Market Overview: Rising Demand for Sustainable and High-Speed Flow Wrap Packaging

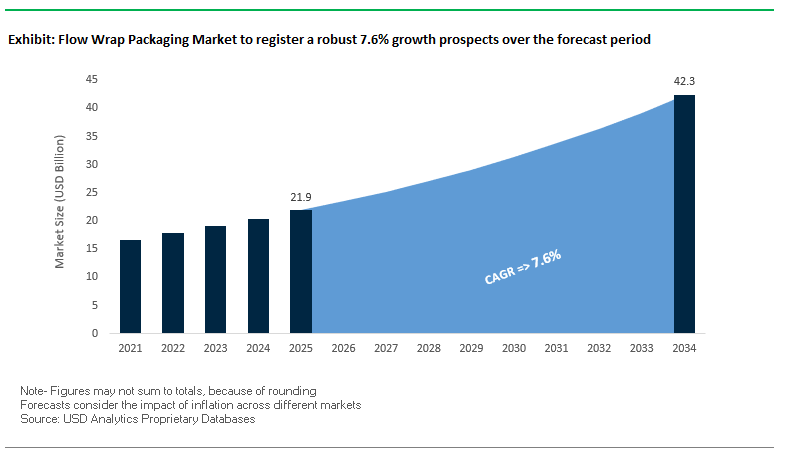

The Global Flow Wrap Packaging Market is projected to grow from USD 21.9 billion in 2025 to USD 42.3 billion by 2034, expanding at a robust CAGR of 7.6%. Flow wrap packaging, also known as horizontal form-fill-seal (HFFS), has become an essential packaging solution across the food, pharmaceutical, and consumer goods industries, offering lightweight, cost-efficient, and protective formats. Its popularity stems from its ability to deliver high-speed automation, reduced material usage, and superior product visibility, making it the preferred choice for both manufacturers and retailers.

A defining shift in the industry is the strong emphasis on sustainability, as companies innovate with recyclable films, compostable substrates, and post-consumer recycled (PCR) content. High-speed automation is another critical driver, with advanced machines now capable of packaging up to 1,400 products per minute, enabling brands to meet surging consumer demand efficiently.

The use of lightweight materials further strengthens the market’s sustainability proposition, as flow wrap uses less material than rigid alternatives, resulting in lower production costs, reduced freight expenses, and minimized carbon emissions. Moreover, the boom in e-commerce and direct-to-consumer channels is fueling the demand for flow wrap solutions that can withstand supply chain stresses while maintaining product integrity.

Key Insights for professionals and Buyers:

- Market to reach USD 42.3B by 2034 at 7.6% CAGR.

- Sustainability-driven innovation with recyclable and compostable films.

- Automation speeds reaching 1,400 packs per minute for high-volume industries.

- Lightweight designs reduce carbon footprint and shipping costs.

- E-commerce growth accelerates demand for resilient and protective packaging.

Market Analysis: Recent Developments in the Flow Wrap Packaging Industry

The Flow Wrap Packaging Market is witnessing rapid transformation, with new product launches, acquisitions, and infrastructure investments reinforcing its trajectory toward sustainability and advanced automation.

In September 2025, the Flexible Plastic Fund (FPF) released its FlexCollect report in the UK, which highlighted an 89% satisfaction rate for its at-home flexible plastic recycling initiative. This underscores industry momentum toward scalable recycling systems, directly impacting flow wrap packaging recovery. In August 2025, ProAmpac announced plans to acquire PAC Worldwide, expanding its presence in e-commerce protective packaging, where flow wrap is widely used. That same month, Amcor upgraded its Heanor, UK recycling facility, adding 2,800 tonnes of recyclate capacity annually, strengthening its closed-loop flexible packaging ecosystem.

Also in April 2025, Syntegon unveiled its Pack 103 flow wrapping machine, specifically designed for small and medium enterprises (SMEs), offering compact, efficient, and sustainable packaging capabilities. In March 2025, a sector report highlighted rising use of flow wrap in pharmaceutical single-dose medications, where precision, safety, and contamination control are critical.

