Dimethylolpropionic Acid Market to Reach $1,464.7 Billion by 2034 at 6.3% CAGR Driven by Polyurethane Dispersions and Sustainable Resin Innovation

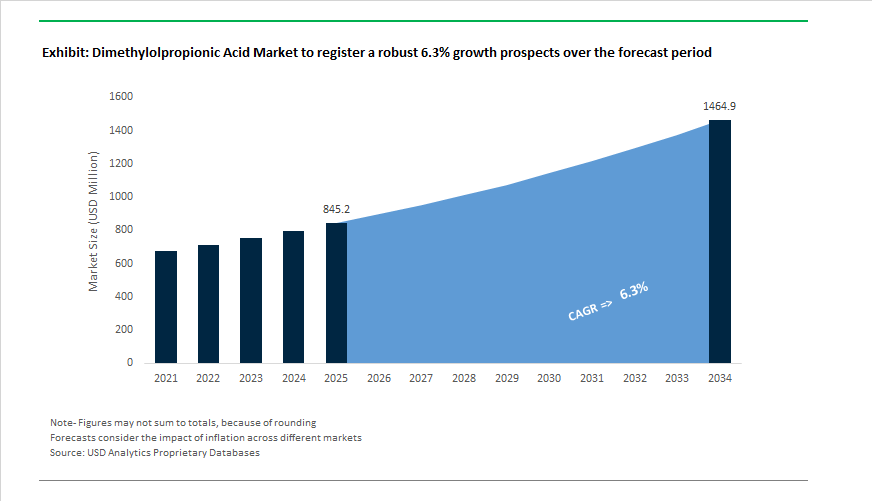

The Dimethylolpropionic Acid (DMPA) Market is projected to expand from $845.2 billion in 2025 to $1,464.7 billion by 2034, registering a CAGR of 6.3%. Market growth is anchored in the accelerating adoption of waterborne polyurethane dispersions (PUDs), alkyd resins, UV-curable coatings, and formaldehyde-free adhesives across construction, automotive, wood coatings, and electronics. DMPA functions as a critical internal emulsifier in polyurethane systems, enabling the shift toward low-VOC, solvent-free coating technologies aligned with global decarbonization mandates. The value chain is increasingly characterized by vertical integration, biomass-balanced feedstocks, electronic-grade purification, and advanced specialty derivatives beyond traditional coatings.

A structural shift occurred in early 2024 when Perstorp completed the acquisition of GEO Specialty Chemicals’ DMPA business. The integration of the DMPA® brand consolidated Perstorp’s position as a dominant global supplier of building blocks for polyurethane and alkyd dispersions. Following this divestment, GEO Specialty Chemicals pivoted toward nutrition and personal care under CPS Performance Materials, signaling a bifurcation between high-volume industrial intermediates and specialty consumer-focused portfolios. In parallel, manufacturers implemented selective price adjustments for Bis-MPA throughout 2024–2025 in response to volatility in propionaldehyde and formaldehyde feedstocks and elevated European energy costs. During 2024, demand for ultra-high-purity DMPA grades rose sharply in electronic coatings used in 5G infrastructure and wearable devices, where trace metallic contaminants can disrupt high-frequency signal transmission.

Application diversification intensified in 2025. In January 2025, Perstorp announced the startup of a synthetic ester plant near Amsterdam, expanding into specialty thermal management fluids for data centers. Although centered on esters, the move leverages DMPA-based building blocks and reflects the growing intersection between specialty resins and advanced cooling systems. Throughout 2025, adhesive formulators accelerated the use of DMPA as a curing agent in formaldehyde-free wood paneling systems, responding to stricter indoor air quality regulations across Europe and North America. At the advanced materials frontier, CD Bioparticles introduced DMPA-based dendrimers during 2024–2025, including azide and carboxyl variants for theranostic adhesives, biosensors, and high-performance optical systems, illustrating DMPA’s transition into precision functional materials. In China, Jiangxi Nancheng Hongdu Chemical achieved ISO9001:2000 recertification in 2025, reinforcing its strategy of import substitution by supplying high-purity DMPA to the Asian synthetic leather and ink sectors.

