Cling Wrap Market Overview: Polyethylene Dominance and Bio-Based Innovation

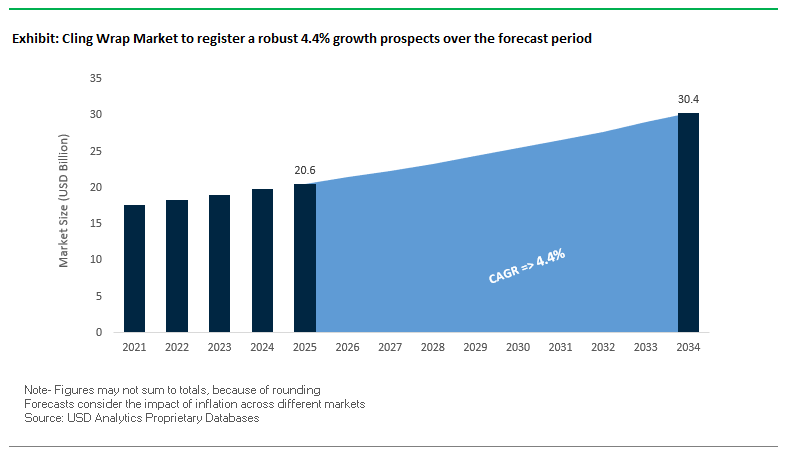

Market Value (MV): $20.6 Billion in 2025 → $30.4 Billion by 2034 | CAGR (2025–2034): 4.4%

The global cling wrap market is entering a transformative growth phase as polyethylene (PE) films replace legacy PVC wraps and bio-based alternatives gain traction amid stricter regulations on plastic waste. Polyethylene’s moisture barrier strength, clarity, and recyclability make it the preferred choice for food-grade wraps, while new compostable films derived from corn starch and sugarcane are appealing to sustainability-conscious consumers. Regulatory bodies such as the FDA and EFSA are enforcing stricter food-contact rules, eliminating harmful additives like BPA and certain phthalates from compliant cling films.

Importantly, the market is diversifying beyond kitchens. Cling films are now being engineered for medical applications, industrial wrapping with ESD protection, and personal care treatments, broadening end-user demand. The next decade will witness innovation in lightweight, recyclable, and bio-based structures that align with the circular economy.

Key Insights for buyers and industry leaders:

- Polyethylene cling wrap dominates due to recyclability and barrier performance.

- Bio-based wraps certified compostable are entering retail, driven by sustainability regulations.

- Food-grade compliance ensures BPA- and phthalate-free formulations for safety.

- Non-food uses expanding into healthcare, industrial, and personal care sectors.

Market Analysis: Sustainability, Legal Precedents, and Material Shifts Reshape Cling Wrap Demand

The industry has seen a surge of sustainability-driven innovation and legal precedents shaping packaging design. In November 2024, Berry Global launched Omni Xtra+, a recyclable polyethylene cling film that reduces weight by 25% while improving elasticity and clarity a major milestone in moving away from PVC-based alternatives. Similarly, May 2025 PMMI data revealed a projected decline in rigid plastics and glass, with a shift toward paper-based and flexible packaging, reinforcing the market’s pivot to sustainable formats.

Regulatory and legal rulings are also playing a crucial role. In July 2025, a UK Court of Appeal ruled that Aldi’s Taurus cider packaging infringed on Thatchers’ design, setting a precedent for distinctive and defensible packaging strategies. While not directly on cling wrap, the ruling underlines the rising importance of IP protection in flexible packaging markets. Sustainability advances continue to cross-pollinate sectors: in July 2025, Amcor unveiled its Hector CRC closure with up to 100% PCR plastic, signaling how rigid and flexible packaging are converging on sustainability goals.

On the capacity expansion side, January 2025 TekniPlex Healthcare’s investment in multilayer blown film within an ISO cleanroom highlights the demand for high-barrier films in medical and pharmaceutical applications, a trend indirectly bolstering cling film technology. Similarly, consolidation activities like October 2023 Thomas Scientific’s acquisition of Quintana Associates are strengthening portfolios in specialty films and bags, building competitive muscle across adjacent markets. Overall, the cling wrap industry is evolving into a regulated, innovation-driven ecosystem, where sustainability, IP defensibility, and material science advancements dictate growth.