On the innovation front, in October 2024, Klöckner Pentaplast introduced a lightweight recyclable flow wrap film with a lower carbon footprint, aligning with the circular economy agenda. That same month, the International Paper–DS Smith merger was approved, creating a paper-based packaging giant, likely to influence paper-alternative flow wrap solutions. Earlier in February 2024, PAC Machinery’s FW 650SI Flow Wrapper was shortlisted for the MHI Innovation Awards for its ability to work with both poly and paper-based substrates, highlighting dual-material compatibility as a growing sustainability trend.

Emerging Trends and High-Value Opportunities in the Flow Wrap Packaging Market

Strategic Shift to Monomaterial Polyolefin Films for Recyclability

The flow wrap packaging market is increasingly embracing monomaterial polyolefin films as manufacturers respond to brand sustainability commitments and Extended Producer Responsibility (EPR) regulations. By replacing multi-material laminates with high-performance polyethylene (PE) or polypropylene (PP) films, recyclability improves substantially, allowing packaging to be reintegrated into existing recycling streams. Publications by DNP highlight that multi-material packaging is challenging to separate, often resulting in incineration or landfill disposal. Collaborative efforts, such as the Cefic case study, demonstrate seven leading companies—including ExxonMobil, Hosokawa Alpine, and Henkel—developing a high-oxygen barrier pouch with over 95% mono-material content. The recycled output met or exceeded original performance standards, proving that sustainability need not compromise functionality. Regulatory frameworks like the European PPWR reinforce the market incentive, positioning monomaterial flow wrap films as a high-growth avenue. This trend is reshaping the supply chain, fostering collaboration between resin manufacturers, converters, and machinery producers, with a focus on films compatible with existing horizontal form-fill-seal (HFFS) lines.

Integration of Advanced Seal Integrity Technologies for Food Safety

To reduce food waste and maintain product integrity, there is growing adoption of flow wrap films with advanced sealant layers. Enhanced sealing technologies prevent contamination, leaks, and spoilage, which is crucial for extending shelf life and protecting brand reputation. PTI reports that conventional visual inspection methods often fail to detect micro-leaks, resulting in compromised product quality. Industry adoption includes non-contact ultrasonic technology capable of detecting defects down to 10-20 microns immediately after sealing, enabling real-time quality control and reducing defective output. Machinery providers like Schubert have developed unique sealing systems, including flying cross-sealing units and ultrasonic sealing, adaptable for mono-material and paper-based films. Brands prioritize high-performance flow wrap films with superior seal integrity, creating a growth avenue in food and beverage packaging and reducing recall risks.

Development of High-Speed, Compatible Paper-Based Flow Wrap Alternatives

There is a significant opportunity to develop paper-based substrates with sufficient thermal, tensile, and barrier properties to run on existing HFFS machinery. This enables brands and converters to transition to renewable materials without extensive capital investment. As highlighted by WestRock, heat-sealable kraft paper can run at high speeds, providing a recyclable alternative to traditional poly mailers. Mondi’s re/cycle FunctionalBarrier Papers offer mechanical strength, grease and water vapor barriers, and heat sealability, demonstrating paper-based films’ viability in automated processes. Commercializing such solutions allows manufacturers to appeal to environmentally conscious consumers and aligns with corporate sustainability goals. This opportunity fosters collaboration between paper manufacturers, material science firms, and machinery providers, creating a more interconnected, circular value chain.

Incorporation of Digital Watermarking for Intelligent Sorting and Traceability

The adoption of digital watermarks (e.g., HolyGrail 2.0) presents a dual opportunity: precise automated sorting of post-consumer flexible packaging and enhanced supply chain traceability. Watermarks carry information on material type, composition, and usage, enabling high-speed, granular sorting in recycling facilities. Pellenc ST reports that sorting lines equipped with high-resolution cameras can accurately read these codes, vastly improving recycling output quality. Industrial trials, such as those in Germany under HolyGrail 2.0, detected 5.66 million instances across 5,949 SKUs with efficiency ranging from 87.9% to 93.8%, demonstrating the technology’s real-world effectiveness. This innovation helps brands meet recycling targets, separate food-grade from non-food-grade materials, and unlock higher-value recycled streams. Implementation requires close collaboration among flow wrap packaging manufacturers, technology providers like Digimarc, and waste management firms, creating a more circular and data-driven packaging ecosystem.

