Enhanced Fire Protection Systems Market Overview Anchored in NFPA Compliance and Critical Asset Protection

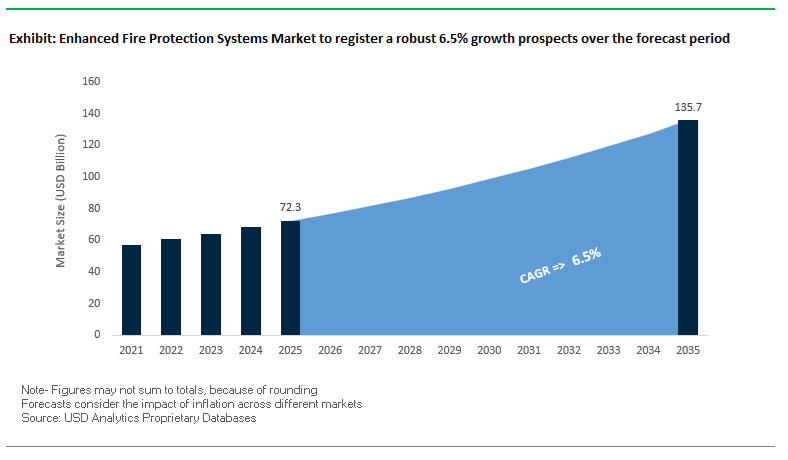

The global enhanced fire protection systems market is projected to grow from USD 72.3 billion in 2025 to USD 135.7 billion by 2035, registering a solid CAGR of 6.5% (2025–2035). This growth is underpinned by tightening NFPA, ISO, and building safety regulations, rapid digitalization of fire detection, and the rising value density of assets in data centers, high-rise residential, oil & gas, and critical industrial facilities. For manufacturers and vendors of clean agent systems, high-pressure water mist solutions, inert gas systems, and intelligent detectors, the market is shifting from simple code-compliance toward data-driven, high-availability, and sustainability-aligned fire protection.

From an engineering standpoint, enhanced fire protection systems are increasingly specified on the basis of quantifiable performance metrics and maintenance KPIs, rather than purely on upfront cost. NFPA 2001–compliant clean agent fire suppression, high-pressure water mist (HPMW) with tightly controlled droplet sizes, and inert gas discharge systems optimized for sub-60-second flooding are now baseline expectations in premium projects. Vendors that can combine robust hardware with IoT-enabled monitoring, AI analytics, and easy retrofitting are best positioned to capture this expanding demand.

Key technical and commercial insights for manufacturers and vendors

- Tight NFPA 2001 agent loss tolerance drives precision monitoring- Refillable containers for halocarbon clean agent fire suppression systems must be refilled or replaced if they exhibit >5% agent loss or a >10% pressure loss (temperature-compensated). This low tolerance is accelerating demand for high-precision monitoring technologies, such as ultrasonic liquid level indicators and smart cylinder pressure sensors, across mission-critical facilities.

- Maintenance KPIs redefine fire protection system readiness- In high-risk industrial facilities, leading operators target ≥95% on-time preventive maintenance (PM) completion each month as a core metric of fire protection system readiness. Achieving this level significantly reduces corrective maintenance (CM) interventions, lowers unplanned downtime, and improves overall operational safety health, creating a strong business case for connected CMMS-integrated fire systems.

- High-pressure water mist systems reduce water damage in sensitive sites- High-pressure water mist (HPMW) systems used in data centers, archives, museums, and process control rooms generate micro-droplets with a volume median diameter (VMD) < 200 μm. This fine droplet spectrum maximizes heat absorption and oxygen displacement while minimizing residual water volume, making HPMW the preferred enhanced fire protection technology where water damage risk is almost as critical as the fire itself.

- Inert gas systems engineered for sub-60-second discharge- Inert gas suppression systems (e.g., argon, nitrogen blends) designed for critical asset protection are optimized to reach the minimum design concentration within 60 seconds, in line with NFPA and ISO requirements. This rapid discharge is essential to interrupt sustained combustion in control rooms, server halls, and high-value industrial enclosures, pushing demand for high-flow valves, robust piping, and precision flow calculations.