Emerging Trends and Strategic Opportunities Shaping the Cling Wrap Market

Strategic Pivot Towards Post-Consumer Recycled (PCR) Content in Industrial Formats

The cling wrap market is witnessing a major shift towards integrating high percentages of PCR polyethylene, especially in industrial and commercial applications. This movement is driven by Extended Producer Responsibility (EPR) regulations and corporate sustainability mandates, compelling resin producers and converters to adopt recycled content without compromising performance. Industrial cling wraps, particularly in logistics, agriculture, and foodservice, are adopting 30% PCR-based films while maintaining critical attributes like puncture resistance and tensile strength. Companies such as Grounded Packaging and Thong Guan Industries are leading this transition, aligning their product lines with corporate ESG targets. This trend offers a significant growth avenue, as industrial-scale adoption creates high-volume demand, fostering innovation in recycling technologies and sustainable polymer sourcing.

Material Science Innovation in Home-Compostable Bio-Polymers

Beyond recycling, home-compostable cling wrap solutions are gaining traction. Driven by increasing consumer demand for circular packaging, material scientists are developing bio-based polymers that match LDPE in clarity, stretch, and barrier properties. Innovations like BASF’s ecovio®, a blend of ecoflex® and polylactic acid (PLA), provide industrial compostability while maintaining product performance. Academic studies emphasize challenges such as moisture and oxygen resistance, critical for food preservation. While currently a niche segment, the home-compostable cling wrap market represents a high-growth opportunity, particularly as production costs decline and mainstream consumers prioritize sustainable and convenient alternatives.

Development of High-Barrier, Extendable Shelf-Life Films for E-Commerce Grocery

The surge in online grocery delivery has created demand for cling wraps with active packaging properties to extend product freshness during last-mile logistics. High-barrier films capable of scavenging oxygen or ethylene are being developed to reduce spoilage in produce, meat, and perishables. Studies highlight that these films withstand temperature fluctuations and multiple handling points, making them ideal for e-commerce supply chains. This innovation enables the creation of premium cling wrap products marketed for their ability to extend shelf life, creating a value-added proposition for retailers and consumers alike. The integration of these films necessitates collaboration across manufacturers, e-commerce platforms, and grocery retailers, as well as advanced quality control to ensure consistent performance.

Integration of Antimicrobial Properties for Food Safety in Commercial Settings

Post-pandemic hygiene concerns have accelerated the need for cling wraps with non-migratory antimicrobial properties. Designed to inhibit microbial growth on the film’s surface, these wraps reduce cross-contamination risks in restaurant kitchens, catering services, and supermarket delicatessens. Research highlights the use of embedded silver nanoparticles or essential oils that remain surface-active without migrating into food, ensuring both efficacy and regulatory compliance. This segment offers a high-value growth opportunity, providing premium, food-safe packaging solutions. Adoption of antimicrobial cling wrap requires collaboration between material scientists, packaging manufacturers, and commercial food service providers, along with certification processes to validate effectiveness a potential key differentiator in the market.

Competitive Landscape: Global Leaders Expand Sustainable and High-Performance Cling Film Portfolios

The cling wrap industry is moderately consolidated, with global leaders competing on sustainability, material innovation, and regulatory compliance. Each company is building differentiation through bio-based innovations, lightweight films, and expanded application areas.

Reynolds Consumer Products Inc. focuses on household leadership

Reynolds remains a household name through its Reynolds Wrap and Handi-Wrap lines. Its strength lies in brand equity and wide distribution, ensuring top-of-mind recall in North America. The company continues to invest in sustainable materials and lightweighting strategies, aligning with consumer-driven innovation that emphasizes safety and recyclability.

Berry Global drives recyclable PE film innovation

Berry Global has been a frontrunner in sustainable alternatives. In November 2024, it introduced Omni Xtra+, a recyclable PE cling film with 25% reduced weight, improved elasticity, and superior clarity. This innovation positions Berry as a pioneer in replacing PVC films while pushing for a circular economy across industrial and household applications.

Amcor PLC integrates circularity into its flexible packaging portfolio

Amcor is leveraging its global scale to integrate sustainable materials into both rigid and flexible formats. Its July 2025 Hector CRC launch, though closure-focused, underscores its role in driving PCR integration and sustainability across packaging solutions. For cling films, Amcor’s deep expertise in recyclability, reuse, and compliance makes it a preferred partner for global food and healthcare clients.

Sealed Air Corporation strengthens Cryovac high-barrier solutions

Through its Cryovac brand, Sealed Air provides multi-layer, high-barrier films widely adopted in food and medical applications. With 2024 initiatives to reduce plastic use in PET bottles by 25%, the company demonstrates its ongoing sustainability and lightweighting agenda. Sealed Air’s R&D strength and global reach give it a competitive edge in high-performance cling wrap applications.

Sigma Plastics Group Inc. leverages scale in film production

As one of North America’s largest private film manufacturers, Sigma Plastics supplies a wide range of cling films, stretch films, and liners. Its strategic focus on lightweighting and recycled content aligns with global sustainability trends. Sigma’s deep expertise in film production and broad product portfolio strengthen its market share in both household and industrial cling film categories.

