Market Overview: Growing Demand for Sustainable and Smart Food Wrap Solutions

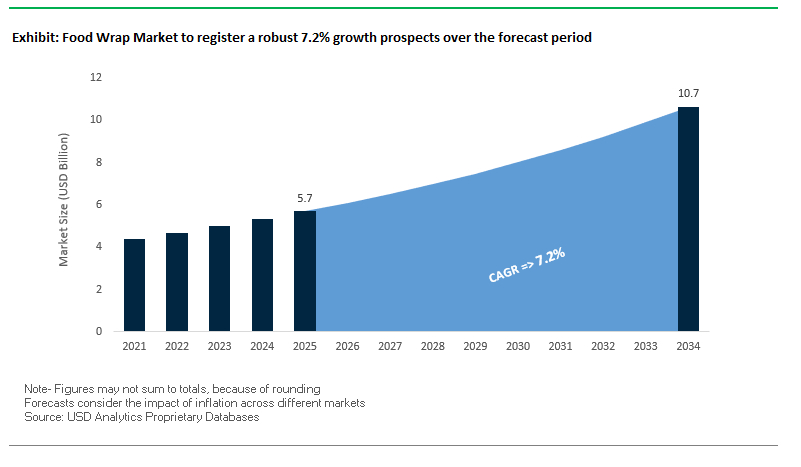

The Global Food Wrap Market is forecasted to grow from USD 5.7 billion in 2025 to USD 10.7 billion by 2034, at a steady CAGR of 7.2%. Food wraps—including plastic cling films, aluminum foils, and paper wraps—are critical to the global food supply chain, ensuring freshness, extended shelf life, and protection from contamination. Their widespread use spans food, pharmaceuticals, and consumer goods industries, where convenience, hygiene, and sustainability are primary concerns.

The industry is increasingly influenced by sustainability mandates, with manufacturers investing in biodegradable, compostable, and post-consumer recycled (PCR) materials. Additionally, the adoption of smart packaging technologies—such as time-temperature indicators (TTIs) and embedded freshness sensors—is helping reduce food waste by providing real-time insights to consumers.

Advanced barrier properties in nano-engineered films and metalized laminates are extending the shelf life of perishables by protecting against oxygen, light, and moisture. At the same time, automation and robotics integration in the packaging process is driving operational efficiency, with AI-powered robotics improving precision in sealing, wrapping, and packing tasks.

Key Insights for professionals and Buyers:

- Market to reach USD 10.7B by 2034, expanding at 7.2% CAGR.

- Biodegradable and compostable wraps gaining traction in line with global sustainability goals.

- Smart packaging features like QR codes and TTIs support transparency and freshness tracking.

- Barrier-enhanced films and foils enable longer product shelf life.

- Automation and robotics streamline high-volume packaging operations.

Market Analysis: Recent Developments in the Global Food Wrap Industry

The Food Wrap Market is undergoing a wave of transformation with companies driving sustainability programs, M&A activity, and technological innovations to meet rising consumer and regulatory expectations.

In September 2025, the Flexible Plastic Fund (FPF) launched its FlexCollect report in the UK, showing an 89% satisfaction rate in recycling initiatives for flexible packaging, including cling films. In August 2025, ProAmpac announced plans to acquire PAC Worldwide, strengthening its role in protective packaging and e-commerce wraps. That same month, Amcor completed an upgrade at its Heanor, UK recycling plant, adding 2,800 tonnes of recyclate capacity to improve closed-loop flexible film production.

Industry consolidation gained momentum in July 2025, when Amcor and Berry Global Group finalized their all-stock merger, creating a packaging powerhouse with an expanded food wrap portfolio. Also in July 2025, Smurfit Kappa and WestRock completed their merger, strengthening paper-based alternatives to plastic wraps.

Earlier, in June 2025, consumer-driven reports highlighted the surge in demand for recyclable and compostable wraps, while in April 2025, innovation was spotlighted with growing use of QR codes, NFC, and RFID-enabled films for food traceability. By January 2025, new studies pointed to the shift toward sugarcane-based wraps, driven by plastic regulations and consumer preference for bio-based materials.