Market Analysis: Digital Twins, PFAS-Free Foams, and IoT Rules Reshaping Fire Protection

The enhanced fire protection systems industry is being reshaped by a combination of smart building technologies, environmental regulations, and sector-specific risk profiles. In November 2025, Johnson Controls launched a digital twin-enabled fire detection platform for commercial buildings that leverages AI-powered modeling to predict fire spread trajectories with around 90% accuracy during design and simulation. This marks a major inflection point where fire detection, life safety engineering, and BIM/digital twin ecosystems converge, allowing consultants and owners to optimize detector layouts, suppression coverage, and evacuation strategies before a single device is installed. Complementing this, research published in April 2024 on multi-sensor fire detectors using machine learning demonstrated a 45% reduction in nuisance alarms in dusty industrial settings, signaling a transition toward algorithm-enhanced, multi-criteria fire detection that can differentiate real fires from process emissions and dust.

Environmental compliance is another powerful growth vector in the enhanced fire protection systems market. In August 2025, Minimax Viking Group commissioned a new manufacturing line in Mexico dedicated to fluorine-free foam concentrates, directly targeting the global phase-down of PFAS-containing firefighting foams. This investment positions fluorine-free foam as the new standard for oil & gas, aviation, and industrial tank farm fire protection, and creates room for R&D on foam performance optimization with environmentally benign surfactant systems. Concurrently, Tyco Fire Protection Products launched a new corridor sprinkler family in September 2025, engineered specifically for narrow spaces, which meets UL listing requirements while lowering installation costs by roughly 15% per m². These product launches underscore a broader trend toward application-specific hardware that balances code compliance, cost efficiency, and environmental performance.

Policy and long-term investment decisions are also catalyzing the adoption of enhanced fire protection systems. In March 2025, the UK Health and Safety Executive (HSE) mandated IoT-enabled monitoring systems for fire panels in all high-rise residential buildings, enforcing real-time remote diagnostics and improved compliance with the Building Safety Act. This has effectively made connected fire safety infrastructure a regulatory requirement in a key segment, spurring demand for cloud-connected panels, remote service platforms, and cybersecurity-hardened endpoints. In parallel, a leading data center operator announced a USD 50 million retrofit program in December 2024 to upgrade legacy sites with preaction sprinkler systems and inert gas agents, emphasizing uptime, damage mitigation, and NFPA-compliant redundancy for mission-critical IT infrastructure. Added to this are long-term partnerships such as the January 2024 agreement between a major European oil & gas engineering firm and a gaseous suppression provider to deploy SIL 3–compliant fire and gas systems on offshore platforms, illustrating how functional safety standards and asset integrity programs are expanding the addressable market for advanced detection and suppression solutions.

Breakthrough Suppression Mechanisms and Predictive Detection Capabilities Accelerating Market Opportunities

Market Trend 1: Mandated Aerosol and Water Mist Suppression Technologies to Mitigate Lithium-Ion BESS Thermal Runaway Risks

Growing deployments of lithium-ion Battery Energy Storage Systems (BESS) in utility-scale, commercial, and industrial facilities are driving strict regulatory enforcement around fire propagation control. The UL 9540A test standard sets the benchmark for evaluating thermal runaway propagation, and modern enhanced fire protection systems are engineered to limit fire spread to fewer than one adjacent module, a performance threshold now required for certification in many jurisdictions. Condensed aerosol systems demonstrate strong relevance because they maintain agent concentration above the critical suppression threshold for ≥30 minutes, compliant with EN-15276-1 and ISO-15779—triple the hold time of some legacy suppression agents, which average around 10 minutes and are insufficient for cooling high-energy cells.

Complementing aerosol suppression, water mist systems are engineered to meet the high wetting intensity requirement of 12.2 mm/min per 50 kWh, providing rapid convective cooling essential for preventing temperature rebound. BESS installations with gas concentrations near 25% of the Lower Flammable Limit (LFL) must also integrate explosion suppression or deflagration venting under NFPA 69, positioning advanced fire protection solutions as mandatory infrastructure. Collectively, these engineering requirements elevate the role of aerosol suppression, water mist technologies, and gas management systems as core components of next-generation BESS fire safety strategies, reshaping market demand dynamics.