Competitive Landscape: Key Players Driving the Flow Wrap Packaging Market

The Flow Wrap Packaging Market is highly competitive, with leading equipment manufacturers and packaging companies leveraging automation, sustainability, and technological innovation to expand market share.

Syntegon Technology GmbH introduces Pack 103 for SMEs

Syntegon, formerly Bosch Packaging, is a global leader in food and pharmaceutical packaging systems. In April 2025, it launched the Pack 103 flow wrapping machine for SMEs, expanding its reach in mid-scale automation. Syntegon also offers the paper-ON-form retrofit kit, enabling paper-based packaging on existing lines without speed loss. Its Sigpack RN and Sigpack TTMP machines highlight its expertise in high-speed, hygienic flow wrapping.

ULMA Packaging expands sustainable Pack Eco line

ULMA Packaging is known for its versatile, eco-friendly flow wrapping solutions. The company recently expanded its high-speed automated flow wrappers with multi-lane configurations. Its Pack Eco line pioneers paper-based flow wrapping, reducing film usage. With a brand motto “better packaging, better world,” ULMA focuses on user-friendly machines with fast changeovers and sustainable integration.

FUJI Machinery achieves speeds up to 1,400 packs per minute

FUJI Machinery, a Japanese leader in packaging, has built a reputation for durable, high-speed flow wrapping machines. Its equipment can handle 1,400 packs per minute, making it ideal for large-scale confectionery, bakery, and pharmaceutical operations. Its RECLO-SURE solution reduces plastic usage by half in meat and cheese packaging. FUJI integrates multi-servo drives and precision temperature controls, ensuring accuracy and efficiency.

PFM Packaging Machinery pioneers MAP technology

Italy-based PFM Packaging Machinery brings over 60 years of expertise, offering flow wrappers ranging from 10 to 300+ packs per minute. It has been a pioneer in Modified Atmosphere Packaging (MAP), essential for fresh food preservation. PFM also provides customer innovation centers for product testing, emphasizing its partnership-driven strategy.

IMA Group delivers compact, energy-efficient flow wrappers

IMA Group is a global leader in packaging machinery across food, pharmaceuticals, and cosmetics. It has launched compact, energy-efficient flow wrappers, such as the IMA FB8, known for speed and integration with weight-checkers. IMA’s systems are increasingly automated with robotics, enabling sustainability and precision at scale, reinforcing its leadership in advanced packaging technology.

Flow Wrap Packaging Market Share Insights

Horizontal Flow Wrap Dominates Market Share by Packaging Type in Flow Wrap Packaging

Horizontal flow wrapping leads the flow wrap packaging market with 55% share in 2025, reflecting its unmatched efficiency in packaging pre-formed, rigid, or semi-rigid products at extremely high speeds. This technology is indispensable for confectionery, bakery, frozen foods, and medical device kits, where products are already structured and only require a protective, tamper-evident wrapper. Its dominance is reinforced by its ability to deliver tight, uniform seals at high throughput, ensuring product freshness while reducing packaging waste per unit. By contrast, Vertical Form Fill Seal (VFFS) systems, while accounting for nearly the rest of the market, stand out for versatility—forming, filling, and sealing directly from rollstock to package nuts, powders, snacks, and pet food. This balance between high-volume efficiency in horizontal lines and versatility in vertical systems defines the competitive dynamics of the packaging type segment.

Food and Beverages Anchor Market Share by End-Use Industry in Flow Wrap Packaging

The food and beverage industry accounts for 70% of end-use share in the flow wrap packaging market, underscoring its role as the principal growth engine. Flow wrapping is the default technology for packaging everything from chocolate bars, biscuits, and noodles to frozen pizzas and pasta packs. Its high-speed capability ensures efficiency on mass production lines, while its ability to preserve freshness and offer tamper evidence addresses both regulatory and consumer demands. Pharmaceuticals and healthcare, representing 15% share, are the most specification-driven segment, where flow wrapping secures sterile medical kits, diagnostic strips, and blister packs under stringent FDA and GMP standards. Pet food adds further demand momentum through the adoption of VFFS systems for kibble and treats, while cosmetics, personal care, and industrial goods remain niche users of the technology. Collectively, these dynamics demonstrate how food and beverages dominate volume, pharmaceuticals drive compliance-driven value, and pet food sustains growth through packaging versatility.