Key Trends and Emerging Opportunities Driving the Food Wrap Market

Regulatory-Driven Phase-Out of PVC and PVDC Cling Films

The food wrap market is experiencing a rapid shift due to regulatory pressure to eliminate PVC and PVDC cling films. Governments globally are banning these chlorine-based films because of health concerns, potential plasticizer migration, and dioxin generation when incinerated. This has accelerated the adoption of polyethylene (PE)-based alternatives and other innovative materials that match the cling, stretch, and barrier performance of traditional films without environmental or safety risks. Scientific studies highlight migration levels of DEHA (di-(2-ethylhexyl) adipate) in cheeses exceeding the EU's safety limits, reinforcing the regulatory rationale. Governments are issuing concrete timelines for phase-outs, such as British Columbia’s 2028 restriction and New Zealand’s ban on PVC trays since 2022, providing a clear market roadmap. Industry leaders are responding proactively; the Saran wrap brand has transitioned to LDPE, showcasing a commitment to safer, regulatory-compliant materials. This trend creates a high-value growth avenue for PE-based and other non-chlorinated wraps, particularly for applications in meat, cheese, and produce.

Commercialization of High-Performance Bio-Based and Compostable Wraps

Beyond PE substitution, there is a growing push toward bio-based and compostable wraps, made from PLA, PHA, or other biopolymers, which offer functional advantages such as breathability for produce and home-compostable end-of-life options. Consumer and corporate demand for circular packaging drives this trend, as traditional bio-polymers often faced limitations in mechanical strength, clarity, and barrier properties. Companies are innovating to overcome these issues; for instance, Compostic offers 100% home-compostable cling wrap from certified bio-based blends. Academic R&D continues to strengthen these materials through formulation improvements and optimized processing techniques. The ability to offer functional, certified, sustainable wraps presents a major growth opportunity, with corporations like Google and Valmet adopting plastic-free alternatives, signaling robust demand across industries.

Development of Reusable Silicone and Hybrid Food Wrap Systems

The reusable food wrap segment is emerging as a high-value opportunity. Innovations in food-grade silicone and hybrid systems—such as a silicone sheath with a replaceable compostable liner—combine reusability with convenience and hygiene. Consumer demand for durable, reusable solutions is increasing, exemplified by Vytal Global’s $15.5 million funding to expand US operations. Market leaders like Bee's Wrap and W&P are offering beeswax-based and silicone stretch wraps, respectively, positioning themselves as alternatives to single-use plastics. The commercialization of these systems represents a $10 billion potential opportunity, as estimated by UNEP, and fosters new business models, including pay-per-use systems and enhanced logistics for reusable packaging. This opportunity reshapes the value chain toward a circular economy, integrating cleaning, distribution, and reuse workflows.

Integration of Active and Intelligent Properties into Wraps

There is a significant opportunity to move beyond passive barrier protection toward active and intelligent food wraps. These wraps can absorb ethylene to slow ripening, indicate spoilage via pH-sensitive dyes, or incorporate antimicrobial agents, directly addressing household food waste reduction. The global need to mitigate food waste is a core driver, with technologies such as time-temperature indicators (TTIs) providing real-time assurance of freshness. Companies like GreenPod Labs and StenCo are developing plant-extract-based active packaging and oxygen-scavenging biodegradable films, respectively. Offering high-tech, performance-enhancing wraps creates a high-value market service by extending shelf life, reducing waste, and delivering measurable economic benefits to brands and retailers. This opportunity is fostering collaboration across food wrap manufacturers, technology developers, and food scientists, establishing a more innovative and value-driven supply chain.

Competitive Landscape: Leading Companies Shaping the Food Wrap Market

The competitive landscape is characterized by global leaders and regional specialists focusing on innovation, recyclability, and consumer convenience.