Market Trend 2: AI-Powered Video Analytics and VESDA Becoming the New Standard for Ultra-Early Detection in High-Value Critical Infrastructure

Critical environments such as data centers, semiconductor fabs, aviation facilities, and hyperscale computing infrastructure increasingly depend on aspirating smoke detection (ASD) combined with AI-driven verification. VESDA systems, with a sensitivity range of 0.005%–20% obscuration/m, are hundreds of times more sensitive than conventional photoelectric detectors. Their ability to detect smoke concentrations as low as 0.1% obs/m—equivalent to smoldering insulation at microscopic levels—enables intervention long before a fire becomes self-sustaining.

The integration of AI-based video analytics significantly reduces false alarms by confirming smoke or flame signatures after a VESDA alert, enabling near-zero false-positive suppression activations in high-value assets. Because VESDA actively samples air, it performs reliably in high-ACH environments like data centers where stratification and dilution undermine the effectiveness of passive detectors. This trend is redefining early-warning architectures, with AI-VESDA hybrids emerging as the preferred detection model for mission-critical, ultra-low-tolerance applications.

Market Opportunity 1: Rapid Commercialization of Non-Toxic Short-Chain and Fluorine-Free Foams to Replace Legacy PFAS-Based Agents

The global pivot away from PFOS/PFOA-containing firefighting agents is creating major growth opportunities for fluorine-free foams (F3) and short-chain C6 foams engineered for high-performance aviation and industrial fire suppression. F3 agents are now being certified to the stringent MIL-PRF-32725 (MILSPEC) standard—historically difficult for fluorine-free chemistry to achieve—and are accepted for FAA Part 139 compliance. Performance requirements include a minimum expansion ratio ≥7.0, a 25% drainage time of ≥3.5 minutes, and robust burn-back resistance.

Crucially, next-generation C6 foams maintain purity levels below 10 ppm of C8 PFOS/PFOA, ensuring compliance with global PFAS regulations. Manufacturers must also meet corrosion limits such as ≤1.5 mils/year corrosion rate on cold-rolled steel to ensure compatibility with firefighting hardware. These specifications open a profitable pathway for suppliers capable of delivering F3 agents that match or exceed the performance of AFFF while eliminating environmental toxicity concerns, positioning fluorine-free foam technologies as central to future aviation, petrochemical, and industrial fire protection strategies.

Market Opportunity 2: Standardized Deployment of Compressed Air Foam Systems (CAFS) for Wildland-Urban Interface (WUI) Protection

As wildfire intensity accelerates globally, CAFS is rapidly becoming the preferred technology for WUI fire defense, offering substantial operational advantages over traditional water-based suppression. CAFS reduces water consumption dramatically—achieving fire extinguishment using less than one-third the water and completing suppression in one-third the time compared to water alone. The enhanced knockdown power provides up to a fivefold increase in suppression effectiveness, a critical advantage during fast-moving wildfire conditions.

CAFS-generated foam, with adjustable expansion ratios from 1:10 (dry) to 1:3 (wet), adheres strongly to vertical structures and vegetation, forming a consistent thermal barrier that prevents ignition by radiant heat. This foam blanket delays combustible material ignition and increases available evacuation or response time. For municipal fire departments, forestry agencies, and private property protection services, CAFS delivers a scalable, high-value solution for reducing wildfire damage. As WUI risk continues to rise, the demand for standardized CAFS deployment protocols and purpose-built equipment is set to increase substantially.

Enhanced Fire Protection Systems Market Share Analysis

Market Share by System Type: Active Fire Protection Systems Lead Due to Mandatory Compliance and Technology-Driven Rapid Response

Active Fire Protection (AFP) Systems hold the largest share of the global enhanced fire protection systems market—approximately 55% in 2025—because they provide the immediate, technology-enabled response capabilities required to detect, suppress, and contain fire incidents before they escalate. AFP solutions—including advanced fire detection networks, intelligent alarm panels, automatic sprinkler systems, water mist systems, gaseous and clean-agent suppression units—are foundational in meeting stringent global fire safety codes, such as NFPA, EN standards, and regional building mandates for commercial and high-occupancy structures. Compared to passive fire protection systems, AFP generates higher revenue per installation due to its reliance on complex electronics, integrated sensors, connectivity hardware, and mechanically engineered suppression infrastructure. Rising adoption of IoT-enabled fire detection, AI-based threat differentiation, predictive maintenance algorithms, and cloud-connected monitoring platforms has further accelerated investment in AFP. As buildings transition into smart infrastructure ecosystems, AFP systems become essential for real-time oversight, remote diagnostics, and faster emergency response—directly contributing to reduced property damage and improved life safety outcomes. This strong regulatory, technological, and operational value proposition solidifies AFP’s dominant share in the global market.

