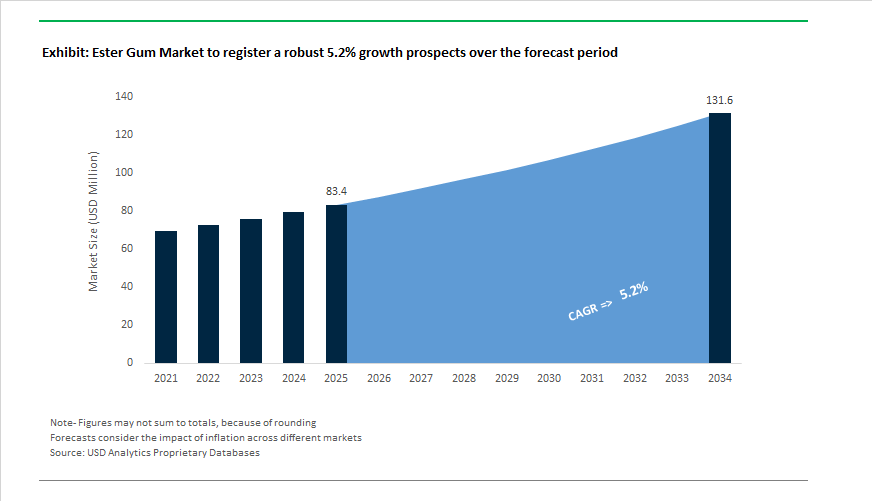

Ester Gum Market to Reach $131.6 Million by 2034 at 5.2% CAGR as Beverage Reformulation and Bio-Based Tackifiers Drive Structural Demand

The Ester Gum Market is projected to grow from $83.4 Million in 2025 to $131.6 Million by 2034, registering a CAGR of 5.2%. A defining catalyst for near-term demand emerged in July 2024, when the U.S. Food and Drug Administration finalized its rule revoking authorization for Brominated Vegetable Oil (BVO) in beverages. This regulatory action immediately accelerated substitution toward glycerol ester of wood rosin (E445) as the primary weighting and stabilizing agent in citrus-flavored carbonated drinks and sports beverages. Multinational beverage formulators initiated rapid reformulation cycles to ensure compliance before enforcement timelines, creating a sharp spike in procurement of high-purity, light-colored ester gums. In parallel, the U.S. International Trade Commission launched a Section 337 investigation in January 2026 concerning certain glycerol esters of rosin and related packaging, introducing trade and intellectual property scrutiny that may shift sourcing preferences toward domestically manufactured, traceable, and certified-grade ester gum suppliers.

Technology integration and portfolio upgrades are reshaping competitive positioning among leading producers. In April 2024, Cargill implemented AI-driven monitoring across its esterification lines, using predictive analytics to optimize temperature control, reaction kinetics, and color consistency—critical parameters for pharmaceutical and beverage applications requiring zero-defect specifications. Grupo RB strengthened its European footprint through the acquisition of Pinopine in March 2024, expanding access to forest-certified gum rosin feedstock and reinforcing supply stability for sustainable tackifier production. Earlier in February 2024, Pinova Inc. launched ultra-light-colored ester gums engineered to minimize organoleptic impact in clear beverages, addressing historical challenges of discoloration and off-odor associated with traditional rosin esters. Meanwhile, Arakawa Chemical Industries expanded pharmaceutical-grade capacity by 30% at its Singapore facility in June 2024, targeting controlled-release formulations and moisture-barrier coatings for tablets.

Sustainability credentials and high-performance industrial applications are broadening end-use penetration. DRT introduced environmentally certified ester gums in April 2024, produced via decarbonized processes and sustainable forestry inputs to support clean-label and ESG-driven procurement strategies. Eastman Chemical Company secured a patent in August 2024 for a thermally stable modified ester gum tailored for electronic adhesives, enabling adhesion retention during high-temperature PCB assembly. Supply-side expansion remains active in Asia; by late 2025, new esterification plants in China and Vietnam collectively added 15,000 metric tons of annual capacity, intensifying price competition in glycerol ester of gum rosin (GEGR) for adhesives and chewing gum markets. Foreverest Resources concurrently upgraded export logistics infrastructure to accelerate delivery into North America and Europe. These structural shifts—regulatory reformulation in beverages, AI-driven process optimization, pharma-grade specialization, and sustainability-certified production—are redefining growth trajectories across the global ester gum value chain.