Amcor plc strengthens position with Berry Global merger

Amcor is a leader in responsible food packaging, offering barrier films, recyclable foils, and AmLite® Recyclable wraps. In August 2025, it expanded its healthcare network in Costa Rica and upgraded recycling in the UK. By July 2025, Amcor completed its merger with Berry Global, broadening its food wrap portfolio. Its AmPrima® solutions enable high-barrier laminates with recyclability, supporting its 2025 goal of fully recyclable packaging.

Reynolds Consumer Products maintains U.S. dominance with Reynolds Wrap®

Reynolds enjoys high U.S. household penetration with Reynolds Wrap® aluminum foil and Hefty® food storage bags. In Q2 2025, it recorded 6% retail volume growth in its storage segment, supported by innovative launches. The company reduced debt by USD 150 million in 2024, strengthening financial stability. Its portfolio spans foil, cling film, parchment paper, and storage bags, underpinned by a U.S.-centric strategy focusing on innovation and brand equity.

Berry Global Group expands sustainable film portfolio

Berry Global, now merged with Amcor (July 2025), remains a leader in sustainable food wrap films. Its offerings include compostable and PCR-based wraps, alongside circular polymer investments. Its advanced blown and cast film processes deliver durability and recyclability. With the merger, Berry aims to accelerate its transition toward consumer-focused, growth-oriented packaging while expanding global reach.

SC Johnson enhances innovation with Ziploc® and Saran™ Wrap

SC Johnson holds strong consumer recognition through Ziploc® bags and Saran™ Wrap. Its food wrap materials use LDPE and polybutylene cling agents, approved for direct food contact. Recent innovations include resealable bags with expandable bottoms and easy-open features, designed for convenience and safety. The company continues to focus on branded product innovation, maintaining its leadership in household food storage solutions.

Inteplast Group expands production capacity in North America

Inteplast Group is a leading U.S. producer of PVC and antimicrobial food wraps under its Select Series®. In late 2022, it expanded capacity at its Remington, Indiana plant, adding new extrusion lines for stretch and cling films. Its antimicrobial wraps are designed to minimize bacterial growth, addressing hygiene concerns in food storage and service. With strong vertical integration, Inteplast provides both plastic and paper-based wraps for foodservice, grocery, and industrial applications.

Food Wrap Market Share Insights

Household Segment Leads Market Share by Application in Food Wrap Industry

The household segment dominates the food wrap market with 45% projected share in 2025, reflecting its position as a staple product in everyday consumer lifestyles. Food wrap is indispensable for food storage, leftovers, and preparation, and its recurring purchase cycle ensures steady high-volume demand across global households. Growth in this segment is further fueled by brand loyalty, affordability, and rising awareness of food waste reduction, which has positioned wraps as an essential tool for extending shelf life at home. The food service industry follows as an operationally critical user, relying on bulk wraps for storage, portioning, and prep work in restaurants and catering establishments. The fastest-growing demand is coming from online food delivery platforms, where wraps are essential for ensuring meal integrity, spill protection, and temperature retention during last-mile delivery. Institutional and commercial users—such as schools, hospitals, and corporate cafeterias—sustain steady demand through bulk procurement, prioritizing cost-effectiveness and compliance with safety protocols. Collectively, this segmentation highlights how household adoption anchors scale while food service and delivery applications fuel innovation in durability and performance.

Food and Beverages Dominate Market Share by End-Use Industry in Food Wrap Industry

The food and beverages industry accounts for over 95% of total food wrap demand, making it the undisputed backbone of the market. Food wrap’s intrinsic role in preserving freshness, preventing contamination, and extending shelf life ties its consumption almost exclusively to food applications, from direct household use to industrial-scale food processing and secondary packaging. Beyond this overwhelming dominance, other end-use industries remain niche, representing specialized, non-food-contact applications. In pharmaceuticals and healthcare, wraps are used sparingly for bundling non-sterile components or providing a secondary protective layer for medical kits. In cosmetics and personal care, they play a role in gift bundling and presentation packaging, while in industrial goods, their use is limited to temporary corrosion protection or bundling small components. These marginal shares underscore that while alternative industries create small specialized outlets, the food and beverages sector will continue to anchor near-total demand for food wraps worldwide.