Sustainability strategy and operational optimization defined the period entering 2026. In August 2025, Perstorp initiated a global rightsizing program, reducing its workforce by approximately 8% to preserve resilience amid energy cost pressure and intensified price competition. In October 2025, the company published its RE-carbonization whitepaper outlining a roadmap for mass-balance production of monomers such as DMPA, replacing fossil carbon inputs with renewable and recycled sources to meet EU Green Deal 2030 targets. At PaintIndia 2026 in February 2026, Perstorp showcased biomass-balanced DMPA and polyol building blocks under its Pro-Environment concept, targeting automotive OEM coatings and wood finishes seeking Scope 3 emission reductions. These initiatives underscore the transition of the Dimethylolpropionic Acid market from conventional polyurethane emulsifier chemistry toward low-carbon, high-purity, and electronically compatible specialty applications across global advanced manufacturing sectors.

Trends and Opportunities Defining the Dimethylolpropionic Acid (DMPA) Market

DMPA as a Non-Substitutable Enabler for High-Performance Waterborne PUDs

- The shift away from solvent-borne polyurethane systems has reached an irreversible inflection point, particularly in automotive refinishing, industrial wood coatings, and protective topcoats. DMPA plays a central role by introducing internal carboxylic functionality into the polyurethane backbone, which upon neutralization with tertiary amines enables stable water dispersibility without sacrificing mechanical strength.

- Technical disclosures presented at the European Coatings Show in early 2025 demonstrated that DMPA-based polyurethane dispersions now deliver impact resistance, abrasion durability, and adhesion to steel and fiberglass that closely match solvent-borne urethanes, while achieving up to a 90% reduction in VOC emissions. This performance parity has removed the last technical barriers to adoption in high-spec industrial applications.

- The furniture and wood coatings sector is emerging as a major demand center. By mid-2025, large furniture manufacturers in Vietnam and Poland reported a 15% increase in the use of DMPA-modified waterborne resins, driven by the European Union’s Green Public Procurement criteria and stricter indoor air quality standards. As public infrastructure and residential developers increasingly specify low-toxicity coatings, DMPA consumption is becoming structurally embedded in global PUD production.

Intensifying R&D into DMPA Alternatives and Hybrid Internal Dispersants

- Despite its market leadership, DMPA faces technical scrutiny related to thermal yellowing and sensitivity to hard-water electrolytes. A July 2025 study published through National Institutes of Health-linked research explored solvent-free polyurethane synthesis routes using UDMA and IPDI in combination with DMPA. While dispersibility and film formation remained excellent, elevated processing temperatures were shown to accelerate yellowing in stoving and coil coating applications.

- As a result, formulators are actively evaluating sulfonated diols and itaconic acid derivatives as partial co-dispersants to enhance thermal stability without compromising water dispersibility. In parallel, global coatings manufacturers are investing in next-generation internal emulsifiers designed to tolerate high concentrations of calcium and magnesium ions. DMPA-based dispersions can destabilize under hard-water conditions, which is a critical issue for marine, coastal, and infrastructure coatings deployed in high-salinity environments. Research initiatives launched in 2025 increasingly focus on zwitterionic internal dispersants that aim to replicate DMPA’s performance while offering broader electrolyte resilience.

UV-Curable Waterborne Oligomers for 3D Printing and Advanced Inks

- The convergence of waterborne polyurethane chemistry and radiation curing is opening a premium opportunity space for DMPA in additive manufacturing and functional inks. At the 2025 Pittsburg State University Research Colloquium, researchers presented castor oil-based, UV-curable polyurethane acrylates incorporating DMPA-modified backbones. These materials demonstrated high resolution and enhanced toughness in Digital Light Processing 3D printing, addressing long-standing brittleness issues associated with conventional UV resins.

- In parallel, DMPA’s carboxylic functionality is being leveraged in the synthesis of UV-curable waterborne oligomers for overprint varnishes and packaging inks. Industry announcements in late 2025 confirmed that these systems deliver the curing speed associated with UV technologies while maintaining the low migration and low sensitization profile of water-based formulations. This positions DMPA-derived oligomers as a strategic solution in segments where traditional UV inks face tightening regulatory scrutiny related to skin contact and occupational exposure.

Bio-Based and Low-Carbon DMPA Pathways Supporting Coatings Decarbonization

- Sustainability imperatives are reshaping the upstream chemistry of DMPA itself. While conventional DMPA production relies on petrochemical aldehydes, the industry is actively exploring structural analogs derived from bio-succinic and itaconic acid as part of broader circular economy strategies. Leading suppliers such as Perstorp have introduced 100% renewable base polyols under their sustainable solutions platforms, accelerating interest in complementary bio-derived internal dispersants.