Cling Wrap Market Share Insights

Commercial Applications Dominate Market Share in the Cling Wrap Industry

The commercial segment accounts for 65% of the cling wrap market, highlighting its indispensable role in food service, retail, and hospitality. Restaurants, catering businesses, and supermarkets are the heaviest users, where the priority is speed, hygiene, and food preservation at scale. In these environments, cling wrap is valued for its low unit cost, stretchability, and ability to reduce food waste factors that often outweigh sustainability concerns. Bulk purchasing and high turnover in commercial kitchens secure this segment’s dominance, while innovation in biodegradable and compostable alternatives is only beginning to penetrate this space. By contrast, the household segment is increasingly pressured by substitution from reusable silicone lids, beeswax wraps, and containers, which limits its growth prospects. Mature markets like North America and Europe are seeing declining household adoption, further consolidating commercial applications as the engine of demand for cling wrap.

Food & Beverages Secure the Largest Market Share by End-Use Industry in the Cling Wrap Market

With 75% of overall demand, the food and beverages sector is the absolute anchor of the cling wrap industry. From crop protection post-harvest to food processing, retail packaging, and restaurant service, cling film is integrated at every stage of the food supply chain. Its ability to extend shelf life by preventing moisture loss and contamination makes it critical for perishable goods such as meat, dairy, and fresh produce. However, this segment faces mounting regulatory and consumer scrutiny over single-use plastics, forcing the industry to experiment with bio-based PE films, compostable wraps, and recyclable mono-material solutions. Despite these challenges, the sheer volume of food packaging needs ensures that F&B continues to dominate market share, while other industries industrial logistics, pharmaceuticals, and cosmetics remain niche users with limited overall impact on global demand.

United States Cling Wrap Market Driven by Sustainability Regulations and Advanced Bio-Based Materials

The U.S. cling wrap market is experiencing increasing regulatory pressure from the Environmental Protection Agency (EPA) following the release of the "National Strategy to Prevent Plastic Pollution" in November 2024. This policy emphasizes source reduction and alternative materials, compelling manufacturers to innovate environmentally friendly cling wrap solutions. Corporate investments are focused on lightweight, recyclable, and compostable materials, with production lines being upgraded for bio-based polymers such as polylactic acid (PLA) derived from cornstarch and sugarcane.

Technological advancements are pushing the development of functional and sustainable films, including water-based silk fibroin coatings and hybrid films made from chitin and cellulose, offering superior oxygen barrier properties compared to PET. Key applications are concentrated in food service, retail, and household sectors, amplified by the rise of meal kit delivery services and heightened post-pandemic hygiene awareness. Extended Producer Responsibility (EPR) initiatives in Washington and Maryland are shifting packaging waste responsibility to producers, encouraging recyclable and compostable cling wrap. Companies are also innovating with antimicrobial and smart packaging solutions to extend shelf life and enhance food safety.

Germany Cling Wrap Market Shaped by Circular Economy Regulations and Compostable Innovations

Germany’s cling wrap market operates under stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, mandating fully recyclable or reusable packaging with set targets for recycled content. The Packaging Act (VerpackG) reinforces producer responsibility for the lifecycle of packaging, prompting design and material innovations to enhance recyclability. Technological advancements include machinery capable of handling sustainable polymers and in-house production on modern extrusion, printing, and converting equipment, ensuring quality and traceability.

The food service and household sectors dominate demand, with growing interest in sustainable cling wrap for commercial and residential use. Investments in R&D focus on lighter, stronger, and eco-friendly films, including home and industrial compostable options, supported by digital product passports and material watermarks to improve transparency. Full traceability from raw material to finished product, offering up to 10 years of data, positions Germany as a leader in quality-driven and environmentally responsible cling wrap production.

China Cling Wrap Market Expands Through Regulatory Reforms and Domestic Innovation

China’s cling wrap market is driven by the government’s “dual carbon” goal and green industrial transformation under the 14th Five-Year Plan. Regulatory initiatives, including the new “Limit of Harmful Substances of Coatings” standard released on May 30, 2025 (effective June 1, 2026), strengthen controls on hazardous substances and encourage environmentally friendly packaging. The government’s crackdown on single-use plastics and over-packaging has created a favorable regulatory environment for sustainable cling wrap solutions.

Technological advancements focus on AI and “5G plus industrial internet” integration to enhance production efficiency and flexibility. Domestic manufacturing is being expanded to reduce dependency on imported technology, catering to growing demand from e-commerce, takeaway food, and food and beverage industries. China has also become a major hub for packaging innovation, generating a high number of patents for advanced materials and production methods, further positioning the country as a key player in the global cling wrap market.