Trends and Opportunities in the Ester Gum Market

Reformulation Momentum Toward Clean-Label and Non-GMO Ingredient Declarations

- Global food and beverage manufacturers are accelerating the replacement of synthetic emulsifiers with Glycerol Ester of Wood Rosin to comply with clean-label, non-GMO, and naturally derived ingredient positioning. Ester gum has become a preferred solution because it combines regulatory familiarity with proven functional performance in acidic and carbonated systems.

- During 2024–2025, Cargill integrated artificial intelligence into its ester gum manufacturing processes to improve control over esterification degree, solubility, and impurity removal. This investment supports the production of high-stability ester gums that meet beverage industry requirements for clarity, flavor protection, and consistent emulsification while satisfying increasingly strict natural ingredient declarations. From a formulation standpoint, ester gum is now embedded in mainstream beverage recipes. Industry assessments from late 2025 show that more than 55% of modern carbonated soft drink formulations use ester gum as a primary stabilizer to prevent flavor oil separation and surface ring formation.

- Consumer behavior is reinforcing this shift. Surveys conducted across North America and Europe in 2025 indicate that over 60% of shoppers actively favor products formulated with natural resins over synthetic alternatives. This preference translated into a measurable 4.6% increase in United States retail food and beverage service demand for bio-based additives by March 2025, strengthening ester gum’s position as a default clean-label emulsifier rather than a specialty substitute.

Rising Penetration in High-Performance Industrial Adhesives and Sealants

- Beyond food applications, ester gum is gaining strategic importance as a renewable tackifier in industrial adhesives and sealants. Glycerol rosin esters are increasingly replacing petroleum-derived hydrocarbon resins due to their favorable balance of adhesion, cohesion, and environmental compliance.

- By late 2024, adhesives accounted for roughly 45% of total polymerized ester gum consumption. Demand is closely linked to construction and automotive activity, where ester gum-based tackifiers are valued for strong bonding performance in flooring systems, roofing membranes, interior trims, and pressure-sensitive applications. The low VOC profile of ester gum aligns well with tightening indoor air quality and emissions standards, particularly in urban construction projects.

- Global construction output is projected to reach $15.5 trillion by 2030, and this expansion is directly supporting the uptake of bio-based adhesive systems. In 2025, Harima Chemicals Group introduced a new generation of rosin-based tackifiers engineered for low-temperature hot-melt adhesives. These products improved processing efficiency and bonding consistency, driving a reported 27% increase in demand from electronics packaging and footwear manufacturers across Asia. This trend underscores how ester gum is evolving from a commodity resin into a performance-tuned bio-material.

Stabilization Solutions for Plant-Based Dairy and Beverage Alternatives

- The rapid expansion of plant-based beverages and dairy analogues is creating a significant opportunity for ester gum as a natural stabilizer capable of managing complex fat and protein systems. In 2025, 61% of global consumers reported increasing their intake of plant-based products compared with two years earlier, sharply raising formulation challenges around phase separation, sedimentation, and visual stability.

- Ester gum functions as both a clouding agent and emulsifier in oat, almond, soy, and hemp-based beverages, offering a natural alternative to synthetic hydrocolloids. Its ability to maintain uniform dispersion directly addresses common quality issues in dairy alternatives. Mid-2025 research into oleogels used in plant-based ice creams further demonstrated the importance of ester-based structuring agents in stabilizing air incorporation and preserving mouthfeel in reduced-fat vegan formulations.

- Regulatory developments are reinforcing this opportunity. European Commission Regulation (EU) 2025/651, adopted in April 2025, expanded authorized uses of bio-based glazing agents and carriers. This regulatory flexibility supports broader application of ester gum within dairy and dairy analogue categories, including products intended for young children, where clean-label and safety perceptions are especially critical.

