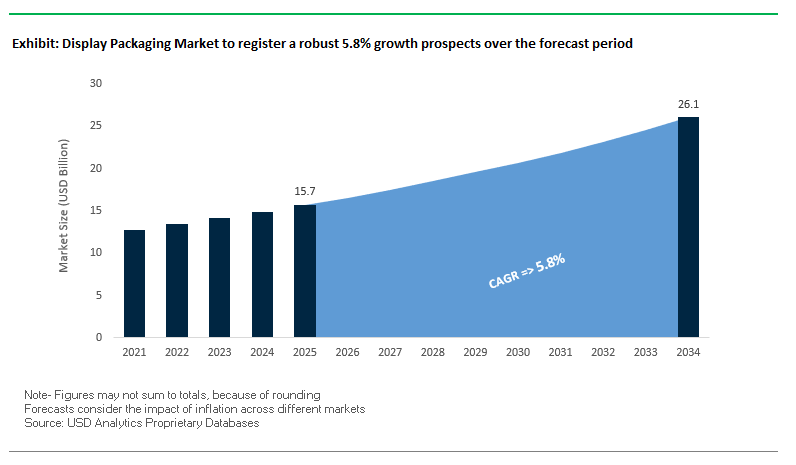

Market Overview: Display Packaging Market Valued at $15.7 Billion in 2025, Poised to Reach $26.1 Billion by 2034

The Global Display Packaging Market is projected to expand from $15.7 billion in 2025 to $26.1 billion by 2034, at a CAGR of 5.8%. This steady growth is fueled by the dual demand for retail-ready displays and e-commerce-driven unboxing experiences. Paperboard, including corrugated and folding carton, dominates due to its durability, cost-effectiveness, and superior printability, making it the leading choice for shelf-ready packaging and freestanding floor displays.

The sector’s importance lies in its role at the point-of-sale (POS), where more than 60% of purchase decisions occur in-store, highlighting display packaging as a powerful marketing tool for influencing consumer choice. Beyond retail, the e-commerce boom has transformed display packaging into a branding and consumer engagement asset, with brands investing in unboxing experiences that are both visually appealing and shareable on social media.

At the same time, sustainability pressures are reshaping product portfolios. By 2025, over 40% of brand owners introduced or tested display packaging featuring recycled content, mono-materials, and compostable films, reflecting growing consumer demand and government-backed regulations targeting single-use plastics.

Key Insights for Industry Professionals

- Paperboard dominates: Corrugated and folding cartons remain the backbone of retail displays.

- POS-driven growth: Over 60% of retail decisions are influenced by display packaging.

- E-commerce influence: The “unboxing experience” drives premium packaging innovation.

- Sustainability shift: More than 40% of brand owners adopting recycled and compostable solutions.

Market Analysis: Strategic Mergers and Sustainability-Driven Innovations Fuel Market Expansion

The display packaging industry has undergone rapid transformation, with mergers, divestitures, and product innovations reshaping competitive positioning.

In August 2025, Smurfit WestRock, formed from the merger of Smurfit Kappa and WestRock, reported strong Q2 performance, emphasizing its expanded reach in retail packaging, including display solutions. The same month, Graphic Packaging International unveiled a child-resistant paperboard detergent pod pack, demonstrating its ability to combine safety with sustainability. DS Smith, also in August 2025, partnered with Martins Brewery to launch a sustainable paper-based 6-pack handle, reinforcing its mission to replace problem plastics with recyclable alternatives. Meanwhile, International Paper announced a $1.5 billion divestiture of its cellulose fibers division to sharpen its focus on packaging.

Earlier in July 2025, International Paper also finalized the divestiture of five European corrugated plants tied to its acquisition of DS Smith, enabling the company to streamline its display packaging operations. That same month, Graphic Packaging published its 2024 Impact Report, highlighting its replacement of nearly 1 billion plastic packages with paperboard, underscoring the sector’s sustainability commitment. Mondi showcased its premium sustainable papers at LUXE PACK Paris in June 2025, reflecting demand for high-quality luxury-oriented display solutions.

Major consolidation has further transformed the industry. The Smurfit Kappa–WestRock merger in February 2025 created one of the world’s largest paper-based packaging leaders, with extensive influence in display packaging. Similarly, the International Paper–DS Smith $7.2 billion merger approved in October 2024 is set to establish another powerhouse in sustainable display packaging across Europe and North America.

Emerging Trends and Opportunities Reshaping the Display Packaging Market

Display Packaging Market Driven by Digital Integration and Sustainable Innovation

The global display packaging market is transforming rapidly as brands leverage digital technologies and sustainable materials to elevate consumer engagement and retailer efficiency. Augmented reality (AR), near-field communication (NFC), and digital printing are redefining how display packaging functions as both a marketing and operational tool. Simultaneously, opportunities are opening in plant-based substrates and smart inventory systems that align with retailer needs for sustainability, efficiency, and security. These shifts are making display packaging more than just a promotional tool it is becoming a critical part of the retail ecosystem.

