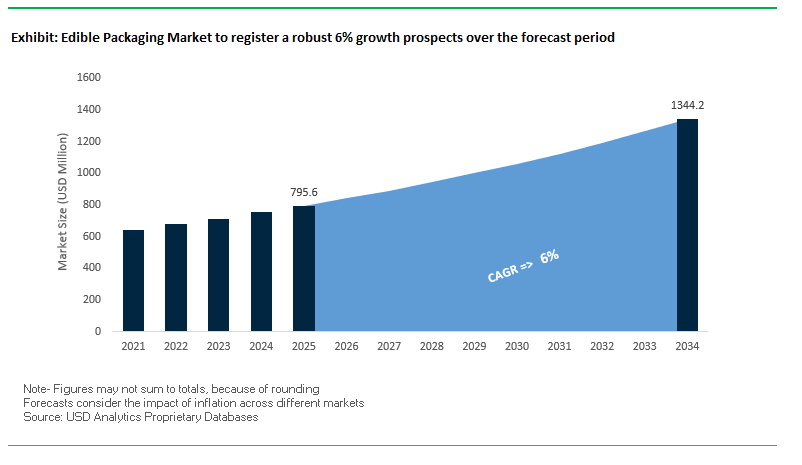

Market Overview: Edible Packaging Expands to $1.34B by 2034 at 6% CAGR, Fueled by Seaweed, Starch, and Plastic Bans

The global edible packaging market is projected to grow from $795.6 million in 2025 to $1.34 billion by 2034, advancing at a steady 6% CAGR. This rapid rise is powered by regulatory bans on single-use plastics, escalating consumer preference for eco-friendly alternatives, and breakthroughs in plant-based films and coatings. For senior professionals, key questions include how edible packaging integrates into mainstream FMCG supply chains, how shelf-life extension technologies can reduce food waste, and what strategies ensure cost competitiveness against conventional plastics.

Key Insights for buyers and industry leaders

- Ingredient innovation: Seaweed, cassava, and cornstarch dominate edible packaging R&D, creating films, sachets, and wrappers that are biodegradable and consumable.

- Shelf-life advantage: Edible coatings with antimicrobial properties extend freshness of fruits, vegetables, and proteins, reducing spoilage costs.

- Consumer readiness: Premium willingness-to-pay is rising, with eco-conscious shoppers driving early adoption across beverages, snacks, and QSR channels.

- Policy push: Plastic bans (e.g., India 2022) are transforming regulation into a mandated market for edible and compostable alternatives.

Market Analysis: Plastic Bans, Seaweed Scaling, and Strategic Partnerships (2024–2025)

The edible packaging landscape is being shaped by policy shifts, startup–corporate collaborations, and material science breakthroughs.

In September 2025, Hong Kong initiated a public consultation to expand restrictions into a full plastic cutlery ban by 2025, creating a strong runway for edible cutlery adoption. This follows global momentum where regulators are tightening gaps in earlier single-use rules, particularly in

Asia-Pacific markets. Similarly, in August 2025, YUTOECO launched a PFAS-free molded fiber oil-resistant packaging solution, signaling an industry-wide commitment to chemical-free, food-safe alternatives a principle also driving edible coatings.

Commercial partnerships are accelerating scaling capacity. Loliware secured an exclusive distribution deal with Entec in June 2025, extending seaweed-based products across North America, Central America, and the EU. Meanwhile, TIPA, in February 2025, introduced home-compostable pouch closures, complementing its January 2025 metallized barrier film important milestones in creating fully compostable snack packs.

Investment and M&A are validating edible packaging’s potential. In November 2024, Amcor moved to acquire Berry Global, strengthening its sustainable and edible packaging portfolio. At the startup level, UK-based Kelpi raised funding in October 2024 to expand its seaweed bioplastic line, and Brazil’s growPack received capital in September 2024 to pilot sustainable films, many of which serve as precursors to edible solutions. These developments reinforce edible packaging’s shift from pilot stage to scalable commercial adoption.