- According to insights shared at the European Coatings Show 2025, replacing fossil-based DMPA with bio-based analogs can reduce the product carbon footprint of a finished polyurethane dispersion coating by up to 30%. This reduction is strategically aligned with Science Based Targets initiative commitments adopted by global coatings leaders such as AkzoNobel and PPG Industries, both of which are under increasing pressure to decarbonize Scope 3 emissions across their raw material supply chains.

Dimethylolpropionic Acid (DMPA) Market Share and Segmentation Insights

DMPA Market Share by Application : Polyurethane Dispersions Dominate the Waterborne Coatings Revolution

Polyurethane dispersions (PUDs) account for 58% of total DMPA demand in 2025, underscoring DMPA’s critical role in enabling waterborne polyurethane chemistry. Its diol functionality combined with carboxylic acid groups allows internal emulsification, eliminating the need for external surfactants and supporting stable, high-performance low-VOC polyurethane dispersions. This chemistry underpins growth in waterborne coatings, adhesives, and textile finishes. Waterborne resins represent a significant segment, driven by global transition away from solvent-based alkyds and polyesters toward environmentally compliant systems. Powder coatings utilize DMPA as a crosslinking modifier to improve flow and mechanical performance, while electrodeposition coatings apply DMPA in cathodic epoxy primers for corrosion resistance in automotive applications. Glass fiber sizing and specialty inks remain smaller niches, focused on interfacial adhesion enhancement and flexible waterborne ink systems for packaging and textile printing.

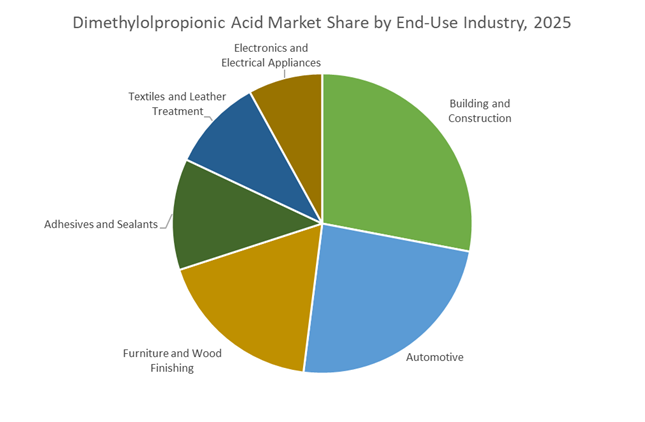

DMPA Market Share by End-Use Industry : Construction and Automotive Propel Waterborne Resin Adoption

Building and construction lead DMPA end-use demand with 28% market share, fueled by rising adoption of waterborne architectural coatings, concrete sealers, and protective finishes compliant with stringent VOC regulations. Automotive represents a major growth engine, particularly in waterborne basecoats, clearcoats, and electrocoat primers where DMPA-derived polyurethane dispersions deliver durability, chemical resistance, and appearance retention. Furniture and wood finishing maintain strong uptake of low-odor waterborne stains and topcoats that enhance sustainability credentials. Adhesives and sealants show robust growth as DMPA-based waterborne polyurethane adhesives gain traction in footwear, laminates, and construction bonding applications. Textiles and leather treatment applications leverage DMPA chemistry for flexible, breathable coatings, while electronics and electrical appliances remain a niche but strategic segment using DMPA in coil coatings and insulation systems aligned with environmental compliance standards.

Competitive Landscape of the Dimethylolpropionic Acid (DMPA) Market

The Dimethylolpropionic Acid (DMPA) market is increasingly defined by consolidation, sustainability-driven innovation, and rising demand from polyurethane dispersions (PUD), waterborne coatings, synthetic leather, UV-curable resins, and electronics-grade finishes. In 2026, competitive advantage is anchored in bio-attributed DMPA, backward integration, low-sodium purity grades, and technical formulation support for solvent-to-water transitions.

Perstorp Specialty Chemicals AB leads the DMPA market through consolidation and bio-attributed innovation

Perstorp Specialty Chemicals AB is the undisputed global leader in the DMPA market, securing over 40% global market share by 2026 following its strategic acquisition of GEO Specialty Chemicals’ DMPA business in early 2022. Through its “Pro-Environment” initiative, Perstorp is transitioning its polyol portfolio toward bio-attributed DMPA using mass-balance accounting, supporting low-carbon furniture and automotive coatings in Europe. Its flagship Bis-MPA™ brand is prized for ultra-low color and ash content, critical for clear-coat electronics and premium wood finishes. With full integration from propionaldehyde to finished DMPA, Perstorp ensured supply continuity during 2024–2025 disruptions while offering industry-leading PUD formulation expertise for waterborne systems.

