethylene Glycol Monomethyl Ether

- Ethylene Glycol Monoethyl Ether

- Ethylene Glycol Monobutyl Ether

- Ethylene Glycol Monohexyl Ether

- Ethylene Glycol Monopropyl Ether

By Grade

- Industrial Grade

- Electronics Grade

- Pharmaceutical and Cosmetic Grade

By Application

- Solvents

- Chemical Intermediates

- Functional Fluids

- Formulation Components

By End-Use Industry

- Paints and Coatings

- Automotive and Transportation

- Electrical and Electronics

- Healthcare and Pharmaceuticals

- Household and Industrial Cleaning

- Agrochemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the E-Series Glycol Ether Industry

- Dow Inc.

- BASF SE

- LyondellBasell Industries N.V.

- SABIC

- Indorama Ventures

- Shell plc

- INEOS Group Limited

- Huntsman Corporation

- China Petroleum & Chemical Corporation

- PetroChina Company Limited

- Nippon Nyukazai Co., Ltd.

- Hannong Chemicals Inc.

- Sasol Limited

- India Glycols Limited

- Lotte Chemical Corporation

*- List not Exhaustive