Trends and Opportunities Transforming the Edible Packaging Market

Strategic Corporate Investment and Piloting in Water-Soluble Pods and Films

The edible packaging market is witnessing rapid growth through corporate investment in water-soluble pods and films, driven by global consumer goods companies seeking breakthrough solutions to reduce plastic waste. Major players such as Unilever, PepsiCo, and Nestlé are investing in alternative packaging formats, including ultra-thin edible films and refill systems, with Unilever’s 2024 sustainability report highlighting pilot programs for dissolvable pods and bio-coated paper-based packaging. The adoption of polyvinyl alcohol (PVA) films already proven in household detergent pods, which represent nearly 30% of the U.S. detergent packaging market is paving the way for adaptation in food and beverage sectors. Companies like DisSolves are pioneering 100% natural, plastic-free dissolvable films as an alternative to fossil-based PVA, reflecting rising consumer demand for waste-free solutions. This trend is expected to accelerate as consumer familiarity with single-dose soluble formats expands beyond home care into food, beverage, and even nutraceutical applications.

Academic and Institutional R&D Focus on Bio-Polymer Performance Enhancement

The viability of edible packaging depends heavily on improving the barrier and mechanical performance of bio-based polymers to match conventional plastics. Universities, government-funded institutions, and private R&D centers are accelerating research into seaweed, starches, and chitosan-based films to strengthen their commercial application potential. A recent scientific paper demonstrated how advanced emulsion technology enhanced lipid-based films, improving their ability to resist moisture migration and thereby extending shelf life. Other studies highlighted cellulose-curcumin composites that combine improved barrier properties with antimicrobial and antioxidant benefits, offering the dual value of preservation and functional health appeal. Industry leaders are also exploring marine-biodegradable materials, such as Panasonic’s plant-derived cellulose fibers, which can be engineered into eco-friendly edible coatings. These innovations demonstrate that bio-polymers are no longer experimental but are becoming scalable solutions for food packaging that aligns with circular economy principles.

Development of Edible Barriers for Paper-Based Packaging

One of the most immediate opportunities in the edible packaging market is the integration of edible coatings and barriers into paper-based packaging, addressing the long-standing challenge of grease and moisture resistance without relying on PFAS or plastic liners. Startups are commercializing graphene oxide coatings that can improve paper strength by up to 30–50%, offering both enhanced durability and sustainable barrier protection. In parallel, research into natural waxes such as beeswax and soy wax has demonstrated that these edible coatings can significantly improve water vapor resistance, ensuring that packaging remains both functional and safe for food contact. These hybrid systems combine the structural integrity of paperboard with natural edible coatings, producing a fully curbside recyclable and compostable package. For quick-service restaurants and food delivery, such innovation provides a solution that meets tightening regulatory restrictions while also enhancing consumer appeal through sustainable branding.

Targeting the Premium “Experience-Driven” Food Service and Confectionery Segments

Before edible packaging achieves widespread cost competitiveness in mass markets, significant growth potential lies in premium and experiential food sectors. High-end restaurants, confectionery brands, and catering companies are adopting edible packaging as a differentiation strategy where the packaging itself becomes part of the customer experience. For instance, edible cocktail toppers made from sugar-based films can be custom-printed with branding or artistic designs, transforming a garnish into an immersive, shareable experience. Similarly, edible spoons and cutlery made from rice, wheat, and sorghum are being embraced by premium caterers and restaurants in response to global plastic cutlery bans, combining functionality with sustainability. The zero-waste value proposition resonates strongly with environmentally conscious consumers willing to pay a premium for waste-free solutions. Products like edible coffee or tea pods deliver both convenience and novelty, positioning edible packaging as not just a sustainable alternative, but a luxury-driven, consumer engagement tool in the food service industry.

Competitive Landscape: Startups Drive Seaweed and Starch Innovation, While Leaders Consolidate Sustainable Portfolios

The edible packaging market is a mix of pioneering startups leveraging seaweed and bioresins and established packaging leaders expanding sustainable portfolios. Competition is defined by material IP, scaling capacity, and partnerships with FMCG brands.