GEO Specialty Chemicals, Inc. strengthens North American DMPA derivatives and NMP-free resin pathways

Despite divesting its core DMPA business, GEO Specialty Chemicals, now under CPS Performance Materials, remains a key North American force via specialty derivatives and performance monomers. Its DMPA® Regular Grade delivers superior hydrolytic stability in aqueous resins and dominates the electrodeposition (E-coat) segment for aerospace and heavy machinery. GEO’s DMPA® Polyol HA-0135 directly addresses 2026 regulatory pressure by enabling NMP-free resin processing, aligning with global solvent-reduction mandates. Expansion into nutrition and personal care leverages DMPA derivatives as functional additives, while GEO’s proprietary Single Kettle Charge technology simplifies resin manufacturing by combining reactants in one step, improving throughput and operational efficiency.

Henan Tianfu Chemical Co., Ltd. scales low-sodium DMPA for Asia’s synthetic leather and coatings boom

Henan Tianfu Chemical has emerged as a major global exporter, holding an estimated 15.7% market share in 2026, largely driven by Asia’s booming synthetic leather, footwear, textile finishes, and architectural coatings sectors. In 2025, Tianfu upgraded production to introduce low-sodium DMPA grades, targeting high-end electronics coatings where minimized ionic conductivity is essential. Its “Import Substitution” strategy delivers European-comparable purity at a 10 to 15% cost advantage, accelerating adoption across domestic Chinese manufacturers. Tianfu supplies at scale to a regional market forecast to grow at 6.9% CAGR through 2036, positioning the company as a cost-competitive alternative to Western specialty acid producers.

Jiangxi Nancheng Hongdu Chemical differentiates with DMPA and DMBA for composites and glass fiber sizing

Jiangxi Nancheng Hongdu Chemical stands out as one of the few large-scale producers of both DMPA and DMBA, supported by a provincial-certified research center for environmentally friendly polyols. The company operates China’s largest domestic DMPA production base, supplying ASEAN and European export markets with industrial, specialty salt, and neutralized DMPA grades that streamline PUD neutralization. Hongdu’s core strength lies in glass fiber sizing, where DMPA enhances adhesion between fibers and polymer matrices for wind energy blades and automotive composites. Its professor-led R&D team continues to refine environmentally optimized polyols, reinforcing Hongdu’s position in advanced composite and structural material applications.

Jiangxi Selon Industrial Co., Ltd. targets UV-curable and electronics-grade DMPA through green manufacturing

Jiangxi Selon Industrial represents China’s fast-rising second tier of DMPA suppliers, focusing on automotive coatings, UV-curable waterborne resins, and electronics/3C applications. In late 2025, Selon announced a capacity expansion to meet accelerating demand for UV-curable systems, where DMPA enables water dispersibility without compromising cure speed. The company is actively supplying high-clarity DMPA for protective films and high-gloss plastic coatings used in consumer electronics. Alongside aggressive regional distribution, Selon is piloting green production methods with energy-efficient batch processing, lowering energy intensity per metric ton and strengthening its competitive position against established Western producers.

Sweden: Specialty Optimization and Sustainability-Driven Differentiation

Sweden remains the strategic nucleus of innovation in the dimethylolpropionic acid market, anchored by Perstorp and its global Bis-MPA™ platform. Effective February 1, 2025, Perstorp implemented a portfolio-wide price adjustment for polyols and specialty acids, including DMPA, reflecting sustained inflation in propionaldehyde and formaldehyde feedstocks. Rather than signaling demand weakness, this pricing move underscores the company’s confidence in its specialty positioning and its ability to pass through costs in high-value waterborne polyurethane and coatings applications. In August 2025, Perstorp initiated a global rightsizing program, reducing its workforce by roughly 8%. This restructuring is widely viewed as a margin-defense strategy that reallocates capital and operational focus toward high-margin specialty molecules such as DMPA, rather than commoditized oxo-chemicals.