United States Flow Wrap Packaging Market Strengthened by EPR Regulations and Mono-Material Innovations

The U.S. flow wrap packaging market is shaped by a fragmented regulatory environment, with Extended Producer Responsibility (EPR) laws increasingly shifting recycling and waste management costs from taxpayers to manufacturers. This regulatory evolution is fostering sustainable packaging practices and innovations that reduce environmental impact. Technological advancements such as mono-material films for pouches, which are easier to recycle, are gaining traction. Notably, Amcor launched its AmFiber Performance Paper in North America, a high-barrier, recyclable laminated paper compatible with existing flow wrap machinery.

Corporate investments are accelerating market growth. Amcor’s planned acquisition of Berry Global Group, expected to close in mid-2025, will consolidate capabilities with $180 million in annual R&D focused on sustainable packaging solutions. Demand remains particularly strong in food and beverages, e-commerce, and direct-to-consumer segments, where lightweight, robust, and protective flow wrap solutions are essential. Sustainability continues to be a central business focus, with bio-based films and recyclable paperboard meeting growing consumer expectations for eco-friendly packaging.

Germany Flow Wrap Packaging Market Accelerates with Circular Economy Leadership and Advanced Machines

Germany’s flow wrap packaging market operates under strict regulations, including the EU Packaging and Packaging Waste Regulation (PPWR), which mandates fully recyclable or reusable packaging by 2030 and restricts hazardous chemicals such as PFAS. The market is responding with technological innovation, exemplified by Syntegon’s SVX Agile vertical packaging machine showcased at Fachpack, capable of handling all common bag types, including paper-based and mono-material films, aligning with sustainable production goals.

Germany’s Packaging Act (VerpackG) reinforces circular economy practices by incentivizing designs that enhance recyclability through modulated fees. The food, beverage, and personal care sectors are particularly strong markets, with consumer preference for premium, sustainable products driving demand for high-barrier films that extend shelf life. Innovation and regulatory compliance position Germany as a leader in sustainable flow wrap packaging in Europe.

China Flow Wrap Packaging Market Expands Through Dual Carbon Initiatives and Domestic Production

China’s flow wrap packaging market is driven by the government’s “dual carbon” goals and policies promoting green industrial transformation. Regulatory reforms such as the revised national standard GB/T 31268, effective November 2024, limit excessive packaging by defining maximum layers and void ratios, directly affecting e-commerce and consumer goods packaging.

Technological advancements include automation and AI integration, with “5G plus industrial internet” optimizing production efficiency and flexible manufacturing capacity. Local companies are increasingly substituting imported technology, expanding domestic production to meet growing demand for high-quality, circular packaging. The rapid expansion of domestic e-commerce, food delivery, and food and beverage sectors is fueling demand for flow wrap packaging that is sustainable, durable, and capable of maintaining product freshness during transit.

India Flow Wrap Packaging Market Grows with Circular Economy Policies and Frozen Food Demand

India’s flow wrap packaging market is supported by government initiatives promoting a circular economy, including the Food Safety and Standards (Packaging) Regulations, 2018, which enforce food-grade material requirements. Automation adoption is increasing, with companies developing efficient solutions for a variety of applications, particularly in frozen and packaged foods, including snacks and vegetables.

Corporate investments are expanding domestic manufacturing capacity, with UFlex operating large plants in Noida and Jammu. Key applications include food and beverage, and personal care packaging, driven by rising e-commerce penetration and consumer demand for sustainable solutions. The “Make in India” initiative further encourages local technological development, positioning India as a growing hub for modern, high-performance flow wrap packaging.