Loliware Inc. Scaling Seaweed-Based SEA Technology™ Globally

Loliware leverages its proprietary SEA Technology™ bioresin, derived from seaweed, to create edible straws, cups, and other compostable formats. Its core strength lies in its ability to use existing plastic manufacturing infrastructure for seamless adoption. In June 2025, it partnered with Entec for North America and EU expansion, positioning itself to replace billions of single-use plastics. Loliware’s strategy focuses on large-scale plastic replacement with Fortune 500 collaborations and hospitality adoption.

Notpla Limited Regenerative Seaweed Films and Edible Cups

UK-based Notpla creates regenerative packaging from seaweed and plants, including films, sachets, and edible cups. A winner of the Google Single-Use Plastics Challenge, Notpla emphasizes materials that naturally disappear post-use. Recent launches include an edible cup and film for condiments and snacks, underscoring versatility. Its focus remains on flexible packaging displacement, aiming for wide integration into FMCG supply chains.

MonoSol, LLC PVOH Expertise Expands to Food-Grade Films

As a subsidiary of Kuraray, MonoSol specializes in water-soluble PVOH-based films widely used in detergents but expanding into food-grade edible formats. Its films are designed to biodegrade in wastewater and other environments, making them a sustainable dosing and wrapping solution. MonoSol’s strength lies in chemistry expertise and its ability to integrate soluble films into food and beverage applications.

TIPA Corp Ltd. Compostable Films and Pouch Closures Driving Circularity

TIPA produces fully compostable flexible films and laminates that operate on existing converting equipment. Its February 2025 home-compostable pouch closure and January 2025 metallized barrier film reinforced its leadership in high-performance sustainable packaging. While not all solutions are edible, TIPA is pivotal in the transition to a circular economy, creating food-safe, compost-ready films that compete with plastics in durability and barrier properties.

Evoware Seaweed-Based Edible Films with Nutritional Benefits

Indonesian startup Evoware develops biodegradable and edible films/wrappers from seaweed. Unique in its positioning, Evoware’s products not only replace plastics but also contain nutrients, adding consumer value. In late 2024, the company gained visibility at Trade Expo Indonesia, seeking international partners. Its mission, branded as “RethinkPlastic,” blends sustainability with social impact, empowering businesses to adopt affordable, eco-safe packaging alternatives.

Edible Packaging Market Share Insights

Food & Beverages Dominate Market Share by Application in Edible Packaging

The food and beverages sector commands a massive 85% share of the edible packaging market in 2025, positioning itself as the primary testing ground for this transformative innovation. Single-serve products like condiments, coffee pods, and snack wraps are the leading adopters, as edible formats eliminate packaging waste and integrate directly into consumption. Growth is fueled by sustainability initiatives from major food brands seeking to meet aggressive waste reduction targets while enhancing consumer experiences through edible wrappers and coatings. Pharmaceuticals and medical applications, while smaller in share, add high-value use cases with edible films and dissolvable strips designed for precise dosing and improved compliance. Meanwhile, experimental applications such as edible water pods and dissolvable cutlery serve as innovation showcases, driving consumer awareness and shaping the future trajectory of this emerging industry.

Films & Wraps Lead Market Share by Product Type in Edible Packaging

Among product types, films and wraps hold 40% share in 2025, making them the most versatile and commercially viable format in the edible packaging market. Leveraging materials like seaweed extracts, starch, and proteins, these films provide scalable solutions for candies, cheese blocks, and single-serve sachets of instant mixes. Coatings, accounting for 35%, play a quieter but equally impactful role in extending shelf life of fresh produce without altering consumer behavior, making them a silent growth engine. Capsules remain well-established in pharmaceuticals and supplements, while edible cutlery and tableware continue to act as novelty-driven concepts that generate marketing buzz rather than mass adoption. Together, these product types highlight the dual growth path of the market scalable solutions for mainstream food systems on one hand, and high-visibility niche innovations on the other.