Integration of Augmented Reality (AR) and Near-Field Communication (NFC) for Experiential Engagement

Brands are turning display packaging into a digital media channel by embedding AR and NFC triggers to deliver immersive product experiences, authentication, and real-time analytics. This transformation is redefining the role of packaging as a persistent brand touchpoint. For instance, Nintendo and Kellogg’s partnered to embed NFC tags into cereal boxes, which unlocked in-game rewards for Mario Kart when scanned with a Nintendo Switch. This gamified approach drives repeat purchases and increases consumer loyalty. In luxury, Bulgari integrated NFC chips into its BVLGARI TOVCH collection, allowing customers to verify product authenticity and access exclusive digital experiences with a simple smartphone tap. Beyond engagement, these technologies provide valuable first-party consumer data from scan frequency to location insights that guide marketing strategy. The ability to merge physical retail with digital interaction positions AR and NFC-enabled display packaging as a cornerstone of future brand-consumer relationships.

Rapid Adoption of Digitally Printed Short Runs for Hyper-Targeted Campaigns

The rising need for agility in marketing is fueling the widespread adoption of digitally printed short runs in display packaging. Unlike traditional flexography, digital printing allows cost-effective customization without expensive tooling, making it ideal for limited-edition campaigns or regional promotions. Brands are increasingly using digital for prototyping and testing a major CPG brand recently reduced costly production errors by testing digitally printed proofs before tooling full-scale runs. Similarly, LEGO used digital printing for a limited F1-themed launch, delivering region-specific displays tied to a single event. Hybrid models are also gaining ground; for example, Yankee Candle leverages flexo for its main display body but applies digital printing for seasonal headers, balancing efficiency with flexibility. By enabling faster time-to-market, personalization, and reduced waste, digital printing is transforming display packaging into a dynamic marketing tool that adapts to real-time consumer trends.

Development of Plant-Based and Home-Compostable Structural Substrates

Sustainability is becoming a competitive differentiator in display packaging, creating opportunities for plant-based, recyclable, and compostable substrates to replace plastics and foam. Companies are innovating with natural coatings and fibers that maintain strength and barrier performance without compromising recyclability. Notpla’s seaweed-based coating, for example, eliminates the need for plastic liners in food and display packaging, enabling home compostability while providing grease and moisture resistance. Similarly, mushroom mycelium-based inserts are emerging as a replacement for polystyrene foam, offering lightweight yet durable protection for electronics and high-value items. With retailers and brands under mounting regulatory and consumer pressure to reduce plastic waste, all-paper and plastic-free display systems not only reduce environmental impact but also enhance brand image. These developments present a lucrative opportunity for packaging producers to align with corporate ESG goals while capturing eco-conscious market segments.

Embedding Smart Inventory and Anti-Theft Technology

The integration of RFID tags, electronic article surveillance (EAS), and weight sensors into display packaging is creating smarter retail ecosystems. By embedding these technologies directly into display units, retailers gain 98–99% inventory accuracy, as validated by a University of Parma study on RFID-enabled systems. This precision reduces stockouts, boosts sales, and enhances overall operational efficiency. Dual RFID and EAS systems also address theft concerns, providing real-time alerts and item-level tracking to improve loss prevention strategies. Additionally, connected packaging supports seamless supply chain management by offering end-to-end visibility from warehouse to sales floor, reducing loading times and ensuring consistent product availability. For retailers balancing efficiency with security, smart display packaging offers a clear return on investment while positioning them at the forefront of retail innovation.

Competitive Landscape: Leading Companies Shaping the Display Packaging Industry

The display packaging market is defined by strategic mergers, vertical integration, and innovations in sustainable, retail-ready designs. Industry leaders are investing in recyclable materials, high-end graphics, and functional structures to enhance both point-of-sale impact and e-commerce brand engagement.

Smurfit WestRock: A New Global Leader After the Merger of Smurfit Kappa and WestRock

Smurfit WestRock emerged in February 2025 as a global packaging giant with robust offerings in corrugated displays, folding cartons, and point-of-sale packaging. The merger strengthened its global reach, innovation pipeline, and sustainability focus. Its vertical integration, from forestry to finished display products, ensures quality, consistency, and a closed-loop recycling approach. Smurfit WestRock’s retail display packaging solutions are designed to capture consumer attention while aligning with circular economy goals.