Specialty Ester Gum Grades for Vaping and Cannabinoid Liquid Formulations

- A high-margin niche is emerging for ultra-refined ester gum in vaping and cannabinoid liquid formulations, where stability, viscosity control, and ingredient purity are tightly regulated. Hydrophobic actives such as CBD, THC, and nicotine require stabilizers that prevent stratification while maintaining consistent aerosolization under repeated heating cycles.

- From July 1, 2025, regulators such as Australia’s Therapeutic Goods Administration began enforcing stricter safety and compositional standards for vaping products. These rules limit excipients to pharmaceutical-grade materials, creating a clear opening for high-purity ester gum as a compliant thickening and stabilizing agent. In parallel, the global cannabis vape segment is transitioning toward more reliable, temperature-controlled hardware, increasing demand for carrier systems that remain stable during prolonged thermal exposure.

- As CBD products continue their transition from niche wellness offerings to regulated therapeutic formats in 2025, manufacturers are prioritizing stabilizers that reinforce a natural and plant-derived brand narrative. Ester gum aligns strongly with this positioning, offering a bio-based alternative to synthetic glycol thickeners while delivering the viscosity and thermal stability required for next-generation inhalation products.

Ester Gum Market Share and Segmentation Insights

Glycerol Esters of Wood Rosin Lead Beverage and Food-Grade Ester Gum Consumption

Glycerol esters of wood rosin capture 38% of global ester gum market share in 2025, driven primarily by beverage applications where they stabilize flavor emulsions and provide consistent clouding in soft drinks and fruit juices. Their broad regulatory acceptance, reliable quality, and food-contact compliance position them as the industry standard for beverage formulation. Pentaerythritol ester gums hold a strong secondary share, valued for higher softening points and superior thermal stability in chewing gum bases, adhesives, and high-temperature applications. Glycerol esters of gum rosin remain important in traditional paints, coatings, and printing inks, particularly in regions with accessible gum rosin feedstocks. Modified ester gums are gaining momentum in premium inks and specialty coatings requiring enhanced hardness and gloss, while polymerized rosin esters serve niche adhesive markets demanding higher molecular weight and tailored rheology.

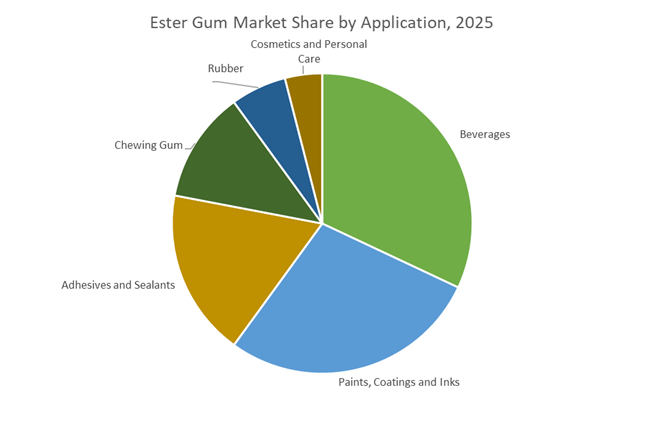

Beverages Drive Primary Demand Supported by Expanding Adhesives and Coatings Applications

Beverages account for 32% of ester gum consumption in 2025, reinforcing their role as the largest application segment. Ester gums function as essential emulsion stabilizers and clouding agents, preventing flavor oil separation and maintaining visual appeal throughout shelf life. Paints, coatings, and inks represent a major secondary market, utilizing ester gums as film formers, gloss enhancers, and adhesion promoters in alkyd systems and overprint varnishes. Adhesives and sealants follow closely, incorporating ester gums as tackifiers in hot-melt and pressure-sensitive formulations to improve initial tack and cohesive strength. Chewing gum maintains steady demand for food-grade ester gums within gum bases, while rubber compounding uses them as processing aids. Cosmetics and personal care constitute a fast-growing segment, leveraging ester gums as film formers in long-wear makeup for durability and water resistance.