United States: Biopolymer Innovation and Automated Production Driving Edible Packaging Growth

The U.S. edible packaging market is a global hub for research and development of advanced biopolymers, with a focus on plant-based sources such as corn and soy. Government support through USDA and DOE grants for pilot plants is fostering innovation in edible films and coatings. Companies are investing in automation-ready manufacturing lines to address labor shortages and scale up production, meeting the growing commercial demand from consumer packaged goods (CPGs) companies.

Regulatory pressures, particularly state-level mandates on PFAS ("forever chemicals"), are driving innovation in edible coatings that provide grease and moisture barriers without fluorinated chemistries. Integration of edible packaging into single-serve and on-the-go food products, including films for seasoning packets and coatings for fruits, is helping to reduce food waste while enhancing convenience and sustainability.

Germany: Leading the Shift to Sustainable and Circular Edible Packaging

Germany’s edible packaging market is at the forefront of Europe’s move toward sustainable solutions, heavily influenced by the European Green Deal and strict national environmental policies. Innovation focuses on improving barrier properties of edible packaging to ensure food safety. For instance, PAPACKS has developed plant-based coatings that provide a plastic-free barrier for paper-based packaging, ideal for baked goods and chocolates, supporting a circular economy.

The market is characterized by strong B2B collaborations, where packaging manufacturers partner with food companies to develop customized edible solutions integrated into production lines. The country is also witnessing a surge in edible and compostable products, including molded fiber and paper-based solutions, catering to both consumer demand and regulatory requirements on waste management.

China: Government Initiatives and Food Safety Regulations Accelerating Edible Packaging Adoption

China’s edible packaging market is driven by government initiatives to reduce food loss and waste, such as the Food Conservation and Anti-Food Waste Action Plan. This creates a favorable environment for edible packaging solutions that extend shelf life and improve supply chain efficiency. Regulatory frameworks under the Food Safety Law are emphasizing food safety, traceability, and safe materials, prompting manufacturers to innovate with edible films that comply with new standards.

Chinese companies and researchers are developing cost-effective edible films using traditional materials such as rice and wheat starch, offering practical solutions for domestic and export markets. The focus on food safety, functional performance, and compliance is a key driver for market growth.

India: Edible Cutlery and Bioplastic Innovations Driving Market Expansion

India’s edible packaging market is expanding rapidly, fueled by the national ban on single-use plastics and the growing food delivery and catering industry. There is a significant rise in edible cutlery and tableware made from grains such as rice, wheat, and sorghum, offering sustainable alternatives to plastic. Companies are innovating with bioplastic and starch-based materials, including bagasse and natural starches, aligning with government regulations and consumer demand for eco-friendly solutions.

Research and development efforts are increasingly focused on edible coatings for fruits and vegetables to extend shelf life and reduce post-harvest food loss. Collaborations between academic institutions and private companies are driving innovation, ensuring that India becomes a prominent player in sustainable edible packaging solutions.

Brazil: Agro-Industrial Byproducts and Functional Innovations Leading Market Trends

Brazil is leveraging its agro-industrial byproducts to develop edible packaging, with research led by institutions such as Embrapa. Edible films from materials like tomato, spinach, papaya, and sugarcane bagasse not only reduce waste but also create new revenue streams for farmers. The inclusion of antimicrobial and antioxidant compounds, such as pine resin and fruit extracts, extends the shelf life of perishable foods like fresh meat and cheese, representing a significant technological advancement.

Partnerships between research institutions and private companies are focused on scaling production of edible packaging materials for commercial applications. This collaboration is critical to move innovations from laboratory research to industrial manufacturing, creating sustainable and functional packaging solutions.

Japan: Precision-Driven R&D and Water-Soluble Innovations for Edible Packaging

Japan’s edible packaging market emphasizes precision, high-quality R&D, and functional performance. Companies are developing edible films with precise texture, transparency, and consistency, catering to both food and pharmaceutical applications. A key innovation is water-soluble, oil-resistant pouches made from polyvinyl alcohol and sodium alginate, suitable for single-serving sauces and condiments, eliminating the need for plastic packaging.

The Japanese pharmaceutical and medical industries are integrating edible films for capsules and casings, focusing on safe, tasteless, and high-purity materials. This approach highlights Japan’s commitment to functional, sustainable, and safe edible packaging solutions for both food and medical applications.