International Paper: Strengthening Core Focus on Sustainable Display Packaging

International Paper is repositioning around sustainable packaging after acquiring DS Smith in late 2024. Its display packaging offerings include premium containerboard and paperboard materials for high-impact retail environments. In July 2025, it divested five European corrugated plants to satisfy merger conditions, streamlining operations. The company also invested $250 million to convert a mill to containerboard, boosting capacity for recyclable display packaging. Its strategy is rooted in providing innovative, high-performance papers that balance functionality with sustainability.

DS Smith Plc: Championing the Closed-Loop Recycling Model

DS Smith continues to drive fiber-based sustainable packaging, producing 100% recycled display packaging solutions. Following its merger approval with International Paper in October 2024, DS Smith is positioned as a critical player in global circular packaging. Its purpose, “Redefine Packaging for a Changing World,” guides efforts to replace plastics with fiber-based solutions. DS Smith’s vertically integrated recycling and paper-making model ensures a consistent supply of high-quality recycled display packaging, making it a leader in eco-friendly retail solutions.

Graphic Packaging International: Innovating with Plastic-Reduction Technologies

Graphic Packaging remains a leader in fiber-based display packaging for food, beverage, and household goods. Its 2024 Impact Report highlighted the replacement of 1 billion plastic packages with paperboard, demonstrating sustainability leadership. Its proprietary Boardio™ and EnviroClip™ technologies enable brand owners to shift from plastics to fiber-based POS displays. The company is investing in growth with a new recycled paperboard mill in Texas, due in late 2025, reinforcing its capacity to meet global demand for sustainable display packaging.

Mondi Group: Expanding Premium and Sustainable Display Packaging Solutions

Mondi combines innovation with sustainability, offering specialty papers and high-barrier recyclable display packaging. In June 2025, it showcased premium solutions at LUXE PACK Paris, appealing to luxury brands seeking sustainable unboxing experiences. Mondi’s FunctionalBarrier Paper Ultimate is a breakthrough ultra-high-barrier material designed to replace multi-layer plastics in high-end displays. The recent acquisition of Schumacher Packaging’s Western European operations strengthens Mondi’s corrugated offering, making it a versatile player in both retail and luxury display packaging segments.

Display Packaging Market Share Insights

Floor Displays Dominate Market Share by Packaging Type in Display Packaging

Floor displays command the largest share of the display packaging market, representing 35% of demand in 2025. Their dominance stems from their unique ability to combine high visibility with large product capacity, making them indispensable for food, beverage, and seasonal promotions in high-traffic retail zones. Once limited to temporary corrugated structures, floor displays are now evolving into semi-permanent marketing assets with reinforced designs, premium printing, and even integrated lighting or digital signage to maximize consumer engagement. For brand owners, the ROI of floor displays lies in their ability to capture impulse purchases and drive incremental volume sales, while retailers favor them for their restocking efficiency and capacity to anchor themed promotions. This format’s dominance highlights the convergence of logistics and marketing in retail packaging, where visibility and efficiency are equally critical.

Food & Beverages Lead Market Share by End-Use Industry in Display Packaging

Food and beverages account for 40% of display packaging demand, making them the undisputed driver of the segment. The fast-moving, promotion-heavy nature of the category means that brands rely on displays to launch new products, communicate discounts, and stimulate impulse purchases during seasonal peaks. From floor-ready packaging for canned goods to countertop displays for confectionery, the segment requires packaging that balances durability with cost-effectiveness, as most units are designed for short lifecycles. Regulatory requirements for food labeling further reinforce the role of display packaging as a vehicle for both compliance and marketing. With retailers demanding packaging that optimizes shelf replenishment while enhancing visual appeal, food and beverage companies continue to define the innovation roadmap for display packaging formats.

United States: Smart and Sustainable Display Packaging Enhances Retail and E-Commerce Appeal

The U.S. display packaging market is witnessing strong growth driven by rising consumer awareness of sustainability and eco-friendly retail solutions. Modern consumers and corporations are demanding aesthetically appealing, recyclable display packaging for both in-store and e-commerce channels. Technological advancements, including NFC (Near Field Communication) and AR (Augmented Reality) integration, are creating interactive and immersive retail experiences, allowing shoppers to access product information, exclusive content, or promotional offers by scanning the packaging.

Sustainability remains a key focus, with the American Forest & Paper Association (AF&PA) investing over $4.5 million between 2019 and 2025 in paper recycling infrastructure to enhance recycled paper capacity. The surge of e-commerce has increased demand for durable, tamper-evident display solutions that double as point-of-sale displays, particularly in the beauty and personal care sectors, where brands are using post-consumer recycled (PCR) materials to meet corporate sustainability goals. These trends highlight the U.S. market’s emphasis on innovative, eco-conscious, and digitally integrated display packaging.