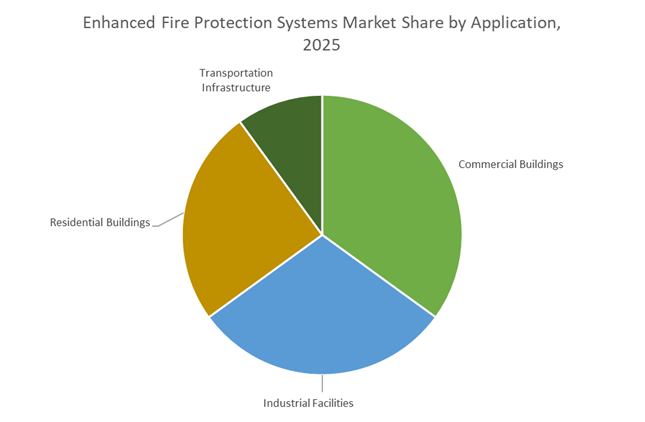

Market Share by Application: Commercial Buildings Dominate as High-Occupancy Structures Require Robust, Redundant Fire Protection

The Commercial Buildings segment accounts for ~35% of the global enhanced fire protection systems market, driven by stringent regulatory mandates, high asset density, and the elevated life safety risk associated with large, continuously occupied premises. Office towers, hospitals, hotels, retail centers, educational institutions, laboratories, and data centers all require comprehensive fire detection, alarm, communication, and suppression systems due to the concentration of people, valuable equipment, and sensitive operational environments. Data centers, for instance, demand premium clean-agent systems that suppress fires without damaging electronics, while hospitals require integrated smoke control, sprinklers, alarms, and emergency communication systems that function reliably around the clock. The rapid expansion of commercial real estate—particularly high-rise developments in Asia-Pacific and the Middle East—continues to drive first-time installation demand, while aging infrastructure in North America and Europe fuels retrofit activity aimed at meeting evolving fire safety codes. Because commercial buildings typically install the most extensive, redundant, and technologically advanced fire protection architectures, they remain the largest contributor to market revenue and a central growth engine for AFP and PFP system providers globally.

Country Analysis: Global Drivers in Enhanced Fire Protection Systems Development

United States: AI-Driven Fire Intelligence, Lithium-Ion Fire Protection, and NFPA-Centric Compliance Expansion

The United States remains the center of innovation in the Enhanced Fire Protection Systems Market, driven by strict NFPA regulatory frameworks, rapid adoption of artificial intelligence in fire detection, and heavy federal investment in critical infrastructure security. The deployment of AI-enabled alarm and analytics platforms—such as Honeywell’s airport-scale systems launched in 2024—has significantly transformed monitoring accuracy in high-traffic, mission-critical environments. These systems reduce false alarms, improve triage capability, and allow real-time risk interpretation, positioning the U.S. as the global leader in intelligent fire detection algorithms.

Additionally, modernization mandates coming from the U.S. Department of Defense (DoD) in 2025 accelerated the adoption of advanced suppression systems in military depots, protecting hazardous materials, ammunition storage, and classified assets. Cloud-integrated platforms like Johnson Controls’ OpenBlue now allow national-scale operators to remotely monitor compliance, conduct predictive maintenance, and assess multi-site fire system health through real-time analytics—shifting the industry toward service-based and cloud-enabled fire management models. The U.S. is also a leading adopter of specialized Li-ion battery fire suppression technologies, driven by EV charging expansion and rising ESS deployments. Manufacturers like Amerex are bringing to market new Class D and lithium-ion–specific extinguishing agents designed for thermal runaway. Meanwhile, the sustained preference for clean agent systems such as NOVEC 1230 alternatives—primarily in data centers—underscores the country’s long-term shift toward asset-protective, non-water suppression systems in high-value digital infrastructure.