From a technology standpoint, Swedish production sites have increasingly specialized in low-dusting, large-particle DMPA and fine-particle Bis-MPA™ grades engineered to improve solubilization kinetics in anionic waterborne polyurethane dispersions. These product innovations directly reduce resin processing energy consumption, a key performance metric for coatings manufacturers. Sustainability leadership is further reinforced by the integration of Product Carbon Footprint data into digital product passports at Swedish facilities, enabling downstream users to align with the EU’s 2026 Ecodesign for Sustainable Products Regulation. Beyond architectural coatings, Swedish R&D efforts have extended DMPA chemistry into marine and wind energy applications. Pilot trials conducted in the Baltic Sea during 2025 demonstrated a 14% improvement in alkali resistance for offshore wind turbine blade coatings formulated with DMPA-based resins, positioning Sweden as a technical reference point for extreme-environment applications.

China: Regulatory Pressure Converting into Waterborne Demand Acceleration

China’s dimethylolpropionic acid market is being reshaped by regulatory tightening and industrial upgrading rather than pure capacity expansion. Heightened anti-dumping scrutiny from the United States and European Union in 2025, initially targeting intermediates such as MDI and adipic acid, has had spillover effects on specialty carboxylic acids. Chinese DMPA producers are therefore optimizing domestic supply chains to reduce export exposure and mitigate the risk of retaliatory trade actions. At the provincial level, Zhejiang’s 2025 directive on the Smart Transformation of Fine Chemicals has provided subsidies to integrate AI-driven sensor networks into DMPA synthesis. Companies such as Shenzhen Vtolo and Henan Tianfu are deploying real-time monitoring of exothermic reaction stages, improving yield consistency and reducing safety risks.

Demand-side dynamics in China are decisively regulation-led. Updated VOC emission standards issued by the Ministry of Ecology and Environment in 2025 now require automotive OEMs to use coatings with a minimum of 40% waterborne content. This single policy shift has materially increased domestic demand for high-purity DMPA as a neutralizing agent in waterborne polyurethane dispersions. Beyond automotive coatings, China is also piloting DMPA-based biodegradable coatings for food packaging. A major infrastructure project in Guangzhou launched in 2025 aims to replace polyethylene-coated packaging in municipal school systems with DMPA-enabled biodegradable alternatives by 2026, signaling early-stage diversification of DMPA demand into sustainability-focused packaging applications.

United States: Domestic Supply Security and Functional Coatings Expansion

In the United States, the DMPA market has been strongly influenced by supply chain localization and occupational safety regulation. Following its acquisition of GEO Specialty Chemicals’ DMPA business, Perstorp completed the integration of U.S. production assets in Allentown, Pennsylvania by mid-2025. This move established a secure domestic supply base for North American polyurethane dispersion formulators, reducing dependence on transatlantic imports and improving lead-time reliability for coatings customers.

Regulatory developments have also shaped operational practices. As of January 2025, the U.S. Environmental Protection Agency included specialty diols within a broader TSCA risk evaluation framework. While DMPA itself remains permitted, manufacturers have proactively adopted closed-loop handling and dust-mitigation systems to address inhalation risks during pre-polymer formation. On the demand side, DMPA consumption is expanding beyond traditional architectural coatings. Electronics manufacturers in the Pacific Northwest’s Silicon Forest cluster have increased procurement of DMPA for UV-curable printed circuit board coatings used in 5G hardware, where thermal stability and dielectric performance are critical. In parallel, updated 2025 Department of Energy efficiency guidelines have accelerated the adoption of DMPA-based powder coatings for HVAC heat exchangers, as corrosion protection is increasingly linked to long-term energy efficiency metrics.

Japan: Precision Performance for Automotive, Composites, and Electronics

Japan’s dimethylolpropionic acid market is characterized by precision-driven innovation and tight performance tolerances. In 2025, major automotive OEMs such as Toyota and Honda introduced Next-Gen Gloss standards for vehicle topcoats. This has driven demand for low-sodium DMPA grades that maintain clarity and distinction of image under Japan’s highly variable humidity conditions. Domestic suppliers have responded by refining purification processes to minimize ionic impurities that can compromise waterborne coating aesthetics.

Beyond automotive finishes, Japanese composites manufacturers have advanced glass fiber sizing technologies using DMPA-based emulsions. A 2025 breakthrough demonstrated a 22% improvement in resin-to-fiber interfacial bond strength, directly enhancing the mechanical performance of aerospace-grade composites. Electronics applications represent another high-value frontier. Specialty chemical firms in Japan are piloting DMPA-modified epoxy resins for semiconductor encapsulation, focusing on lowering the coefficient of thermal expansion to support the miniaturization of wearable and consumer electronics devices.