Competitive Landscape of the Ester Gum Market

The global Ester Gum Market is defined by high-purity beverage stabilizers, solvent-free adhesive innovation, and traceable pine-chemistry supply chains, with leading producers competing on regulatory compliance, circular feedstocks, and specialty-grade performance for food, cosmetics, inks, and industrial adhesives.

Eastman Chemical sets global benchmarks in beverage-grade ester gums and regulatory compliance

Eastman Chemical Company remains the gold standard in high-purity ester gum production, dominating beverage weighting agents and specialty adhesive applications. Its Ester Gum 8D and 8BG grades are widely adopted to stabilize citrus oils in soft drinks, meeting strict FDA and EFSA requirements for glycerol esters of wood rosin. In late 2025, Eastman optimized its Kingsport, Tennessee facility to boost output of pale ester gums, supporting premium cosmetics and fragrance demand. The company’s core strength lies in regulatory leadership and molecular-level purification. Looking ahead, Eastman is advancing molecular recycling integration, exploring bio-based glycerol to develop a 100% renewable-content ester gum portfolio for circular beverage and packaging markets.

Arakawa Chemical advances low-odor ester gums for hot-melt and eco-friendly construction adhesives

Arakawa Chemical Industries Ltd. is a specialist in rosin-based chemistry, supplying high-performance ester gums to electronics, chewing gum base, and hot-melt adhesive manufacturers. Its ESTER GUM™ series is recognized for low acid numbers and high oxidative stability, making it ideal for solvent-free HMA systems. In early 2026, Arakawa launched a low-odor ester gum tailored for Japanese and European indoor construction, targeting sustainable flooring adhesives. The company also expanded Arakawa Chemical (USA) with a new technical support center to help North American customers reformulate VOC-free products. Arakawa’s precision purification and application-driven R&D underpin its strong position in premium adhesive resins and food-grade elastomer systems.

DRT-Givaudan integrates pine chemistry with flavor science for organoleptic-neutral ester gums

Following its acquisition by Givaudan, DRT Derives Resiniques et Terpeniques has become the most vertically integrated player in ester gum pine chemistry. Its DERTOLINE range supports pressure-sensitive adhesives and depilatory waxes, while close collaboration with Givaudan ensures zero taste or odor impact in beverage applications. In 2026, DRT fully aligned with Givaudan’s “Sourcing for Good” program, delivering 100% traceable crude tall oil and wood rosin. The company also commercialized enzymatically refined ester gums in 2025–2026, cutting refining carbon footprints by 20%. Global distribution and flavor R&D synergy give DRT a unique advantage in food-safe, cosmetic-grade ester gum solutions.

Pine Chemical Group dominates Asia’s industrial ester gum supply through scale and cost leadership

Pine Chemical Group is a high-volume powerhouse headquartered in the world’s largest rosin-producing region. By 2026, it accounts for roughly 15% of global industrial-grade ester gum supply, serving construction, paint, and ink markets across China and Southeast Asia. In late 2025, the group commissioned a fully automated distillation facility in Guangxi, adding 25,000 metric tons of annual glycerol ester of rosin capacity. Pine Chemical’s strategic focus is cost leadership, leveraging proximity to pine forests and deep gum rosin integration to hedge raw material volatility. This scale-driven model positions the company as a primary merchant supplier for bulk buyers seeking consistent quality at competitive pricing.

Respol customizes ester gum performance for European road marking and cosmetic wax markets

Respol S.A. is Europe’s leading pine-resin specialist, concentrating on high-performance industrial adhesives and road marking paints. Its RESITACK series uses ester gum to deliver superior thermal stability and tack in extreme climate applications. In early 2026, Respol introduced bio-polymer blends combining ester gum with plant-based resins to support upcoming EU bio-content mandates for coatings. The company is widely recognized for technical customization, tailoring softening points and viscosities to customer machinery requirements. Respol also dominates the European depilatory wax segment, where its cosmetic-grade ester gums are valued for skin-neutral pH and optical clarity, reinforcing its niche leadership in specialty resin engineering.