China: Smart City Fire Integration, High-Rise Compliance Expansion, and Industrial-Grade Suppression Growth

China’s Enhanced Fire Protection Systems Market is strongly influenced by rapid urbanization, aggressive high-rise construction, and national initiatives to create fully networked Smart City fire ecosystems. The government’s increasingly stringent fire codes for high-density residential and commercial towers—especially amid the growth of 40+ story real estate clusters—have intensified demand for integrated fire detection, water mist suppression, and advanced alarm systems capable of covering large vertical complexes. In 2025, compliance requirements for high-rise insulation, emergency evacuation routes, and automated suppression systems became a major driver of fire systems procurement nationally.

China’s Smart City initiatives are pushing the deployment of IoT-enabled fire panels, street-level detectors, and cloud-connected municipal oversight systems that allow thousands of fire devices to be monitored in real time. These municipal-scale networks drastically shorten response times and offer integrated analytics for population-dense areas. Alongside urban upgrades, China’s massive industrial base—including chemicals, automotive, and electronics—continues to accelerate the adoption of high-performance foam-based, dry chemical, and deluge suppression systems to meet industrial safety regulations. As China scales manufacturing in its industrial parks, demand for rugged fire systems engineered for hazardous environments continues to climb.

Germany: Mandatory Passive Retrofitting, Low-GWP Suppression Transition, and High-Pressure Water Mist Adoption

Germany remains one of the most regulation-driven markets for Enhanced Fire Protection Systems, underpinned by nationwide commitments to building safety and environmental performance. In 2025, the German government mandated passive fire protection upgrades across public schools, catalyzing nationwide retrofitting activity involving fire-rated barriers, intumescent materials, and advanced compartmentation solutions. These regulations have intensified demand for certified passive fire products and expanded service opportunities for installers and materials suppliers.

Simultaneously, the European Union’s 2024 fluorinated gas phase-down regulation compelled manufacturers, industrial facilities, and commercial buildings to transition to low-GWP clean agent systems and environmentally sustainable suppression technologies. This accelerated market traction for water mist systems, inert gas blends, and next-generation synthetic agents. Siemens’ strategic acquisition of Danfoss Fire Safety in late 2024 strengthened Germany’s leadership in high-pressure water mist systems, a favored solution for data centers, tunnel networks, heritage sites, and critical infrastructure. Germany’s broader sustainability orientation ensures that the growth of Enhanced Fire Protection Systems continues to align with circular-economy goals, energy efficiency standards, and reduced environmental impact.

United Arab Emirates: Predictive AI Safety Intelligence and High-End Micro-Mist Suppression for Luxury Infrastructure

The United Arab Emirates is emerging as a global early adopter of next-generation AI-driven predictive fire protection technologies, largely due to its constant development of luxury skyscrapers, mega-malls, and smart urban districts. Emaar’s 2025 deployment of predictive fire AI demonstrated the capability to detect electrical anomalies and identify potential ignition pathways up to 48 hours in advance with 92% accuracy, marking one of the most advanced real-world applications of AI in fire safety. These systems integrate thermal imaging, real-time load monitoring, and machine-learning algorithms to strengthen early-stage detection in high-value commercial towers.

Additionally, the UAE is adopting micro-mist sprinkler systems, which reduce water usage by up to 50% while offering superior cooling and oxygen displacement—making them ideal for luxury hotels, museums, financial hubs, and architecturally sensitive spaces. The Dubai Civil Defence (DCD) continues to enforce some of the most rigorous regional fire codes, mandating comprehensive integrated fire protection solutions for all new high-rise buildings. This regulatory rigor maintains continuous momentum for premium fire suppression equipment, smart detection systems, and predictive analytics platforms throughout the Gulf region.

Canada: Urban High-Rise Retrofitting and Clean-Tech–Driven Fire Safety Incentives

Canada’s Enhanced Fire Protection Systems Market is shaped by retrofitting initiatives across aging high-rise infrastructure and government-supported clean-technology investments. In 2025, Toronto implemented a major mandate requiring all older high-rise buildings to undergo fire-resilient retrofitting, including sprinkler modernization, upgraded alarm communication infrastructure, and replacement of legacy passive fire materials. This policy triggered a wave of commercial and residential investments aimed at strengthening building safety across major metropolitan regions.

In parallel, provincial governments are offering clean-tech grants that incentivize the integration of AI-driven predictive fire systems, remote monitoring platforms, and environmentally friendly suppression technologies such as water mist and non-fluorinated clean agents. These incentives are particularly impactful in public housing, universities, and municipal facilities. Canada’s combined emphasis on sustainability, modernization, and risk mitigation positions it as a fast-evolving market for advanced fire detection and suppression systems, especially in climate-sensitive and high-density urban regions.