Japan Cling Wrap Market Focused on Precision Manufacturing and High-Performance Eco-Friendly Films

Japan’s cling wrap industry is a cornerstone of its precision manufacturing ecosystem, with innovations such as cellulose nanofiber (CNF)-based flexible sheets by Oji Holdings in March 2025 targeting electronics and packaging applications. Regulatory guidance under the “Plastic Resource Circulation Act” (April 2022) promotes sustainable design and reduction of single-use plastics, influencing the industry toward biodegradable and recyclable materials.

Key players like Asahi Kasei, DIC Corporation, Berry Japan, and Nippon Paper Industries are driving innovation in high-performance cling wraps with enhanced dimensional stability, deformation resistance, and eco-friendly properties. Academic research complements industry efforts, exploring biopolymers and natural agents to create sustainable solutions. The Japanese market is increasingly focused on functionality, eco-consciousness, and high-quality packaging performance for both consumer and industrial applications.

Brazil Cling Wrap Market Accelerates with Sustainable Materials and Advanced Production Technologies

Brazil’s cling wrap market is guided by the National Solid Waste Policy and new legislation introduced in 2024, aiming to ban single-use disposable items and mandate fully recyclable or compostable packaging by 2030. States such as Paraiba and Pernambuco have established reverse logistics frameworks, holding producers accountable for end-of-life packaging management.

Technological advancements include robotics and AI for enhanced efficiency, automated sorting, and defect detection. Biodegradable films with low water vapor permeability, made from carboxymethyl cellulose (CMC) extracted from sugarcane bagasse, highlight innovation in sustainable materials. The food, beverage, and cosmetics sectors are major drivers, with growing demand for eco-friendly solutions in the expanding food processing industry. Governmental support and corporate investments in advanced machinery ensure adherence to recycling targets, efficiency improvements, and high-quality production, further promoting Brazil as a key emerging market in the global cling wrap industry.

Cling Wrap Market Report Scope

Cling Wrap Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$20.6 Billion

|

|

Market Size (2034)

|

$30.4 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Material Type (Polyethylene, Polyvinyl Chloride, Polyvinylidene Chloride, Bio-based materials, Other Materials), By Application (Household, Commercial), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Industrial & Logistics, Others), By Thickness (Up to 9 microns, 9 to 12 microns, Above 12 microns)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Berry Global Group, Inc., Reynolds Consumer Products Inc., Dow Inc., Amcor plc, SC Johnson, The Glad Products Company, Novolex Holdings, LLC, Wrapmaster, Asahi Kasei Corporation, Mitsubishi Chemical Holdings, MMP Corporation Ltd, Genpak, LLC, Sigma Plastics Group, Inteplast Group Corporation, Sealed Air

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cling Wrap Market Segmentation

By Material Type

- Polyethylene

- Polyvinyl Chloride

- Polyvinylidene Chloride

- Bio-based materials

- Other Materials

By Application

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Industrial & Logistics

- Others

By Thickness

- Up to 9 microns

- 9 to 12 microns

- Above 12 microns

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cling Wrap Market

- Berry Global Group, Inc.

- Reynolds Consumer Products Inc.

- Dow Inc.

- Amcor plc

- SC Johnson

- The Glad Products Company

- Novolex Holdings, LLC

- Wrapmaster

- Asahi Kasei Corporation

- Mitsubishi Chemical Holdings

- MMP Corporation Ltd

- Genpak, LLC

- Sigma Plastics Group

- Inteplast Group Corporation

- Sealed Air

* List Not Exhaustive

Methodology

The insights presented in this report on the global cling wrap market have been developed using a comprehensive research approach by USDAnalytics, combining both primary and secondary data sources to ensure accuracy and reliability. Primary research included in-depth interviews with industry stakeholders, including manufacturers, distributors, and end-users across household, commercial, and industrial segments, to capture current trends, technological innovations, and sustainability initiatives. Secondary research encompassed the analysis of corporate reports, regulatory publications, patent filings, press releases, and industry journals to map competitive strategies, material innovations, and market drivers. The research also examined regulatory frameworks across key regions such as North America, Europe, Asia-Pacific, and Latin America, focusing on food-contact compliance, extended producer responsibility, and environmental legislation. Advanced analytical techniques, including trend mapping, technology adoption assessment, and application-specific demand evaluation, were applied to identify emerging growth opportunities in bio-based polymers, high-barrier films, and antimicrobial wraps. The methodology further incorporated a detailed competitive landscape assessment, evaluating key players’ product portfolios, sustainability strategies, and market positioning. All findings have been synthesized to provide actionable intelligence for industry professionals seeking insights into material innovation, regulatory impact, and strategic growth avenues in the evolving cling wrap market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.