United States Food Wrap Market Strengthened by FDA Guidelines and Sustainable Packaging Innovations

The U.S. food wrap market operates under a fragmented regulatory environment, with the FDA providing guidance on food contact materials to ensure safety under the GRAS (Generally Recognized as Safe) framework. Recent post-market surveillance initiatives and varying state-level regulations are creating additional compliance complexities for manufacturers. Technological advancements are reshaping the industry, with companies like Amcor introducing recyclable high-barrier laminated papers, and active packaging materials equipped with temperature-sensitive sensors to enhance food shelf life.

Corporate investments are fueling growth, highlighted by Amcor’s planned acquisition of Berry Global Group, consolidating resources to create a company with $180 million in annual R&D investments in sustainable packaging. Key applications include food and beverage, e-commerce, and direct-to-consumer segments, driven by the surge in online food delivery and the need for robust, lightweight, and efficient wraps. Sustainability remains a core focus, with eco-friendly bio-based films and recyclable paperboard meeting rising consumer demand for environmentally responsible packaging solutions.

Germany Food Wrap Market Pioneers Circular Economy and Sustainable Packaging Compliance

Germany’s food wrap industry is strongly influenced by the EU Packaging and Packaging Waste Regulation (PPWR), which mandates fully recyclable or reusable packaging by 2030, with strict guidelines on recycled content and elimination of hazardous chemicals like PFAS. Germany’s Packaging Act (VerpackG) further drives innovation in recycling and reusable containers, incentivizing designs that are easier to recycle and support circular economy principles.

Technological innovation is a key growth driver, with companies like Syntegon developing vertical packaging machines capable of processing paper-based and mono-material films, advancing sustainable food wrapping solutions. The market thrives in food, beverage, and personal care sectors, fueled by consumer preference for premium, high-barrier packaging that extends shelf life and enhances product quality. Germany’s regulatory leadership and commitment to sustainable materials make it a benchmark for advanced food wrap solutions in Europe.

China Food Wrap Market Expands with Dual Carbon Goals and Advanced Manufacturing

China’s food wrap market is experiencing strong growth due to governmental initiatives, including the “dual carbon” goal, which promotes sustainable manufacturing and circular materials. The government’s March 2024 Action Plan and the revised GB/T 31268 standard, which limits excessive packaging, are reshaping industry practices, particularly for e-commerce and food delivery applications.

Technological advancements such as AI, automation, and “5G plus industrial internet” integration are enhancing production efficiency and capacity flexibility. Domestic manufacturing is prioritized, with local companies expanding capabilities to replace imported technology and meet growing demand for high-quality, circular packaging. The rapid growth of online grocery and food delivery sectors is a significant driver, establishing China as a key market for modern and sustainable food wrap solutions.

India Food Wrap Market Driven by Circular Economy Policies and Rapid Food Sector Growth

India’s food wrap market is benefiting from government initiatives promoting a circular economy, including the Food Safety and Standards (Packaging) Regulations, 2018, which ensure safe use of food-grade materials and prohibit recycled plastics for food contact. Technological adoption, particularly automated systems for flow wrap packaging, is increasing in sectors like frozen foods, snacks, and vegetables.

Corporate investments, supported by the Make in India initiative, are driving the establishment of new production facilities to meet domestic demand. Expanding food and beverage and personal care sectors, alongside the rapid growth of e-commerce, are key growth drivers. According to industry projections, India’s food processing sector is expected to reach $535 billion by FY26, directly influencing demand for modern, high-performance food wraps.

Japan Food Wrap Market Focuses on Sustainable High-Performance Films

Japan’s food wrap industry leverages advanced precision manufacturing and sustainable technologies. In September 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., successfully developed recycled BOPP film ready for mass production. Regulatory support from the Plastic Resource Circulation Act encourages environmentally-conscious material use, driving adoption of sustainable food wrap solutions.