Competitive Landscape: Global Leaders in Integrated Detection and Suppression Solutions

The competitive landscape of the enhanced fire protection systems market is dominated by a mix of global diversified building technology players and specialized fire safety groups. Companies such as Johnson Controls, Minimax Viking Group, Carrier Global, Siemens, and Halma bring complementary strengths across digital fire detection, gaseous and water-based suppression, fluorine-free foams, water mist, and niche automatic suppression technologies. Their strategies converge around integrated platforms, smart building connectivity, special-hazard expertise, and recurring service revenues, reflecting the market shift from one-off system sales toward lifecycle management and performance-based fire protection.

Johnson Controls: Digital twin-enabled and connected fire protection platforms

Johnson Controls, through brands such as Tyco Fire Protection Products, ANSUL, and ZETTLER, offers one of the broadest portfolios of fire detection and suppression systems globally, spanning clean agent, gaseous, and water-based suppression as well as intelligent detection. Its core strategic differentiator in the enhanced fire protection systems industry is the tight integration of these solutions with the OpenBlue smart building platform, enabling connected fire sprinkler systems, predictive maintenance, and portfolio-wide analytics. The November 2025 launch of a digital twin-enabled fire detection platform for commercial buildings further strengthens Johnson Controls’ position in AI-driven fire engineering, giving building owners the ability to simulate fire spread, optimize device placement, and streamline code-compliance documentation.

Minimax Viking Group: Special-hazard water mist and gaseous suppression expertise

Minimax Viking Group specializes in complex industrial and high-risk fire protection projects, providing Minifog high-pressure water mist systems, Oxeo inert gas systems, spark extinguishing solutions, and foam suppression technologies. Its dedicated fire research center in Germany underpins proprietary water mist nozzle and droplet engineering, resulting in systems optimized for machinery spaces, archives, and now lithium-ion battery storage. In July 2025, the group introduced Minifog ProCon XP, a high-pressure water mist system designed specifically for lithium-ion battery storage facilities, where enhanced cooling, containment, and re-ignition control are critical. With over 10,500 employees globally and a full-service model from design to maintenance, Minimax Viking is a key competitor in fluorine-free foams and HPMW solutions, reinforced by its August 2025 F3 foam production expansion in Mexico.

Carrier Global Corporation: Detection-centric fire protection with strong aftermarket

Through brands such as Kidde Fire Protection, Range Guard, and Autronica Fire and Gas, Carrier Global focuses on high-value detection technologies and specialized pre-engineered systems. Its portfolio includes high-sensitivity smoke detection (HSSD), industrial fire and gas detection for harsh environments, and restaurant and vehicle fire suppression solutions. Carrier’s strategic emphasis is on commercial and industrial detection where early warning and nuisance-alarm reduction are essential, supported by Autronica’s advanced detector platforms. The company’s extensive global service network for inspection, testing, and maintenance (ITM) provides significant recurring revenue and enhances system reliability, positioning Carrier as a preferred partner for operators seeking long-term compliance and lifecycle support for their enhanced fire protection systems.

Siemens AG: Fully integrated fire safety within building automation ecosystems

Siemens leverages its strengths in building technologies and automation to deliver fully integrated fire safety solutions centered on Cerberus™ PRO fire detection systems and Sinorix™ suppression platforms. A key differentiator is the native integration of fire safety systems with the Desigo building management system, using BACnet/IP and secure networking to support scalable, resilient building-wide safety architectures. Siemens’ advanced multi-criteria detectors employ proprietary signal analysis algorithms to provide early warning while minimizing false alarms, particularly important in complex commercial and industrial environments. Its strategy in the enhanced fire protection systems market is to deliver holistic building safety and security, enabling facility owners to orchestrate HVAC, access control, and fire protection within a single digital backbone for better risk governance and energy efficiency.