United States: Regulatory Certainty and High-Value Application Migration

The United States ester gum market in 2025–2026 is being shaped by regulatory affirmation combined with targeted innovation in food, beverage, and adhesive applications. In March 2025, the U.S. Food and Drug Administration reaffirmed the safety status of Glycerol Ester of Wood Rosin as a direct food additive. This decision has reinforced long-term confidence among beverage formulators using ester gum as a density-adjusting and cloud-stabilizing agent in citrus-flavored drinks and electrolyte-rich sports beverages. For manufacturers, this regulatory clarity reduces reformulation risk and supports multi-year supply contracts with brand owners focused on functional hydration products.

On the industrial side, innovation in adhesive chemistry is accelerating ester gum penetration into sustainable packaging systems. Kraton Corporation announced the rollout of next-generation rosin ester tackifiers in mid-2025, engineered for improved thermal stability and lighter color profiles. These characteristics are increasingly critical in high-speed hot-melt adhesive applications used in e-commerce packaging, where clean appearance and performance consistency are essential. At the same time, clean-label dynamics in beverages are reshaping procurement patterns. Major U.S. brands have increased sourcing of natural ester gum grades such as Pinova™ Ester Gum 8BG, replacing synthetic clouding agents in response to strong consumer preference for plant-derived ingredients. Supply-side resilience is also improving, as Eastman Chemical Company optimized domestic wood rosin distillation in 2025, stabilizing feedstock availability for pharmaceutical and cosmetic-grade ester gum.

India: Capacity Expansion Aligned with Beverage and Coatings Demand

India’s ester gum market is expanding through a combination of domestic capacity additions and policy-driven growth in food processing and coatings exports. In early 2025, Mahendra Rosin & Turpentine Pvt Ltd expanded its food-grade ester gum production capacity, directly addressing rising demand from India’s fast-growing non-alcoholic beverage segment. The scale-up reflects a strategic shift toward localized sourcing as beverage manufacturers seek consistent stabilizer quality amid rising volumes of fruit-based and carbonated drinks.

Government policy is reinforcing this trajectory. Increased budgetary allocations under the Pradhan Mantri Kisan SAMPADA Yojana for 2025–2026 have strengthened cold-chain and value-addition infrastructure, indirectly stimulating demand for stabilizers and emulsifiers such as ester gum in processed beverages. Beyond food applications, ester gum consumption is benefiting from export momentum in paints and coatings. Data from the Department for Promotion of Industry and Internal Trade indicates steady growth in exports of paints and allied products during 2025, particularly into Southeast Asian markets. As ester gum remains a key binder in certain coating formulations, export-oriented manufacturers are increasing long-term procurement to support volume scalability and performance consistency.

China: FMCG Scale and Bio-Based Specialty Positioning

China represents one of the most consumption-driven ester gum markets, supported by the scale of its food and beverage industry. With food and drink service revenues reaching CNY 5.3 trillion in the latest fiscal cycle, the use of Glycerol Esters of Gum Rosin has expanded rapidly in mass-market chewing gum and citrus-flavored soft drinks. Ester gum’s role as a stabilizing and texturizing agent aligns well with China’s high-throughput FMCG manufacturing model, where ingredient reliability at scale is critical.

Strategically, China is also repositioning ester gum as a bio-based specialty resin. Under the Ministry of Industry and Information Technology’s 2026 work plan emphasizing bio-based materials, producers such as Wuzhou Pine Chemicals have introduced refined, low-odor ester gum grades for international fragrance and cosmetics markets. Process modernization is supporting this shift. In 2025, manufacturers in the Guangdong chemical cluster integrated AI-driven distillation controls, achieving higher purity rosin esters while reducing material waste by double-digit percentages. This combination of volume consumption and specialty-grade upgrading positions China as both a demand center and a competitive exporter of ester gum.

Germany (European Union): Sustainability-Driven Reformulation and Coatings Demand

Germany’s ester gum market is being shaped by regulatory sustainability targets and steady growth in high-performance coatings. In alignment with the European Green Deal, German manufacturers have intensified R&D into solvent-free ester gum dispersions that comply with 2026 VOC reduction requirements. These developments are particularly relevant for architectural coatings and industrial varnishes, where ester gum contributes to film formation and adhesion while meeting stricter environmental thresholds.