The market is shifting toward high-performance, specialty films with superior barrier properties and integrated IoT sensors for real-time tracking. Innovation is focused on functionality enhancements such as easy-open tear notches and resealable closures, catering to an aging population and single-person households. These strategies position Japan as a leader in sustainable and technologically advanced food wrapping solutions in the Asia-Pacific region.

Brazil Food Wrap Market Accelerates with Sustainable Innovation and Digital Packaging Solutions

Brazil’s food wrap market is increasingly shaped by sustainable waste management policies, including amendments to the National Solid Waste Policy in January 2025, which promote domestic recycling and circular economy initiatives. Technological innovation is a significant growth driver, with robotics and AI enhancing production efficiency, quality control, and defect detection.

Premium and specialized digital packaging solutions are gaining traction, offering extended shelf life while maintaining product freshness. Sustainability initiatives, exemplified by Klabin’s EkoFlex flexible packaging paper, highlight the shift toward eco-friendly materials for various food applications. These trends demonstrate Brazil’s commitment to sustainable and innovative food wrap solutions, catering to both domestic and export markets.

Food Wrap Market Report Scope

Food Wrap Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.7 Billion

|

|

Market Size (2034)

|

$10.7 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Material Type (Plastic Films, Aluminum Foil, Paper & Waxed Paper, Plant-Based/Bio-Based Films), By Application (Food Service, Online Food Delivery, Institutional/Commercial, Household), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Reynolds Consumer Products Inc., Berry Global Group, Inc., Sonoco Products Company, Sealed Air Corporation, ProAmpac, UFlex Ltd., Constantia Flexibles Group, Pactiv Evergreen Inc., Mitsubishi Chemical Group Corporation, Veritiv Corporation, Novolex Holdings, LLC, Ahlstrom-Munksjö Oyj

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Wrap Market Segmentation

By Material Type

- Plastic Films

- Aluminum Foil

- Paper & Waxed Paper

- Plant-Based/Bio-Based Films

By Application

- Food Service

- Online Food Delivery

- Institutional/Commercial

- Household

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Wrap Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Reynolds Consumer Products Inc.

- Berry Global Group, Inc.

- Sonoco Products Company

- Sealed Air Corporation

- ProAmpac

- UFlex Ltd.

- Constantia Flexibles Group

- Pactiv Evergreen Inc.

- Mitsubishi Chemical Group Corporation

- Veritiv Corporation

- Novolex Holdings, LLC

- Ahlstrom-Munksjö Oyj

* List Not Exhaustive

Methodology

USDAnalytics conducted a rigorous and integrated research methodology to deliver a comprehensive analysis of the Global Food Wrap Market. Our approach combined extensive primary research through interviews with packaging manufacturers, food processors, regulatory authorities, and industry stakeholders with secondary research using company reports, trade publications, patent filings, and government regulations. Market sizing and forecasts were calculated across material types (plastic films, aluminum foil, paper & waxed paper, plant-based/bio-based films), applications (food service, online food delivery, institutional/commercial, household), and end-use industries (food & beverages, pharmaceuticals, cosmetics, industrial goods). Key trends, including sustainable bio-based wraps, reusable silicone systems, smart packaging with embedded freshness sensors, and automation in high-volume production, were analyzed alongside regulatory influences such as PVC/PVDC phase-outs, EU PPWR, FDA guidelines, and India’s Food Safety Packaging Regulations. Competitive intelligence highlighted strategic moves by leaders like Amcor, Berry Global, SC Johnson, and Reynolds, focusing on mergers, technological innovation, and sustainable portfolio expansion. Regional dynamics spanning the U.S., Germany, China, India, Japan, and Brazil were examined for policy impact, technological adoption, and circular economy initiatives, providing actionable insights for industry professionals and investors seeking growth opportunities and compliance strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.