Edible Packaging Market Report Scope

Edible Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$795.6 Million

|

|

Market Size (2034)

|

$1344.1 Million

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Material Type (Polysaccharides, Proteins, Lipids, Other Materials), By Application (Food and Beverages, Pharmaceuticals & Medical, Other Applications), By Product Type (Films, Coatings, Capsules, Cutlery and Tableware)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cargill, Incorporated, DuPont de Nemours, Inc., Archer-Daniels-Midland Company, Monosol LLC, Notpla Ltd., Loliware Inc., TIPA Corp. Ltd., SABIC, Gelita AG, Ingredion Incorporated, Tate & Lyle plc, Eco-Friendly Foods, WikiCell Designs Inc., Evoware, JRF Technology LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Edible Packaging Market Segmentation

By Material Type

- Polysaccharides

- Proteins

- Lipids

- Other Materials

By Application

- Food and Beverages

- Pharmaceuticals & Medical

- Other Applications

By Product Type

- Films

- Coatings

- Capsules

- Cutlery and Tableware

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Edible Packaging Market

- Cargill, Incorporated

- DuPont de Nemours, Inc.

- Archer-Daniels-Midland Company

- Monosol LLC

- Notpla Ltd.

- Loliware Inc.

- TIPA Corp. Ltd.

- SABIC

- Gelita AG

- Ingredion Incorporated

- Tate & Lyle plc

- Eco-Friendly Foods

- WikiCell Designs Inc.

- Evoware

- JRF Technology LLC

*List not Exhaustive

Research Coverage

This report investigates the dynamic global edible packaging market, offering comprehensive insights into material innovations, application trends, and emerging business models shaping the industry. USDAnalytics’ analysis reviews breakthroughs in seaweed, starch, and protein-based films, as well as the integration of edible coatings and dissolvable pods into mainstream FMCG and pharmaceutical supply chains. The report highlights strategic partnerships, investment activity, and regulatory drivers, including global single-use plastic bans, that are accelerating adoption and commercial scalability. This report is an essential resource for packaging executives, sustainability leads, and R&D managers seeking actionable intelligence on barrier-enhanced bio-polymers, functional coatings, and novel product formats such as edible cutlery and capsules. Additionally, it provides in-depth company profiling, examines competitive landscapes, and identifies technological trends and high-value market opportunities. By bridging scientific research with market adoption, USDAnalytics delivers a resource that enables stakeholders to navigate risk, optimize material selection, and capitalize on evolving consumer demand for eco-conscious packaging while maintaining food safety and cost efficiency.

Scope Highlights:

- Segmentation: By Material Type (Polysaccharides, Proteins, Lipids, Other Materials); By Application (Food and Beverages, Pharmaceuticals & Medical, Other Applications); By Product Type (Films, Coatings, Capsules, Cutlery and Tableware)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: In-depth profiles and analysis of 15+ companies, including Cargill, DuPont, Monosol, Notpla, Loliware, TIPA, SABIC, Gelita, Ingredion, Tate & Lyle, Eco-Friendly Foods, WikiCell Designs, Evoware, and JRF Technology

Methodology

The research methodology applied in this report combines both primary and secondary approaches to ensure a high level of accuracy and comprehensiveness. Primary research includes interviews with senior executives, R&D managers, and sustainability officers across leading edible packaging firms to validate product adoption, regulatory impact, and market trends. Secondary research incorporates trade publications, patent filings, company annual reports, government policies, and scientific literature to track material innovations, functional performance, and commercial scale-up. Market sizing and forecasts are generated using a combination of bottom-up and top-down modeling, factoring in historical growth patterns, technological adoption curves, regulatory pressures, and consumer behavior trends. Competitive benchmarking involves detailed profiling of major players, including SWOT analysis, strategic partnerships, and mergers & acquisitions activity, while regional analysis integrates macroeconomic, policy, and supply chain considerations. USDAnalytics applies a rigorous validation process to cross-check data points, ensuring a reliable framework for decision-making and strategy formulation for industry professionals.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.