Japan Flow Wrap Packaging Market Innovates Through Recycled Films and High-Performance Solutions

Japan’s flow wrap packaging industry benefits from advanced manufacturing technologies and regulatory guidance from the Plastic Resource Circulation Act (April 2022), which promotes environmentally conscious designs and limits single-use plastics. Developments such as the recycled BOPP film created by Toppan Inc., RM Tohcello Co. Ltd., and Mitsui Chemicals Inc. in September 2024 highlight Japan’s emphasis on sustainable packaging materials.

High-performance films with superior barrier properties and integrated IoT sensors are becoming standard, while functionality innovations such as easy-open tear notches and resealable closures cater to aging populations and single-person households. Japan’s focus on sustainability, material performance, and technological innovation ensures continued growth and leadership in the Asia-Pacific flow wrap packaging market.

Brazil Flow Wrap Packaging Market Accelerates with Sustainable Materials and Digital Innovations

Brazil’s flow wrap packaging market is advancing through government-driven sustainable waste management practices, including amendments to the National Solid Waste Policy in January 2025 to restrict imports and encourage domestic recycling. Technological innovation is a major driver, with robotics and AI being applied to improve efficiency, quality control, automated label selection, and defect detection.

The market is witnessing a shift toward premium and specialized digital packaging solutions, enabling extended shelf life while maintaining product freshness and quality. Sustainable material development is accelerating, as demonstrated by Klabin’s introduction of EkoFlex, its first flexible packaging paper for multiple industries, highlighting Brazil’s growing commitment to eco-friendly flow wrap packaging.

Flow Wrap Packaging Market Report Scope

Flow Wrap Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.9 Billion

|

|

Market Size (2034)

|

$42.3 Billion

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Packaging Type (Horizontal Flow Wrap, Vertical Form Fill Seal), By Material Type (Plastic Films, Paper, Aluminum Foil), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Industrial Goods, Pet Food)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Syntegon Technology GmbH, Coesia S.p.A., FUJI Packaging, PFM Packaging Machinery S.p.A., ULMA Packaging, Omori Machinery Co., Ltd., IMA S.p.A., Sonoco Products Company, Sealed Air Corporation, UFlex Ltd., Constantia Flexibles Group, Berry Global Group, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flow Wrap Packaging Market Segmentation

By Packaging Type

- Horizontal Flow Wrap

- Vertical Form Fill Seal

By Material Type

- Plastic Films

- Paper

- Aluminum Foil

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Industrial Goods

- Pet Food

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flow Wrap Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Syntegon Technology GmbH

- Coesia S.p.A.

- FUJI Packaging

- PFM Packaging Machinery S.p.A.

- ULMA Packaging

- Omori Machinery Co., Ltd.

- IMA S.p.A.

- Sonoco Products Company

- Sealed Air Corporation

- UFlex Ltd.

- Constantia Flexibles Group

- Berry Global Group, Inc.

* List Not Exhaustive

Methodology

USDAnalytics adopted a robust, multi-step research methodology to provide a detailed and actionable analysis of the Global Flow Wrap Packaging Market. Our approach integrated extensive primary research, including interviews with industry stakeholders such as packaging manufacturers, machinery suppliers, converters, and sustainability experts, alongside secondary research from company reports, regulatory filings, trade journals, and industry publications. Market sizing and forecasts were calculated based on packaging type (horizontal flow wrap, vertical form-fill-seal), material type (plastic films, paper, aluminum foil), and end-use industry (food & beverages, pharmaceuticals, personal care, industrial goods, pet food). Key trends including sustainability initiatives, mono-material films, advanced seal integrity technologies, high-speed automation, and digital watermarking for recycling and traceability were thoroughly analyzed. Regional market dynamics across the U.S., Germany, China, India, Japan, and Brazil were assessed to reflect local regulatory frameworks, technological adoption, and corporate investments. Competitive analysis focused on leading players like Syntegon, FUJI Machinery, ULMA, Amcor, and Mondi, highlighting mergers, acquisitions, and product innovations that drive market growth. This methodology ensures industry professionals, investors, and decision-makers gain a comprehensive, data-driven understanding of market opportunities, challenges, and future growth avenues.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.