Germany: Circular Economy and Advanced Printing Drive Display Packaging Innovation

Germany’s display packaging industry is strongly influenced by a stringent regulatory environment, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which mandates fully recyclable packaging by 2030 and sets reuse and refill targets. German manufacturers are increasingly developing eco-friendly display packaging incorporating high percentages of recycled content, reflecting the country’s leadership in the circular economy.

Technological innovation is also a key driver. Investments in advanced converting equipment and digital printing solutions allow cost-effective short runs, high-quality graphics, and consumer-centric branding initiatives. The combination of regulatory mandates, eco-conscious consumer preferences, and advanced production technologies positions Germany as a leading market for sustainable and innovative display packaging solutions in Europe.

China: Eco-Friendly Initiatives and E-Commerce Expansion Transform Display Packaging

China’s display packaging market is being reshaped by government-led sustainability initiatives, aligned with the dual carbon goal of achieving carbon peak and neutrality. Policies promoting eco-friendly, reduced, and reusable materials are encouraging manufacturers to adopt sustainable display packaging designs. Technological advancements, including AI-driven production, 5G integration, and industrial internet solutions, are enhancing production efficiency and enabling flexible manufacturing processes.

The rapid expansion of domestic e-commerce platforms is driving demand for display packaging that serves both online and offline retail channels. Trends are shifting toward minimalist yet visually striking designs that enhance brand visibility and consumer engagement. China’s market reflects a dynamic blend of sustainability regulations, technological innovation, and omnichannel retail demands, making it a fast-evolving hub for premium display packaging solutions.

India: Gifting Culture and Sustainable Innovations Propel Display Packaging Demand

India’s display packaging market is growing rapidly due to government initiatives like Make in India and Zero Effect Zero Defect, which support domestic production and infrastructure investment. The rising gifting culture, especially during festivals such as Diwali and Raksha Bandhan, is driving demand for premium, aesthetically pleasing display packaging across consumer goods.

Sustainability remains a crucial market driver. The Plastic Waste Management (Amendment) Rules are promoting eco-friendly alternatives, influencing manufacturers and retailers to adopt sustainable materials. Significant investments in new machinery and printing technology by companies such as Parksons Packaging are enhancing production efficiency and product quality. India’s display packaging market is thus characterized by eco-conscious innovations, premium design trends, and government-supported industrial growth, positioning it as a vibrant and evolving sector.

Display Packaging Market Report Scope

Display Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.7 Billion

|

|

Market Size (2034)

|

$26.1 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastic, Glass, Metal, Other Materials), By Packaging Type (Countertop Display, Floor Display, Power Wing Display, End-Cap Display, POP Display, Other Types), By End-Use Industry (Food & Beverages, Cosmetics & Personal Care, Pharmaceuticals & Healthcare, Consumer Electronics, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

WestRock Company, Graphic Packaging Holding Company, Smurfit Kappa Group, DS Smith plc, International Paper, Mayr-Melnhof Karton AG, Mondi Group, Amcor plc, Stora Enso Oyj, AR Packaging, Parksons Packaging Ltd., TCPL Packaging Ltd., Sonoco Products Company, Huhtamaki Oyj, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Display Packaging Market Segmentation

By Material Type

- Paper & Paperboard

- Plastic

- Glass

- Metal

- Other Materials

By Packaging Type

- Countertop Display

- Floor Display

- Power Wing Display

- End-Cap Display

- POP Display

- Other Types

By End-Use Industry

- Food & Beverages

- Cosmetics & Personal Care

- Pharmaceuticals & Healthcare

- Consumer Electronics

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Display Packaging Market

- WestRock Company

- Graphic Packaging Holding Company

- Smurfit Kappa Group

- DS Smith plc

- International Paper

- Mayr-Melnhof Karton AG

- Mondi Group

- Amcor plc

- Stora Enso Oyj

- AR Packaging

- Parksons Packaging Ltd.

- TCPL Packaging Ltd.

- Sonoco Products Company

- Huhtamaki Oyj

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology to provide a precise and actionable analysis of the global Display Packaging Market. This approach combined primary research, including interviews with key stakeholders such as packaging manufacturers, brand owners, retail experts, and sustainability consultants, with extensive secondary research from company reports, press releases, government regulations, and trade publications. Market sizing and forecasting were derived from historical data, production volumes, material adoption rates, and consumption trends across paperboard, plastics, glass, and metals, while segmentation focused on material type, packaging type, and end-use industries. Qualitative analysis emphasized emerging innovations such as digital printing, AR and NFC integration, plant-based and compostable substrates, and smart inventory systems, highlighting how sustainability and technological advancements are reshaping the market. Competitive landscape evaluation included mergers, strategic partnerships, and product diversification, offering industry professionals a robust view of growth opportunities, market dynamics, and technological and regulatory influences driving the Display Packaging Market through 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.