Germany: Regulatory Cost Pass-Through and Premium Waterborne Systems

Germany represents the most regulation-intensive DMPA market in Europe, with compliance costs directly shaping pricing and product strategy. Following the 2025 increase in evaluation fees by the European Chemicals Agency, German distributors introduced regulatory surcharges of approximately €15–€20 per metric ton to offset the higher costs of dossier maintenance and substance evaluation. Rather than dampening demand, this has accelerated a shift toward premium, high-purity DMPA grades used in certified low-emission systems.

Demand growth is strongest in architectural and wood coatings. In 2025, a leading German coatings producer launched an indoor wall paint line based on DMPA-synthesized dispersions that achieved OECD biodegradability certification, marking a milestone for the European architectural segment. Concurrently, furniture manufacturers in Westphalia transitioned roughly 60% of luxury wood finishes to DMPA-based aqueous systems to comply with stringent 2026 indoor air quality regulations. These shifts underscore Germany’s role as a demand center for regulatory-compliant, high-performance DMPA formulations.

Dimethylolpropionic Acid Market: Country-Level Strategic Summary

Dimethylolpropionic Acid Market County Level Snapshot

|

Country

|

Strategic Emphasis

|

Primary Demand Drivers

|

Market Implication

|

|

Sweden

|

Specialty optimization and PCF transparency

|

Waterborne PUDs, offshore coatings

|

Technology and sustainability benchmark

|

|

China

|

VOC regulation and smart manufacturing

|

Automotive waterborne coatings, packaging

|

Rapid domestic demand expansion

|

|

United States

|

Supply localization and safety compliance

|

Electronics, HVAC, PUDs

|

Stable growth with higher purity standards

|

|

Japan

|

Precision performance innovation

|

Automotive topcoats, composites, electronics

|

High-value niche applications

|

|

Germany

|

Regulatory compliance and green coatings

|

Architectural and wood finishes

|

Premium pricing and certified systems

|

Dimethylolpropionic Acid Market Report Scope

Dimethylolpropionic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$845.2 Million

|

|

Market Size (2034)

|

$1464.7 Million

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Type (Standard Grade, Special Grade, Fine Grade), By Application (Polyurethane Dispersions, Waterborne Resins, Powder Coatings, Electrodeposition Coatings, Glass Fiber Sizing, Specialty Inks), By End-Use Industry (Automotive, Building and Construction, Furniture and Wood Finishing, Textiles and Leather Treatment, Electronics and Electrical Appliances, Adhesives and Sealants)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Perstorp Specialty Chemicals AB, GEO Specialty Chemicals, Inc., Henan Tianfu Chemical Co., Ltd., Shenzhen Vtolo Chemicals Co., Ltd., Jiangxi Nancheng Hongdu Chemical Technology Development Co., Ltd., Jiangxi Selon Industrial Co., Ltd., Anhui Sinograce Chemical Co., Ltd., Huzhou Changsheng Chemical Co., Ltd., Merck KGaA, Evonik Industries AG, BASF SE, Dow Inc., Huntsman Corporation, Yigyooly Enterprise Limited, Biosynth Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dimethylolpropionic Acid Market Segmentation

By Type

- Standard Grade

- Special Grade

- Fine Grade

By Application

- Polyurethane Dispersions

- Waterborne Resins

- Powder Coatings

- Electrodeposition Coatings

- Glass Fiber Sizing

- Specialty Inks

By End-Use Industry

- Automotive

- Building and Construction

- Furniture and Wood Finishing

- Textiles and Leather Treatment

- Electronics and Electrical Appliances

- Adhesives and Sealants

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dimethylolpropionic Acid Industry

- Perstorp Specialty Chemicals AB

- GEO Specialty Chemicals, Inc.

- Henan Tianfu Chemical Co., Ltd.

- Shenzhen Vtolo Chemicals Co., Ltd.

- Jiangxi Nancheng Hongdu Chemical Technology Development Co., Ltd.

- Jiangxi Selon Industrial Co., Ltd.

- Anhui Sinograce Chemical Co., Ltd.

- Huzhou Changsheng Chemical Co., Ltd.

- Merck KGaA

- Evonik Industries AG

- BASF SE

- Dow Inc.

- Huntsman Corporation

- Yigyooly Enterprise Limited

- Biosynth Ltd.

*- List not Exhaustive