Halma plc: Specialist niche fire detection and compact suppression technologies

Halma operates a portfolio model built around acquiring and scaling specialized safety technology companies, including Apollo Fire Detectors, Firetrace Automatic Suppression, and Advanced Fire Systems (AFS). Apollo provides a wide array of conventional and addressable detectors used in commercial buildings and industrial facilities, while Firetrace focuses on direct-to-source compact fire suppression for electrical cabinets, CNC machines, engine compartments, and small enclosures—a rapidly growing niche in enhanced fire protection. Halma’s group-wide R&D investment typically exceeds 5% of revenue, fuelling a steady pipeline of innovative detectors, control panels, and localized suppression solutions tailored to specialist applications. This “federated specialist” approach allows Halma to serve demanding, high-margin segments that require custom, fast-acting fire protection systems rather than generic commodity sprinklers.

Enhanced Fire Protection Systems Market Report Scope

Enhanced Fire Protection Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$72.3 Billion

|

|

Market Size (2035)

|

$135.7 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By System Type (Active Fire Protection Systems, Passive Fire Protection Systems), By Product Function (Fire Detection Systems, Fire Suppression Systems, Fire Sprinkler Systems, Fire Analysis & Control Panels, Fire Response & Emergency Systems), By Vertical Application (Commercial Buildings, Industrial Facilities, Residential Buildings, Transportation Infrastructure), By Service Type (Installation & Replacement, Inspection & Maintenance, Managed Services)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Johnson Controls, Honeywell, Siemens, Bosch, Eaton, Carrier, Halma, Minimax, APi Group, Hochiki, Fike, Tyco Fire Protection, United Technologies (Carrier), NAFFCO, Reliable Automatic Sprinkler

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Global Enhanced Fire Protection Systems Market Segmentation

By System Type

- Active Fire Protection (AFP) Systems

- Passive Fire Protection (PFP) Systems

By Product Function

- Fire Detection Systems

- Fire Suppression Systems

- Fire Sprinkler Systems

- Fire Analysis & Control Panels

- Fire Response & Emergency Systems

By Vertical Application

- Commercial Buildings

- Industrial Facilities

- Residential Buildings

- Transportation Infrastructure

By Service Type

- Installation & Replacement

- Inspection & Maintenance

- Managed Services

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Enhanced Fire Protection Systems Market

- Johnson Controls

- Honeywell

- Siemens

- Bosch

- Eaton

- Carrier

- Halma

- Minimax

- APi Group

- Hochiki

- Fike

- Tyco Fire Protection

- United Technologies (Carrier)

- NAFFCO

- Reliable Automatic Sprinkler.

*- List not Exhaustive

Research Coverage

The latest USDAnalytics study on the Enhanced Fire Protection Systems Market delivers a rigorous, regulation-centric view of how NFPA- and ISO-driven upgrades, PFAS-free suppression agents, and AI-enabled detection are transforming global fire safety infrastructure. Drawing on quantitative and qualitative evidence, this report investigates the shift from conventional code-compliance toward high-availability, digitally connected fire protection architectures for commercial buildings, industrial facilities, high-rise residential, transport infrastructure, and special-hazard environments such as BESS and data centers. It tracks breakthroughs in high-pressure water mist, inert gas suppression, aerosol systems, fluorine-free foams, ultra-early warning detection (VESDA), and AI-powered video analytics, while our in-depth analysis reviews OEM strategies, regulatory inflection points, and technology adoption curves across key verticals. The report highlights the impact of digital twins, IoT-enabled monitoring, and predictive maintenance KPIs on lifecycle cost, uptime, and compliance, and benchmarks how leading suppliers integrate detection, suppression, and cloud platforms into end-to-end solutions. With granular coverage of system architectures, performance metrics, and regional regulatory trends up to 2035, this report is an essential resource for fire engineering consultants, EPCs, OEMs, investors, and asset owners seeking to future-proof critical facilities with sustainable, standards-compliant enhanced fire protection systems.

Scope Highlights

- Segmentation:

By System Type – Active Fire Protection (AFP) Systems; Passive Fire Protection (PFP) Systems

By Product Function – Fire Detection Systems; Fire Suppression Systems; Fire Sprinkler Systems; Fire Analysis & Control Panels; Fire Response & Emergency Systems

By Vertical Application – Commercial Buildings; Industrial Facilities; Residential Buildings; Transportation Infrastructure

By Service Type – Installation & Replacement; Inspection & Maintenance; Managed Services

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies: Analysis / profiles of 15+ companies across integrated building technology groups, fire safety specialists, and regional system providers.