Innovation in personal care is also expanding the application envelope. Synthomer introduced Ester Gum 8D Cosmetic Grade in 2025, targeting long-wear and waterproof cosmetic formulations that must meet stringent REACH safety standards. Demand fundamentals remain strong, as Germany’s paints and varnishes sector is forecast to generate revenues exceeding $1.29 billion by 2026. This outlook is directly supporting procurement of pentaerythritol ester gums for protective and decorative coatings, reinforcing Germany’s role as a high-value, regulation-driven market.

Japan: Electronics-Focused Innovation and Infrastructure-Led Consumption

Japan’s ester gum market is differentiated by its strong linkage to advanced manufacturing and infrastructure spending. In 2025, Arakawa Chemical Industries launched high-heat-resistant rosin ester grades designed for electronics applications. These materials are used as tackifiers in lead-free solder pastes and high-density circuit board adhesives, where thermal stability and clean processing are essential for miniaturized electronics.

Construction activity is providing an additional demand pillar. According to the Ministry of Land, Infrastructure, Transport, and Tourism, construction investment reached JPY 68.8 trillion, stimulating the use of ester gum-based binders in road marking paints and durable floor coatings. These applications value ester gum for its adhesion performance and resistance to environmental stress, supporting steady consumption in public infrastructure projects.

Ester Gum Market: Country-Level Strategic Summary

Ester Gum Market County Level Snapshot

|

Country

|

Primary Demand Drivers

|

Key Applications

|

Strategic Direction

|

|

United States

|

Regulatory affirmation, clean-label shift

|

Beverages, hot-melt adhesives

|

Natural ingredient substitution

|

|

India

|

Capacity expansion, food processing policy

|

Soft drinks, paints & coatings

|

Import substitution and exports

|

|

China

|

FMCG scale, bio-based roadmap

|

Chewing gum, soft drinks, cosmetics

|

Volume plus specialty upgrading

|

|

Germany

|

VOC mandates, coatings growth

|

Architectural coatings, cosmetics

|

Sustainability-led reformulation

|

|

Japan

|

Electronics R&D, infrastructure spend

|

Solder pastes, road markings

|

High-performance niche applications

|

Ester Gum Market Report Scope

Ester Gum Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$83.4 Million

|

|

Market Size (2034)

|

$131.6 Million

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Product Type (Glycerol Esters of Wood Rosin, Glycerol Esters of Gum Rosin, Polymerized Rosin Esters, Pentaerythritol Ester Gums, Modified Ester Gums), By Grade (Food Grade, Industrial Grade, Cosmetic Grade), By Application (Beverages, Chewing Gum, Paints, Coatings and Inks, Adhesives and Sealants, Cosmetics and Personal Care, Rubber)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Eastman Chemical Company, Kraton Corporation, Arakawa Chemical Industries, Ltd., DRT, BASF SE, Lawter Inc., Mahendra Rosin & Turpentine Pvt. Ltd., Wuzhou Pine Chemicals, Pinova Holdings, Sakata InX Corporation, Guangdong KOMO Co., Ltd., Foreverest Resources Ltd., Respol, Florachem Corporation, Polimeros Sinteticos

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ester Gum Market Segmentation

By Product Type

- Glycerol Esters of Wood Rosin

- Glycerol Esters of Gum Rosin

- Polymerized Rosin Esters

- Pentaerythritol Ester Gums

- Modified Ester Gums

By Grade

- Food Grade

- Industrial Grade

- Cosmetic Grade

By Application

- Beverages

- Chewing Gum

- Paints, Coatings and Inks

- Adhesives and Sealants

- Cosmetics and Personal Care

- Rubber

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ester Gum Industry

- Eastman Chemical Company

- Kraton Corporation

- Arakawa Chemical Industries, Ltd.

- DRT

- BASF SE

- Lawter Inc.

- Mahendra Rosin & Turpentine Pvt. Ltd.

- Wuzhou Pine Chemicals

- Pinova Holdings

- Sakata InX Corporation

- Guangdong KOMO Co., Ltd.

- Foreverest Resources Ltd.

- Respol

- Florachem Corporation

- Polimeros Sinteticos

*- List not Exhaustive